|

시장보고서

상품코드

1959573

산업용 라벨 프린터 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Industrial Label Printer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

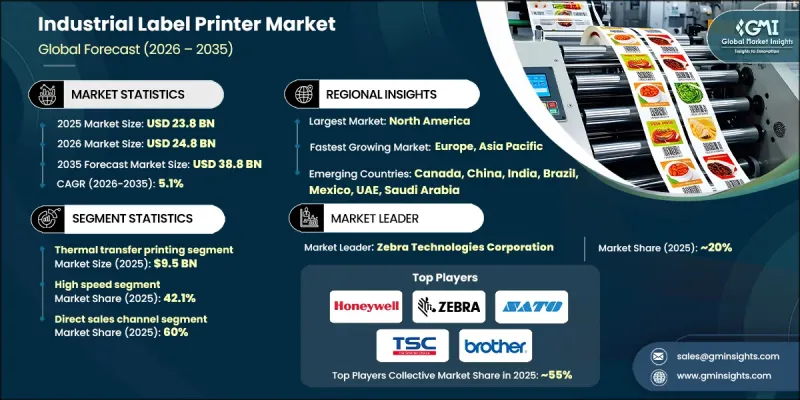

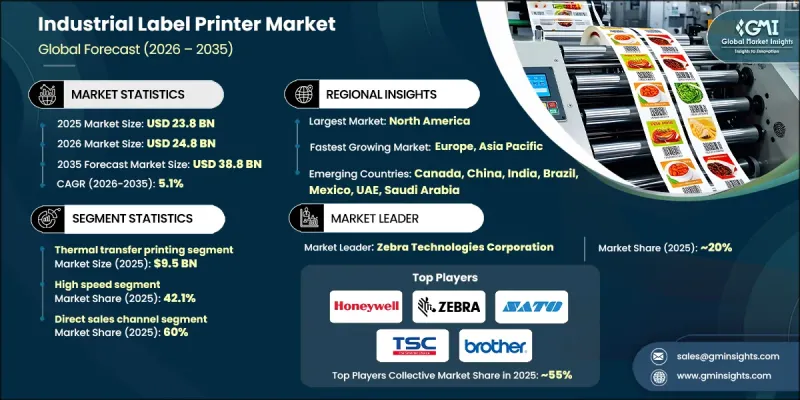

세계의 산업용 라벨 프린터 시장은 2025년에 238억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 5.1%로 성장하여 388억 달러에 이를 것으로 예측됩니다.

시장 성장은 생산 환경 전반에 걸쳐 산업 자동화 및 디지털 제조 기법의 도입이 가속화되고 있는 것과 관련이 있습니다. 제조업체들이 사업 규모를 확장하고 시설을 현대화함에 따라 일관된 품질, 운영 안정성, 장기적인 내구성을 제공하는 라벨링 시스템에 대한 수요가 증가하고 있습니다. 산업용 라벨 프린터는 자동화된 생산 생태계의 필수 인프라로 인식되고 있으며, 식별 정확도, 자산 가시성, 효율적인 워크플로우 관리를 지원하고 있습니다. 커넥티드 제조 환경으로의 전환은 데이터 기반 시스템 및 실시간 모니터링 플랫폼과 통합되는 지능형 라벨링 솔루션의 필요성을 더욱 높이고 있습니다. 생산량이 증가하고 품질에 대한 요구가 강화됨에 따라 제조업체들은 산업 운영의 효율성, 정확성, 추적성을 향상시킬 수 있는 첨단 인쇄 기술에 투자할 수밖에 없는 상황입니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 238억 달러 |

| 예측 금액 | 388억 달러 |

| CAGR | 5.1% |

열전사 인쇄 부문은 2025년 95억 달러 시장 규모를 기록할 것으로 예상되며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 5%를 나타낼 것으로 예측됩니다. 이 인쇄 방식은 열악한 환경 조건에서도 성능을 유지하는 고화질 라벨을 생산할 수 있기 때문에 널리 채택되고 있습니다. 내구성은 장기적인 식별 및 컴플라이언스 요구 사항을 지원하며, 규제 분야 및 고성능 산업 응용 분야에서 지속적으로 수요를 주도하고 있습니다.

고속 산업용 라벨 프린터 부문은 2025년 42.1%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 5.7%의 성장률을 보일 것으로 예측됩니다. 생산 속도 향상과 납기 단축에 대한 요구로 인해 다운타임을 최소화하면서 정밀도를 유지할 수 있는 고출력 프린터의 채택이 촉진되고 있습니다. 물류 집약적 운영의 주문량 증가는 이 부문의 선도적 지위를 더욱 공고히 하고 있습니다.

미국 산업용 라벨 프린터 시장은 2025년 76억 달러에 달할 것으로 예상되며, 2026년부터 2035년까지 연평균 4.9%의 성장률을 보일 것으로 전망됩니다. 시장 확대는 첨단 제조 능력, 탄탄한 물류 인프라, 산업용 라벨링 솔루션에 의존하는 통합 자동화 시스템 활용 확대에 힘입은 바 큽니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 인쇄 기술별, 2022-2035

제6장 시장 추산 및 예측 : 자동화 레벨별, 2022-2035

제7장 시장 추산 및 예측 : 속도별, 2022-2035

제8장 시장 추산 및 예측 : 접속 방식별, 2022-2035

제9장 시장 추산 및 예측 : 최종 용도별, 2022-2035

제10장 시장 추산 및 예측 : 유통 채널별, 2022-2035

제11장 시장 추산 및 예측 : 지역별, 2022-2035

제12장 기업 개요

LSH 26.03.18The Global Industrial Label Printer Market was valued at USD 23.8 billion in 2025 and is estimated to grow at a CAGR of 5.1% to reach USD 38.8 billion by 2035.

Market growth is linked to the accelerating adoption of industrial automation and digital manufacturing practices across production environments. As manufacturers scale operations and modernize facilities, demand is rising for labeling systems that deliver consistent quality, operational reliability, and long-term durability. Industrial label printers are increasingly viewed as essential infrastructure within automated production ecosystems, supporting identification accuracy, asset visibility, and streamlined workflow management. The shift toward connected manufacturing environments has further increased the need for intelligent labeling solutions that integrate with data-driven systems and real-time monitoring platforms. Growing production volumes and stricter quality expectations are pushing manufacturers to invest in advanced printing technologies that enhance efficiency, precision, and traceability across industrial operations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $23.8 Billion |

| Forecast Value | $38.8 Billion |

| CAGR | 5.1% |

The thermal transfer printing segment generated USD 9.5 billion in 2025 and is expected to grow at a CAGR of 5% from 2026 to 2035. This printing method is widely adopted due to its ability to produce high-clarity labels that maintain performance under demanding environmental conditions. Its durability supports long-term identification and compliance requirements, which continue to drive demand across regulated and high-performance industrial applications.

The high-speed industrial label printers segment accounted for 42.1% share in 2025 and is forecast to grow at a CAGR of 5.7% through 2035. Increasing production speeds and shorter fulfillment cycles are encouraging the adoption of high-output printers capable of maintaining accuracy while minimizing downtime. Rising order volumes across logistics-intensive operations further reinforce this segment's leadership.

U.S. Industrial Label Printer Market reached USD 7.6 billion in 2025 and is projected to grow at a CAGR of 4.9% from 2026 to 2035. Market expansion is supported by advanced manufacturing capabilities, strong logistics infrastructure, and increasing use of integrated automation systems that rely on industrial-grade labeling solutions.

Key companies operating in the Global Industrial Label Printer Market include Zebra Technologies Corporation, Honeywell International Inc., SATO Holdings Corporation, Avery Dennison Corporation, Brady Corporation, Toshiba Tec Corporation, Seiko Epson Corporation, Brother Industries, Ltd., Printronix, LLC, TSC Auto ID Technology Co., Ltd., Datalogic S.p.A., Oki Electric Industry Co., Ltd., Godex International Co., Ltd., Wasp Barcode Technologies, and Primera Technology, Inc. Companies in the industrial label printer market are strengthening their market positions through continuous technology enhancement and portfolio diversification. Many players are focusing on high-speed, high-resolution printing capabilities that support automated and data-driven production environments. Integration with enterprise software platforms and smart factory systems is a key strategic priority. Manufacturers are also investing in ruggedized designs and energy-efficient technologies to improve lifecycle value. Strategic partnerships with logistics providers and industrial solution integrators are expanding market reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Print technology

- 2.2.3 Automation level

- 2.2.4 Speed

- 2.2.5 Connectivity

- 2.2.6 End use

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of manufacturing and industrial automation

- 3.2.1.2 Rapid growth in logistics, warehousing, and e-commerce

- 3.2.1.3 Increasing focus on product traceability and serialization

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Dependence on consumables and price volatility

- 3.2.2.2 Intense price competition and margin pressure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By print technology

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Print Technology, 2022 - 2035, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Thermal transfer printing

- 5.3 Direct thermal printing

- 5.4 Laser printing

- 5.5 Inkjet printing

- 5.6 Specialty printing technologies

Chapter 6 Market Estimates & Forecast, By Automation Level, 2022 - 2035, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Semi-automated

- 6.4 Fully automated

Chapter 7 Market Estimates & Forecast, By Speed, 2022 - 2035, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Low speed

- 7.3 High speed

- 7.4 Mid speed

Chapter 8 Market Estimates & Forecast, By Connectivity, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Wired

- 8.2.1 USB

- 8.2.2 Ethernet

- 8.2.3 Serial

- 8.3 Wireless

- 8.3.1 Wi-Fi

- 8.3.2 Bluetooth

- 8.3.3 NFC

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Consumer good & home care

- 9.3 Healthcare and pharmaceuticals

- 9.4 Chemical and hazardous materials

- 9.5 Food and beverage

- 9.6 Automotive and aerospace

- 9.7 Electronics

- 9.8 Textile and apparel

- 9.9 Others

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Indonesia

- 11.4.7 Malaysia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Avery Dennison Corporation

- 12.2 Brady Corporation

- 12.3 Brother Industries, Ltd.

- 12.4 Datalogic S.p.A.

- 12.5 Godex International Co., Ltd.

- 12.6 Honeywell International Inc.

- 12.7 Oki Electric Industry Co., Ltd.

- 12.8 Primera Technology, Inc.

- 12.9 Printronix, LLC

- 12.10 SATO Holdings Corporation

- 12.11 Seiko Epson Corporation

- 12.12 Toshiba Tec Corporation

- 12.13 TSC Auto ID Technology Co., Ltd.

- 12.14 Wasp Barcode Technologies

- 12.15 Zebra Technologies Corporation