|

시장보고서

상품코드

1959584

식품 산업용 로봇 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Food Robotics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

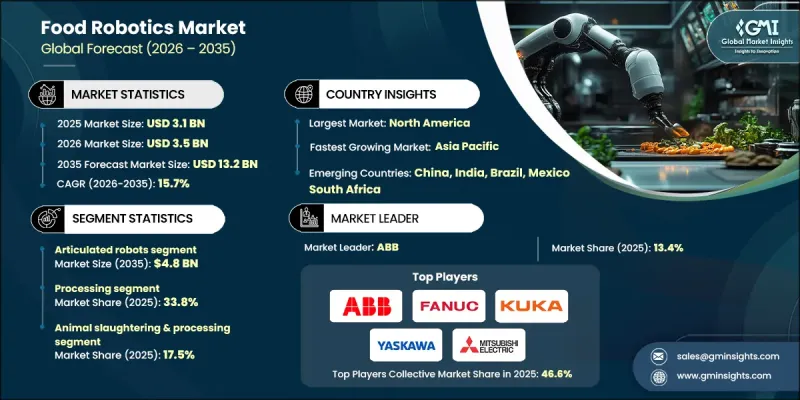

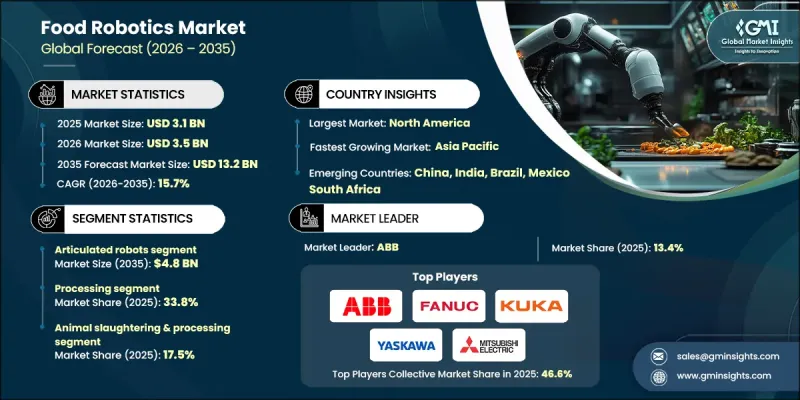

세계의 식품 산업용 로봇 시장은 2025년에 31억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 15.7%로 성장하여 132억 달러에 이를 것으로 예측됩니다.

이 산업의 성장은 노동력 부족, 신선식품의 정밀한 취급에 대한 수요 증가, 가공식품 및 즉석식품의 소비 증가에 의해 주도되고 있습니다. 급속한 도시화와 소비자 라이프스타일의 변화로 인해 간편식에 대한 수요가 증가하고 있으며, 기업들은 가공, 선별, 포장을 위한 고속 자동화에 대한 투자를 촉진하고 있습니다. 식품 산업용 로봇 기술은 고정식 단일 작업 기계에서 AI와 머신 비전을 탑재한 지능형 시스템으로 진화하고 있습니다. 이를 통해, 대규모 재프로그래밍 없이 원자재 변동에 실시간으로 적응할 수 있게 되었습니다. 현재는 생산부터 포장까지 전 공정을 관리하는 엔드투엔드 로봇 솔루션이 도입되어 효율성, 식품 안전, 위생 상태를 향상시키면서 운영비용을 절감하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 31억 달러 |

| 예측 금액 | 132억 달러 |

| CAGR | 15.7% |

델타/병렬 로봇 부문은 2025년 7억 5,580만 달러로 평가되었고, 2035년까지 연평균 17.2% 성장할 것으로 예측됩니다. 이 로봇은 정확성, 빠른 반응성, 섬세한 식품을 최소한의 손상으로 취급할 수 있는 능력으로 인해 고속 픽앤 플레이스 작업에 점점 더 많이 활용되고 있습니다. 신선식품, 과자, 베이커리 제품 등 섬세한 제품 취급에 적용되어 자동화된 식품 환경에서의 도입을 촉진하고 있습니다.

2025년 기준 가공 분야가 33.8%의 점유율을 차지했습니다. AI 탑재 로봇은 식품 절단, 분량 조절, 혼합, 조립 등 반복적, 고위험, 노동집약적인 작업에서 활용이 확대되고 있습니다. 도입으로 생산의 일관성, 위생 기준, 전반적인 업무 효율성을 향상시키는 동시에 위험한 작업에 대한 인적 접촉을 줄일 수 있습니다. 이러한 추세는 대규모 식품 제조 및 포장 시설에서의 도입을 가속화하고 있습니다.

북미 식품 산업용 로봇 시장은 2025년 36%의 점유율을 차지했습니다. 이 지역은 첨단 제조 인프라, 높은 인건비, 엄격한 식품 안전 규제로 인해 자동화가 전략적으로 필요한 지역입니다. 북미는 육류, 유제품, 베이커리, 포장식품 분야에서 로봇 기술을 선도적으로 도입하여 생산 최적화, 노동력 의존도 감소, 엄격한 위생 및 품질 기준 준수를 위해 로봇 기술을 활용하고 있습니다. 로봇 기술의 조기 도입으로 이 지역은 AI 통합형 식품 자동화 기술의 트렌드 세터로 자리매김하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 로봇 유형별, 2022-2035

제6장 시장 추산 및 예측 : 기능별, 2022-2035

제7장 시장 추산 및 예측 : 최종 용도별, 2022-2035

제8장 시장 추산 및 예측 : 지역별, 2022-2035

제9장 기업 개요

LSH 26.03.18The Global Food Robotics Market was valued at USD 3.1 billion in 2025 and is estimated to grow at a CAGR of 15.7% to reach USD 13.2 billion by 2035.

The industry's growth is driven by labor shortages, increasing demand for precise handling of perishable products, and the rising consumption of processed and ready-to-eat foods. Rapid urbanization and changing consumer lifestyles are increasing demand for convenience foods, prompting companies to invest in high-speed automation for processing, sorting, and packaging. Food robotics is evolving from fixed, single-task machines to intelligent systems equipped with AI and machine vision, capable of adapting in real time to variations in ingredients without extensive reprogramming. End-to-end robotic solutions are now being deployed to manage the entire production and packaging workflow, improving efficiency, food safety, and hygiene while reducing operational costs.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.1 Billion |

| Forecast Value | $13.2 Billion |

| CAGR | 15.7% |

The delta/parallel robots segment was valued at USD 755.8 million in 2025 and is forecasted to grow at a CAGR of 17.2% through 2035. These robots are increasingly utilized for high-speed pick-and-place operations due to their precision, rapid response, and ability to handle delicate food items with minimal damage. Their application in sensitive product handling such as fresh produce, confectionery, and bakery items is driving adoption in automated food environments.

The processing segment accounted for 33.8% share in 2025. AI-enabled robots are increasingly being used in repetitive, high-risk, and labor-intensive operations such as cutting, portioning, mixing, and assembling food products. Their deployment enhances production consistency, hygiene standards, and overall operational efficiency, while also reducing human exposure to potentially hazardous tasks. This trend is accelerating adoption across large-scale food manufacturing and packaging facilities.

North America Food Robotics Market held a 36% share in 2025. The region benefits from advanced manufacturing infrastructure, high labor costs, and strict food safety regulations, making automation a strategic necessity. North America leads adoption in meat, dairy, bakery, and packaged food sectors, leveraging robotics to optimize production, reduce labor dependency, and maintain compliance with stringent hygiene and quality standards. Early adoption of robotics has positioned the region as a trendsetter in AI-integrated food automation technologies.

Key players in the Global Food Robotics Market include ABB, FANUC, KUKA, Yaskawa Electric, Mitsubishi Electric, Universal Robots, OMRON, and Staubli. Companies in the Food Robotics Market are implementing strategies to strengthen their market position by investing in AI-driven automation, machine vision, and adaptive robotics capable of handling diverse food items in real time. They are forming strategic alliances with food manufacturers and integrators to enable faster deployment and ensure compatibility with existing production lines. Product diversification, including robotic solutions for packaging, processing, and material handling, allows companies to address multiple food segments. Expansion into emerging markets with rising automation demand is a key growth tactic. Additionally, continuous R&D to improve speed, precision, and hygiene compliance ensures that firms maintain a competitive edge and meet evolving regulatory standards while supporting scalable production.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Robot type trends

- 2.2.2 Function trends

- 2.2.3 End-use application trends

- 2.2.4 Regional trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising automation adoption in food processing and packaging

- 3.2.1.2 Regulatory pressure for traceability and quality compliance

- 3.2.1.3 Increasing consumption of processed and ready-to-eat foods

- 3.2.1.4 Expansion of smart factories and Industry 4.0 adoption

- 3.2.1.5 Acute labor shortages and the need for gentle, high-precision handling of perishable produce

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial capital investment and implementation costs

- 3.2.2.2 Technical complexity and integration challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in ready-to-eat and processed food segments

- 3.2.3.2 Growing adoption of AI and machine vision in robotics

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Emerging business models

- 3.8 Compliance requirements

- 3.9 Patent and IP analysis

- 3.10 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Robot Type, 2022 - 2035 ($ Mn & Units)

- 5.1 Key trends

- 5.2 Articulated robots

- 5.3 Scara robots

- 5.4 Delta/parallel robots

- 5.5 Cartesian/gantry robots

- 5.6 Collaborative robots (cobots)

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Function, 2022 - 2035 ($ Mn & Units)

- 6.1 Key trends

- 6.2 Processing

- 6.3 Packaging

- 6.4 Palletizing & depalletizing

- 6.5 Inspection & quality control

- 6.6 Material handling & logistics

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By End-use Application, 2022 - 2035 ($ Mn & Units)

- 7.1 Key trends

- 7.2 Animal food manufacturing

- 7.3 Grain & oilseed milling

- 7.4 Sugar & confectionery

- 7.5 Fruit & vegetable preserving

- 7.6 Dairy product manufacturing

- 7.7 Animal slaughtering & processing

- 7.8 Seafood product preparation

- 7.9 Bakeries & tortilla manufacturing

- 7.10 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 ABB

- 9.1.2 FANUC

- 9.1.3 KUKA

- 9.1.4 Yaskawa Electric

- 9.2 Regional Key Players

- 9.2.1 North America

- 9.2.1.1 Rockwell Automation

- 9.2.1.2 Key Technology (Duravant)

- 9.2.1.3 Miso Robotics

- 9.2.2 Europe

- 9.2.2.1 Universal Robots

- 9.2.2.2 Staubli

- 9.2.2.3 Buhler Group

- 9.2.3 APAC

- 9.2.3.1 Mitsubishi Electric

- 9.2.3.2 OMRON

- 9.2.3.3 Nachi-Fujikoshi

- 9.2.1 North America

- 9.3 Niche Players / Disruptors

- 9.3.1 Mayekawa

- 9.3.2 Marel