|

시장보고서

상품코드

1959606

비페닐 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Biphenyl Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

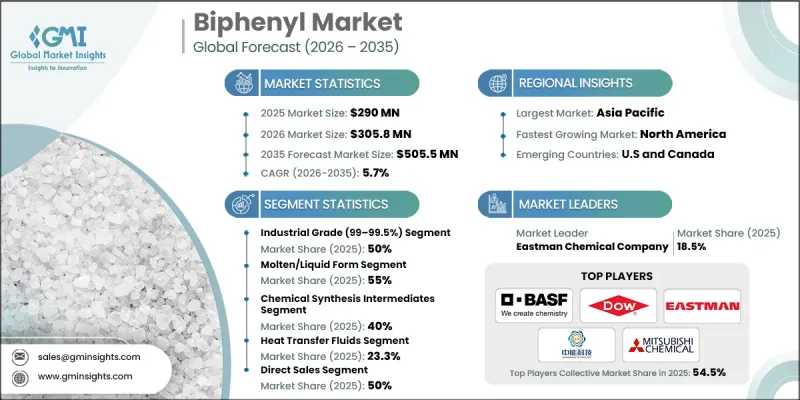

세계의 비페닐 시장은 2025년에 2억 9,000만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 5.7%로 성장하여 5억 550만 달러에 이를 것으로 예측됩니다.

시장 성장은 특수 화학제품 제조에서 비페닐에 대한 수요 증가에 의해 주도되고 있습니다. 제약 및 농약 분야는 고순도 중간체에 대한 의존도가 높아지고 있으며, 비페닐은 복잡한 분자 배합에서 중요한 구성 요소입니다. 화학물질의 순도와 성능에 대한 규제 요건이 강화됨에 따라 안정성과 예측 가능한 결과 때문에 비페닐계 화합물의 채택이 촉진되고 있습니다. 또 다른 중요한 촉진요인은 비페닐을 열 매체 및 산업용 용매로 사용하는 것이 확대되고 있다는 점입니다. 우수한 열 안정성과 용해성은 특히 석유화학 및 자동차 분야의 고성능 산업 응용 분야에 이상적입니다. 환경 및 규제 고려 사항도 비페닐의 채택을 촉진하고 있으며, 비페닐의 명확한 안전 프로파일과 예측 가능한 거동은 코팅, 접착제, 플라스틱 및 기타 규제 대상 응용 분야에 적합합니다. 전반적으로, 시장은 산업 회복, 에너지 효율화 이니셔티브, 신뢰할 수 있고 규정을 준수하는 화학 솔루션에 대한 수요와 함께 혜택을 받고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 2억 9,000만 달러 |

| 예측 금액 | 5억 550만 달러 |

| CAGR | 5.7% |

기술 등급 비페닐 부문은 고급 및 고성능 응용 분야에서 저순도 제품에서 고순도 비페닐로의 대체가 진행됨에 따라 2035년까지 연평균 4.1%의 성장률을 보일 것으로 예측됩니다. 엄격한 품질 기준과 강화된 화학적 성능을 필요로 하는 산업에서는 우수한 안정성, 균일성, 반응성을 제공하는 초순수 등급이 선호됩니다. 이러한 변화로 인해 절대 순도가 중요하지 않은 비교적 단순한 용도에 주로 사용되는 산업용 비페닐에 대한 수요가 제한되고 있습니다.

고체 비페닐 부문은 의약품, 농약, 특수화학제품 생산에 광범위하게 적용되어 2025년 45%의 점유율을 차지할 것으로 예측됩니다. 그 인기는 CAGR 5.4%의 꾸준한 출하량 증가로 뒷받침되고 있습니다. 고체 비페닐은 취급 용이성, 정밀한 투여 능력, 안정된 저장 특성 등 여러 가지 운영상의 이점을 제공하여 제어되고 일관된 화학적 성능이 요구되는 응용 분야에 이상적인 선택이 될 수 있습니다.

북미 비페닐 시장은 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 6.7%를 나타낼 것으로 예측됩니다. 이 지역은 성숙하고 고도로 규제된 시장이며, 수요는 주로 의약품 제조, 특수 화학물질 제조 및 열 매체와 같이 이미 확립된 용도에 집중되어 있습니다. 이 지역의 성장은 비교적 안정적이며, 주로 규제 준수, 점진적인 기술 업그레이드, 일관된 고품질 제품의 필요성에 의해 주도되고 있습니다. 북미에서의 경쟁적 차별화는 제품 성능과 신뢰성을 향상시키는 응용 개발 혁신, 지속 가능한 제조 방법, 고도의 정제 공정과 같은 요소에 의해 점점 더 많이 형성되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 순도 등급별, 2022-2035

제6장 시장 추산 및 예측 : 제품 유형별, 2022-2035

제7장 시장 추산 및 예측 : 용도별, 2022-2035

제8장 시장 추산 및 예측 : 최종 이용 산업별, 2022-2035

제9장 시장 추산 및 예측 : 유통 채널별, 2022-2035

제10장 시장 추산 및 예측 : 지역별, 2022-2035

제11장 기업 개요

LSH 26.03.16The Global Biphenyl Market was valued at USD 290 million in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 505.5 million by 2035.

Market growth is driven by the rising demand for biphenyl in the production of specialty chemicals. The pharmaceutical and agrochemical sectors increasingly rely on high-purity intermediates, making biphenyl a critical component in complex molecular formulations. Stricter regulatory requirements on chemical purity and performance are encouraging manufacturers to adopt biphenyl-based compounds for their stability and predictable results. Another significant driver is the expanding use of biphenyl as a heat transfer fluid and industrial solvent. Its excellent thermal stability and solubility make it ideal for high-performance industrial applications, particularly in the petrochemical and automotive sectors. Environmental and regulatory considerations also support biphenyl adoption, as its well-characterized safety profile and predictable behavior make it suitable for coatings, adhesives, plastics, and other regulated applications. Overall, the market is benefiting from a combination of industrial recovery, energy efficiency initiatives, and the need for reliable, compliant chemical solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $290 Million |

| Forecast Value | $505.5 Million |

| CAGR | 5.7% |

The technical-grade biphenyl segment will grow at a CAGR of 4.1% through 2035 due to the increasing replacement of lower-purity products with higher-purity biphenyl in more advanced and high-performance applications. Industries requiring stringent quality standards and enhanced chemical performance are favoring ultra-pure grades, which offer superior stability, consistency, and reactivity. This shift is limiting the demand for technical-grade biphenyl, which is primarily used in less complex applications where absolute purity is not a critical requirement.

The solid biphenyl segment is projected to capture 45% share in 2025, driven by its widespread use in pharmaceuticals, agrochemicals, and the production of specialty chemicals. Its popularity is supported by steady shipment growth at a CAGR of 5.4%. Solid biphenyl offers several operational advantages, including ease of handling, precise dosing capabilities, and stable storage properties, making it an ideal choice for applications requiring controlled and consistent chemical performance.

North America Biphenyl Market is expected to grow at a CAGR of 6.7% during 2026-2035. The region represents a mature and highly regulated market, where demand is primarily concentrated in pharmaceutical production, specialty chemical manufacturing, and established uses such as heat transfer fluids. Growth in the region is relatively stable, largely driven by regulatory compliance, incremental technological upgrades, and the need for consistent, high-quality products. Competitive differentiation in North America is increasingly shaped by factors such as innovation in application development, sustainable manufacturing practices, and advanced purification processes that enhance product performance and reliability.

Key companies active in the Global Biphenyl Market include Kishida Chemical Co., Ltd., Thermo Fisher Scientific, Eastman Chemical Company, Otto Chemie Pvt. Ltd., Ennore India Chemicals, and others. Market participants are strengthening their position by expanding high-purity biphenyl production capabilities, developing cleaner and more efficient synthesis processes, and diversifying feedstock sources to natural gas-based routes. Companies are also investing in R&D to enhance biphenyl applications in specialty chemicals, heat transfer media, and industrial solvents. Strategic partnerships with downstream chemical manufacturers and regional expansion initiatives help firms secure long-term contracts and global market share.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Purity

- 2.2.3 Physical Form

- 2.2.4 Application

- 2.2.5 End Use Industry

- 2.2.6 Distribution Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising pharmaceutical API production driving demand for ultra-high-purity biphenyl intermediates

- 3.2.1.2 Growing adoption of biphenyl-based heat transfer fluids across industrial thermal management systems

- 3.2.1.3 Expanding high-performance polymer usage in aerospace, electronics, and advanced engineering plastics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent environmental regulations and PCB contamination concerns limiting production flexibility and approvals

- 3.2.2.2 Volatile benzene feedstock pricing impacting production economics and long-term pricing stability

- 3.2.2.3 Increasing competition from alternative heat transfer fluids and substitute chemical synthesis pathways

- 3.2.3 Market opportunities

- 3.2.3.1 Commercialization of bio-based and green-chemistry biphenyl production technologies

- 3.2.3.2 Rapid expansion of electronics manufacturing requiring ultra-pure biphenyl for OLED and semiconductor applications

- 3.2.3.3 Untapped demand in emerging Asia Pacific and Latin American industrializing economies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By purity grade

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Purity Grade, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Pharmaceutical Grade (≥99.5%)

- 5.3 Industrial Grade (99-99.5%)

- 5.4 Technical Grade (95-99%)

Chapter 6 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Solid Form

- 6.2.1 Flakes

- 6.2.2 Powder

- 6.2.3 Crystals

- 6.3 Molten/Liquid Form

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Chemical Synthesis Intermediate

- 7.3 Heat Transfer Agent

- 7.4 Specialty Applications

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Pharmaceutical Industry

- 8.3 Agrochemical Industry

- 8.4 Polymer & Plastics Industry

- 8.5 Electronics & Electrical Industry

- 8.6 Heat Transfer Fluid Industry

- 8.7 Other Industries

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Direct Sales (Manufacturer to End-User)

- 9.3 Chemical Distributors & Wholesalers

- 9.4 Specialty Chemical Suppliers

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 BASF SE

- 11.2 Dow Inc.

- 11.3 Eastman Chemical Company

- 11.4 Huntsman Corporation

- 11.5 Jiangsu Zhongneng Chemical Technology Co., Ltd.

- 11.6 LANXESS AG

- 11.7 Merck KGaA

- 11.8 Mitsubishi Chemical Corporation

- 11.9 Solvay S.A.

- 11.10 Tokyo Chemical Industry Co., Ltd