|

시장보고서

상품코드

1959665

우주 사이버 보안 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Space Cybersecurity Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

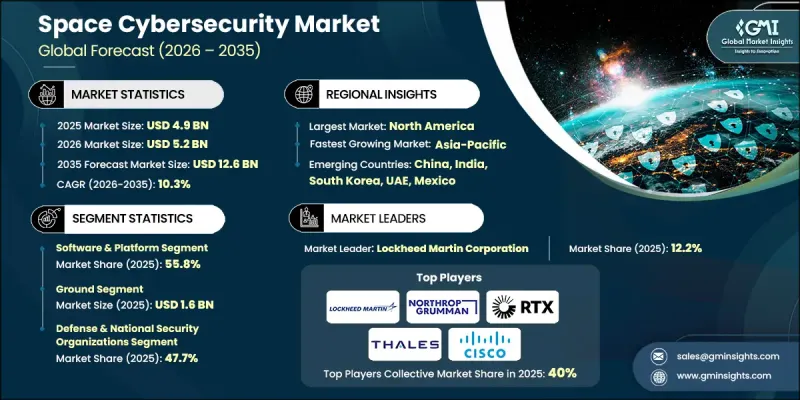

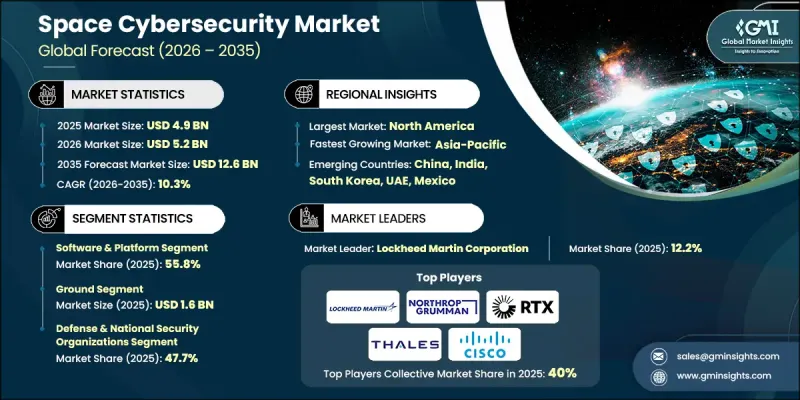

세계의 우주 사이버 보안 시장은 2025년에 49억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 10.3%로 성장하여 126억 달러에 이를 것으로 예측됩니다.

시장 확대의 배경에는 위성지휘통제시스템을 표적으로 한 사이버 공격 증가와 국방기관의 우주기반의 정보, 감시, 정찰 능력에 대한 의존도가 높아진 것을 꼽을 수 있습니다. 소프트웨어 정의 위성 및 클라우드 지원 지상 인프라로의 전환은 상업, 민간 및 군용 우주 프로그램 전반에 걸쳐 사이버 보안 요구 사항을 크게 높이고 있습니다. 궤도 자산의 상호 연결성과 데이터 집약도가 증가함에 따라, 미션 크리티컬 시스템을 침입, 방해, 데이터 변조로부터 보호하는 것이 전략적 우선순위가 되고 있습니다. 저궤도 위성의 급속한 확산으로 규제 당국과 사업자들이 네트워크 혼잡과 신호 간섭에 따른 위험 증가를 인식하면서 보안 프레임워크를 재구축하고 있습니다. 우주 공급망 전반의 사이버 보안 강화는 특히 위성 소프트웨어, 반도체 부품, 서브시스템의 아웃소싱이 증가함에 따라 조달 모델에도 변화를 가져오고 있습니다. 강화된 컴플라이언스 기준과 엄격한 모니터링은 신뢰성을 향상시키고, 제3자 취약성을 최소화하며, 새로운 디지털 위협에 대한 시스템 복원력을 강화합니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 49억 달러 |

| 예측 금액 | 126억 달러 |

| CAGR | 10.3% |

소프트웨어 및 플랫폼 분야는 2025년 55.8%의 점유율을 차지하여 위성 임무 및 지상 인프라 보호에 있어 핵심적인 역할을 반영하고 있습니다. 고급 사이버 보안 플랫폼은 암호화 관리, 액세스 인증, 이상 감지, 궤도 및 지상 시스템의 지속적인 모니터링을 지원합니다. 클라우드 기반 아키텍처와 소프트웨어 정의 위성과의 확장성 및 호환성을 통해 이러한 플랫폼은 적극적인 위험 감소에 필수적입니다. 사업자들이 실시간 위협 인텔리전스 및 자동화된 대응 메커니즘을 우선시하는 가운데, 안전한 디지털 플랫폼에 대한 투자는 계속 증가하고 있습니다.

통신 링크 보안 분야는 위성-지상 및 위성-위성 간 연결에서 신호 가로채기, 스푸핑, 방해의 위험이 증가함에 따라 2026년부터 2035년까지 연평균 11.3%의 성장률을 보일 것으로 예측됩니다. 위성 대역폭의 확대와 궤도상의 고밀도 배치로 인해 고급 암호화 프로토콜, 다층 인증, 전파방해 방지 기술의 필요성이 급증하고 있습니다. 복잡한 우주 통신 네트워크에서 안전한 데이터 전송을 보장하는 것은 정부 및 민간 이해관계자 모두에게 급성장하는 분야입니다.

북미 우주 사이버 보안 시장은 2025년 48.3%의 점유율을 차지할 것으로 예측됩니다. 이 지역의 성장은 위성 인프라에 대한 위협 증가, 우주 통신에 대한 의존도 증가, 국방 및 상업용 첨단 위성 별자리의 급속한 전개에 의해 뒷받침되고 있습니다. 소프트웨어 정의 위성 시스템 및 클라우드 통합형 지상국의 적극적인 도입으로 사이버 위험에 대한 노출이 증가하고 있으며, 제로 트러스트 아키텍처, AI 기반 위협 분석, 강화된 위성 설계에 대한 투자를 촉진하고 있습니다. 사이버 보안 분야에서의 민관 협력의 혁신은 진화하는 이 시장에서 이 지역의 리더십을 더욱 강화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제공 형태별, 2022-2035

제6장 시장 추산 및 예측 : 전개 형태별, 2022-2035

제7장 시장 추산 및 예측 : 용도별, 2022-2035

제8장 시장 추산 및 예측 : 최종 이용 산업별, 2022-2035

제9장 시장 추산 및 예측 : 지역별, 2022-2035

제10장 기업 개요

LSH 26.03.16The Global Space Cybersecurity Market was valued at USD 4.9 billion in 2025 and is estimated to grow at a CAGR of 10.3% to reach USD 12.6 billion by 2035.

Market expansion is driven by the growing number of cyberattacks targeting satellite command-and-control systems and the increasing reliance of defense organizations on space-based intelligence, surveillance, and reconnaissance capabilities. The transition toward software-defined satellites and cloud-enabled ground infrastructure is significantly elevating cybersecurity requirements across commercial, civil, and military space programs. As orbital assets become more interconnected and data-intensive, protecting mission-critical systems from intrusion, disruption, and data manipulation has become a strategic priority. The rapid deployment of low-earth orbit satellite constellations is reshaping security frameworks, as regulators and operators recognize heightened risks associated with network congestion and signal interference. Strengthening cybersecurity across the space supply chain is also transforming procurement models, particularly as outsourcing of satellite software, semiconductor components, and subsystems increases. Enhanced compliance standards and stricter oversight are improving trust, minimizing third-party vulnerabilities, and reinforcing system resilience against emerging digital threats.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.9 Billion |

| Forecast Value | $12.6 Billion |

| CAGR | 10.3% |

The software and platform segment accounted for 55.8% share in 2025, reflecting its central role in safeguarding satellite missions and ground-based infrastructure. Advanced cybersecurity platforms support encryption management, access authentication, anomaly detection, and continuous monitoring of orbital and terrestrial systems. Their scalability and compatibility with cloud-based architectures and software-defined satellites make them indispensable for proactive risk mitigation. As operators prioritize real-time threat intelligence and automated response mechanisms, investment in secure digital platforms continues to rise.

The communication link security segment is projected to grow at a CAGR of 11.3% during 2026-2035, fueled by increasing risks of signal interception, spoofing, and jamming across satellite-to-ground and inter-satellite connections. Expanding satellite bandwidth capabilities and dense orbital deployments are intensifying the need for advanced encryption protocols, multi-layer authentication, and anti-interference technologies. Ensuring secure data transmission across complex space communication networks has become a high-growth focus area for both government and commercial stakeholders.

North America Space Cybersecurity Market held a 48.3% share in 2025. Regional growth is supported by rising threats to satellite infrastructure, expanding dependence on space-based communications, and rapid deployment of advanced satellite constellations for defense and commercial purposes. Strong adoption of software-defined satellite systems and cloud-integrated ground stations is increasing exposure to cyber risks, prompting investment in zero-trust architectures, AI-driven threat analytics, and hardened satellite designs. Public and private sector collaboration in cybersecurity innovation further reinforces the region's leadership in this evolving market.

Key companies operating in the Global Space Cybersecurity Market include Lockheed Martin Corporation, Thales Group, Northrop Grumman Corporation, Airbus SE, L3Harris Technologies, Inc., RTX Corporation, Leonardo S.p.A., Booz Allen Hamilton, General Dynamics Corporation, Leidos Holdings, Inc., BAE Systems Plc, Cisco Systems, Inc., Fortinet, Inc., Check Point Software Technologies, CrowdStrike Holdings, Inc., CGI Group, Anduril Industries, Inc., Xage Security, Inc., and Nightwing Technologies. Companies in the Space Cybersecurity Market are strengthening their competitive positions by investing heavily in advanced encryption technologies, AI-powered threat detection, and post-quantum cryptography research to address future risks. Strategic partnerships with satellite manufacturers, defense agencies, and cloud service providers enable integrated security frameworks across orbital and ground systems. Firms are expanding managed security services and offering end-to-end cybersecurity platforms tailored for space missions. They are also focusing on compliance-driven solutions aligned with evolving regulatory mandates, while enhancing supply chain transparency to mitigate third-party risks.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Offering type trends

- 2.2.2 Deployment trends

- 2.2.3 Application trends

- 2.2.4 End-use industry trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising cyberattacks on satellite command-and-control systems

- 3.2.1.2 Proliferation of LEO satellite mega-constellations

- 3.2.1.3 Increased military reliance on space-based ISR assets

- 3.2.1.4 Integration of cloud-based ground station architectures

- 3.2.1.5 Commercialization of satellite communications and data services

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited cybersecurity standards specific to space systems

- 3.2.2.2 Legacy satellites lacking onboard security upgrade capabilities

- 3.2.3 Market opportunities

- 3.2.3.1 Zero-trust architectures for satellite-ground communications

- 3.2.3.2 AI-driven anomaly detection for space mission networks

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Offering Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Cryptographic modules

- 5.2.2 Secure boot & trusted execution

- 5.2.3 Anti-jamming & secure communication

- 5.3 Software & platform

- 5.3.1 Encryption & cryptography

- 5.3.2 Access control & authentication

- 5.3.3 Threat detection & monitoring

- 5.3.4 Command & control (C2) security

- 5.3.5 Cyber resilience & recovery platforms

- 5.4 Services

- 5.4.1 Managed services

- 5.4.2 Professional & consulting services

Chapter 6 Market Estimates and Forecast, By Deployment, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Space segment (on-orbit) security

- 6.3 Ground segment security

- 6.4 Link segment (communication) security

- 6.5 User segment security

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Satellite communications

- 7.3 Earth observation & remote sensing

- 7.4 Navigation & positioning (PNT)

- 7.5 Space exploration & scientific missions

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By End-use Industry, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Defense & national security organizations

- 8.3 Civil government space agencies & research institutions

- 8.4 Commercial space asset operators

- 8.5 Downstream service providers & system integrators

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Airbus SE

- 10.1.2 RTX Corporation

- 10.1.3 BAE Systems Plc

- 10.1.4 Lockheed Martin Corporation

- 10.1.5 Northrop Grumman Corporation

- 10.1.6 Thales Group

- 10.1.7 Leonardo S.p.A.

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Booz Allen Hamilton

- 10.2.1.2 General Dynamics Corporation

- 10.2.1.3 L3Harris Technologies, Inc.

- 10.2.1.4 Leidos Holdings, Inc.

- 10.2.1.5 CGI Group

- 10.2.2 Asia Pacific

- 10.2.2.1 Cisco Systems, Inc.

- 10.2.3 Europe

- 10.2.3.1 Check Point Software Technologies

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Anduril Industries, Inc.

- 10.3.2 CrowdStrike Holdings, Inc.

- 10.3.3 Fortinet, Inc.

- 10.3.4 Nightwing Technologies

- 10.3.5 Xage Security, Inc.