|

시장보고서

상품코드

1982261

데이터센터용 HVAC 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Data Center HVAC Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

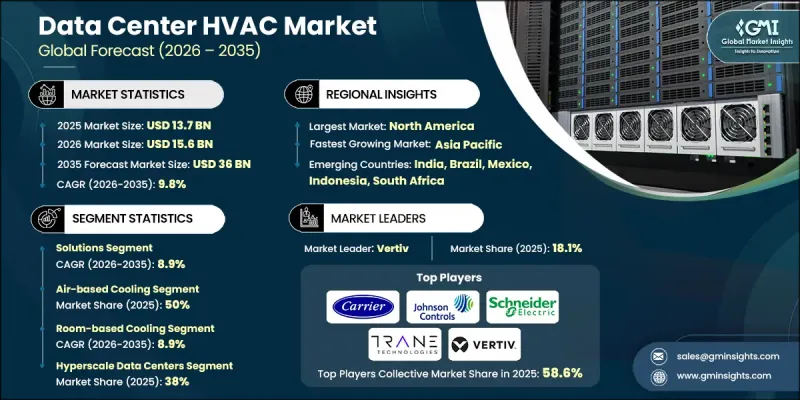

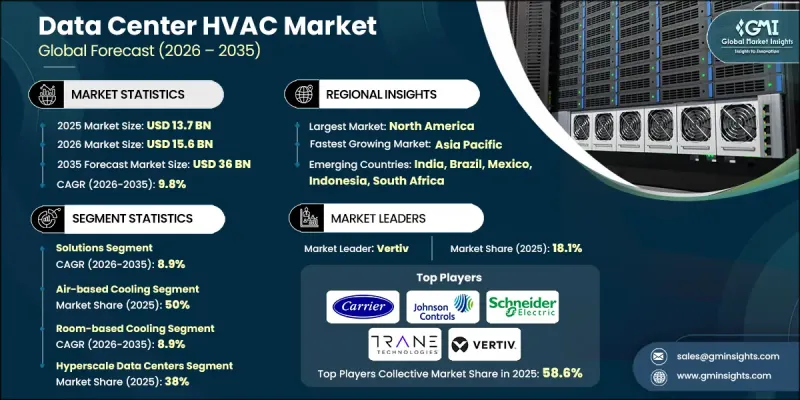

세계의 데이터센터용 HVAC 시장은 2025년에 137억 달러로 평가되었으며, CAGR 9.8%로 성장하여 2035년까지 360억 달러에 달할 것으로 추정됩니다.

세계 데이터센터용 HVAC 시장의 성장은 컴퓨팅 집약도 증가, AI 기반 워크로드 증가, 하이퍼스케일 및 엔터프라이즈 시설의 지속적인 개발로 인해 성장하고 있습니다. 서버 밀도의 증가와 고성능 컴퓨팅 환경으로 인한 열 부하가 증가함에 따라, 운영 안정성과 가동 시간을 유지하기 위해서는 고도의 냉각 인프라가 필수적입니다. HVAC 업계 전반의 연구개발 노력은 액체 냉각 기술과 고출력 밀도에 대응할 수 있는 차세대 열관리 시스템에 점점 더 집중하고 있습니다. 동시에 에너지 소비 및 환경 성능에 대한 규제가 강화됨에 따라 사업자들은 시스템 효율을 높이고 이산화탄소 배출량을 줄여야 하는 상황에 직면해 있습니다. ESG에 초점을 맞춘 노력과 넷제로에 대한 약속은 전력 사용 효율(PUE)을 최적화하고 운영 비용을 절감하기 위한 시설 업그레이드를 촉진하고 있습니다. 기류 설계의 개선, 지속가능한 냉매의 채택, 에너지 효율적인 냉각 아키텍처의 통합으로 인프라 전략이 재편되고 있습니다. 규제 요건과 에너지 비용 상승이 지속됨에 따라 데이터센터의 지능형 고효율 HVAC 솔루션에 대한 수요는 크게 가속화될 것으로 예상됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시시 시장 규모 | 137억 달러 |

| 예측액 | 360억 달러 |

| CAGR | 9.8% |

부하 용량의 증가, 지속가능성 목표 및 규제 준수 요구 사항으로 인해 컴팩트하고 확장성이 뛰어나며 적응력이 뛰어난 HVAC 시스템에 대한 수요가 증가하고 있습니다. 업계 관계자들은 공간 활용도와 에너지 성능을 극대화하면서 다양한 지역에서 효과적으로 운영할 수 있는 모듈식 냉각 플랫폼을 설계하여 이러한 수요에 대응하고 있습니다.

솔루션 분야는 2025년 76%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 8.9%의 성장률을 보일 것으로 전망됩니다. 인공지능(AI)이 탑재된 첨단 모니터링 툴을 통해 예지보전이 가능하고, 기류 관리가 개선되며, 불필요한 전력 소비를 줄일 수 있습니다. 액체 냉각 기술 채택 확대는 고밀도 서버 환경을 지원하는 동시에 에너지 절약 설계를 통해 신뢰성을 높이고 장비의 수명을 연장하고 있습니다.

공기 냉각 기술 부문은 2025년에 50%의 점유율을 차지했으며, 2026년부터 2035년까지 CAGR 8.8%로 성장할 것으로 전망됩니다. 고급 기류 최적화 시스템, 가변 속도 팬 구성 및 지능형 환경 제어를 통해 열 안정성을 향상시키고 에너지 낭비를 최소화합니다. 이코노마이저 지원 설계는 외부 공기 활용을 촉진하는 한편, 모듈식 냉각 유닛은 하이퍼스케일 환경과 엣지 환경 모두에서 확장성을 지원합니다. 서버의 전력 밀도가 높아짐에 따라 열전달 효율을 높이는 첨단 냉각제 배합에 기반한 직접 냉각 및 침수 냉각 방식에 대한 관심도 높아지고 있습니다.

미국 데이터센터용 HVAC 시장은 2025년 47억 달러에 달할 것으로 예상됩니다. 클라우드 통합의 발전과 AI 집약적 애플리케이션의 증가는 보다 효율적인 냉각 아키텍처에 대한 수요를 주도하고 있습니다. 전기화 촉진책과 탈탄소화 이니셔티브를 통한 투자 지원으로 지능형 HVAC 제어 및 에너지 최적화 시스템의 보급이 촉진되고 있습니다. 스마트 빌딩 플랫폼 및 그리드 지원 기술과의 통합을 통해 시설은 피크 부하 관리, 수요 요금 절감, 재생에너지원을 도입할 수 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 제공 서비스별, 2022-2035

제6장 시장 추정 및 예측 : 냉각 기술별, 2022-2035

제7장 시장 추정 및 예측 : 기기별, 2022-2035

제8장 시장 추정 및 예측 : 냉각 방식별, 2022-2035

제9장 시장 추정 및 예측 : 데이터센터별, 2022-2035

제10장 시장 추정 및 예측 : 최종 용도별, 2022-2035

제11장 시장 추정 및 예측 : 지역별, 2022-2035

제12장 기업 개요

KSMThe Global Data Center HVAC Market was valued at USD 13.7 billion in 2025 and is estimated to grow at a CAGR of 9.8% to reach USD 36 billion by 2035.

Growth in the global data center HVAC market is being fueled by rising computing intensity, expanding AI-driven workloads, and the continued development of hyperscale and enterprise facilities. As server densities increase and high-performance computing environments generate greater thermal loads, advanced cooling infrastructure has become essential to maintain operational stability and uptime. Research and development efforts across the HVAC industry are increasingly focused on liquid cooling technologies and next-generation thermal management systems capable of handling elevated power densities. At the same time, stricter regulatory oversight related to energy consumption and environmental performance is encouraging operators to enhance system efficiency and reduce carbon output. ESG-focused initiatives and net-zero commitments are prompting facility upgrades aimed at optimizing Power Usage Effectiveness and lowering operating expenses. Improvements in airflow engineering, adoption of sustainable refrigerants, and integration of energy-efficient cooling architectures are reshaping infrastructure strategies. As regulatory expectations and energy costs continue to rise, demand for intelligent, high-efficiency HVAC solutions in data centers is expected to accelerate significantly.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13.7 Billion |

| Forecast Value | $36 Billion |

| CAGR | 9.8% |

Rising load capacities, sustainability targets, and regulatory compliance requirements are creating pressure for compact, scalable, and adaptable HVAC systems. Industry participants are responding by designing modular cooling platforms that can operate effectively across diverse geographies while maximizing space utilization and energy performance.

The solutions segment accounted for 76% share in 2025 and is forecast to grow at a CAGR of 8.9% from 2026 to 2035. Advanced monitoring tools equipped with artificial intelligence enable predictive maintenance, improve airflow management, and reduce unnecessary power consumption. Increased adoption of liquid-based cooling technologies is supporting high-density server environments while enhancing reliability and extending equipment lifespan through energy-conscious design.

The air-based cooling technologies segment held a 50% share in 2025 and is projected to grow at a CAGR of 8.8% during 2026-2035. Enhanced airflow optimization systems, variable-speed fan configurations, and intelligent environmental controls are improving thermal consistency and minimizing energy waste. Economizer-enabled designs are facilitating greater use of ambient air, while modular cooling units support scalability across both hyperscale and edge environments. Growing server power density is also accelerating interest in direct cooling and immersion-based methods supported by advanced coolant formulations that enhance heat transfer efficiency.

United States Data Center HVAC Market reached USD 4.7 billion in 2025. Increasing cloud integration and AI-intensive applications are driving demand for more efficient cooling architectures. Investments are being supported by electrification incentives and decarbonization initiatives, encouraging broader adoption of intelligent HVAC controls and energy-optimized systems. Integration with smart building platforms and grid-responsive technologies is enabling facilities to manage peak loads, reduce demand charges, and incorporate renewable energy sources.

Key companies operating in the Global Data Center HVAC Market include Vertiv, Schneider Electric, Carrier Global, Daikin Industries, Trane Technologies, Johnson Controls, STULZ, Alfa Laval, Danfoss, and Modine Manufacturing. Companies in the Global Data Center HVAC Market are strengthening their competitive position through continuous innovation, strategic partnerships, and geographic expansion. Leading players are investing heavily in research and development to enhance liquid cooling efficiency, improve airflow intelligence, and integrate AI-driven monitoring systems. Collaborations with cloud service providers and data center developers are enabling customized cooling deployments for high-density environments. Firms are also expanding manufacturing capacity and regional service networks to support rapid infrastructure growth. Sustainability-focused product development, including low-global-warming-potential refrigerants and energy-efficient system architectures, is becoming a central competitive differentiator.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Offering

- 2.2.3 Cooling technology

- 2.2.4 Equipment level

- 2.2.5 Cooling technique

- 2.2.6 Data center

- 2.2.7 End use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising data center energy consumption

- 3.2.1.2 Stricter thermal management standards

- 3.2.1.3 Growth in cloud & hyperscale infrastructure

- 3.2.1.4 Adoption of high-density computing

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial capital expenditure

- 3.2.2.2 Complex integration with legacy systems

- 3.2.3 Market opportunities

- 3.2.3.1 Liquid cooling adoption

- 3.2.3.2 AI-driven HVAC optimization

- 3.2.3.3 Edge data center expansion

- 3.2.3.4 HVAC as a service (HaaS)

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 American Society of Heating, Refrigerating and Air-Conditioning Engineers

- 3.4.1.2 U.S. Department of Energy

- 3.4.2 Europe

- 3.4.2.1 European Commission

- 3.4.2.2 Eurovent Certita Certification

- 3.4.3 Asia Pacific

- 3.4.3.1 BCA - Building and Construction Authority (Singapore)

- 3.4.3.2 JIS - Japanese Industrial Standards

- 3.4.4 Latin America

- 3.4.4.1 Associacao Brasileira de Normas Tecnicas

- 3.4.4.2 Comision Nacional de Energia

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE Ministry of Energy and Infrastructure

- 3.4.5.2 Saudi Standards, Metrology and Quality Organization

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing analysis

- 3.8.1 Pricing by product

- 3.8.2 Pricing by region

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Energy Efficiency Metrics & Benchmarking

- 3.13.1 Power Usage Effectiveness (PUE) Trends

- 3.13.2 Water Usage Effectiveness (WUE) Analysis

- 3.13.3 Carbon Usage Effectiveness (CUE) Metrics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Offering, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Solutions

- 5.2.1 Cooling infrastructure solutions

- 5.2.2 Airflow management & containment solutions

- 5.2.3 Liquid cooling integration solutions

- 5.2.4 HVAC automation & control solutions

- 5.2.5 Thermal monitoring & management solutions

- 5.2.6 Energy optimization & free cooling solutions

- 5.2.7 Modular / scalable cooling solutions

- 5.2.8 Edge data center cooling solutions

- 5.3 Services

- 5.3.1 Professional services

- 5.3.1.1 Consulting & design

- 5.3.1.2 Maintenance and support

- 5.3.1.3 Installation and deployment

- 5.3.2 Managed services

- 5.3.1 Professional services

Chapter 6 Market Estimates & Forecast, By Cooling Technology, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Air-based cooling

- 6.3 Liquid cooling

- 6.4 Evaporative cooling

- 6.5 Hybrid cooling

Chapter 7 Market Estimates & Forecast, By Equipment-Level, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Air conditioning systems

- 7.3 Chillers

- 7.4 Air handling units (AHU)

- 7.5 Liquid cooling systems

- 7.6 Cooling towers

- 7.7 Economizer systems

- 7.8 Control systems

- 7.9 Others

Chapter 8 Market Estimates & Forecast, By Cooling Technique, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Room-based cooling

- 8.3 Row-based cooling

- 8.4 Rack-based cooling

Chapter 9 Market Estimates & Forecast, By Data Center, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 Enterprise data centers

- 9.3 Colocation data centers

- 9.4 Hyperscale data centers

- 9.5 Edge data centers

Chapter 10 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 IT & telecommunications

- 10.3 BFSI

- 10.4 Government & defense

- 10.5 Healthcare

- 10.6 Manufacturing

- 10.7 Retail & e-commerce

- 10.8 Energy & utilities

- 10.9 Research & academic

- 10.10 Others

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Nordics

- 11.3.7 Russia

- 11.3.8 Poland

- 11.3.9 Romania

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Vietnam

- 11.4.7 Indonesia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global companies

- 12.1.1 Alfa Laval

- 12.1.2 Carrier Global

- 12.1.3 Daikin Industries

- 12.1.4 Danfoss

- 12.1.5 Hitachi

- 12.1.6 Johnson Controls

- 12.1.7 Modine

- 12.1.8 Schneider Electric

- 12.1.9 STULZ

- 12.1.10 Trane Technologies

- 12.1.11 Vertiv

- 12.2 Regional players

- 12.2.1 Climaveneta

- 12.2.2 Envicool

- 12.2.3 Huawei Digital Power

- 12.2.4 KyotoCooling

- 12.2.5 Mitsubishi Electric

- 12.3 Emerging players

- 12.3.1 Asetek

- 12.3.2 CoolIT Systems

- 12.3.3 Green Revolution Cooling

- 12.3.4 Iceotope Technologies