|

시장보고서

상품코드

1982284

폴리우레탄 단열재 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2026-2035년)Polyurethane Insulation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

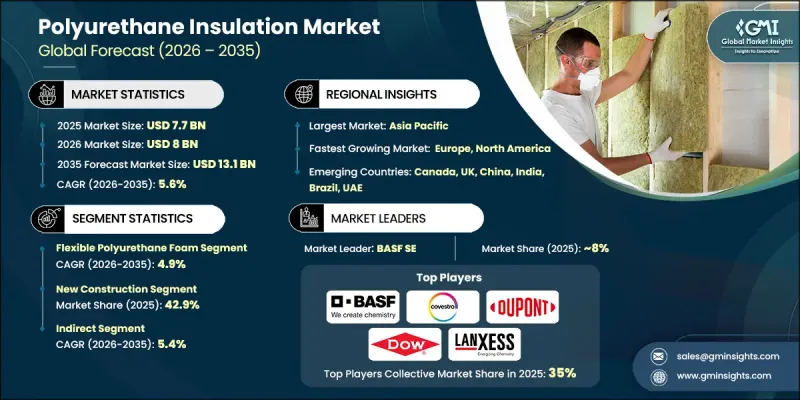

세계의 폴리우레탄 단열재 시장은 2025년 77억 달러로 평가되었고, CAGR은 5.6%를 나타낼 것으로 보이며, 2035년까지 131억 달러에 이를 것으로 추정됩니다.

폴리우레탄 단열재 산업의 성장은 세계적인 에너지 효율 강화 의무화와 상업 및 산업 인프라 전반의 탄소 배출 감축을 목표로 하는 기후 중심 규제에 힘입고 있습니다. 규제 당국은 건축 성능 기준을 강화하여 개발사들이 열 효율을 개선하는 첨단 단열재를 도입하도록 유도하고 있습니다. 동시에 지속 가능한 건축 관행과 에너지 효율 개선 공사로의 전환이 제품 채택을 가속화하고 있습니다. 건설사들은 장기적인 에너지 소비와 환경 영향을 줄이는 단열 솔루션을 우선시하고 있어, 폴리우레탄 단열재는 신축 건물과 리모델링 프로젝트 모두에서 선호되는 재료로 자리 잡고 있습니다. 냉장 보관 인프라와 온도 조절 물류 네트워크의 확장은 수요를 더욱 부추기고 있습니다. 부패하기 쉬운 상품이나 온도에 민감한 상품을 취급하는 산업 분야에서는 운영 효율성을 유지하기 위해 고성능 단열재가 필요하기 때문입니다. 폴리우레탄 단열재는 뛰어난 내열성, 내구성 및 에너지 절약 능력 덕분에 계속해서 주목받고 있으며, 이는 다양한 최종 사용 산업 전반에 걸쳐 꾸준한 시장 확장을 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 시장 규모 | 77억 달러 |

| 예측 금액 | 131억 달러 |

| CAGR | 5.6% |

연질 폴리우레탄 폼 부문은 2025년부터 2035년까지 연평균 성장률(CAGR) 4.9%로 성장할 것으로 전망됩니다. 이 부문에 대한 수요는 광범위한 용도에서 나타나는 적응성, 경량 구조 및 성능 효율성 덕분에 증가하고 있습니다. 쿠션 강도, 탄력성 및 편안함을 향상시키는 특성 덕분에 여러 제조 분야에서 선호되는 재료로 자리 잡고 있습니다. 향상된 편안함, 내구성 및 인체공학적 성능에 대한 소비자의 기대가 높아짐에 따라, 더 넓은 폴리우레탄 단열재 시장 내에서 이 부문의 꾸준한 성장에 기여하고 있습니다.

신축 부문은 2025년에 42.9%의 점유율을 차지하며, 2026년부터 2035년에 걸쳐 CAGR 5.8%를 나타낼 것으로 예측됩니다. 급속한 도시 확장, 지속적인 인프라 투자, 그리고 점점 더 엄격해지는 건축 에너지 규정이 이 부문의 주도적 위치를 공고히 하고 있습니다. 개발사들은 규제 기준을 충족하고 장기적인 운영 성능을 개선하기 위해 현대식 건축물에 고효율 단열 시스템을 도입하고 있습니다. 지속 가능한 도시 계획과 에너지 효율을 고려한 설계에 대한 관심이 높아짐에 따라 폴리우레탄 기반 단열재에 대한 강력한 수요가 지속적으로 발생하고 있습니다.

미국의 폴리우레탄 단열재 시장은 2025년에 16억 달러에 이르고, 2026년부터 2035년에 걸쳐 CAGR 5.1%를 나타낼 것으로 예측됩니다. 미국 내 시장 확대는 지속적인 건설 활동, 에너지 절약을 장려하는 견고한 규제 체계, 그리고 환경 친화적인 건축 기준의 광범위한 채택에 힘입고 있습니다. 주거, 상업 및 산업 부문은 변화하는 건축 요건에 부응하고 운영 에너지 비용을 절감하기 위해 단열 개선에 대한 투자를 늘리고 있습니다. 기존 건물의 지속적인 현대화, 기술 발전, 그리고 비용 효율적인 단열 솔루션에 대한 인식 제고는 미국의 선도적 위치를 더욱 공고히 하고 있습니다.

자주 묻는 질문

목차

제1장 연구 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 엄격한 에너지 효율 규제와 기후 목표

- 지속 가능한 건설 및 건물 리모델링에 대한 수요 증가

- 콜드 체인 물류 및 냉동 부문의 확장

- 업계의 잠재적 위험 및 과제

- 화학 물질 사용에 대한 엄격한 환경 규제

- 원재료 가격 변동

- 성장 촉진요인

- 성장 가능성 분석

- 향후 시장 동향

- 기술 및 혁신 동향

- 현재의 기술 동향

- 신흥 기술

- 가격 동향

- 지역별

- 제품 유형별

- 규제 상황

- 규격 및 규정 준수 요건

- 지역별 규제 프레임워크

- 인증기준

- 무역 통계

- 주요 수입국

- 주요 수출국

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계 및 예측 : 제품 유형별(2022-2035년)

- 경질 폴리우레탄 폼 보드

- 스프레이 폴리우레탄 폼(SPF)

- 폴리이소시아누레이트(PIR) 보드

- 연질 폴리우레탄 폼

제6장 시장 추계 및 예측 : 설치 방법별(2022-2035년)

- 신축

- 개조/리모델링

- 보수 및 교환

제7장 시장 추계 및 예측 : 용도별(2022-2035년)

- 주택 건축

- 상업용 건물

- 산업용 건물

- 인프라

제8장 시장 추계 및 예측 : 최종 사용자별(2022-2035년)

- 지붕 및 천장 단열재

- 벽 단열재

- 바닥 단열재

- 배관 단열재

- 냉장 및 냉동

- 탱크 및 용기

- 기타(HVAC, 자동차 내장)

제9장 시장 추계 및 예측 : 유통 채널별(2022-2035년)

- 직접

- 간접

제10장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 인도네시아

- 말레이시아

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카(MEA)

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

제11장 기업 프로파일

- Armacell

- BASF SE

- Compagnie de Saint-Gobain SA

- Covestro AG

- Dow Inc.

- DuPont

- Foam Supplies Inc.(FSI)

- FoamPartner

- Gallagher Corporation

- Huntsman Corporation

- IMA Srl

- LANXESS

- Nitto Denko Corporation

- Tosoh Corporation

- Wanhua Chemical Group

The Global Polyurethane Insulation Market was valued at USD 7.7 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 13.1 billion by 2035.

Growth in the polyurethane insulation industry is driven by stricter global energy efficiency mandates and climate-focused regulations aimed at lowering carbon emissions across commercial and industrial infrastructure. Regulatory authorities are reinforcing building performance standards, pushing developers to integrate advanced insulation materials that improve thermal efficiency. At the same time, the shift toward sustainable construction practices and energy-efficient retrofitting is accelerating product adoption. Builders are prioritizing insulation solutions that reduce long-term energy consumption and environmental impact, positioning polyurethane insulation as a preferred material for both newly built structures and renovation projects. Expanding cold storage infrastructure and temperature-controlled logistics networks are also fueling demand, as industries handling perishable and temperature-sensitive goods require high-performance insulation to maintain operational efficiency. Polyurethane insulation continues to gain traction due to its strong thermal resistance, durability, and energy-saving capabilities, supporting consistent market expansion across multiple end-use industries.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.7 Billion |

| Forecast Value | $13.1 Billion |

| CAGR | 5.6% |

The flexible polyurethane foam segment is forecast to grow at a CAGR of 4.9% from 2025 to 2035. Demand for this segment is increasing due to its adaptability, lightweight structure, and performance efficiency across a broad range of applications. Its cushioning strength, resilience, and comfort-enhancing properties make it a preferred material across several manufacturing sectors. Rising consumer expectations for enhanced comfort, durability, and ergonomic performance are contributing to steady segment growth within the broader polyurethane insulation market.

The new construction segment accounted for 42.9% share in 2025 and is expected to grow at a CAGR of 5.8% between 2026 and 2035. Rapid urban expansion, continued infrastructure investments, and increasingly rigorous building energy codes are reinforcing the dominance of this segment. Developers are integrating high-efficiency insulation systems into modern structures to meet regulatory benchmarks and improve long-term operational performance. The growing emphasis on sustainable urban planning and energy-conscious design continues to create strong demand for polyurethane-based insulation materials.

United States Polyurethane Insulation Market reached USD 1.6 billion in 2025, with projected growth at a CAGR of 5.1% from 2026 to 2035. Market expansion in the country is supported by sustained construction activity, firm regulatory frameworks promoting energy conservation, and widespread adoption of environmentally responsible building standards. Residential, commercial, and industrial sectors are increasing investments in insulation upgrades to align with evolving building requirements and reduce operational energy costs. Continued modernization of existing properties, technological advancements, and heightened awareness of cost-efficient insulation solutions further reinforce the country's leadership position.

Key companies operating in the Global Polyurethane Insulation Market include Armacell, BASF SE, Compagnie de Saint-Gobain SA, Covestro AG, Dow Inc., DuPont, Foam Supplies Inc. (FSI), FoamPartner, Gallagher Corporation, Huntsman Corporation, IMA Srl, LANXESS, Nitto Denko Corporation, Tosoh Corporation, and Wanhua Chemical Group. Companies in the Global Polyurethane Insulation Market are strengthening their market position through capacity expansion, product innovation, and strategic collaborations. Manufacturers are investing in research and development to enhance thermal performance, improve fire resistance, and develop environmentally compliant formulations that align with evolving regulatory standards. Strategic mergers, acquisitions, and joint ventures are being pursued to expand geographic reach and diversify product portfolios. Many players are also focusing on backward integration and supply chain optimization to secure raw material availability and control production costs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Installation method

- 2.2.4 Application

- 2.2.5 End-user

- 2.2.6 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent energy efficiency regulations and climate goals

- 3.2.1.2 Rising demand for sustainable construction and building renovation

- 3.2.1.3 Expansion of cold chain logistics and refrigeration sector

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Stringent Environmental Regulations on Chemical Use

- 3.2.2.2 Volatility in raw material prices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and Innovation Landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion)

- 5.1 Key trends

- 5.2 Rigid polyurethane foam boards

- 5.3 Spray polyurethane foam (SPF)

- 5.4 Polyisocyanurate (PIR) boards

- 5.5 Flexible polyurethane foam

Chapter 6 Market Estimates & Forecast, By Installation Method, 2022 - 2035, (USD Billion)

- 6.1 Key trends

- 6.2 New construction

- 6.3 Retrofit/Renovation

- 6.4 Maintenance & replacement

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion)

- 7.1 Key trends

- 7.2 Residential buildings

- 7.3 Commercial buildings

- 7.4 Industrial buildings

- 7.5 Infrastructure

Chapter 8 Market Estimates & Forecast, By End-User, 2022 - 2035, (USD Billion)

- 8.1 Key trends

- 8.2 Roof & ceiling insulation

- 8.3 Wall insulation

- 8.4 Floor insulation

- 8.5 Pipe insulation

- 8.6 Cold storage & refrigeration

- 8.7 Tank & vessels

- 8.8 Others (HVAC, automotive interiors)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Indonesia

- 10.4.7 Malaysia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Armacell

- 11.2 BASF SE

- 11.3 Compagnie de Saint-Gobain SA

- 11.4 Covestro AG

- 11.5 Dow Inc.

- 11.6 DuPont

- 11.7 Foam Supplies Inc. (FSI)

- 11.8 FoamPartner

- 11.9 Gallagher Corporation

- 11.10 Huntsman Corporation

- 11.11 IMA Srl

- 11.12 LANXESS

- 11.13 Nitto Denko Corporation

- 11.14 Tosoh Corporation

- 11.15 Wanhua Chemical Group