|

시장보고서

상품코드

1982357

의료기기 상환 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Medical Devices Reimbursement Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

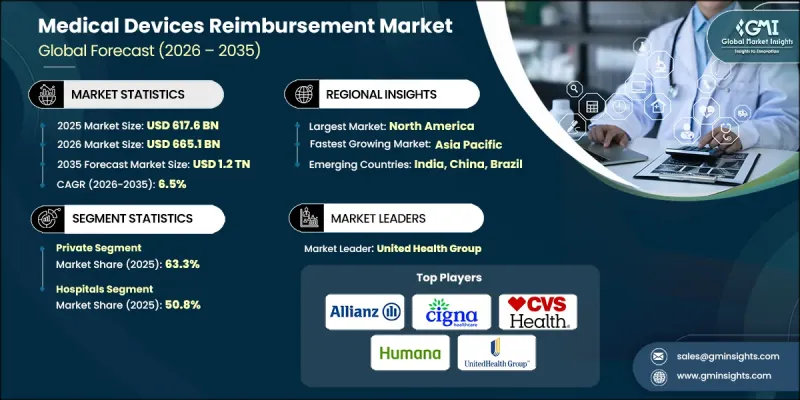

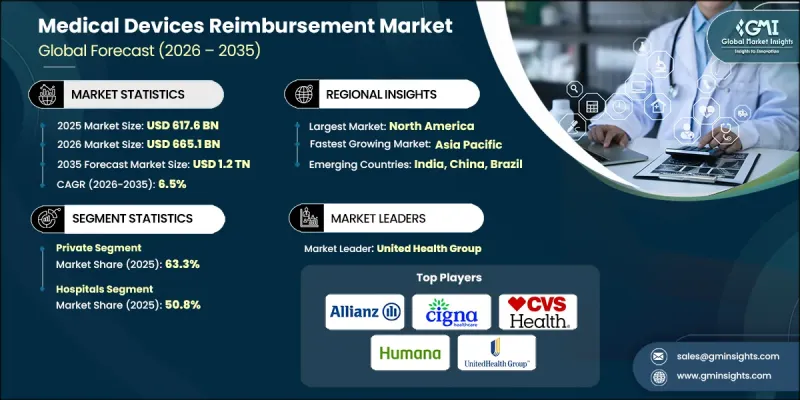

세계의 의료기기 상환 시장은 2025년에 6,176억 달러로 평가되었으며, CAGR 6.5%로 성장하여 2035년까지 1조 2,000억 달러에 달할 것으로 추정됩니다.

시장 확대는 의료비 증가, 만성질환 유병률 증가, 의료기기에 대한 접근성을 높이기 위한 정부 지원책에 의해 주도되고 있습니다. 또한, 가치기반 의료모델의 도입으로 상환의 틀도 재구성되어 임상적 유효성과 비용효과성을 중시하는 방향으로 재편되고 있습니다. 의료기기 상환은 병원, 진료소, 수술 센터 등 의료 서비스 제공자가 진단, 모니터링 및 치료에서 기기의 획득, 유지 및 사용에 대해 보상하는 것을 말합니다. 새로운 지불 모델, 적용 기준 및 시장 진입 경로와 함께 진화하는 상환 구조는 환자 결과를 개선하고 전체 의료 비용을 절감할 수 있는 혁신적인 기기에 대한 기회를 창출하고 있습니다. 이러한 혁신적 추세는 재정적 지속가능성을 보장하는 동시에 현대 의료 시스템에 의료기기의 통합을 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시시점 시장 규모 | 6,176억 달러 |

| 예측액 | 1조 2,000억 달러 |

| CAGR | 6.5% |

2025년 기준, 민간 보험사 부문은 63.3%의 점유율을 차지했습니다. 민간 보험사, 고용주가 제공하는 보험 플랜 및 보충 보험은 일반적으로 공적 보험사보다 더 빠른 혜택 결정과 유리한 지급률을 제공합니다. 또한, 민간보험에서는 첨단 의료기기나 프리미엄 장비가 보험금 지급 대상에 포함될 가능성이 높습니다. 이 부문의 성장은 특히 민간보험이 널리 보급된 아시아태평양에서 중산층 및 고소득층 인구의 증가에 힘입어 성장세를 보이고 있습니다.

2025년 기준, 병원 부문은 50.8%의 점유율을 차지했습니다. 병원의 경우 입원, 외래, 외래 수술 센터, 응급실 등 병원 내 모든 진료과목에 대해 보상받을 수 있습니다. 성장의 원동력은 수술 건수 증가, 첨단 기술 도입, 복잡한 시술에 대한 급여 범위 확대입니다. 많은 의료기기는 개별 기기 단위가 아닌 시술료나 진단 관련 그룹(DRG) 등 포괄수가제 틀 안에서 상환되고 있습니다.

2025년, 북미 의료기기 상환 시장은 47.2%의 점유율을 차지했습니다. 미국 시장은 거대한 의료 경제, 확립된 상환 인프라, 명확한 규제, 그리고 선진적인 의료 기술 도입의 혜택을 누리고 있습니다. 공공 및 민간 지출은 고급 의료기기에 대한 보험 적용을 보장하고 시장의 안정을 지원하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 지불 주체별, 2022-2035

제6장 시장 추정 및 예측 : 의료 시설별, 2022-2035

제7장 시장 추정 및 예측 : 지역별, 2022-2035

제8장 기업 개요

KSMThe Global Medical Devices Reimbursement Market was valued at USD 617.6 billion in 2025 and is estimated to grow at a CAGR of 6.5% to reach USD 1.2 trillion by 2035.

The market expansion is driven by rising healthcare expenditures, increasing prevalence of chronic illnesses, and supportive government initiatives promoting access to medical devices. The adoption of value-based healthcare models has also reshaped reimbursement frameworks, emphasizing clinical effectiveness and cost-efficiency. Medical device reimbursement involves compensating healthcare providers, including hospitals, clinics, and surgical centers, for the acquisition, maintenance, and use of devices in diagnosis, monitoring, and treatment. Reimbursement structures are evolving with new payment models, coverage criteria, and market access pathways, creating opportunities for innovative devices that improve patient outcomes and reduce overall healthcare costs. These transformative trends are strengthening the integration of medical devices into modern healthcare systems while ensuring financial sustainability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $617.6 Billion |

| Forecast Value | $1.2 Trillion |

| CAGR | 6.5% |

The private payer segment held a 63.3% share in 2025. Private insurers, employer-sponsored plans, and supplemental policies generally offer faster coverage decisions and more favorable payment rates than public payers. Private coverage is also more likely to include advanced or premium devices. Growth in this segment is supported by rising middle- and high-income populations, particularly in the Asia-Pacific region, where private insurance adoption is increasing.

The hospitals segment accounted for 50.8% share in 2025. Reimbursement in hospitals includes inpatient, outpatient, ambulatory surgical centers, and emergency departments. Growth is fueled by higher surgical volumes, adoption of advanced technologies, and broader reimbursement for complex procedures. Many devices are reimbursed as part of bundled payments, such as procedure fees or diagnosis-related groups, rather than on an individual device basis.

North America Medical Devices Reimbursement Market held 47.2% share in 2025. The U.S. market benefits from a large healthcare economy, established reimbursement infrastructure, regulatory clarity, and advanced adoption of medical technologies. Public and private spending ensures coverage for premium medical devices and supports market stability.

Key players in the Global Medical Devices Reimbursement Market include Allianz, Anthem Insurance Companies, Inc., Aviva, BNP Paribas, Cigna, CVS Health, Experian Health, Humana Inc., Nippon Life Insurance Company, United Health Group, and WellCare Health Plans, Inc. Companies in the Medical Devices Reimbursement Market strengthen their presence through multiple strategies. They focus on expanding private payer partnerships, offering tailored coverage plans for innovative devices, and negotiating favorable payment terms. Investments in digital claims management, real-time reimbursement analytics, and regulatory compliance tools improve operational efficiency. Firms also develop education programs for healthcare providers to increase adoption of reimbursed devices and demonstrate clinical and economic value. Strategic collaborations with hospitals, insurers, and technology providers enhance market penetration, while ongoing monitoring of evolving policies ensures adaptability to new payment models.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Payer trends

- 2.2.3 Healthcare setting trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases

- 3.2.1.2 Adoption of value-based healthcare models

- 3.2.1.3 Growing burden of healthcare cost

- 3.2.1.4 Supportive government programs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complex reimbursement framework

- 3.2.2.2 Underpayment or denial of claims

- 3.2.3 Opportunities

- 3.2.3.1 Growth in remote patient monitoring reimbursement

- 3.2.3.2 Government & private investment in healthcare

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Policy initiatives

- 3.7 Coding systems overview

- 3.8 Reimbursement models outlook

- 3.9 Regional policy differences & harmonization efforts

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Gap analysis

- 3.13 Future market trends

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Payer, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Public

- 5.3 Private

Chapter 6 Market Estimates and Forecast, By Healthcare Setting, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Outpatient facilities

- 6.4 Other settings

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 MEA

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Allianz

- 8.2 Anthem Insurance Companies, Inc.

- 8.3 Aviva

- 8.4 BNP Paribas

- 8.5 Cigna

- 8.6 CVS Health

- 8.7 Experian Health

- 8.8 Humana Inc.

- 8.9 Nippon Life Insurance Company

- 8.10 United Health Group

- 8.11 WellCare Health Plans, Inc.