|

시장보고서

상품코드

1982380

철도 애프터마켓 시장 : 제품별, 구성요소별, 계약 유형별, 보수 유형별, 서비스 프로바이더별, 성장 예측(2026-2035년)Railway Aftermarket Size - By Product, Component, Contract Type, Maintenance Type, Service Provider - Growth Forecast, 2026 - 2035 |

||||||

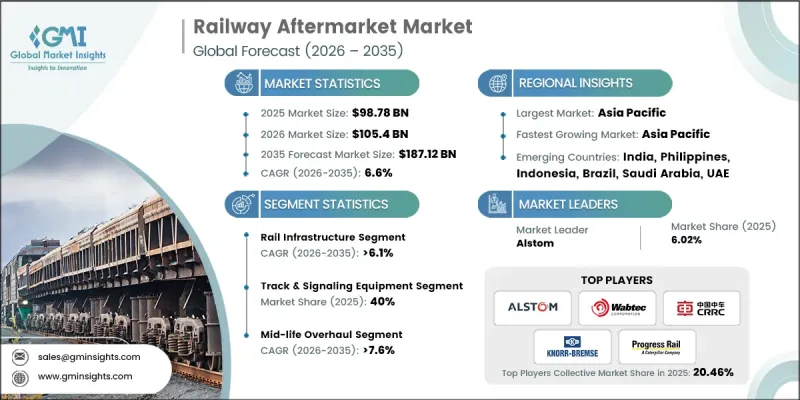

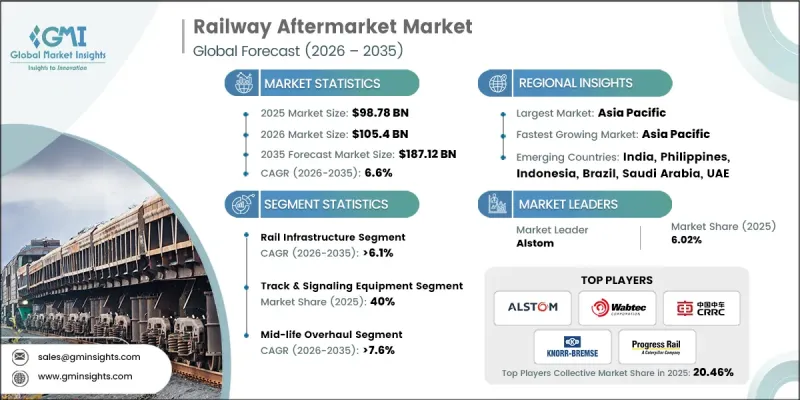

세계의 철도 애프터마켓 시장은 2025년에 987억 8,000만 달러로 평가되었으며, CAGR 6.6%로 성장하여 2035년까지 1,871억 2,000만 달러에 달할 것으로 추정됩니다.

철도 사업자들이 운영 성과, 자산의 수명, 규제 준수에 더 많은 관심을 기울이면서 철도 산업은 구조적 변화를 겪고 있습니다. 전 세계 철도망이 계속 확장되고 차량이 노후화됨에 따라 애프터마켓 서비스는 기존의 예비 부품 공급에서 차량 가동률, 안전 기준 및 총 소유 비용에 직접적인 영향을 미치는 종합적인 라이프사이클 지원 모델로 전환되고 있습니다. 예방적 유지보수 및 예지보전 프레임워크의 채택이 증가함에 따라 조달의 우선순위가 재정의되고 있으며, 철도 사업자들은 내구성, 시스템 호환성 및 성능의 신뢰성에 대해 더 높은 기준을 요구하고 있습니다. 디지털 전환은 이러한 전환을 더욱 가속화하고 있으며, 철도 애프터마켓은 장기적인 인프라 및 차량 관리 계획의 전략적 요소로 자리 매김하고 있습니다. 운행 중단을 최소화하고 유지보수 예산을 최적화해야 한다는 압박이 커지면서 여객 및 화물 철도 부문 모두에서 통합 서비스 계약 및 성과 기반 계약에 대한 수요가 증가하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시시 시장 규모 | 987억 8,000만 달러 |

| 예측액 | 1,871억 2,000만 달러 |

| CAGR | 6.6% |

지속적인 기술 발전으로 철도 애프터마켓의 경쟁 구도가 재편되고 있습니다. 디지털 진단, 상태 모니터링 플랫폼 및 예측 분석 솔루션이 유지보수 전략의 핵심이 되고 있습니다. 현재 주요 구성요소는 데이터 기반 유지보수를 지원하도록 설계되어 운영자가 유지보수 주기를 최적화하고, 다운타임의 위험을 줄이며, 예기치 못한 장비 고장을 줄일 수 있도록 지원합니다. 재료 공학 및 모듈식 제품 아키텍처의 혁신을 통해 열악한 사용 조건에서도 에너지 효율을 향상시키면서 작동 수명을 연장할 수 있게 되었습니다. 업계 전체가 종합적인 라이프사이클 관리 계약으로 전환하면서 애프터마켓은 단순한 거래 기능에서 장기적인 전략적 파트너십 모델로 진화했습니다.

용도별로는 철도 인프라 부문이 2025년 60%의 점유율을 차지했으며, 2035년까지 연평균 6.1%의 성장률을 기록할 것으로 예측됩니다. 인프라의 유지보수는 안전하고 중단 없는 철도 서비스를 보장하기 위해 필수적입니다. 교통량 집중, 자산 노후화 및 운영 부하 증가로 인해 부품의 노후화가 가속화되어 교체 부품, 기술 서비스 및 장기적인 자산 관리 프로그램에 대한 안정적인 수요가 발생하고 있습니다. 사업자들은 서비스 연속성 유지, 규제 프레임워크 준수, 네트워크 성능 유지를 위해 인프라 신뢰성을 최우선 과제로 삼고 있으며, 이 부문이 수익의 주요 원천이 되고 있습니다.

제품 카테고리별로는 선로 및 신호 장비 부문이 2025년 40%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 6.7%의 성장률을 기록할 것으로 전망됩니다. 이러한 시스템은 운행의 안전성, 효율성 및 운행 일정의 정확성을 유지하는 데 필수적입니다. 운영 고도화 및 네트워크 현대화 노력이 진행됨에 따라 지속적인 유지보수, 시스템 업그레이드 및 업데이트의 필요성이 증가하고 있습니다. 규제 당국의 감독과 성능에 대한 기대가 이 부문 전반에 걸쳐 안정적인 애프터마켓 수요를 지속적으로 견인하고 있습니다.

아시아태평양의 철도 애프터마켓은 2025년에 39%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 7.9%의 CAGR을 기록할 것으로 예상됩니다. 철도망의 급속한 확장, 도시 인구 증가, 여객 및 화물 운송량 증가로 인해 이 지역 전체에서 유지보수 솔루션에 대한 수요가 증가하고 있습니다. 현대식 철도 인프라에 대한 지속적인 투자와 더욱 엄격한 운영 표준으로 인해 고급 애프터마켓 서비스와 현지 부품 제조 능력의 도입이 가속화되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 제품별, 2022-2035

제6장 시장 추정 및 예측 : 구성요소별, 2022-2035

제7장 시장 추정 및 예측 : 계약 유형별, 2022-2035

제8장 시장 추정 및 예측 : 보수 유형별, 2022-2035

제9장 시장 추정 및 예측 : 서비스 프로바이더별, 2022-2035

제10장 시장 추정 및 예측 : 지역별, 2022-2035

제11장 기업 개요

KSM 26.04.10The Global Railway Aftermarket was valued at USD 98.78 billion in 2025 and is estimated to grow at a CAGR of 6.6% to reach USD 187.12 billion by 2035.

The industry is experiencing structural evolution as operators place stronger emphasis on operational performance, asset longevity, and regulatory adherence. As global rail networks continue to expand and rolling stock matures, aftermarket services are shifting beyond conventional spare parts supply toward comprehensive lifecycle support models that directly impact fleet availability, safety benchmarks, and total ownership costs. The increasing adoption of preventive and predictive maintenance frameworks is redefining procurement priorities, with rail operators demanding higher standards of durability, system compatibility, and performance reliability. Digital transformation is further accelerating this transition, positioning the railway aftermarket as a strategic component of long-term infrastructure and fleet management planning. Growing pressure to minimize service disruptions and optimize maintenance budgets is reinforcing demand for integrated service agreements and performance-based contracts across both passenger and freight rail segments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $98.78 Billion |

| Forecast Value | $187.12 Billion |

| CAGR | 6.6% |

Ongoing technological progress is reshaping the competitive landscape of the railway aftermarket. Digital diagnostics, condition-based monitoring platforms, and predictive analytics solutions are becoming central to maintenance strategies. Critical components are now engineered to support data-enabled servicing, allowing operators to refine maintenance cycles, lower downtime exposure, and mitigate unexpected equipment failures. Innovations in materials engineering and modular product architecture are extending operational life while supporting improved energy performance under demanding utilization conditions. The industry's shift toward holistic lifecycle management agreements has elevated the aftermarket from a transactional function to a long-term strategic partnership model.

By application, the rail infrastructure segment accounted for 60% share in 2025 and is forecast to grow at a CAGR of 6.1% through 2035. Infrastructure maintenance remains essential to ensuring safe and uninterrupted rail services. High traffic density, aging assets, and heavier operational loads accelerate component degradation, driving consistent demand for replacement parts, technical services, and long-term asset management programs. Operators prioritize infrastructure reliability to maintain service continuity, comply with regulatory frameworks, and preserve network performance, making this segment a dominant revenue contributor.

Within product categories, the track and signaling equipment segment held 40% share in 2025 and is anticipated to grow at a CAGR of 6.7% from 2026 to 2035. These systems are fundamental to maintaining operational safety, efficiency, and scheduling precision. Increasing operational intensity and network modernization initiatives are heightening the need for ongoing maintenance, system upgrades, and replacement programs. Regulatory oversight and performance expectations continue to drive stable aftermarket demand across this segment.

Asia Pacific Railway Aftermarket held 39% share in 2025 and is expected to register a CAGR of 7.9% during 2026-2035. Rapid rail network expansion, urban population growth, and rising passenger and freight volumes are strengthening demand for maintenance solutions across the region. Continued investments in modern rail infrastructure and stricter operational standards are accelerating the adoption of advanced aftermarket services and localized component manufacturing capabilities.

Key participants in the Global Railway Aftermarket include Siemens, Wabtec, Alstom, CRRC, Hitachi Rail, ABB, Knorr-Bremse, Progress Rail Services, CAF, and ZF. Companies operating in the Global Railway Aftermarket are strengthening their market position through digital integration, service portfolio expansion, and long-term contractual partnerships. Industry leaders are investing in predictive maintenance technologies and smart monitoring platforms to deliver higher reliability and performance transparency. Strategic collaborations with rail operators are enabling customized lifecycle service agreements that improve asset uptime and cost predictability. Many firms are expanding regional service networks to enhance responsiveness and localized support capabilities. Product innovation focused on modular design and durability is helping suppliers differentiate their offerings. Additionally, mergers, acquisitions, and targeted investments in advanced manufacturing are being used to broaden technological expertise and secure competitive advantage in high-growth regional markets.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Component

- 2.2.4 Contract Type

- 2.2.5 Maintenance Type

- 2.2.6 Service Provider

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in aging rolling stock requiring replacement and refurbishment.

- 3.2.1.2 Increase in rail network expansion, including metro, high-speed, and freight corridors.

- 3.2.1.3 Surge in government funding and public investment programs for rail modernization.

- 3.2.1.4 Rise in fleet utilization leading to higher maintenance and spare parts demand.

- 3.2.1.5 Increase in adoption of preventive and predictive maintenance strategies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial cost of predictive rail asset maintenance

- 3.2.2.2 Fragmented supply chain in emerging markets

- 3.2.3 Market opportunities

- 3.2.3.1 Surge in adoption of AI and IoT-enabled maintenance and monitoring solutions.

- 3.2.3.2 Rise in localization of aftermarket component manufacturing to reduce lead times.

- 3.2.3.3 Increase in long-term service contracts with rail operators for steady revenue streams.

- 3.2.3.4 Surge in demand in emerging rail markets in Asia-Pacific, Latin America, and Africa.

- 3.2.3.5 Rise in development and adoption of eco-friendly, recyclable, and low-emission aftermarket components.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 United States: Federal Railroad Administration (FRA)

- 3.4.1.2 Canada: Transport Canada Rail Safety Regulations

- 3.4.2 Europe

- 3.4.2.1 EU: Interoperability Directive (EU 2016/797)

- 3.4.2.2 Germany: Eisenbahn-Bau- und Betriebsordnung (EBO)

- 3.4.2.3 UK: Railways (Interoperability) Regulations

- 3.4.2.4 France: Code des Transports

- 3.4.2.5 Italy: Decreto Legislativo 112/1995

- 3.4.3 Asia Pacific

- 3.4.3.1 China: Railway Law of the People’s Republic of China

- 3.4.3.2 India: Indian Railways Safety & Maintenance Standards

- 3.4.3.3 Japan: Railway Business Act

- 3.4.3.4 South Korea: Railroad Safety

- 3.4.3.5 Singapore: LTA Rail Safety and Maintenance Regulations

- 3.4.4 Latin America

- 3.4.4.1 Brazil: National Land Transport Agency (ANTT)

- 3.4.4.2 Mexico: Directorate General of Railways

- 3.4.4.3 Chile: Railway Safety and Maintenance Norms

- 3.4.5 MEA

- 3.4.5.1 UAE: Federal Transport Authority

- 3.4.5.2 Saudi Arabia: Railway Safety Framework under Vision 2030

- 3.4.5.3 South Africa: National Railway Safety Regulator (NRSR)

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Sustainability and environmental impact analysis

- 3.9.1 Sustainable practices

- 3.9.2 Waste reduction strategies

- 3.9.3 Energy efficiency in production

- 3.9.4 Eco-friendly initiatives

- 3.9.5 Carbon footprint considerations

- 3.10 Sustainability and environmental impact analysis

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Future outlook & opportunities

- 3.12 Customer buying behavior & procurement analysis

- 3.12.1 Railway operator procurement processes & decision criteria

- 3.12.2 OEM vs aftermarket purchase decision drivers

- 3.12.3 Total cost of ownership (TCO) evaluation framework

- 3.12.4 Supplier qualification & approval procedures

- 3.12.5 Long-term supply agreements & partnership models

- 3.12.6 Tender & RFP analysis for major railway projects

- 3.12.7 Influence of sustainability & ESG criteria on procurement

- 3.12.8 Regional procurement policy variations

- 3.13 Digitalization & smart rail integration impact

- 3.13.1 IoT-enabled brake pad condition monitoring systems

- 3.13.2 Real-time wear sensor technologies

- 3.13.3 Integration with train management systems (TMS)

- 3.13.4 Big data analytics for predictive replacement

- 3.13.5 Digital twin applications in brake system optimization

- 3.13.6 Blockchain for supply chain traceability

- 3.13.7 Impact of industry 4.0 on manufacturing & distribution

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Rail Infrastructure

- 5.3 Rolling Stock & Locomotives

- 5.3.1 Metro

- 5.3.2 High-Speed Railway (HSR)

- 5.3.3 Light rail & trams

- 5.3.4 Locomotives

- 5.3.5 Passenger coaches

- 5.3.6 Freight wagons

Chapter 6 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Traction & Propulsion Systems

- 6.3 Bogies/Wheelsets & Suspension

- 6.4 Body Structures

- 6.5 Braking Systems

- 6.6 Auxiliary Systems

- 6.7 Track & Signaling Equipment

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By Contract Type, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Long-Term Service Agreements (LTSA)

- 7.3 Annual Maintenance Contracts (AMC)

- 7.4 Pay-Per-Service Model

- 7.5 Performance-Based Contracts (PBC)

Chapter 8 Market Estimates & Forecast, By Maintenance Type, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Scheduled/Preventive Maintenance

- 8.3 Unscheduled/Emergency Maintenance

- 8.4 Mid-Life Overhaul

- 8.5 Full Life-Cycle Maintenance

Chapter 9 Market Estimates & Forecast, By Service Provider, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Railway Operators

- 9.4 Third-Party/Component Suppliers

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Belgium

- 10.3.8 Netherlands

- 10.3.9 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Philippines

- 10.4.7 Indonesia

- 10.4.8 Singapore

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 ABB

- 11.1.2 Alstom

- 11.1.3 Siemens Mobility

- 11.1.4 CRRC

- 11.1.5 Knorr-Bremse

- 11.1.6 Wabtec

- 11.1.7 Hitachi Rail

- 11.1.8 ZF Friedrichshafen

- 11.2 Regional Players

- 11.2.1 Progress Rail Services

- 11.2.2 Strukton Rail

- 11.2.3 Amsted Rail

- 11.2.4 CAF

- 11.2.5 Hyundai Rotem

- 11.2.6 PowerRail

- 11.3 Emerging Players

- 11.3.1 DiMEC Rail Services

- 11.3.2 Precision Roller Bearing Company

- 11.3.3 PowerRail Electronics Technology

- 11.3.4 FreightCar America

- 11.3.5 Motive Equipment