|

시장보고서

상품코드

1998691

철도 물류 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Rail Logistics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

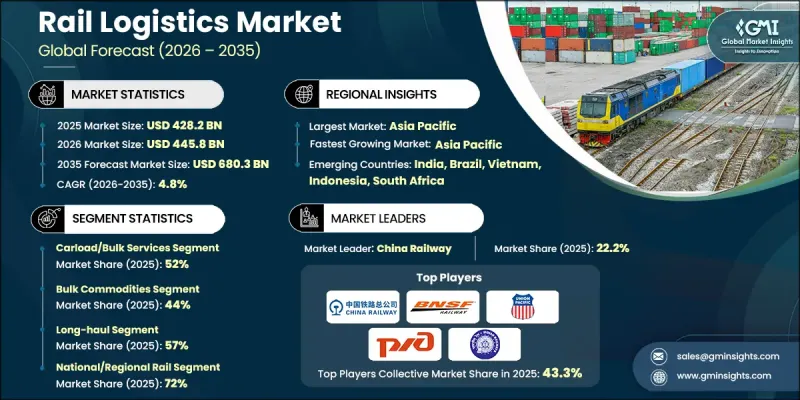

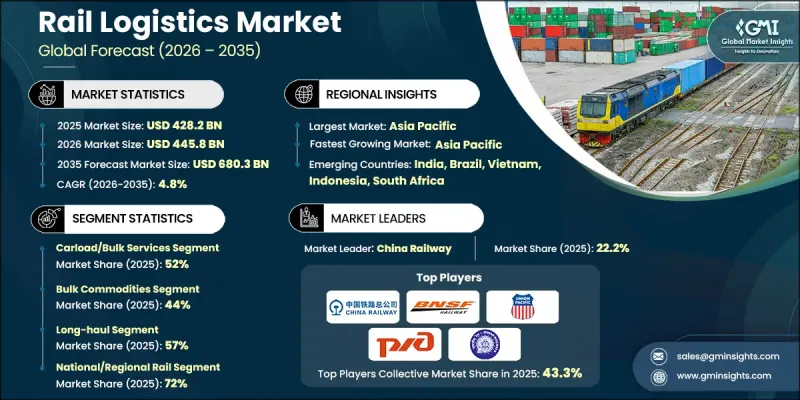

세계의 철도 물류 시장은 2025년에 4,282억 달러로 평가되었고, CAGR 4.8%로 성장하여 2035년까지 6,803억 달러에 달할 것으로 예측됩니다.

철도화물 사업자들은 다양한 운송 수요에 대응할 수 있는 통합 공급망 솔루션을 구축하기 위해 철도 운송과 도로 및 해상 물류를 결합하는 움직임을 강화하고 있습니다. 이러한 멀티모달 접근방식은 업무의 유연성을 높이는 동시에 지역 및 국제 무역 회랑을 가로지르는 화물을 효율적으로 운송할 수 있게 해줍니다. 국경 간 철도 네트워크의 확장은 이용 가능한 화물 노선의 수를 늘리고 생산 기지와 소비 시장 간의 연결성을 향상시킴으로써 세계 공급망을 강화하고 있습니다. 철도 회랑이 확장되고 운영 네트워크의 상호 연결성이 높아짐에 따라 화물 운송업체는 신뢰성을 향상시키면서 더 먼 거리까지 물품을 운송할 수 있게 되었습니다. 세계 물류 네트워크에서 철도의 역할 확대는 철도 인프라 개선, 화물 운송 능력 확대 및 운송 효율성 향상을 위한 투자에 의해 더욱 촉진되고 있습니다. 이러한 추세는 세계 주요 무역로에서 장거리 화물 운송을 위한 비용 효율적이고 환경적으로 지속 가능한 솔루션으로서 철도 화물의 중요성을 더욱 부각시키고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 4,282억 달러 |

| 예측액 | 6,803억 달러 |

| CAGR | 4.8% |

디지털 전환도 철도 물류 시장 재구축에 중요한 역할을 하고 있습니다. 첨단 기술 도입이 진행됨에 따라 사업자는 업무의 가시성을 높이고, 경로 계획의 최적화 및 유지보수 관리를 강화할 수 있게 되었습니다. 철도회사들은 화물의 실시간 추적, 자동 스케줄링, 예지보전 기능을 지원하는 디지털 시스템에 대한 투자를 진행하고 있습니다. 인공지능, 사물인터넷(IoT) 연결, 고급 분석 도구와 같은 기술은 사업자가 화물의 움직임을 보다 효과적으로 모니터링하는 동시에 네트워크의 신뢰성과 업무 효율성을 향상시키는 데 도움을 주고 있습니다. 동시에 철도 화물 인프라에 대한 대규모 투자로 네트워크 용량이 확대되고 화물 운송 속도가 향상되고 있습니다.

2025년에는 차량 단위 운송 및 벌크 화물 서비스 부문이 52%의 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 3.8%를 나타낼 것으로 예측됩니다. 이러한 운송 서비스는 장거리에 걸쳐 대량의 화물을 운송하는 데 필수적인 서비스입니다. 철도 사업자는 전용 화차를 사용하여 대량의 화물을 운송하기 위해 이 화물 운송 모델을 자주 사용하며, 특히 산업 화물 및 대규모 제조 공급망에 적합합니다. 대량 운송이 필요한 산업에서는 광범위한 물류 네트워크를 통해 상품을 효율적으로 운송하기 위해 철도 화물 운송에 의존하는 경우가 많습니다. 벌크 운송 서비스에 대한 안정적인 수요는 안정적인 물동량을 지원하여 철도 회사가 높은 가동률을 유지하면서 비용 효율적인 장거리 물류 솔루션을 제공할 수 있게 해줍니다.

벌크 상품 부문은 2025년 44%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 3.1%를 나타낼 것으로 예측됩니다. 철도 운송은 비용 효율성과 높은 수송 능력으로 인해 대량의 산업 자재 및 원자재를 장거리로 운송하는 데 선호되는 수단으로 남아 있습니다. 벌크 화물 운송은 종종 중량물이나 특수 화물을 포함하기 때문에 많은 양의 화물을 처리할 수 있는 전문적인 운송 인프라가 필요합니다. 철도 사업자는 편성 길이를 연장하고, 적재 용량을 최적화하고, 자동 적재 시스템을 도입하는 등 지속적으로 업무 효율성 향상에 주력하고 있습니다. 이러한 업무 개선을 통해 물류 사업자는 처리 시간을 단축하는 동시에 증가하는 물동량을 보다 효과적으로 처리할 수 있게 되었습니다. 산업 생산 및 에너지 부문의 활동으로 인해 대규모 원자재 운송에 대한 수요가 지속적으로 안정적으로 발생함에 따라 철도 화물 운송 서비스는 세계 물류 네트워크에서 강력한 입지를 계속 유지할 것으로 예측됩니다.

미국 철도 물류 시장은 2025년 915억 달러에 달할 것으로 예상되며, 2026년부터 2035년까지 연평균 4.7%의 성장률을 보일 것으로 예측됩니다. 국내 철도 물류 부문에서 복합운송이 주요 촉진요인으로 부상하고 있습니다. 소매 화물과 디지털 상거래로 인한 배송량이 증가함에 따라 물류 기업들은 철도 운송을 보다 광범위한 공급망 업무에 통합하도록 유도하고 있습니다. 복합운송을 통해 화물이 항만, 철도 터미널, 라스트마일 배송 네트워크 사이를 효율적으로 이동할 수 있게 되어 대량의 컨테이너를 처리할 수 있는 원활한 유통 시스템이 구축되어 있습니다. 철도 사업자들도 실시간 화물 추적, 지능형 스케줄링 시스템, 예측 분석을 지원하는 첨단 기술에 투자하여 업무 효율성을 높이고 있습니다. 이러한 기술적 기능은 운송 지연을 줄이고 복잡한 물류 네트워크에서 화물 이동을 최적화하는 데 기여하며, 진화하는 화물 인프라에서 철도 운송의 역할을 강화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 서비스별, 2022-2035

제6장 시장 추산 및 예측 : 화물별, 2022-2035

제7장 시장 추산 및 예측 : 거리별, 2022-2035

제8장 시장 추산 및 예측 : 최종 용도별, 2022-2035

제9장 시장 추산 및 예측 : 철도별, 2022-2035

제10장 시장 추산 및 예측 : 지역별, 2022-2035

제11장 기업 개요

LSH 26.04.23The Global Rail Logistics Market was valued at USD 428.2 billion in 2025 and is estimated to grow at a CAGR of 4.8% to reach USD 680.3 billion by 2035.

Rail freight operators are increasingly combining rail transport with road and maritime logistics to create integrated supply chain solutions capable of supporting diverse shipping requirements. This multimodal approach improves operational flexibility while enabling cargo to move efficiently across regional and international trade corridors. Expanding cross-border rail networks are strengthening global supply chains by increasing the number of available freight routes and improving connectivity between production centers and consumption markets. As rail corridors expand and operational networks become more interconnected, freight operators are able to deliver goods across longer distances with improved reliability. The growing role of rail within global logistics networks is further supported by investments aimed at improving rail infrastructure, expanding freight capacity, and enhancing transportation efficiency. These developments are reinforcing the importance of rail freight as a cost-effective and environmentally sustainable solution for long-distance cargo transportation across major global trade routes.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $428.2 Billion |

| Forecast Value | $680.3 Billion |

| CAGR | 4.8% |

Digital transformation is also playing a significant role in reshaping the rail logistics market. Increasing adoption of advanced technologies is enabling operators to improve operational visibility, optimize route planning, and enhance maintenance management. Rail companies are investing in digital systems that support real-time freight tracking, automated scheduling, and predictive maintenance capabilities. Technologies such as artificial intelligence, Internet of Things connectivity, and advanced analytics tools are helping operators monitor freight movement more effectively while improving network reliability and operational efficiency. In parallel, large-scale investments in rail freight infrastructure are expanding network capacity and enabling faster cargo movement.

The carload and bulk freight services segment held 52% share in 2025 and is projected to grow at a CAGR of 3.8% between 2026 and 2035. These transportation services remain essential for moving large volumes of goods over long distances. Rail operators frequently rely on this freight model to transport substantial cargo loads in dedicated railcars, making it particularly suitable for industrial shipments and large-scale manufacturing supply chains. Industries requiring high-volume transportation often depend on rail freight to move goods efficiently across extensive logistics networks. The consistent demand for bulk transportation services supports stable freight volumes, enabling rail companies to maintain strong utilization rates while delivering cost-effective long-distance logistics solutions.

The bulk commodities segment captured 44% share in 2025 and is expected to grow at a CAGR of 3.1% from 2026 to 2035. Rail transportation remains a preferred solution for moving large quantities of industrial and raw materials across long distances due to its cost efficiency and high capacity. Bulk freight shipments often involve heavy cargo that requires specialized transportation infrastructure capable of handling substantial loads. Rail operators are continuously focusing on improving operational efficiency by increasing train lengths, optimizing cargo capacity, and implementing automated loading systems. These operational improvements are helping reduce turnaround times while enabling logistics providers to handle growing freight volumes more effectively. As industrial production and energy sector activities continue to generate consistent demand for large-scale raw material transportation, rail freight services are expected to maintain a strong presence within global logistics networks.

United States Rail Logistics Market reached USD 91.5 billion in 2025 and is expected to grow at a CAGR of 4.7% between 2026 and 2035. Intermodal freight transportation is emerging as a key growth driver within the country's rail logistics sector. The increasing volume of retail shipments and digital commerce deliveries is encouraging logistics companies to integrate rail transportation into broader supply chain operations. Intermodal transportation allows cargo to move efficiently between ports, rail terminals, and last-mile delivery networks, creating a seamless distribution system capable of handling large container volumes. Rail operators are also investing in advanced technologies that support real-time shipment tracking, intelligent scheduling systems, and predictive analytics to improve operational efficiency. These technological capabilities help reduce transit delays and optimize freight movement across complex logistics networks, strengthening the role of rail transportation in the country's evolving freight infrastructure.

Major companies operating in the Global Rail Logistics Market include BNSF Railway, Canadian National Railway, Canadian Pacific Kansas City, China Railway, CSX Transportation, Deutsche Bahn (DB Cargo), Indian Railways, Norfolk Southern, Russian Railways (RZD), and Union Pacific. Companies participating in the Global Rail Logistics Market are implementing several strategic initiatives to strengthen their market positions and expand operational capabilities. Rail operators are investing in infrastructure modernization programs to improve network capacity, enhance freight handling capabilities, and support higher cargo volumes. Many companies are also focusing on digital transformation by deploying advanced technologies such as AI-based scheduling systems, predictive maintenance tools, and real-time cargo monitoring platforms to optimize operational performance. Strategic partnerships with shipping companies, port authorities, and logistics providers are helping rail operators develop integrated multimodal transportation solutions that enhance supply chain efficiency. Additionally, companies are prioritizing sustainability initiatives by improving fuel efficiency and adopting environmentally responsible freight transportation practices to align with evolving regulatory standards and customer expectations.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Service

- 2.2.3 Cargo

- 2.2.4 Distance

- 2.2.5 End use

- 2.2.6 Rail

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Rail infrastructure providers

- 3.1.2 Rolling Stock Manufacturers

- 3.1.3 Service Operators

- 3.1.4 Terminal & Transloading Facilities

- 3.1.5 Technology & Software Provider

- 3.1.6 End user

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing intermodal transportation demand

- 3.2.1.2 Increasing e-commerce and retail shipments

- 3.2.1.3 Government investment in dedicated freight corridors

- 3.2.1.4 Rising need for cost-efficient and sustainable transport

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High infrastructure maintenance costs

- 3.2.2.2 Regulatory and cross-border challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Digitalization and IoT-enabled rail solutions

- 3.2.3.2 Expansion in emerging markets (India, Africa)

- 3.2.3.3 Adoption of green and electrified locomotives

- 3.2.3.4 Integration with 3PL and multimodal logistics networks

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Federal Railroad Administration (FRA)

- 3.4.1.2 Association of American Railroads (AAR)

- 3.4.2 Europe

- 3.4.2.1 European Union Agency for Railways (ERA)

- 3.4.2.2 International Union of Railways (UIC)

- 3.4.3 Asia Pacific

- 3.4.3.1 Ministry of Railways (India)

- 3.4.3.2 Japan Transport Safety Board / JR Standards

- 3.4.4 Latin America

- 3.4.4.1 Agencia Nacional de Transportes Terrestres (ANTT, Brazil)

- 3.4.4.2 Comision Nacional de Transporte Ferroviario (Mexico)

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE Federal Transport Authority - Railways

- 3.4.5.2 Saudi Railways Organization / Standards Authority

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Patent analysis (Driven by primary research)

- 3.7.1 Patent Filing Trends by Technology Area

- 3.7.2 Key Patent Holders & IP Positioning

- 3.7.3 Emerging Technology Patent Activity

- 3.8 Technology and innovation landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Pricing Analysis (Driven by primary research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.9.3 Rate Structure by Service Type (Intermodal vs Carload)

- 3.9.4 Fuel Surcharge Mechanisms

- 3.9.5 Demurrage & Accessorial Charges

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis (Driven by primary research)

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Trade Data Analysis (Driven by paid database)

- 3.13.1 Import/export volume & value trends

- 3.13.2 Key trade corridors & tariff impact

- 3.13.3 Cross-border rail freight flows

- 3.14 Impact of AI & Generative AI on the Market

- 3.14.1 AI-Driven Disruption of Existing Business Models

- 3.14.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.14.3 Risks, limitations & regulatory considerations

- 3.15 Service delivery capacity & provider infrastructure (Driven by primary research)

- 3.15.1 Provider network density & coverage by region

- 3.15.2 Capacity gaps & addressable demand mismatch

- 3.16 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.16.1 Base Case - key macro & industry variables driving CAGR

- 3.16.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.16.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Service, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Intermodal services

- 5.3 Carload/bulk services

- 5.4 Transloading services

Chapter 6 Market Estimates & Forecast, By Cargo, 2022 - 2035 ($Mn, Tons)

- 6.1 Key trends

- 6.2 Bulk commodities

- 6.2.1 Minerals & ores

- 6.2.2 Coal

- 6.2.3 Grains & agricultural products

- 6.3 Containerized cargo

- 6.3.1 Consumer goods

- 6.3.2 Electronics

- 6.3.3 Machinery & equipment

- 6.4 Specialized cargo

- 6.4.1 Automotive

- 6.4.2 Pharmaceuticals & chemicals

- 6.4.3 Refrigerated/perishable goods

Chapter 7 Market Estimates & Forecast, By Distance, 2022 - 2035 ($Mn, Tons)

- 7.1 Key trends

- 7.2 Short haul

- 7.3 Medium-haul

- 7.4 Long-haul

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Mn, Tons)

- 8.1 Key trends

- 8.2 Mining

- 8.3 Agriculture

- 8.4 Energy

- 8.5 Manufacturing

- 8.6 Construction

- 8.7 Retail

- 8.8 Automotive

- 8.9 Chemical

- 8.10 Food & beverages

- 8.11 Others

Chapter 9 Market Estimates & Forecast, By Rail, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 National/regional rail

- 9.3 High-speed rail logistics

- 9.4 Dedicated freight corridors

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.3.8 Poland

- 10.3.9 Romania

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Vietnam

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Egypt

Chapter 11 Company Profiles

- 11.1 Global companies

- 11.1.1 BNSF Railway

- 11.1.2 Canadian National Railway (CN)

- 11.1.3 Canadian Pacific Kansas City (CPKC)

- 11.1.4 China Railway Freight

- 11.1.5 CSX Transportation

- 11.1.6 Deutsche Bahn (DB Cargo)

- 11.1.7 Indian Railways

- 11.1.8 Norfolk Southern Railway

- 11.1.9 Russian Railways (RZD)

- 11.1.10 Union Pacific Railroad

- 11.2 Regional players

- 11.2.1 Aurizon

- 11.2.2 Euro Cargo Rail

- 11.2.3 Ferromex

- 11.2.4 Genesee & Wyoming

- 11.2.5 Kansas City Southern

- 11.2.6 OBB Rail Cargo

- 11.2.7 PKP Cargo

- 11.3 Emerging players

- 11.3.1 Japan Freight Railway Company

- 11.3.2 SNCF Logistics

- 11.3.3 VTG