|

시장보고서

상품코드

1998714

플랜지 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Flanges Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

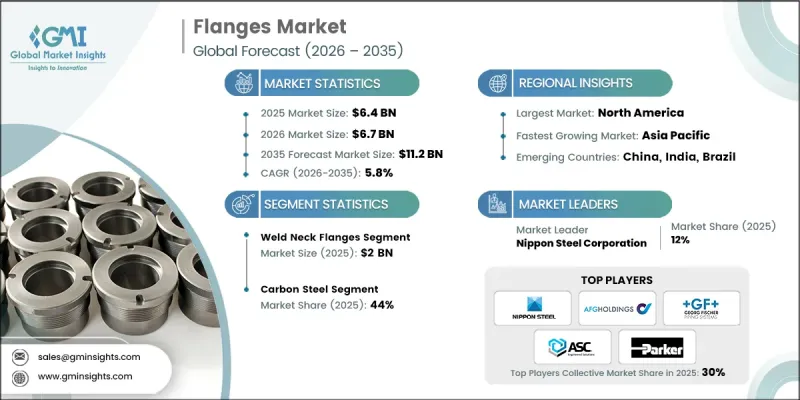

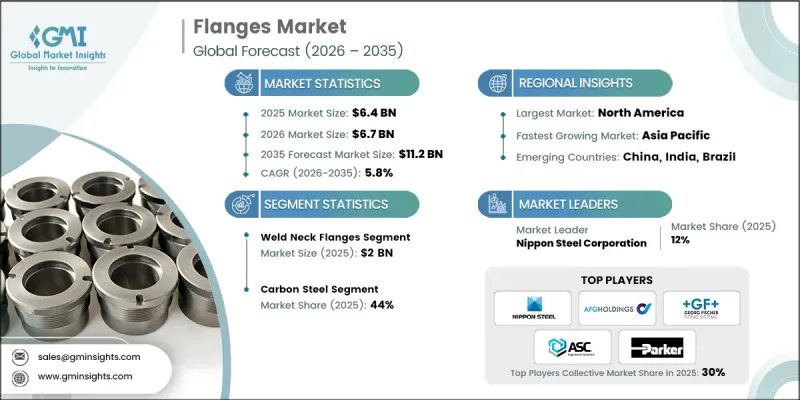

세계의 플랜지 시장은 2025년에 64억 달러로 평가되며, CAGR 5.8%로 성장하며, 2035년까지 112억 달러에 달할 것으로 추정되고 있습니다.

플랜지는 유체 및 가스 수송 시스템에서 파이프, 밸브, 펌프 및 기타 장비를 연결하는 데 사용되는 필수적인 기계 부품으로 산업 인프라에서 매우 중요한 역할을 합니다. 구조는 단순하지만 파이프라인 정렬 유지, 구조적 강도 보장, 유지보수 접근 용이성 등 중요한 기능을 제공합니다. 파이프라인에 의존하는 분야에서는 다양한 압력, 온도 및 환경 조건에서 작동할 수 있는 신뢰할 수 있는 연결 시스템이 필요하므로 플랜지에 대한 수요는 전 세계 산업 활동의 추세와 밀접하게 연동되어 있습니다. 최종사용자는 열악한 환경에서도 안정적으로 작동하는 내구성 있고 고성능의 플랜지를 공급할 수 있는 제조업체를 선호하는 경우가 많습니다. 이에 따라 제조업체는 진화하는 업계의 요구 사항을 충족시키기 위해 생산 기술의 정교화, 재료 품질 향상, 제품 라인업의 확장을 점점 더 많이 추진하고 있습니다. 또한 공급망 강화를 위해 지속가능한 제조 방식을 도입하고 원재료 조달을 다각화하여 공급망을 강화하기 위해 노력하고 있습니다. 또한 신흥 국가에서의 산업 활동의 확대는 플랜지 제조업체에게 새로운 기회를 창출하고 세계 시장의 전반적인 확대에 기여하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 64억 달러 |

| 예측액 | 112억 달러 |

| CAGR | 5.8% |

2025년 현재 용접 목 플랜지 부문은 20억 달러를 차지했습니다. 그 장점은 우수한 기계적 강도, 고압에 대한 내성 및 높은 피로 저항에 기인합니다. 긴 테이퍼형 허브 설계로 파이프와 플랜지 사이에 응력이 균등하게 분산되어 용접 조인트 부분의 응력 집중을 최소화할 수 있습니다. 이러한 구조적 장점으로 인해 용접 넥 플랜지는 고압, 고온 또는 변동 하중에서 작동하는 가혹한 파이프라인 시스템에 적합합니다. 신뢰성과 내구성으로 인해 이 플랜지는 조인트의 무결성과 작동 안전이 필수적인 중요한 산업 파이프라인 네트워크에서 널리 사용되고 있습니다. 다른 플랜지 유형에 비해 용접 넥 유형은 특히 대구경 또는 두꺼운 벽 두께의 파이프라인에서 더 견고하고 신뢰할 수 있는 연결을 제공합니다.

2025년 기준, 탄소강 플랜지 시장 점유율은 44%를 차지했습니다. 그 강력한 존재감은 주로 가성비와 균형 잡힌 기계적 특성에 기인합니다. 탄소강은 스테인리스강이나 니켈 합금 대체품에 비해 내구성, 강도, 경제성이라는 실용적인 조합을 제공합니다. 낮은 비용으로 인해 탄소강은 예산 효율성을 유지하면서 대량의 플랜지를 필요로 하는 대규모 산업 프로젝트에서 여전히 선호되는 재료입니다. 산업계에서는 저압에서 중간 정도의 압력 및 온도 조건에서 작동하는 배관 시스템에 탄소강 플랜지가 일반적으로 채택되어 여러 산업 분야에서 널리 사용되고 있습니다.

미국 플랜지 시장은 83%의 점유율을 차지하고 있으며, 2025년에는 14억 달러 규모에 도달할 것으로 예측됩니다. 이 지역 시장은 탄탄한 산업 기반, 엄격한 규제 기준, 공정 산업 및 에너지 인프라에 대한 지속적인 투자의 혜택을 누리고 있습니다. 에너지 생산, 파이프라인 확장, 시설 현대화와 관련된 지속적인 활동이 플랜지에 대한 지속적인 수요에 기여하고 있습니다. 또한 산업 및 지자체 시스템 전반의 인프라 노후화로 인해 유지보수, 수리 및 교체에 대한 수요가 꾸준히 발생하고 있습니다. 엄격한 기술 표준을 준수하여 열악한 작업 환경에서도 안정적으로 작동하는 고품질 단조 플랜지 및 합금 플랜지의 사용을 촉진합니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 제품 유형별, 2022-2035

제6장 시장 추산·예측 : 압력·온도별, 2022-2035

제7장 시장 추산·예측 : 재료별, 2022-2035

제8장 시장 추산·예측 : 제조 프로세스별, 2022-2035

제9장 시장 추산·예측 : 최종사용자별, 2022-2035

제10장 시장 추산·예측 : 유통 채널별, 2022-2035

제11장 시장 추산·예측 : 지역별, 2022-2035

제12장 기업 개요

KSA 26.04.20The Global Flanges Market was valued at USD 6.4 billion in 2025 and is estimated to grow at a CAGR of 5.8% to reach USD 11.2 billion by 2035.

Flanges play a critical role in industrial infrastructure as essential mechanical components used to connect pipes, valves, pumps, and other equipment within fluid and gas transport systems. Although simple in structure, they provide vital functions such as maintaining pipeline alignment, ensuring structural strength, and enabling easy maintenance access. The demand for flanges closely follows the pace of industrial activity worldwide, as sectors relying on pipelines require reliable connection systems capable of operating under varying pressure, temperature, and environmental conditions. End users often prioritize suppliers that can deliver durable, high-performance flanges capable of functioning consistently in demanding environments. In response, manufacturers are increasingly refining production techniques, improving material quality, and expanding product portfolios to meet evolving industry requirements. Efforts are also being made to incorporate sustainable manufacturing practices and diversify raw material sourcing to strengthen supply chains. In addition, expanding industrial activity in emerging economies is creating new opportunities for flange manufacturers, contributing to the overall expansion of the global market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.4 Billion |

| Forecast Value | $11.2 Billion |

| CAGR | 5.8% |

The weld neck flanges segment accounted for USD 2 billion in 2025. Their dominance is attributed to their superior mechanical strength, ability to handle high pressure, and strong resistance to fatigue. The long tapered hub design distributes stress evenly between the pipe and the flange, minimizing stress concentration at welded joints. This structural advantage makes weld neck flanges suitable for demanding pipeline systems that operate under high pressure, high temperature, or fluctuating loads. Because of their reliability and durability, these flanges are widely used in critical industrial pipeline networks where joint integrity and operational safety are essential. Compared with other flange types, weld neck variants deliver stronger and more dependable connections, particularly in pipelines with large diameters or thicker pipe walls.

The carbon steel flanges segment held 44% share in 2025. Their strong presence is mainly due to their cost-effectiveness and balanced mechanical properties. Carbon steel offers a practical combination of durability, strength, and affordability compared to stainless steel or nickel alloy alternatives. Because of its lower cost, carbon steel remains the preferred material for large-scale industrial projects that require high volumes of flanges while maintaining budget efficiency. Industries commonly rely on carbon steel flanges for piping systems operating under low to moderate pressure and temperature conditions, making them widely used across multiple industrial sectors.

United States Flanges Market held 83% share, generating USD 1.4 billion in 2025. The regional market benefits from a well-established industrial base, strict regulatory standards, and continuous investments in process industries and energy infrastructure. Ongoing activity related to energy production, pipeline expansion, and facility modernization contributes to sustained demand for flanges. Additionally, aging infrastructure across industrial and municipal systems creates steady maintenance, repair, and replacement requirements. Compliance with stringent technical standards encourages the use of high-quality forged and alloy flanges capable of performing reliably in demanding operational environments.

Prominent companies operating in the Global Flanges Market include Nippon Steel Corporation, Parker Hannifin, Georg Fischer (GF Piping Systems), Alleima, AFG Holdings (Ameriforge), ASC Engineered Solutions, Viraj Profiles Pvt. Ltd., Texas Flange, Bonney Forge, Metalfar S.p.A., Flanschenwerk Bebitz GmbH, Victaulic, General Flange & Forge LLC, Coastal Flange, and JFE Steel Corporation. Companies in the Flanges Market strengthen their competitive position through continuous investment in advanced manufacturing technologies and material innovation. Many manufacturers focus on improving product durability, corrosion resistance, and pressure tolerance to meet strict industrial requirements. Strategic partnerships with engineering contractors, industrial operators, and distributors help expand market reach and secure long-term supply agreements. Firms also enhance their supply chains to ensure consistent raw material availability and efficient production. Geographic expansion into emerging industrial markets further supports revenue growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 regional

- 2.2.2 product type

- 2.2.3 pressure temperature

- 2.2.4 material

- 2.2.5 manufacturing process

- 2.2.6 end use sector

- 2.2.7 distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of energy and process industries

- 3.2.1.2 Growth in infrastructure and industrial construction

- 3.2.1.3 Replacement and maintenance of aging assets

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Volatility in raw material prices

- 3.2.2.2 Stringent regulatory and quality compliance

- 3.2.3 Opportunities

- 3.2.3.1 Growth of energy transition and hydrogen infrastructure

- 3.2.3.2 Increasing demand for high-specification and custom flanges

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Major market trends and Disruptions

- 3.5 Future market trends

- 3.6 Risk and mitigation Analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 by product type

- 3.9 Regulatory landscape

- 3.9.1 Standards and compliance requirement

- 3.9.2 Certification standards

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022-2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Weld neck flanges

- 5.3 Slip-on flanges

- 5.4 Blind flanges

- 5.5 Socket weld flanges

- 5.6 Lap joint flanges

- 5.7 Threaded flanges

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Pressure Temperature, 2022-2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Low

- 6.3 Medium

- 6.4 High

- 6.5 Extreme

Chapter 7 Market Estimates & Forecast, By Material, 2022-2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Stainless steel

- 7.3 Alloy steel

- 7.4 Nickel alloy

- 7.5 Carbon steel

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Manufacturing Process, 2022-2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Forged

- 8.3 Cast

- 8.4 Fabricated

Chapter 9 Market Estimates & Forecast, By End User, 2022-2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Oil & gas

- 9.3 Chemical & petrochemical processing

- 9.4 Power generation

- 9.5 Water & wastewater treatment

- 9.6 Pulp & paper

- 9.7 Pharmaceuticals

- 9.8 Food & beverage processing

- 9.9 Mining & metals

- 9.10 General manufacturing

- 9.11 Others

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Argentina

- 11.5.3 Mexico

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Nippon Steel Corporation

- 12.2 Georg Fischer (GF Piping Systems)

- 12.3 Parker Hannifin

- 12.4 AFG Holdings (Ameriforge)

- 12.5 ASC Engineered Solutions

- 12.6 Alleima

- 12.7 Viraj Profiles Pvt. Ltd.

- 12.8 Texas Flange

- 12.9 Bonney Forge

- 12.10 Metalfar S.p.A.

- 12.11 Flanschenwerk Bebitz GmbH

- 12.12 Victaulic

- 12.13 General Flange & Forge LLC

- 12.14 Coastal Flange

- 12.15 JFE STEEL CORPORATION