|

시장보고서

상품코드

1998776

토마토 가공 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Tomato Processing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

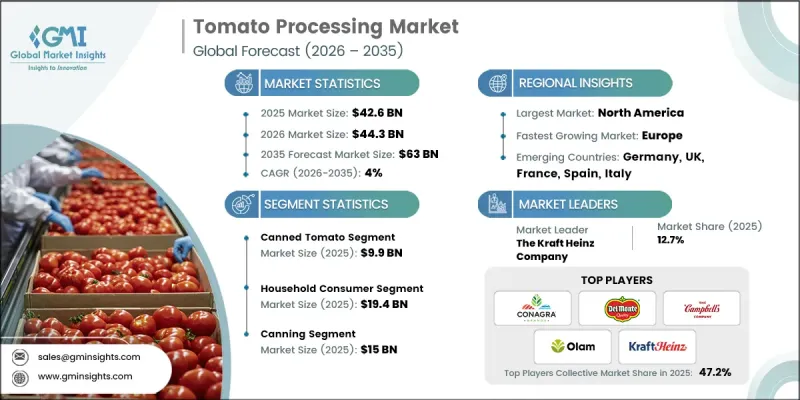

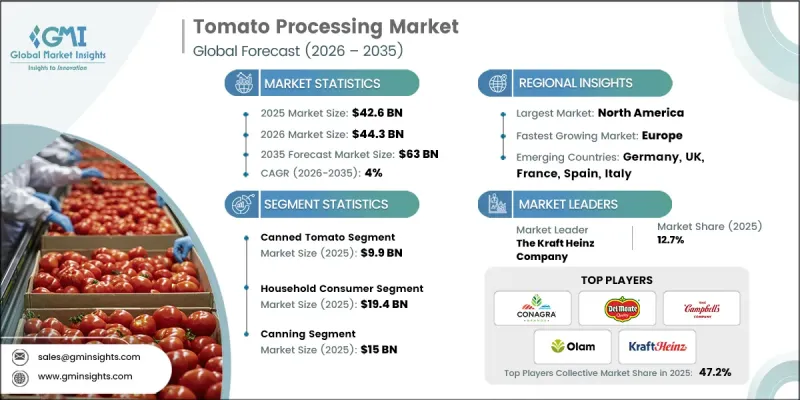

세계의 토마토 가공 시장은 2025년에 426억 달러로 평가되었고, CAGR 4%로 성장하여 2035년까지 630억 달러에 달할 것으로 예측됩니다.

이 시장은 선별, 세척, 세척, 껍질 벗기기, 과육화, 농축, 포장 등의 공정을 거쳐 생산되는 소스, 페이스트, 주스, 주스, 케첩, 통조림 토마토 등 토마토 가공품에 대한 수요 증가에 힘입어 성장세를 보이고 있습니다. 이러한 공정은 저장 기간을 연장하고, 영양가를 유지하며, 식품의 안전성을 보장하는 동시에 수확 후 손실을 줄여 연중 공급을 가능하게 합니다. 토마토 가공을 통해 상하기 쉬운 생토마토를 상업적으로 가치 있고 유용한 제품으로 바꿀 수 있습니다. 이 산업에는 기계적, 열적, 화학적 가공 기술을 채택하는 소규모 시설부터 대규모 자동화 플랜트까지 다양한 시설이 포함되어 있습니다. 토마토 생산이 과잉인 지역에서는 가공이 계절적 변동을 관리하고, 폐기물을 최소화하며, 소비자 수요에 안정적으로 대응하는 데 있어 매우 중요한 역할을 합니다. 또한, 건강 인식 증가, 도시화, 소매 및 전자상거래 네트워크의 확장으로 인해 업계가 더욱 강화되고 있으며, 가공 토마토 제품은 세계 식품 부문에서 필수적인 요소로 자리 잡고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 426억 달러 |

| 예측액 | 630억 달러 |

| CAGR | 4% |

통조림 부문은 장기 보관이 가능하고, 제품의 안전성을 유지하며, 소비자와 소매업체 모두에게 편리함을 제공한다는 점에서 2025년 150억 달러 규모 시장 규모를 형성했습니다. 통조림 외에도 소스 및 주스 제조, 농축, 건조, 냉동, 발효 등 다양한 가공 방법을 통해 다양한 제품 유형과 소비자 기호에 대응하고 있습니다. 가정과 외식 산업에서 바로 조리할 수 있는 간편식 재료에 대한 수요가 증가함에 따라 소스 및 페이스트 생산은 계속 확대되고 있습니다. 주스 추출은 식단에서 영양소 보존, 천연 맛, 기능적 이점을 중시하는 건강 지향적 소비자들로부터 지지를 받고 있습니다.

가정 소비자 부문은 건강한 식습관에 대한 인식이 높아지고, 즉시 사용할 수 있는 편리한 제품에 대한 선호도가 높아지면서 2025년에는 194억 달러에 달했습니다. 가정에서는 일관된 품질, 영양, 맛을 제공하면서 식사 준비를 간소화할 수 있는 토마토 기반 제품이 요구되고 있습니다. 가정 외에도 식품 가공업체, 레스토랑, 음료 산업이 시장을 주도하고 있습니다. 이들 부문은 고객 수요를 효율적으로 충족시키기 위해 안정적인 원료 품질, 생산 확장성, 안정적인 공급망을 갖춘 토마토 가공품에 의존하고 있습니다.

미국의 토마토 가공 시장은 편리하고 건강하며 고품질의 토마토 제품에 대한 소비자의 강력한 수요에 힘입어 2025년 116억 달러 규모에 달했습니다. 영양을 해치지 않으면서도 빠른 조리를 중시하는 라이프스타일의 변화로 가정에서 소스, 페이스트, 주스의 소비가 급증하고 있습니다. 현대적인 소매 인프라, 효율적인 전자상거래 플랫폼, 첨단 유통 네트워크가 도시터 시골까지 토마토 가공품의 원활한 배송을 지원하고 있습니다. 가공 및 포장 효율화에 대한 투자는 제품의 품질과 일관성을 보장하는 한편, 콜드체인 및 유통기한 연장과 관련된 기술 혁신은 공급 안정성을 더욱 강화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품별, 2022-2035

제6장 시장 추산 및 예측 : 가공 방법별, 2022-2035

제7장 시장 추산 및 예측 : 최종 용도별, 2022-2035

제8장 시장 추산 및 예측 : 유통 채널별, 2022-2035

제9장 시장 추산 및 예측 : 지역별, 2022-2035

제10장 기업 개요

LSH 26.04.23The Global Tomato Processing Market was valued at USD 42.6 billion in 2025 and is estimated to grow at a CAGR of 4% to reach USD 63 billion by 2035.

The market is driven by the rising demand for processed tomato products such as sauces, pastes, juices, ketchup, and canned tomatoes, which are produced through operations like sorting, washing, peeling, pulping, concentrating, and packaging. These processes extend shelf life, preserve nutritional value, and ensure food safety, while reducing post-harvest losses and providing year-round availability. Tomato processing enables the transformation of perishable raw tomatoes into commercially viable, convenient products. The industry encompasses a mix of small-scale facilities and large automated plants that employ mechanical, thermal, and chemical processing techniques. In regions with surplus tomato production, processing plays a critical role in managing seasonal fluctuations, minimizing waste, and meeting consumer demand consistently. The industry is further reinforced by growing health awareness, urbanization, and the expansion of retail and e-commerce networks, making processed tomato products an essential component of the global food sector.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $42.6 Billion |

| Forecast Value | $63 Billion |

| CAGR | 4% |

The canning segment generated USD 15 billion in 2025, owing to its ability to provide long shelf life, maintain product safety, and offer convenience for consumers and retailers alike. Alongside canning, other processing methods, such as sauce and juice production, concentration, drying, freezing, and fermentation, cater to diverse product types and consumer preferences. Sauce and paste production continue to expand as demand rises for ready-to-use and easy-to-cook ingredients in households and foodservice channels. Juice extraction has gained traction with health-conscious consumers who prioritize nutrient retention, natural flavor, and functional benefits in their diets.

The household consumer segment reached USD 19.4 billion in 2025, driven by rising awareness about healthy diets and the increasing preference for ready-to-use, convenient products. Households are seeking tomato-based items that simplify meal preparation while delivering consistent quality, nutrition, and taste. Beyond households, industrial food processors, restaurants, and the beverage industry are substantial contributors to the market. These segments rely on processed tomato products for consistent ingredient quality, scalability in production, and reliable supply chains to meet customer demand efficiently.

U.S. Tomato Processing Market accounted for USD 11.6 billion in 2025, underpinned by strong consumer demand for convenient, healthy, and high-quality tomato products. Household consumption of sauces, pastes, and juices has surged due to evolving lifestyles that prioritize time-saving meal solutions without compromising nutrition. Modern retail infrastructure, efficient e-commerce platforms, and advanced distribution networks support the seamless delivery of processed tomato products across urban and rural areas. Investments in processing and packaging efficiency ensure product quality and consistency, while technological innovations in cold chain and shelf-life extension reinforce supply stability.

Prominent players in the Global Tomato Processing Market include Del Monte Foods, Inc., Campbell Soup Company, ConAgra Brands, Inc., Dabur, Erregi s.r.l., General Mills, Inc., Mutti S.p.A., Neil Jones Food Company, Mizkan Americas, Pacific Coast Producers, and Kraft Heinz Inc. Companies in the Global Tomato Processing Market are leveraging several strategies to strengthen market presence and expand their foothold. Key approaches include investment in advanced processing and packaging technologies to enhance product quality and shelf life, adoption of automated manufacturing systems to improve efficiency, and expansion into emerging markets to capture new consumer bases. Firms are also focusing on product diversification with health-oriented, organic, and convenient tomato-based offerings. Strategic partnerships with distributors, retailers, and e-commerce platforms enable wider market reach, while branding and marketing initiatives drive consumer loyalty. Sustainability practices, such as reducing post-harvest losses and eco-friendly packaging, are also being employed to enhance competitiveness and align with growing consumer and regulatory expectations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product

- 2.2.2 Processing Method

- 2.2.3 End Use

- 2.2.4 Distribution Channel

- 2.2.5 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global demand for processed tomato products

- 3.2.1.2 Technological advancements enhancing efficiency and quality

- 3.2.1.3 Expansion of retail, foodservice, and distribution channels

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Price volatility and supply fluctuations of raw tomatoes

- 3.2.2.2 Intense competition and brand saturation in market

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for health-oriented and organic products

- 3.2.3.2 Utilization of byproducts for additional revenue streams

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Tomato paste

- 5.3 Tomato puree

- 5.4 Canned tomatoes

- 5.5 Tomato sauces

- 5.6 Tomato ketchup

- 5.7 Tomato juice & concentrate

- 5.8 Dried tomatoes & powder

- 5.9 Others

Chapter 6 Market Estimates and Forecast, By Processing Method, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Canning

- 6.3 Sauce production

- 6.4 Juice extraction

- 6.5 Concentration

- 6.6 Drying

- 6.7 Freezing

- 6.8 Fermentation

- 6.9 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Household consumers

- 7.3 Industrial food processors

- 7.4 Restaurants & foodservice

- 7.5 Beverage industry

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Hypermarkets & supermarkets

- 8.3 Food Specialty Stores

- 8.4 Convenience Stores

- 8.5 Online/E-commerce

- 8.6 Direct Sales

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Campbell Soup Company

- 10.2 ConAgra Brands, Inc.

- 10.3 Dabur

- 10.4 Del Monte Foods, Inc.

- 10.5 Erregi s.r.l.

- 10.6 General Mills, Inc.

- 10.7 Mutti S.p.A.

- 10.8 Neil Jones Food Company

- 10.9 Olam International

- 10.10 Pacific Coast Producers

- 10.11 The Kraft Heinz Company