|

시장보고서

상품코드

2019199

베이비 케어용 포장 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Baby Care Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

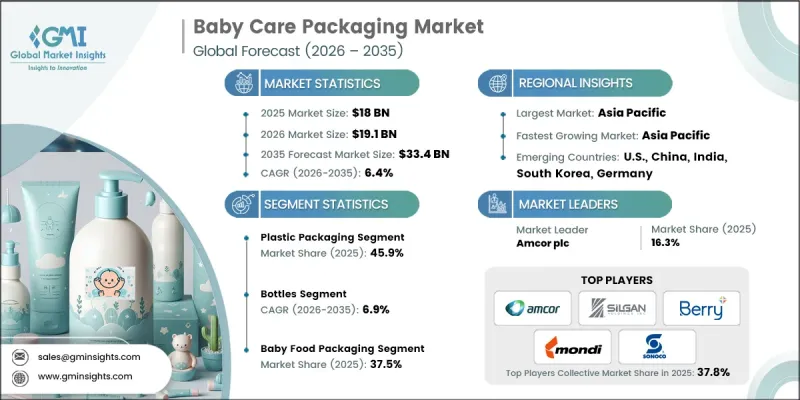

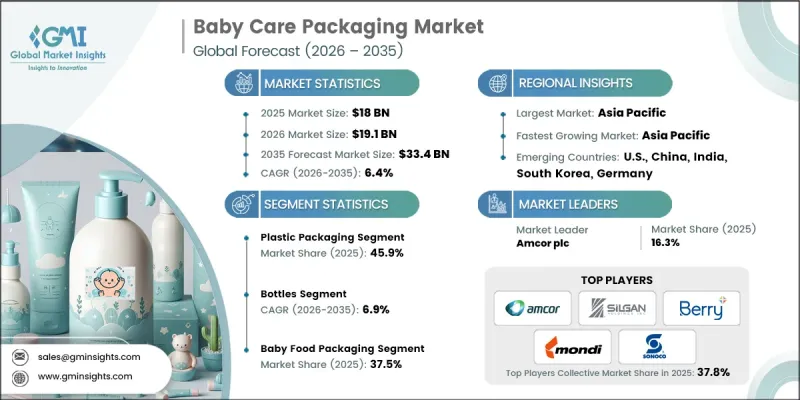

세계의 베이비 케어용 포장 시장은 2025년에 180억 달러로 평가되고 CAGR 6.4%로 성장하며, 2035년까지 334억 달러에 달할 것으로 추정되고 있습니다.

영유아의 건강에 대한 부모들의 인식이 높아진 데다, 이유식 및 건강보조식품의 1회 제공량 포장 형태가 확대되면서 이 시장의 성장세를 견인하고 있습니다. 또한 포장된 베이비 케어 제품에 대한 접근을 용이하게 하는 온라인 소매 플랫폼의 부상과 제품의 안전과 오염 방지를 보장하기 위한 정부의 규제 강화도 시장을 지원하는 요인으로 작용하고 있습니다. 가볍고 재활용이 가능하며 위생적인 포장 솔루션의 혁신은 제조업체들이 제품의 품질을 유지하면서 부모에게 편리함을 제공하는 소재와 형태에 초점을 맞추면서 시장 성장을 더욱 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 180억 달러 |

| 예측액 | 334억 달러 |

| CAGR | 6.4% |

플라스틱 포장 부문은 병, 용기, 파우치 및 기타 유연한 포장 형태에 광범위하게 사용되면서 2025년에는 45.9%의 점유율을 차지했습니다. 폴리에틸렌이나 폴리프로필렌과 같은 소재는 가볍고 다루기 쉽고 내구성이 뛰어나며 내습성이 뛰어나 보관 및 운송 중에 섬세한 유아용품을 보호할 수 있으며, 널리 선호되고 있습니다. 또한 플라스틱은 고배리어성 라미네이트, 재밀봉 가능한 캡, 변조 방지 설계를 통해 제품의 안전성과 소비자의 편의성을 높였습니다.

파우치 부문은 베이비푸드에서 짜먹을 수 있는 팩과 유연한 포장 형태가 인기를 끌면서 2025년에는 39억 달러에 달했습니다. 파우치는 가볍고 다루기 쉽고, 분량 조절이 쉽고, 먹이기 쉽기 때문에 퓌레, 반유동성 제품, 스낵류에 선호되고 있습니다. 높은 차단성으로 신선도와 영양가가 유지되며, 재밀봉이 가능한 디자인과 컴팩트한 패키지는 휴대성을 높이고 재료 사용량을 줄여줍니다.

2025년 북미의 베이비 케어용 포장 시장은 30%의 점유율을 차지했습니다. 이 지역은 첨단인 유통 시스템, 고급 영유아 영양 제품의 보급, 식품 접촉 포장에 대한 엄격한 규제의 혜택을 누리고 있습니다. 재활용이 가능하고 플라스틱 사용량을 줄이는 솔루션을 포함한 지속가능한 포장에 대한 노력은 이해관계자 및 정부 정책의 지원을 받아 북미에서 추진력을 얻고 있습니다. 이 지역은 높은 장벽과 친환경적인 베이비 케어용 포장 솔루션의 혁신 거점이 될 것으로 예상됩니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 포장재료별, 2022-2035년

제6장 시장 추산·예측 : 포장 형태별, 2022-2035년

제7장 시장 추산·예측 : 제품 용도별, 2022-2035년

제8장 시장 추산·예측 : 지역별, 2022-2035년

제9장 기업 개요

KSA 26.05.13The Global Baby Care Packaging Market was valued at USD 18 billion in 2025 and is estimated to grow at a CAGR of 6.4% to reach USD 33.4 billion by 2035.

Increasing parental awareness of infant health, combined with the growing adoption of single-serve packaging formats for baby food and nutrition products, is fueling this expansion. The market is also supported by the rise of online retail platforms, which facilitate access to packaged baby care solutions, and by stricter government regulations ensuring product safety and contamination prevention. Innovation in lightweight, recyclable, and hygienic packaging solutions further strengthens market growth, as manufacturers focus on materials and formats that preserve product quality while providing convenience for parents.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $18 Billion |

| Forecast Value | $33.4 Billion |

| CAGR | 6.4% |

The plastic packaging segment held a 45.9% share in 2025 owing to its extensive use in bottles, tubs, pouches, and other flexible packaging formats. Materials like polyethylene and polypropylene are widely preferred for their lightweight handling, durability, and excellent resistance to moisture, ensuring protection of sensitive baby products during storage and transport. Plastic also supports high-barrier laminates, resealable closures, and tamper-evident designs, which enhance product safety and consumer convenience.

The pouches segment reached USD 3.9 billion in 2025, as squeezable packs and flexible packaging formats become increasingly popular for baby food. Pouches offer lightweight handling, precise portion control, and ease of feeding, making them a preferred choice for purees, semi-liquid products, and snacks. Their high-barrier protection maintains freshness and nutritional quality, while resealable designs and compact packaging support portability and reduce material use.

North America Baby Care Packaging Market held a 30% share in 2025. The region benefits from advanced distribution systems, widespread adoption of premium infant nutrition products, and strict food-contact packaging regulations. Sustainable packaging initiatives, including recyclable and low-plastic solutions, are gaining traction in North America, supported by both industry stakeholders and government policies. The region is expected to remain a hub for innovation in high-barrier and eco-friendly baby care packaging solutions.

Key players in the Global Baby Care Packaging Market include Amcor plc, AptarGroup, Inc., Berry Global Inc., CDF Corporation, Constantia Flexibles, Gerresheimer AG, Greiner Packaging, Guala Pack S.p.a., Huhtamaki, ITC Packaging, KDWPACK, Mondi, Printpack, SIG Group, Silgan Unicep, Sonoco Products Company, Tetra Pak International S.A., Trivium Packaging, UFlex Limited, and Winpak LTD. Companies in the Baby Care Packaging Market are focusing on innovation, sustainability, and digital transformation to strengthen their market positions. They are investing in research to develop lightweight, recyclable, and contamination-resistant materials while improving barrier performance. Strategic partnerships with infant nutrition and baby care brands enable tailored packaging solutions that meet regulatory compliance and consumer convenience needs. Expanding global distribution networks and e-commerce collaborations allow faster market reach and improved accessibility. Many companies provide value-added services, including design support, custom printing, and supply chain management, to enhance customer loyalty. Continuous product portfolio expansion, coupled with marketing strategies highlighting hygiene and sustainability, strengthens their presence and competitiveness in the growing baby care packaging industry.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Packaging material type trends

- 2.2.2 Packaging format trends

- 2.2.3 Product application trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global demand for packaged infant formula products

- 3.2.1.2 Growth of e-commerce baby product distribution channels

- 3.2.1.3 Expansion of single-serve pouches for infant nutrition

- 3.2.1.4 Increasing regulatory standards for infant product safety

- 3.2.1.5 Rising hygiene and contamination prevention requirements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Strict food-grade packaging compliance regulations

- 3.2.2.2 Complex recycling for multilayer flexible packaging

- 3.2.3 Market opportunities

- 3.2.3.1 Development of recyclable mono-material baby food pouches

- 3.2.3.2 Smart packaging for product authenticity and freshness monitoring

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Packaging Material Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Plastic Packaging

- 5.3 Paper & Paperboard Packaging

- 5.4 Metal Packaging

- 5.5 Glass Packaging

Chapter 6 Market Estimates and Forecast, By Packaging Format, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Bottles

- 6.2.1 Rigid plastic bottles

- 6.2.2 Glass bottles

- 6.3 Pouches

- 6.3.1 Stand-up pouches

- 6.3.2 Spouted pouches

- 6.3.3 Flat pouches

- 6.3.4 Refill pouches

- 6.4 Tubes

- 6.4.1 Laminated tubes

- 6.4.2 Plastic squeeze tubes

- 6.5 Jars & containers

- 6.5.1 Plastic jars

- 6.5.2 Glass jars

- 6.6 Tubs & canisters

- 6.6.1 Wide-mouth tubs

- 6.6.2 Cylindrical canisters

- 6.7 Cans

- 6.7.1 Aluminum cans

- 6.7.2 Tin-plated steel cans

- 6.8 Cartons & paperboard packaging

- 6.9 Sachets & stick packs

- 6.10 Others

Chapter 7 Market Estimates and Forecast, By Product Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Baby food packaging

- 7.3 Infant formula packaging

- 7.4 Baby wipes packaging

- 7.5 Baby personal care packaging

- 7.6 Diaper & hygiene products packaging

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Amcor plc

- 9.1.2 Berry Global Inc.

- 9.1.3 Tetra Pak International S.A.

- 9.1.4 Mondi Group

- 9.2 Regional key players

- 9.2.1 North America

- 9.2.1.1 Sonoco Products Company

- 9.2.1.2 Printpack

- 9.2.1.3 CDF Corporation

- 9.2.2 Asia Pacific

- 9.2.2.1 Huhtamaki

- 9.2.2.2 UFlex Limited

- 9.2.2.3 ITC Packaging

- 9.2.2.4 KDWPACK

- 9.2.3 Europe

- 9.2.3.1 Constantia Flexibles

- 9.2.3.2 Silgan Unicep

- 9.2.3.3 Gerresheimer AG

- 9.2.3.4 Guala Pack S.p.a.

- 9.2.3.5 Greiner Packaging

- 9.2.3.6 SIG Group

- 9.2.1 North America

- 9.3 Niche Players/Disruptors

- 9.3.1 Trivium Packaging

- 9.3.2 AptarGroup, Inc.