|

시장보고서

상품코드

2027493

발포 유리 : 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Foam Glass Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

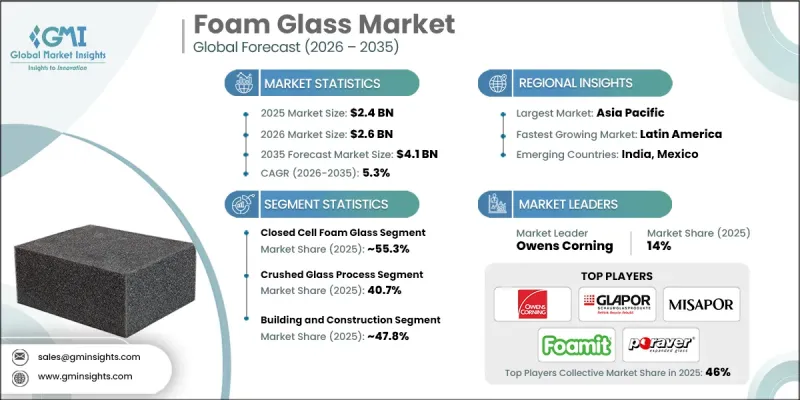

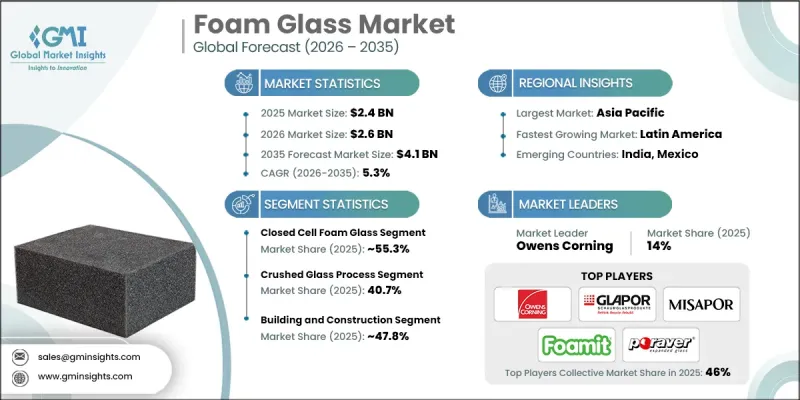

세계의 발포 유리 시장은 2025년에 24억 달러로 평가되었고 CAGR 5.3%를 나타내 2035년까지 41억 달러에 이를 것으로 추정되고 있습니다.

건설 및 산업 응용 분야에서 지속 가능하고 고성능 단열재에 대한 수요가 증가함에 따라 전 세계 발포 유리 산업은 꾸준히 성장하고 있습니다. 발포 유리는 재활용 유리를 가공하여 경량성과 높은 내구성을 겸비한 경질 다공성 구조물로 제조됩니다. 우수한 단열 효율, 방음 성능, 그리고 습기, 화학물질, 화재에 대한 내성으로 널리 인정받고 있습니다. 이러한 특성으로 인해 건축 외피, 지붕 시스템, 산업 시설, 보관 환경, 해양 관련 인프라의 특수 단열 용도에 사용하기에 적합합니다. 지속 가능한 건설 방식과 순환형 자재 활용에 대한 중요성이 점점 더 강조되고 있는 것이 시장 보급을 촉진하고 있습니다. 에너지 효율과 친환경 건축자재를 장려하는 규제 압력도 수요를 더욱 촉진하고 있습니다. 그러나 특히 비용 효율성과 시공 편의성이 우선시되는 분야에서는 대체 단열재와의 경쟁이 시장 역학에 지속적으로 영향을 미치고 있습니다. 그럼에도 불구하고, 지속적인 제품 혁신과 성능 향상으로 인해 첨단 건축 및 엔지니어링 분야에서 발포 유리의 채택이 확대되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 24억 달러 |

| 예측액 | 41억 달러 |

| CAGR | 5.3% |

2025년 기준, 독립 기포 발포 유리 부문은 55.3%의 점유율을 차지했으며, 2035년까지 연평균 복합 성장률(CAGR) 5.4%를 나타낼 것으로 예측됩니다. 이 부문이 선두를 달리고 있는 이유는 우수한 내수성, 높은 기계적 안정성, 열악한 환경 조건에서도 일관된 단열 성능을 발휘하기 때문입니다. 까다로운 건설 환경에서도 높은 신뢰성으로 폭넓게 활용되고 있습니다.

유리 분쇄 공정 부문은 2025년 40.7%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 5.5%의 성장률을 나타낼 것으로 전망됩니다. 이 제조 방법은 비용 효율성, 재활용 재료의 높은 활용률, 산업 생산의 확장성 등으로 인해 여전히 주류로 자리 잡고 있습니다. 균일한 구조적 특성과 강도를 실현하기 때문에 단열 블록 및 경량 골재 용도에 적합합니다. 지속적인 공정 최적화를 통해 생산 효율성과 용도의 다양성을 더욱 향상시키고 있습니다.

북미의 발포 유리 시장은 2025년 35.8%의 점유율을 차지했으며, 이는 이 지역의 강력한 수요를 반영합니다. 이 시장은 높은 건축 기준, 에너지 절약형 건축 솔루션에 대한 관심 증가, 재활용 소재 기반의 제품 채택 확대에 힘입어 성장하고 있습니다. 특히 내구성, 안전성, 지속가능성을 중시하는 상업용 인프라 및 특수 단열 응용 분야에서 수요가 지속적으로 증가하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 제조 공정별(2022-2035년)

제7장 시장 추산 및 예측 : 용도별(2022-2035년)

제8장 시장 추산 및 예측 : 지역별(2022-2035년)

제9장 기업 개요

KTH 26.05.20The Global Foam Glass Market was valued at USD 2.4 billion in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 4.1 billion by 2035.

The global foam glass industry is gaining steady traction as demand increases for sustainable, high-performance insulation materials across construction and industrial applications. Foam glass is produced by converting recycled glass into a rigid, porous structure that delivers a combination of lightweight characteristics and strong durability. It is widely valued for its thermal insulation efficiency, acoustic control capabilities, and resistance to moisture, chemicals, and fire exposure. These properties make it suitable for use in building envelopes, roofing systems, and specialized insulation applications across industrial facilities, storage environments, and marine-related infrastructure. Growing emphasis on sustainable construction practices and circular material usage is supporting market adoption. Regulatory pressure promoting energy efficiency and environmentally responsible building materials is further strengthening demand. However, competition from alternative insulation materials continues to influence market dynamics, particularly where cost efficiency and installation convenience are prioritized. Despite this, ongoing product innovation and performance improvements are reinforcing foam glass adoption across advanced construction and engineering applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.4 Billion |

| Forecast Value | $4.1 Billion |

| CAGR | 5.3% |

The closed-cell foam glass segment accounted for 55.3% share in 2025 and is expected to grow at a CAGR of 5.4% through 2035. This segment leads due to its superior resistance to water absorption, strong mechanical stability, and consistent insulation performance under extreme environmental conditions. Its reliability in demanding construction environments continues to support its widespread use.

The crushed glass process segment held a 40.7% share in 2025 and is projected to grow at a CAGR of 5.5% from 2026 to 2035. This production method remains dominant due to its cost efficiency, high utilization of recycled materials, and scalability for industrial manufacturing. It supports uniform structural properties and strength, making it suitable for insulation blocks and lightweight aggregate applications. Continuous process optimization is further improving production efficiency and application versatility.

North America Foam Glass Market accounted for 35.8% share in 2025, reflecting strong regional demand. The market is supported by advanced construction standards, increasing focus on energy-efficient building solutions, and growing adoption of recycled material-based products. Demand continues to rise across commercial infrastructure and specialized insulation applications, particularly in projects emphasizing durability, safety, and sustainability.

Key companies operating in the Global Foam Glass Market include Owens Corning, Foamit Group, Glapor Werk Mitterteich GmbH, Misapor AG, Dennert Poraver GmbH, Veriso GmbH & Co. KG, AeroAggregates of North America, LLC, Uusioaines Oy, Glasopor AS, Glavel Inc., Energocell Kft., Zhejiang Zhenshen Insulation Technology Corp., Refaglass s.r.o., and Steinbach Schaumglas GmbH & Co. KG. Companies in the Global Foam Glass Market are implementing targeted strategies to strengthen their competitive positioning and expand market share. A major focus is placed on product innovation to enhance thermal performance, durability, and sustainability characteristics. Manufacturers are investing in advanced recycling and production technologies to improve efficiency and reduce operational costs. Strategic partnerships with construction firms and infrastructure developers are being used to expand application reach. Capacity expansion initiatives are supporting increased demand from large-scale construction projects. Companies are also strengthening their distribution networks to improve market accessibility across regions. In addition, sustainability-driven strategies, including increased use of recycled raw materials and low-emission production methods, are helping firms align with environmental regulations and attract eco-conscious customers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Production process

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth in Construction and Infrastructure

- 3.2.1.2 Lightweight and Durable

- 3.2.1.3 Sustainability and Recycling

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Competition from alternatives

- 3.2.2.2 High Production Cost

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets with growing construction activity

- 3.2.3.2 Innovation in additive manufacturing & 3d printing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Open cell foam glass

- 5.3 Closed cell foam glass

- 5.4 Mixed cell foam glass

Chapter 6 Market Estimates and Forecast, By Production Process, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Crushed glass process

- 6.3 Glass powder process

- 6.4 Direct foaming process

- 6.5 Slurry methods

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Building and construction

- 7.2.1 Flat roofs

- 7.2.2 Facades & exterior walls

- 7.2.3 Underground & below grade applications

- 7.2.4 Interior insulation

- 7.2.5 Others

- 7.3 Industrial

- 7.3.1 Tank base insulation

- 7.3.2 Pipe insulation

- 7.3.3 Vessel & equipment insulation

- 7.3.4 Other

- 7.4 Chemical

- 7.4.1 Corrosion resistant insulation

- 7.4.2 High temperature applications

- 7.5 Marine

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Owens Corning

- 9.2 Glapor Werk Mitterteich GmbH

- 9.3 Misapor AG

- 9.4 Veriso GmbH & Co. KG

- 9.5 Dennert Poraver GmbH

- 9.6 AeroAggregates of North America, LLC

- 9.7 Uusioaines Oy

- 9.8 Zhejiang Zhenshen Insulation Technology Corp.

- 9.9 Energocell Kft.

- 9.10 Glasopor AS

- 9.11 Glavel Inc.

- 9.12 Refaglass s.r.o.

- 9.13 Steinbach Schaumglas GmbH & Co. KG

- 9.14 Foamit Group