|

시장보고서

상품코드

2027532

금속 분말 이용 적층제조 : 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Additive Manufacturing With Metal Powders Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

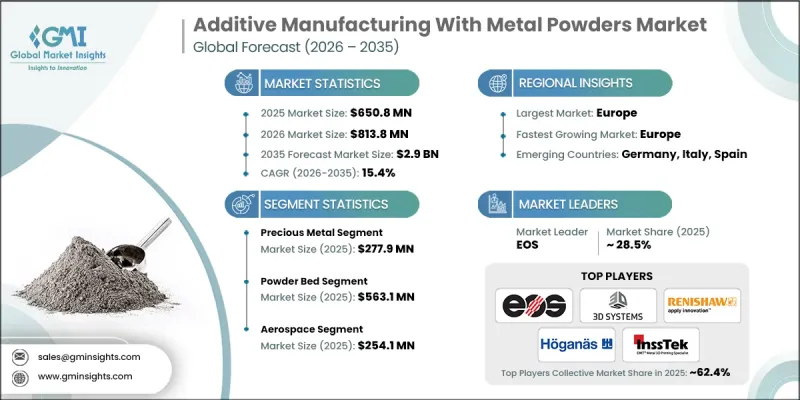

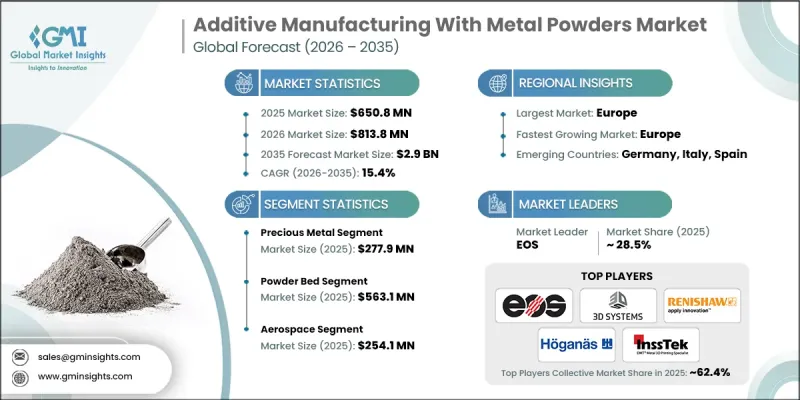

세계의 금속 분말 이용 적층제조 시장은 2025년에 6억 5,080만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 15.4%를 나타내 29억 달러에 이를 것으로 추정되고 있습니다.

시장 확대는 여러 고성능 산업 분야에서 가볍고 내구성이 뛰어난 부품에 대한 수요 증가에 힘입은 바 큽니다. 제조업체들은 효율성 향상, 재료 낭비 감소, 기존 방식으로는 구현하기 어려운 복잡한 형상을 생산할 수 있도록 금속 기반 적층 가공 기술을 점점 더 많이 채택하고 있습니다. 이러한 변화는 특히 각 산업계가 성능과 에너지 효율성 향상을 우선시하는 가운데 제조 전략을 재정의하고 있습니다. 레이저 기반 시스템, 전자빔 프로세스, 멀티 레이저 구성 등의 개선을 포함한 3D 프린팅 기술의 지속적인 발전으로 조형 속도와 정확도가 크게 향상되었습니다. 이러한 혁신은 공정의 신뢰성을 높이고 금속 분말 기반 제조 솔루션의 상업적 타당성을 확대합니다. 또한, 의료 분야에서의 적층조형 적용 확대도 수요 증가에 기여하고 있으며, 맞춤형 고정밀 부품에 대한 필요성이 지속적으로 증가하고 있습니다. 전반적으로, 기술 혁신, 산업 도입 및 첨단 제조 능력에 대한 수요가 결합되어 세계 시장에서 지속적인 성장을 주도하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 6억 5,080만 달러 |

| 예측 금액 | 29억 달러 |

| CAGR | 15.4% |

2025년 기준, 파우더 베드 방식 부문은 5억 6,310만 달러 규모였으며, 2026년부터 2035년까지 연평균 15.6% 성장할 것으로 예측됩니다. 이 부문은 높은 정밀도와 일관된 품질로 복잡한 금속 부품을 제조할 수 있는 능력으로 인해 계속해서 선도적인 위치를 유지하고 있습니다. 복잡한 구조의 제조에 적합하여 정밀도가 요구되는 산업 분야에서 널리 채택되고 있습니다. 한편, 블로우 파우더 기술은 수리 및 개조, 대형 부품 제조의 유연성으로 인해 주목을 받고 있습니다. 정밀 제조와 비용 효율적인 수리 솔루션을 결합할 수 있는 능력은 금속 분말 기반 적층 가공 기술에 대한 수요를 크게 증가시키고 있습니다.

항공우주 부문은 2025년 2억 5,410만 달러 시장 규모를 기록하여 39%의 점유율을 차지했으며, 2035년까지 연평균 15.9%의 성장률(CAGR)을 나타낼 전망입니다. 기업들이 경량, 고성능, 고정밀 부품 제조에 금속 적층 가공을 점점 더 많이 활용함에 따라 항공우주, 자동차, 의료 등 주요 산업에서 성장이 가속화되고 있습니다. 항공우주 분야에서는 첨단 구조 및 기능 부품에 대한 수요가 주도하고 있으며, 자동차 분야에서는 시제품 제작, 금형 제작 및 특수 생산 요구에 대응하기 위해 이러한 기술이 활용되고 있습니다. 한편, 의료 분야에서는 맞춤형 고정밀 부품에 대한 수요가 증가함에 따라 용도가 빠르게 확대되고 있습니다. 이러한 각 산업 분야 수요를 합치면 금속 분말을 기반으로 한 첨단 제조 공정으로의 전환을 촉진하고 있습니다.

북미의 금속 분말 이용 적층제조 시장은 2025년 2억 5,310만 달러에 달했습니다. 이 지역에서는 잘 구축된 산업 인프라와 지속적인 연구개발 투자에 힘입어 금속 적층제조 기술의 급속한 보급이 이루어지고 있습니다. 시제품 제작, 금형 및 특수 생산에 대한 사용 증가가 여러 분야에 걸쳐 수요를 주도하고 있습니다. 자동화 및 하이브리드 제조 공정의 발전으로 업무 효율성이 더욱 향상되고 시장 확대가 가속화되고 있습니다. 이 지역의 강력한 산업 기반과 조기 도입 추세는 계속해서 세계 성장의 주요 원동력으로 자리매김하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 재료별(2022-2035년)

제6장 시장 추산 및 예측 : 기술별(2022-2035년)

제7장 시장 추산 및 예측 : 용도별(2022-2035년)

제8장 시장 추산 및 예측 : 지역별(2022-2035년)

제9장 기업 개요

KTH 26.05.20The Global Additive Manufacturing with Metal Powders Market was valued at USD 650.8 million in 2025 and is estimated to grow at a CAGR of 15.4% to reach USD 2.9 billion by 2035.

Market expansion is fueled by the rising demand for lightweight yet durable components across multiple high-performance industries. Manufacturers are increasingly adopting metal-based additive manufacturing technologies to enhance efficiency, reduce material waste, and enable the production of complex geometries that are difficult to achieve through conventional methods. This shift is redefining manufacturing strategies, particularly as industries prioritize improved performance and energy efficiency. Continuous advancements in 3D printing technologies, including improvements in laser-based systems, electron beam processes, and multi-laser configurations, are significantly enhancing build speed and precision. These innovations are strengthening process reliability and expanding the commercial viability of metal powder-based manufacturing solutions. Additionally, the growing application of additive manufacturing in healthcare is contributing to rising demand, as the need for customized and high-precision components continues to increase. Overall, the convergence of technological innovation, industrial adoption, and demand for advanced manufacturing capabilities is driving sustained growth in the global market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $650.8 Million |

| Forecast Value | $2.9 Billion |

| CAGR | 15.4% |

The powder bed segment accounted for USD 563.1 million in 2025 and is expected to grow at a CAGR of 15.6% from 2026 to 2035. This segment continues to lead due to its ability to produce intricate metal components with high accuracy and consistent quality. Its suitability for manufacturing complex structures has made it widely adopted across precision-driven industries. At the same time, blown powder technologies are gaining traction because of their flexibility in repairing, modifying, and producing larger components. The ability to combine precision manufacturing with cost-effective repair solutions is significantly boosting the demand for metal powder-based additive manufacturing technologies.

The aerospace segment generated USD 254.1 million in 2025 and held a share of 39%, with a projected CAGR of 15.9% through 2035. Growth across key industries such as aerospace, automotive, and healthcare is accelerating as companies increasingly utilize metal additive manufacturing to produce lightweight, high-performance, and highly accurate components. Aerospace applications are driving demand for advanced structural and functional parts, while the automotive sector is leveraging these technologies for prototyping, tooling, and specialized production needs. Meanwhile, healthcare applications continue to expand rapidly due to the increasing requirement for customized, high-precision components. The combined demand across these industries is reinforcing the shift toward advanced manufacturing processes based on metal powders.

North America Additive Manufacturing with Metal Powders Market accounted for USD 253.1 million in 2025. The region is experiencing rapid adoption of metal additive manufacturing technologies, supported by well-established industrial infrastructure and continuous investments in research and development. Increasing use in prototyping, tooling, and specialized production is driving demand across multiple sectors. Advancements in automation and hybrid manufacturing processes are further enhancing operational efficiency and accelerating market expansion. Strong industry presence and early adoption trends continue to position the region as a key contributor to global growth.

Key companies operating in the Additive Manufacturing With Metal Powders Market include 3D Systems Corporation, Additive Industries, Advanced Powder & Coatings, Inc., Aubert & Duval S.A, Aerojet Rocketdyne (L3Harris), Airbus SE, Allegheny Technologies (ATI), APWorks, Xi'an Bright Laser Technologies, Carpenter Technologies Corp, Colibrium Additive (GE Additive), Constellium, Cookson Precious Metals Ltd, EOS GmbH, Equispheres, Inc., ExOne, Fabrisonic, LLC, Farsoon Technologies, Fonon Technologies, Elmet Technologies (HC Starck), Hilderbrand & Cie SA, Hoganas AB, Insstek GmbH, Legor Group SpA, Materialise NV, PyroGenesis Canada, Inc., Renishaw PLC, Sandvik Group, STELIA Aerospace, Linde AMT (Praxair Surface Technologies), and others. Companies in the Additive Manufacturing with Metal Powders Market are focusing on technological innovation, capacity expansion, and strategic collaborations to strengthen their market position. Investments in advanced printing systems, improved powder materials, and process optimization are enhancing product performance and manufacturing efficiency. Firms are also expanding production capabilities and global distribution networks to meet rising demand. Partnerships with end-use industries are enabling faster adoption and application development. Additionally, companies are emphasizing research and development to improve precision, reduce costs, and enhance scalability.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material

- 2.2.3 Technology

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Material, 2022- 2035 (USD Million, Kilo Tons)

- 5.1 Key trends

- 5.2 Alloy

- 5.2.1 Titanium

- 5.2.1.1 Ti6Al4V

- 5.2.1.2 Ti6Al4V (ELI)

- 5.2.1.3 Others

- 5.2.2 Cobalt

- 5.2.2.1 CoCr

- 5.2.2.2 CoCrWC

- 5.2.2.3 CoCrMo

- 5.2.3 Copper

- 5.2.3.1 C18150

- 5.2.3.2 CuCr1Zr

- 5.2.3.3 CuNi2SiCr

- 5.2.4 Nickel

- 5.2.4.1 Inconel 625

- 5.2.4.2 Inconel 718

- 5.2.4.3 Hastelloy X

- 5.2.5 Aluminium

- 5.2.5.1 ALSi12

- 5.2.5.2 ALSi7Mg

- 5.2.5.3 ALSi10Mg

- 5.2.5.4 AL6061

- 5.2.5.5 Others

- 5.2.1 Titanium

- 5.3 Stainless Steel

- 5.3.1 Austenitic Steel

- 5.3.2 Martensitic Steel

- 5.3.3 Duplex steel

- 5.3.4 Ferritic Steel

- 5.4 Other Steel

- 5.4.1 High Speed Steel

- 5.4.2 Tool Steel

- 5.4.3 Low Alloy Steel

- 5.5 Precious Metal

- 5.5.1 Platinum

- 5.5.2 Other precious metal

- 5.6 Tungsten

- 5.7 Silicon carbide

- 5.8 Aluminium oxide powder

- 5.9 Zirconium

- 5.10 Zirconium dioxide

- 5.11 Molybdenum

- 5.12 Magnesium

- 5.13 Aluminium nitride

- 5.14 Tungsten carbide

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Million, Kilo Tons)

- 6.1 Key trends

- 6.2 Powder Bed

- 6.2.1 Direct Metal Laser Sintering (DMLS)

- 6.2.2 Selective Laser Melting (SLM)

- 6.2.3 Electron Beam Melting (EBM)

- 6.3 Blown powder

- 6.3.1 Direct Metal Deposition (DMD)

- 6.3.2 Laser Engineering Net Shapes (LENS)

- 6.4 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million, Kilo Tons)

- 7.1 Key trends

- 7.2 Aerospace

- 7.3 Automotive

- 7.4 Medical

- 7.5 Oil & Gas

- 7.6 Energy

- 7.6.1 Nuclear

- 7.6.2 Renewable

- 7.7 Other

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million, Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 3D Systems Corporation

- 9.2 Additive Industries

- 9.3 Advanced Powder & Coatings, Inc

- 9.4 Aubert & Duval S.A

- 9.5 Aerojet Rocketdyne (L3Harris)

- 9.6 Airbus SE

- 9.7 Allegheny Technologies (ATI)

- 9.8 APWorks

- 9.9 Xi'an Bright Laser Technologies

- 9.10 Carpenter Technologies Corp

- 9.11 Colibrium Additive (GE Additive)

- 9.12 Constellium

- 9.13 Cookson Precious Metals Ltd

- 9.14 EOS GmbH

- 9.15 Equispheres, Inc

- 9.16 ExOne

- 9.17 Fabrisonic, LLC

- 9.18 Farsoon Technologies

- 9.19 Fonon Technologies

- 9.20 Elmet Technologies (HC Starck)

- 9.21 Hilderbrand & Cie SA

- 9.22 Hoganas AB

- 9.23 Insstek GmbH

- 9.24 Legor Group SpA

- 9.25 Materialise NV

- 9.26 PyroGenesis Canada, Inc

- 9.27 Renishaw PLC

- 9.28 Sandvik Group

- 9.29 STELIA Aerospace

- 9.30 Linde AMT (Praxair Surface Technologies)