|

시장보고서

상품코드

2027562

4PL(Fourth Party Logistics) : 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Fourth-Party Logistics (4PL) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

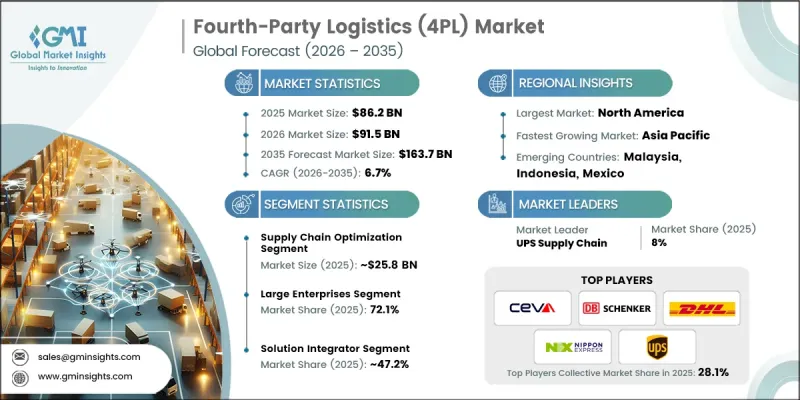

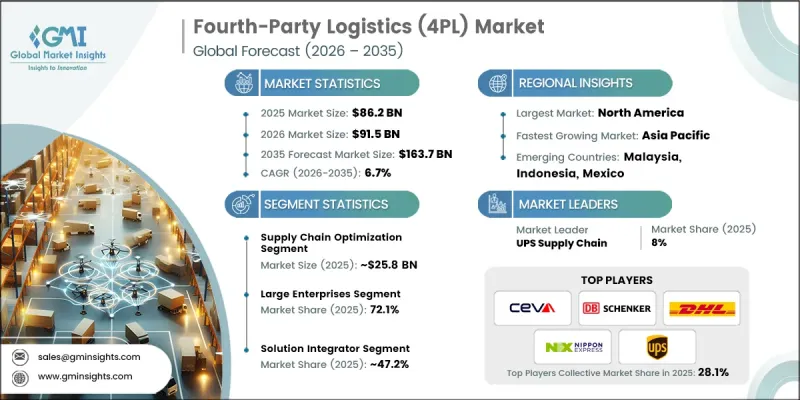

세계의 4PL(Fourth Party Logistics) 시장은 2025년에 862억 달러로 평가되었고 CAGR 6.7%를 나타내 2035년까지 1,637억 달러에 이를 것으로 추정되고 있습니다.

이러한 시장 확대는 무역량 증가와 세계 상거래의 통합, 국제 공급망의 복잡성 증가에 따른 것으로 분석됩니다. 기업들은 조정을 간소화하고, 업무 효율성을 개선하며, 여러 이해관계자간의 가시성을 높일 수 있는 종합적인 물류 솔루션을 점점 더 많이 필요로 하고 있습니다. 4PL(Fourth Party Logistics) 제공업체는 단순히 개별 물류업무를 수행하는 것이 아니라, 고객을 대신하여 전체 공급망을 관리하는 전략적 파트너로서의 역할을 수행합니다. 기술 플랫폼, 여러 물류 파트너 및 업무 워크플로우를 통합함으로써 4PL(Fourth Party Logistics) 기업은 기업이 복잡성을 줄이고, 프로세스를 최적화하며, 단일 관리 조직으로 책임을 통합할 수 있도록 지원합니다. 디지털 전환, 예측 분석, 공급망 복원력에 대한 관심 증가와 더불어, 지리적 확장을 위한 합작 투자 및 인수합병의 추세는 세계 4PL(Fourth Party Logistics) 솔루션의 채택을 더욱 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 862억 달러 |

| 예측액 | 1,637억 달러 |

| CAGR | 6.7% |

공급망 최적화 부문은 29.9%의 점유율을 차지하며 2025년 258억 달러 시장 규모를 형성했습니다. 기업들은 점점 더 엔드 투 엔드 효율성에 초점을 맞추고 있으며, 공급망 최적화는 4PL(Fourth Party Logistics) 서비스 제공의 기초가 되고 있습니다. 이 서비스는 운송업체, 창고 솔루션, 기술 플랫폼을 통합하여 복잡한 세계 공급망 전반에 걸쳐 운영을 간소화하고 민첩성을 높이며 대응력을 향상시킵니다. 기업들은 변동이 심한 시장 환경에서 수익성을 유지하고, 비용을 절감하고, 업무의 일관성을 보장하기 위해 공급망 최적화에 의존하고 있습니다.

솔루션 통합업체 부문은 2025년 47.2%의 점유율을 차지했습니다. 솔루션 통합자는 여러 제3자 물류 제공업체, 기술 시스템 및 프로세스 워크플로우를 통합하여 일관되고 효율적인 운영을 실현하는 중심 조정자 역할을 수행합니다. 엔드투엔드 물류 관리, 자원 최적화, 지역 간 통합 서비스 제공 능력은 비용 절감, 운영 관리, 공급망 가시성 향상을 목표로 하는 기업에게 필수적인 요소로 자리 잡고 있습니다. 이 부문의 성장은 세계 공급망의 복잡성 증가, 디지털 전환 노력, 실시간 모니터링 및 예측 분석에 대한 수요 증가에 힘입어 성장세를 보이고 있습니다.

미국의 4PL(Fourth Party Logistics) 시장은 2025년 278억 달러로 평가되었고, 2026년부터 2035년까지 연평균 7.2% 성장할 것으로 예측됩니다. 중국의 선진화된 물류 인프라와 복합운송 능력은 통합형 4PL(Fourth Party Logistics) 솔루션의 도입을 촉진하고 있습니다. 공급망의 탄력성, 투명성, 지속가능성을 촉진하는 연방정부의 정책은 기업들이 종합적인 물류 관리 모델을 도입하도록 장려하고 있습니다. 무역 정책의 우선순위는 안전하고 다각화된 공급망에 중점을 두고 있으며, 이에 따라 기업들은 지정학적 및 세계 경제 압력으로 인한 혼란의 위험을 줄이기 위해 4PL(Fourth Party Logistics) 전략을 채택하도록 촉구하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 솔루션별(2022-2035년)

제6장 시장 추산 및 예측 : 사업 모델별(2022-2035년)

제7장 시장 추산 및 예측 : 기업 규모별(2022-2035년)

제8장 시장 추산 및 예측 : 업계별(2022-2035년)

제9장 시장 추산 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

KTH 26.05.20The Global Fourth-Party Logistics Market was valued at USD 86.2 billion in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 163.7 billion by 2035.

The market expansion is fueled by the rising intricacy of international supply chains, driven by growing trade volumes and global commerce integration. Businesses increasingly require comprehensive logistics solutions that simplify coordination, improve operational efficiency, and enhance visibility across multiple stakeholders. Fourth-party logistics providers serve as strategic partners, managing entire supply chains on behalf of clients rather than merely executing isolated logistics tasks. By integrating technology platforms, multiple logistics partners, and operational workflows, 4PL companies enable enterprises to reduce complexity, optimize processes, and consolidate accountability under a single management entity. Rising interest in digital transformation, predictive analytics, and supply chain resilience, along with the trend of forming joint ventures and acquisitions for geographic expansion, further supports the adoption of 4PL solutions worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $86.2 Billion |

| Forecast Value | $163.7 Billion |

| CAGR | 6.7% |

The supply chain optimization segment held a 29.9% share, generating USD 25.8 billion in 2025. Businesses are increasingly focusing on end-to-end efficiency, making supply chain optimization a cornerstone of 4PL service delivery. This service integrates carriers, warehousing solutions, and technology platforms to streamline operations, enhance agility, and improve responsiveness across complex global supply chains. Companies rely on supply chain optimization to maintain profitability, reduce costs, and achieve operational consistency amid volatile market conditions.

The solution integrator segment held a 47.2% share in 2025. Solution integrators act as central orchestrators by combining multiple third-party logistics providers, technology systems, and process workflows into cohesive, efficient operations. Their ability to manage end-to-end logistics, optimize resources, and provide uniform services across regions makes them essential for companies pursuing cost savings, operational control, and improved supply chain visibility. Growth in this segment is driven by increasing global supply chain complexity, digital transformation initiatives, and the rising demand for real-time monitoring and predictive analytics.

U.S. Fourth-Party Logistics Market was valued at USD 27.8 billion in 2025 and is estimated to grow at a CAGR of 7.2% from 2026 to 2035. The country's sophisticated logistics infrastructure and multi-modal transport capabilities favor the adoption of integrated 4PL solutions. Federal policies promoting supply chain resilience, transparency, and sustainability encourage enterprises to implement comprehensive logistics management models. Trade policy priorities emphasize secure, diversified supply chains, prompting businesses to adopt 4PL strategies that mitigate disruption risks from geopolitical and global economic pressures.

Leading companies operating in the Global Fourth-Party Logistics Market include DB Schenker, CEVA Logistics, FedEx Logistics, UPS Supply Chain, DHL, C.H. Robinson, Geodis, Kuehne + Nagel, XPO Logistics, and Nippon Express. Market players strengthen their presence and expand their foothold through strategic initiatives such as forming global partnerships, joint ventures, and acquisitions to enter new regions. Companies invest heavily in technology, including real-time tracking, predictive analytics, AI-based route optimization, and warehouse automation, to enhance operational efficiency and customer value. They focus on offering end-to-end solutions that integrate multiple logistics partners, optimizing resource allocation while maintaining high service standards. Expanding digital platforms, enhancing client-specific solutions, and providing centralized management dashboards improve visibility and accountability. Firms also emphasize sustainability and compliance, adopting environmentally responsible practices to attract socially conscious customers and maintain competitive differentiation in the Global Fourth-Party Logistics Market

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Solution

- 2.2.3 Operational model

- 2.2.4 Organization size

- 2.2.5 Industry

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth of e-commerce & omnichannel retail expansion

- 3.2.1.2 Increasing complexity of global supply chains & cross-border trade

- 3.2.1.3 Rising demand for end-to-end supply chain visibility & integration

- 3.2.1.4 Focus on cost optimization & operational efficiency

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Loss of direct control over logistics operations

- 3.2.2.2 High dependency on single external service provider

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets with growing trade volumes

- 3.2.3.2 Increasing demand for green & sustainable logistics solutions

- 3.2.3.3 Growth in industry-specific 4PL solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. - Federal Maritime Commission

- 3.4.1.2 Canada - Canada Border Services Agency

- 3.4.2 Europe

- 3.4.2.1 UK - HM Revenue and Customs

- 3.4.2.2 Germany - Federal Office for Goods Transport

- 3.4.3 Asia Pacific

- 3.4.3.1 China - Ministry of Transport of the People's Republic of China

- 3.4.3.2 India - Directorate General of Foreign Trade

- 3.4.4 Latin America

- 3.4.4.1 Brazil - Agencia Nacional de Transportes Terrestres

- 3.4.4.2 Mexico - Secretaria de Infraestructura, Comunicaciones y Transportes

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE - Federal Transport Authority

- 3.4.5.2 South Africa - South African Department of Transport

- 3.4.1 North America

- 3.5 Investment & funding analysis

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and innovation landscape

- 3.8.1 Current technologies

- 3.8.1.1 Transportation Management Systems (TMS)

- 3.8.1.2 Warehouse Management Systems (WMS)

- 3.8.1.3 Enterprise Resource Planning (ERP)

- 3.8.1.4 Real-Time Tracking & Telematics

- 3.8.2 Emerging technologies

- 3.8.2.1 Artificial Intelligence & Machine Learning (AI/ML)

- 3.8.2.2 Blockchain for Supply Chain

- 3.8.2.3 Digital Twins

- 3.8.1 Current technologies

- 3.9 Patent landscape (Driven by Primary Research)

- 3.10 Impact of e-commerce on the 4PL market

- 3.10.1 Growth of Direct-to-Consumer (D2C) logistics

- 3.10.2 Last-mile delivery challenges & solutions

- 3.10.3 Integration with e-commerce platforms & marketplaces

- 3.10.4 Demand for real-time visibility & tracking

- 3.10.5 Effect on order fulfillment speed & inventory management

- 3.11 Impact of global trade agreements & geopolitical developments

- 3.11.1 Influence of Free Trade Agreements (FTAs)

- 3.11.2 Tariff changes & customs regulations

- 3.11.3 Political instability & sanctions

- 3.11.4 Regional trade blocs & cross-border logistics

- 3.11.5 Strategic sourcing & diversification decisions

- 3.12 Impact of AI & Generative AI on the Market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.13.1 Base Case - key macro & industry variables driving CAGR

- 3.13.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.13.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Solution, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Supply chain optimization

- 5.3 Transportation management

- 5.3.1 Air

- 5.3.2 Sea

- 5.3.3 Rail & Road

- 5.4 Inventory management

- 5.5 Warehouse management

- 5.6 Order fulfillment

- 5.7 Distribution management

Chapter 6 Market Estimates & Forecast, By Operational model, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Synergy plus organization

- 6.3 Solution integrator

- 6.4 Industry innovator

Chapter 7 Market Estimates & Forecast, By Organization size, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 SMEs

- 7.3 Large enterprises

Chapter 8 Market Estimates & Forecast, By Industry, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Retail & E-commerce

- 8.3 Food & Beverage

- 8.4 Healthcare

- 8.5 Automotive

- 8.6 Manufacturing

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Sweden

- 9.3.7 Czech Republic

- 9.3.8 Poland

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 South Korea

- 9.4.4 India

- 9.4.5 Australia

- 9.4.6 Singapore

- 9.4.7 Vietnam

- 9.4.8 Indonesia

- 9.4.9 Malaysia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Chile

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 DHL

- 10.1.2 C.H. Robinson

- 10.1.3 UPS Supply

- 10.1.4 XPO Logistics

- 10.1.5 DB Schenker

- 10.1.6 Kuehne + Nagel

- 10.1.7 CEVA Logistics

- 10.1.8 Geodis

- 10.1.9 Nippon Express

- 10.1.10 FedEx

- 10.2 Regional players

- 10.2.1 Rhenus

- 10.2.2 Incora

- 10.2.3 Allyn International

- 10.2.4 Denholm Good Logistics

- 10.2.5 Gefco

- 10.2.6 Logistics Plus

- 10.2.7 Yusen Logistics

- 10.3 Emerging players

- 10.3.1 De Rijke

- 10.3.2 X2 UK

- 10.3.3 SmartWay Logistics