|

시장보고서

상품코드

2027655

식품 하이드로콜로이드 : 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Food Hydrocolloids Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

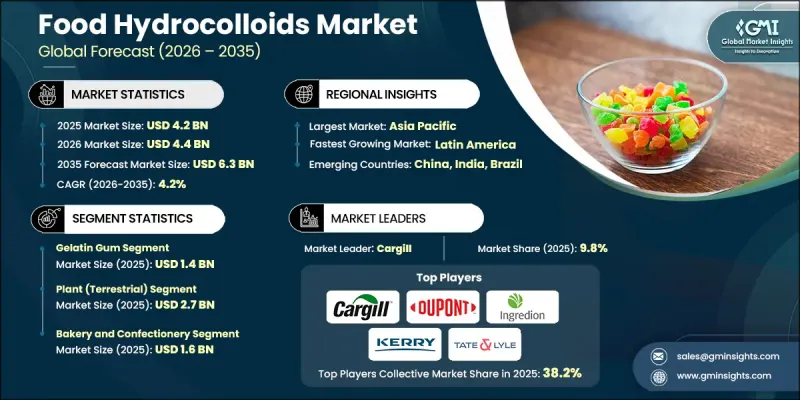

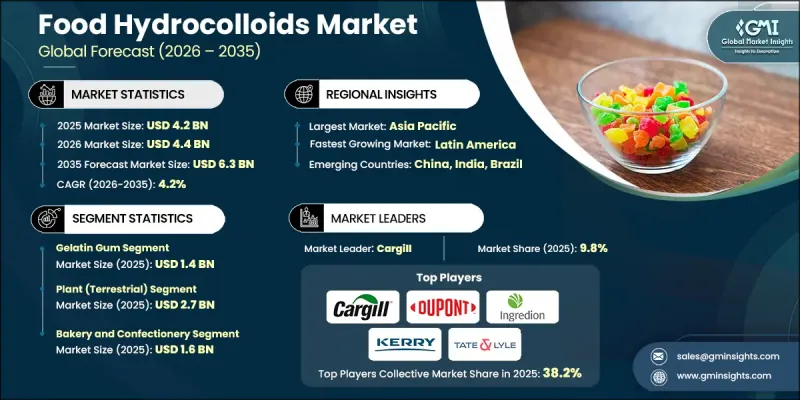

세계의 식품 하이드로콜로이드 시장은 2025년에 42억 달러로 평가되었고 CAGR 4.2%를 나타내 2035년까지 63억 달러에 이를 것으로 추정되고 있습니다.

가공식품 전반에서 식감, 안정성, 보존성을 높이는 기능성 원료에 대한 수요가 증가하면서 전 세계 식품 하이드로콜로이드 산업은 꾸준히 성장하고 있습니다. 식품 하이드로콜로이드는 식물, 동물, 미생물, 해조류를 원료로 한 겔화제, 증점제, 안정제로 널리 사용되고 있습니다. 이들 원료는 식품 시스템에서 점도와 구조적 안정성을 향상시키는 데 중요한 역할을 하며, 베이커리, 제과, 유제품, 음료 등의 응용 분야에서 필수적인 역할을 하고 있습니다. 다양한 열 조건, pH 수준 및 기계적 스트레스 하에서도 성능을 유지할 수 있는 특성으로 인해 상온 및 냉장 식품 모두에서 사용이 더욱 확대되고 있습니다. 또한, 하이드로콜로이드는 합성 첨가물을 사용하지 않고 천연의 기능성을 제공하기 때문에 클린 라벨 원료에 대한 소비자 선호도가 높아진 것도 수요를 견인하고 있습니다. 추출 및 정제 기술의 발전으로 제품의 품질이 더욱 향상되어 분자 구조와 성능 특성을 더욱 정밀하게 제어할 수 있게 되었습니다. 효소 처리 및 제어된 가수분해 기술의 통합으로 제조업체는 겔 강도 및 점도와 같은 기능적 특성을 조정할 수 있어 현대 식품 배합에 대한 응용 가능성이 확대되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 42억 달러 |

| 예측액 | 63억 달러 |

| CAGR | 4.2% |

젤라틴 검 부문은 우수한 겔화 성능과 광범위한 응용 분야로 인해 2025년 14억 달러 시장 규모를 차지했습니다. 이 부문은 열 가역성이라는 특성으로 인해 제과류, 유제품, 의약품 용도에 적합합니다. 가공 기술의 지속적인 개선으로 제조업체는 다양한 배합 요구 사항을 충족시키기 위해 다양한 블룸 강도 맞춤형 젤라틴을 개발할 수 있게 되었습니다. 한편, 펙틴과 같은 식물 유래 하이드로콜로이드는 저당 및 과일을 기반으로 한 용도, 특히 클린 라벨 제품 개발에 적합하다는 점에서 주목받고 있습니다.

식물 유래 부문은 비건 및 천연 유래 원료에 대한 수요 증가에 힘입어 2025년 27억 달러 시장 규모를 기록했습니다. 식품 제조업체들이 클린 라벨 트렌드와 식물성 성분을 선호하는 소비자의 기호에 맞추어 이 카테고리는 계속 성장하고 있습니다. 동물성 하이드로콜로이드는 특정 응용 분야에서 여전히 중요하지만, 식물성 대체품은 여러 식품 카테고리에서 그 입지를 넓혀가고 있습니다. 해조류 유래 하이드로콜로이드는 특히 유제품 및 육류 제품 배합의 안정화 및 겔 형성 용도로 빠르게 보급되고 있습니다.

북미의 식품 하이드로콜로이드 시장은 클린 라벨 원료의 채택 확대와 천연 식품 배합 전략에 대한 관심이 높아지면서 2025년 12억 달러에서 2035년까지 18억 달러로 성장할 것으로 예측됩니다. 식품 제조업체들은 소비자의 기대에 부응하기 위해 식물성 원료와 투명성이 높은 원료 시스템으로 전환을 가속화하고 있습니다. 식물성 식품의 성장과 더불어 유제품 대체품, 베이커리 제품, 기능성 음료의 천연 안정제에 대한 수요 증가는 이 지역 전체 시장의 성장을 더욱 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 소스별(2022-2035년)

제7장 시장 추산 및 예측 : 용도별(2022-2035년)

제8장 시장 추산 및 예측 : 지역별(2022-2035년)

제9장 기업 개요

KTH 26.05.20The Global Food Hydrocolloids Market was valued at USD 4.2 billion in 2025 and is estimated to grow at a CAGR of 4.2% to reach USD 6.3 billion by 2035.

The global food hydrocolloids industry is witnessing steady growth as demand increases for functional ingredients that enhance texture, stability, and shelf life across processed food products. Food hydrocolloids are widely used as gelling, thickening, and stabilizing agents derived from plant, animal, microbial, and seaweed sources. These ingredients play a vital role in improving viscosity and structural integrity in food systems, making them essential across bakery, confectionery, dairy, and beverage applications. Their ability to maintain performance under varying thermal conditions, pH levels, and mechanical stress further strengthens their use in both ambient and chilled food products. Increasing consumer preference for clean-label ingredients is also driving demand, as hydrocolloids provide natural functionality without synthetic additives. Advancements in extraction and purification technologies are further enhancing product quality, enabling better control over molecular structure and performance characteristics. The integration of enzymatic processing and controlled hydrolysis techniques is allowing manufacturers to tailor functional properties such as gel strength and viscosity, thereby expanding application potential across modern food formulations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.2 Billion |

| Forecast Value | $6.3 Billion |

| CAGR | 4.2% |

The gelatin gum segment accounted for USD 1.4 billion in 2025 owing to its strong gelling performance and wide applicability. This segment is highly valued for its thermoreversible properties, making it suitable for confectionery, dairy, and pharmaceutical uses. Ongoing improvements in processing techniques have enabled manufacturers to develop gelatin with customized bloom strength levels to meet diverse formulation requirements. At the same time, plant-based hydrocolloids such as pectin are gaining traction due to their suitability in low-sugar and fruit-based applications, particularly within clean-label product development.

The plant-derived segment captured USD 2.7 billion in 2025, supported by increasing demand for vegan-friendly and naturally sourced ingredients. This category continues to grow as food manufacturers align with clean-label trends and consumer preference for plant-based formulations. While animal-derived hydrocolloids remain important in certain applications, plant-based alternatives are expanding their presence across multiple food categories. Seaweed-based hydrocolloids are also witnessing strong adoption, particularly in stabilization and gel formation applications across dairy and meat product formulations.

North America Food Hydrocolloids Market is projected to grow from USD 1.2 billion in 2025 to USD 1.8 billion by 2035 driven by the rising adoption of clean-label ingredients and increased focus on natural food formulation strategies. Food manufacturers are increasingly shifting toward plant-based and transparent ingredient systems to align with consumer expectations. The growth of plant-based food products, combined with rising demand for natural stabilizers in dairy alternatives, bakery goods, and functional beverages, is further supporting market development across the region.

Key companies operating in the Global Food Hydrocolloids Market include Ingredion Incorporated, Kerry Group plc, Tate & Lyle PLC, Cargill, FMC Corporation, DuPont de Nemours, Inc., CP Kelco, Koninklijke DSM N.V., Lonza Group AG, Ashland Global Holdings Inc., Gum Technology Corporation, and TIC Gums, Inc. Companies in the Food Hydrocolloids Market are focusing on strategic initiatives to strengthen their market position and expand global reach. A key focus is investment in research and development to enhance functional performance, improve stability, and expand application versatility across food systems. Manufacturers are developing advanced extraction and modification technologies to achieve precise control over viscosity, gel strength, and texture properties. Strategic collaborations with food and beverage producers are helping companies tailor solutions to evolving formulation needs. Expansion of production capacities and modernization of processing facilities are supporting rising demand for clean-label ingredients. Companies are also prioritizing sustainability by sourcing raw materials responsibly and reducing environmental impact in production processes. Product innovation in plant-based and seaweed-derived hydrocolloids is further strengthening portfolio diversification. In addition, mergers, acquisitions, and global expansion strategies are enabling firms to improve market access, strengthen distribution networks, and enhance competitive positioning across regional markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type

- 2.2.2 Form

- 2.2.3 Application

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Gelatin Gum

- 5.3 Pectin

- 5.4 Xanthan Gum

- 5.5 Guar Gum

- 5.6 Carrageenan

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Source, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Plant (Terrestrial)

- 6.3 Animal

- 6.4 Seaweed/Marine

- 6.5 Synthetic/Modified

- 6.6 Microbial

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Bakery and Confectionery

- 7.3 Dairy and Frozen Products

- 7.4 Beverages

- 7.5 Meat and Seafood Products

- 7.6 Other Applications

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Ashland Global Holdings Inc.

- 9.2 Cargill, Incorporated

- 9.3 CP Kelco

- 9.4 DuPont de Nemours, Inc.

- 9.5 FMC Corporation

- 9.6 Gum Technology Corporation

- 9.7 Ingredion Incorporated

- 9.8 Kerry Group plc

- 9.9 Koninklijke DSM N.V.

- 9.10 Lonza Group AG

- 9.11 Tate & Lyle PLC

- 9.12 TIC Gums, Inc.