|

시장보고서

상품코드

2027663

프로그래머블 로직 컨트롤러(PLC) : 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Programmable Logic Controller (PLC) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

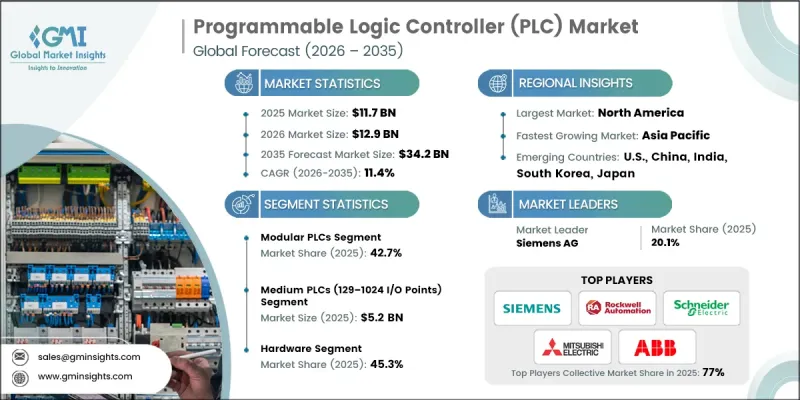

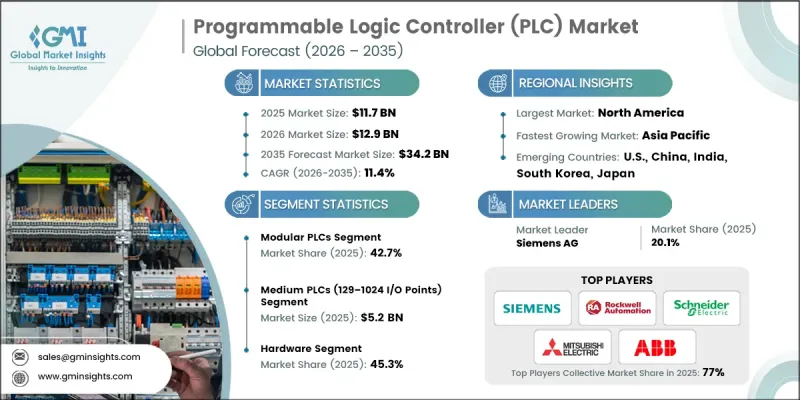

세계의 프로그래머블 로직 컨트롤러(PLC) 시장은 2025년에 117억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 11.4%를 나타내 342억 달러에 이를 것으로 추정되고 있습니다.

이러한 시장 확대는 자동차 및 전자제품 제조 산업의 급속한 공장 자동화, 이산형 산업에서의 인더스트리 4.0 기술 도입 확대, 석유 및 가스 사업에서의 실시간 공정 제어에 대한 수요 증가, PLC와 디지털 산업 플랫폼의 통합이 주도하고 있습니다. 주도하고 있습니다. 또한, 신재생에너지 프로젝트와 고정밀 제조 환경에서의 자동화 시스템 도입 확대도 시장 성장을 가속화하고 있습니다. PLC는 복잡한 생산 공정을 관리하고, 로봇을 연계하고, 운영 효율을 향상시키는 데 있어 점점 더 중요한 역할을 하고 있습니다. 제조업체들은 다운타임을 최소화하고 생산성을 향상시키기 위해 스마트 팩토리 개념, 기계 간 상호 연결 및 클라우드 기반 모니터링을 우선시하고 있으며, 이는 다양한 산업 분야에서 견조한 시장 도입을 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 117억 달러 |

| 예측액 | 342억 달러 |

| CAGR | 11.4% |

2025년 기준, 모듈형 PLC 부문은 42.7%의 점유율을 차지했습니다. 이 시스템은 복잡한 산업 운영에 대응할 수 있는 확장 가능한 솔루션을 제공하는 동시에 다른 자동화 기술과의 원활한 통합이 가능하기 때문에 자동차, 석유, 가스 및 제조 환경에 이상적입니다.

129-1024개의 I/O 포인트가 있는 중형 PLC 부문은 2025년 52억 달러에 달했습니다. 성능과 비용 효율성의 균형이 뛰어나며, 반자동화된 디지털 커넥티드 생산 시스템으로 전환하는 중규모 플랜트에서 중간 정도의 복잡한 자동화 프로세스를 지원합니다.

2025년 북미 프로그래머블 로직 컨트롤러(PLC) 시장은 36.3%의 점유율을 차지했습니다. 이 지역의 성장은 자동차, 석유 및 가스, 식품 가공 부문에서 산업 자동화의 강력한 도입과 함께 스마트 제조 및 산업용 IoT 솔루션의 확산에 힘입어 성장세를 보이고 있습니다. PLC와 클라우드 기반 제어 시스템의 통합은 운영 효율성과 실시간 모니터링을 향상시킵니다. 다운타임을 최소화하고 생산 유연성 향상에 초점을 맞추어 레거시 시설 전반에 걸쳐 PLC 업그레이드가 광범위하게 이루어지고 있습니다. 디지털 제조와 탄력적인 공급망에 대한 정부의 이니셔티브와 민간의 투자는 자동화 기술 분야에서 북미의 리더십을 더욱 강화시키고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 용량별(2022-2035년)

제7장 시장 추산 및 예측 : 구성 요소별(2022-2035년)

제8장 시장 추산 및 예측 : 제공별(2022-2035년)

제9장 시장 추산 및 예측 : 기능별(2022-2035년)

제10장 시장 추산 및 예측 : 설치 유형별(2022-2035년)

제11장 시장 추산 및 예측 : 최종 사용자 산업별(2022-2035년)

제12장 시장 추산 및 예측 : 지역별(2022-2035년)

제13장 기업 개요

KTH 26.05.20The Global Programmable Logic Controller (PLC) Market was valued at USD 11.7 billion in 2025 and is estimated to grow at a CAGR of 11.4% to reach USD 34.2 billion by 2035.

The market expansion is driven by rapid factory automation across automotive and electronics manufacturing, increasing adoption of Industry 4.0 technologies in discrete industries, growing demand for real-time process control in oil & gas operations, and wider integration of PLCs with digital industrial platforms. Additionally, the rising deployment of automation systems in renewable energy projects and high-precision manufacturing environments is accelerating market growth. PLCs are increasingly critical for managing complex production processes, coordinating robotics, and enhancing operational efficiency. Manufacturers are prioritizing smart factory initiatives, interconnected machines, and cloud-based monitoring to minimize downtime and improve productivity, supporting robust market adoption across diverse industrial sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $11.7 Billion |

| Forecast Value | $34.2 Billion |

| CAGR | 11.4% |

The modular PLCs segment held a 42.7% share in 2025. These systems offer scalable solutions that can handle complex industrial operations while allowing seamless integration with other automation technologies, making them ideal for automotive, oil, gas, and manufacturing environments.

The medium PLCs, with 129-1024 I/O points, segment reached USD 5.2 billion in 2025. They provide a balance of performance and cost efficiency, supporting moderate-to-complex automation processes in mid-sized plants transitioning toward semi-automated, digitally connected production systems.

North America Programmable Logic Controller (PLC) Market held a 36.3% share in 2025. The region's growth is driven by strong adoption of industrial automation across automotive, oil & gas, and food processing sectors, coupled with increased deployment of smart manufacturing and industrial IoT solutions. Integration of PLCs with cloud-based control systems enhances operational efficiency and real-time monitoring. The focus on minimizing downtime and boosting production flexibility has led to widespread PLC upgrades across legacy facilities. Government initiatives and private investments in digital manufacturing and resilient supply chains further reinforce North America's leadership in automation technologies.

Key players operating in the Global Programmable Logic Controller (PLC) Market include ABB Ltd., Beckhoff Automation, Bosch Rexroth AG, Delta Electronics, Emerson Electric Co., Fuji Electric, Hitachi Industrial Equipment Systems, Honeywell International Inc., Mitsubishi Electric, Omron Corporation, Panasonic Industry, Phoenix Contact, Rockwell Automation, Schneider Electric, and Siemens AG. Key strategies adopted by companies in the Global Programmable Logic Controller (PLC) Market include expanding product portfolios with modular and medium-capacity controllers, investing in R&D for Industry 4.0-compatible solutions, and strengthening partnerships with system integrators to access new industrial sectors. Companies focus on developing IoT-enabled PLCs with cloud connectivity, cybersecurity features, and advanced analytics to improve operational efficiency for clients. Strategic mergers, acquisitions, and collaborations with technology providers help enhance market reach and adoption in high-growth regions. Continuous innovation in scalable, flexible, and energy-efficient PLC solutions supports companies in maintaining a competitive advantage and increasing their global footprint.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.3 Type trends

- 2.3.1 Capacity trends

- 2.3.2 Component trends

- 2.3.3 Offering trends

- 2.3.4 Functionality trends

- 2.3.5 Installation type trends

- 2.3.6 End-user industry trends

- 2.3.7 Regional trends

- 2.4 TAM Analysis, 2026-2035

- 2.5 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid factory automation across automotive and electronics manufacturing

- 3.2.1.2 Increasing adoption of Industry 4.0 in discrete industries

- 3.2.1.3 Rising demand for real-time process control in oil & gas

- 3.2.1.4 Integration of PLCs with SCADA and MES systems

- 3.2.1.5 Growth in renewable energy plant automation projects

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Cybersecurity vulnerabilities in connected PLC environments

- 3.2.2.2 Skilled workforce shortage for advanced PLC programming

- 3.2.3 Market opportunities

- 3.2.3.1 Edge-enabled PLCs for low-latency industrial analytics

- 3.2.3.2 Increasing PLC deployment in EV battery manufacturing lines

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Compact/integrated PLCs

- 5.3 Modular PLCs

- 5.4 Rack-mounted PLCs

Chapter 6 Market Estimates and Forecast, By Capacity, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Nano/micro PLCs (≤32 I/O Points)

- 6.3 Small PLCs (33-128 I/O Points)

- 6.4 Medium PLCs (129-1024 I/O Points)

- 6.5 Large PLCs (>1024 I/O Points)

Chapter 7 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 CPU/processor modules

- 7.3 I/O modules

- 7.4 Power supply modules

- 7.5 Communication modules

Chapter 8 Market Estimates and Forecast, By Offering, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Hardware

- 8.3 Software

- 8.4 Services

Chapter 9 Market Estimates and Forecast, By Functionality, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Discrete control

- 9.3 Process control

- 9.4 Motion control

- 9.5 Safety control

Chapter 10 Market Estimates and Forecast, By Installation Type, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 New installations

- 10.3 Retrofit/replacement

Chapter 11 Market Estimates and Forecast, By End-User Industry, 2022 - 2035 (USD Million)

- 11.1 Key trends

- 11.2 Automotive

- 11.3 Oil & gas

- 11.4 Energy & power

- 11.5 Food & beverage

- 11.6 Pharmaceuticals

- 11.7 Water & wastewater

- 11.8 Chemicals

- 11.9 Metals & mining

- 11.10 Pulp & paper

- 11.11 Others

Chapter 12 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Spain

- 12.3.5 Italy

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.6 Middle East and Africa

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global Key Players

- 13.1.1 Siemens AG

- 13.1.2 Rockwell Automation

- 13.1.3 Schneider Electric

- 13.1.4 ABB Ltd.

- 13.1.5 Mitsubishi Electric

- 13.2 Regional key players

- 13.2.1 North America

- 13.2.1.1 Emerson Electric Co.

- 13.2.1.2 Honeywell International Inc.

- 13.2.2 Asia Pacific

- 13.2.2.1 Omron Corporation

- 13.2.2.2 Delta Electronics

- 13.2.2.3 Fuji Electric

- 13.2.2.4 Hitachi Industrial Equipment Systems

- 13.2.2.5 Panasonic Industry

- 13.2.3 Europe

- 13.2.3.1 Bosch Rexroth AG

- 13.2.3.2 Phoenix Contact

- 13.2.1 North America

- 13.3 Niche Players/Disruptors

- 13.3.1 Beckhoff Automation