|

시장보고서

상품코드

2027667

비디오 감시 : 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Video Surveillance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

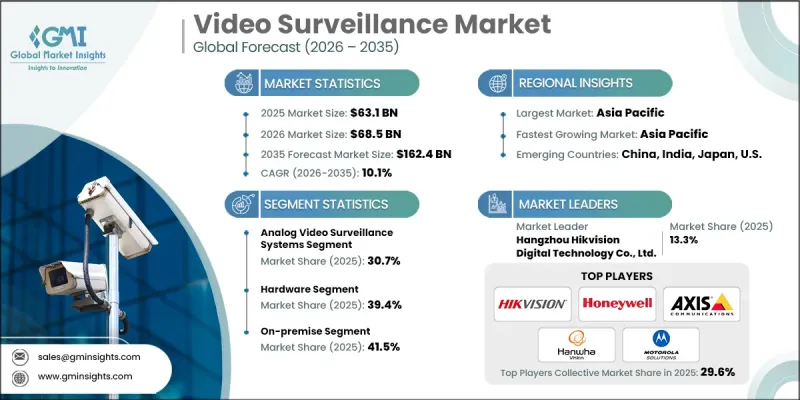

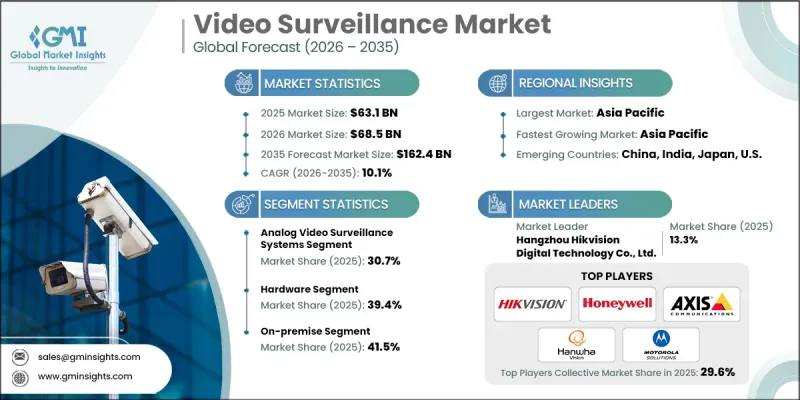

세계의 비디오 감시 시장은 2025년에 631억 달러로 평가되었고 CAGR 10.1%를 나타내 2035년까지 1,624억 달러에 이를 것으로 추정되고 있습니다.

시장 확대는 첨단 보안 기술의 도입 확대와 공공 및 민간 인프라 전반에 걸쳐 실시간 모니터링에 대한 중요성이 높아짐에 따라 주도되고 있습니다. 범죄, 테러, 안전 위협과 관련된 보안에 대한 우려가 높아지면서 전 세계적으로 감시 시스템 도입이 크게 가속화되고 있습니다. 동시에 엣지 기반 인공지능(AI)의 통합이 주요 성장 촉매제로 부상하고 있으며, 이를 통해 더 빠른 데이터 처리, 더 낮은 지연 시간, 더 나은 프라이버시 관리를 가능하게 합니다. 이러한 기능은 즉각적인 대응과 지속적인 모니터링이 필요한 환경에서 특히 가치가 있습니다. 또한, 비디오 감시를 출입 통제 시스템 및 경보 솔루션과 통합하여 전반적인 보호를 강화하는 '통합 보안 에코시스템'의 추세도 강화되고 있습니다. 모든 부문의 조직이 안전 규정 준수를 점점 더 우선순위로 삼고 있으며, 이는 시스템 도입을 더욱 촉진하고 있습니다. 디지털 전환이 가속화됨에 따라 상업, 산업, 공공 부문 용도에서 지능적이고 연결성이 높으며 확장성이 뛰어난 모니터링 솔루션에 대한 수요가 지속적으로 증가하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 631억 달러 |

| 예측액 | 1,624억 달러 |

| CAGR | 10.1% |

2025년 기준, 아날로그 비디오 감시 시스템 부문은 30.7%의 점유율을 차지했습니다. 이 부문은 IP 기반 및 AI 지원 기술로의 전환으로 인해 점차 축소되고 있지만, 비용 중심의 환경에서는 여전히 중요한 역할을 하고 있습니다. 이러한 시스템은 주로 기본적인 모니터링 요구 사항으로 충분한 소규모 설치 및 레거시 인프라에서 주로 활용되고 있습니다. 또한, 이 부문은 전체 시스템을 교체할 필요 없이 부분적인 디지털화를 가능하게 하는 하이브리드 DVR 솔루션을 통해 진화하고 있으며, 특정 용도의 지속적인 활용을 지원하고 있습니다.

하드웨어 부문은 2025년 39.4%의 점유율을 차지했습니다. 이 부문은 고해상도 카메라, 스토리지 시스템, 네트워크 인프라 구성 요소 등 첨단 감시 장치에 대한 수요가 견고하여 시장을 지속적으로 주도하고 있습니다. 인공지능 기능이 탑재된 스마트 카메라의 도입이 진행되면서 실시간 분석과 자동화된 의사결정이 강화되고 있습니다. 또한, 교통망, 상업시설, 공공 인프라 전반에 걸친 첨단 녹화 시스템 및 센서 기반 기술의 도입은 하드웨어 수요를 더욱 촉진하고 있습니다.

2025년 북미의 비디오 감시 시장은 31.1%의 점유율을 차지했습니다. 이 지역에서는 의료, 교통, 소매, 스마트시티 프로젝트 등 다양한 분야에서 AI 탑재형 및 클라우드 통합형 모니터링 시스템 도입이 빠르게 진행되고 있습니다. 공공 안전과 보안에 대한 우려가 높아지면서 첨단 감시 인프라에 대한 투자가 증가하고 있습니다. 원격 모니터링 및 규제 준수에 대한 요구가 증가함에 따라 조직은 레거시 시스템을 현대화하고 데이터 분석 및 자동화 기술을 기반으로 한 지능형 커넥티드 솔루션을 채택하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제공별(2022-2035년)

제6장 시장 추산 및 예측 : 전개 형태별(2022-2035년)

제7장 시장 추산 및 예측 : 시스템 유형별(2022-2035년)

제8장 시장 추산 및 예측 : 용도별(2022-2035년)

제9장 시장 추산 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

KTH 26.05.20The Global Video Surveillance Market was valued at USD 63.1 billion in 2025 and is estimated to grow at a CAGR of 10.1% to reach USD 162.4 billion by 2035.

Market expansion is driven by the rising adoption of advanced security technologies and the growing emphasis on real-time monitoring across public and private infrastructure. Increasing security concerns related to crime, terrorism, and safety threats are significantly accelerating the deployment of surveillance systems worldwide. At the same time, the integration of edge-based artificial intelligence is emerging as a key growth catalyst, enabling faster data processing, reduced latency, and improved privacy management. These capabilities are particularly valuable in environments that require immediate response and continuous monitoring. There is also a growing trend toward unified security ecosystems, where video surveillance is integrated with access control systems and alarm solutions to enhance overall protection. Organizations across sectors are increasingly prioritizing compliance with safety regulations, which is further driving system adoption. As digital transformation accelerates, demand for intelligent, connected, and scalable surveillance solutions continues to rise across commercial, industrial, and public sector applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $63.1 Billion |

| Forecast Value | $162.4 Billion |

| CAGR | 10.1% |

The analog video surveillance systems segment accounted for 30.7% share in 2025. Although this segment is gradually declining due to the shift toward IP-based and AI-enabled technologies, it still maintains relevance in cost-sensitive environments. These systems are primarily used in smaller-scale installations and legacy infrastructures where basic monitoring requirements are sufficient. The segment is also evolving through hybrid DVR solutions that allow partial digital transition without requiring full system replacement, thereby supporting continued usage in specific applications.

The hardware segment held a 39.4% share in 2025. This segment continues to dominate due to strong demand for advanced surveillance devices such as high-resolution cameras, storage systems, and network infrastructure components. The increasing adoption of smart cameras equipped with artificial intelligence capabilities is enhancing real-time analytics and automated decision-making. Additionally, the deployment of advanced recording systems and sensor-based technologies across transportation networks, commercial spaces, and public infrastructure is further strengthening hardware demand.

North America Video Surveillance Market accounted for 31.1% share in 2025. The region is experiencing strong adoption of AI-powered and cloud-integrated surveillance systems across multiple sectors, including healthcare, transportation, retail, and smart city projects. Growing concerns around public safety and security are driving investments in advanced monitoring infrastructure. The increasing need for remote surveillance and regulatory compliance is also encouraging organizations to modernize legacy systems and adopt intelligent, connected solutions supported by data analytics and automation technologies.

Key companies operating in the Global Video Surveillance Market include Motorola Solutions, Inc., Axis Communications AB, Bosch Security Systems, CP Plus International, Dahua Technology Co., Ltd, Genetec Inc., Hangzhou Hikvision Digital Technology Co., Ltd., Hanwha Vision Co., Ltd., and Honeywell. Companies in the Video Surveillance Market are strengthening their competitive position through continuous technological innovation, strategic partnerships, and expansion of AI-driven solutions. They are investing heavily in edge computing, artificial intelligence, and cloud-based platforms to enhance real-time monitoring and data processing capabilities. Many players are focusing on developing high-performance cameras and integrated security systems that combine video analytics, access control, and alarm management. Expansion into smart city projects and critical infrastructure sectors is also supporting market growth. Additionally, companies are enhancing their global distribution networks and service capabilities to improve customer reach.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Offering trends

- 2.2.2 Deployment trends

- 2.2.3 System type trends

- 2.2.4 Application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of edge-based Artificial Intelligence (AI)

- 3.2.1.2 Increasing security concerns

- 3.2.1.3 Shift toward smart cities and adopting smart security systems

- 3.2.1.4 Growing demand for remote monitoring

- 3.2.1.5 Growing usage of cloud-based surveillance systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Integration complexity

- 3.2.2.2 Privacy concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for real-time video analytics in public safety and transportation

- 3.2.3.2 Advancements in low-power, high-performance AI chipsets for edge devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Offering, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Cameras

- 5.2.2 Storage devices

- 5.2.3 Monitors

- 5.2.4 Others

- 5.3 Software

- 5.3.1 Video analytics

- 5.3.2 Video management software (VMS)

- 5.3.3 Access control software

- 5.3.4 Others

- 5.4 Services

- 5.4.1 Video surveillance as a service (VSaaS)

- 5.4.2 Installation & maintenance

- 5.4.3 Consulting & system integration

Chapter 6 Market Estimates and Forecast, By Deployment, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 On-premise

- 6.3 Cloud

- 6.4 Hybrid

Chapter 7 Market Estimates and Forecast, By System Type, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Analog video surveillance systems

- 7.3 IP video surveillance systems

- 7.4 Hybrid video surveillance systems

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Commercial

- 8.2.1 Retail

- 8.2.2 Banking & finance

- 8.2.3 Hospitality

- 8.2.4 Healthcare

- 8.2.5 Others

- 8.3 Residential

- 8.4 Industrial

- 8.4.1 Manufacturing

- 8.4.2 Oil & gas

- 8.4.3 Energy

- 8.4.4 Others

- 8.5 Infrastructure & Transportation

- 8.5.1 Transportation

- 8.5.2 City surveillance

- 8.5.3 Defense

- 8.5.4 Others

- 8.6 Institutional

- 8.6.1 Education

- 8.6.2 Religious buildings

- 8.6.3 Sports & entertainment venues

- 8.6.4 Others

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.3.7 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Rest of MEA

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Motorola Solutions, Inc.

- 10.1.2 Axis Communications AB

- 10.1.3 Bosch Security Systems

- 10.1.4 Dahua Technology Co., Ltd

- 10.1.5 Genetec Inc.

- 10.1.6 Hangzhou Hikvision Digital Technology Co., Ltd.

- 10.1.7 Hanwha Vision Co., Ltd.

- 10.1.8 Honeywell

- 10.1.9 Johnson Controls

- 10.1.10 Panasonic

- 10.1.11 Sony India Private Limited

- 10.1.12 Teledyne FLIR LLC

- 10.2 Regional key players

- 10.2.1 CP Plus International

- 10.2.2 Infinova Group

- 10.2.3 VIVOTEK Inc.

- 10.2.4 Uniview

- 10.3 Niche Players/Disruptors

- 10.3.1 Verkada Inc.

- 10.3.2 Eagle Eye Networks

- 10.3.3 Deep Sentinel