|

시장보고서

상품코드

2038369

위성 지상국 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Satellite Ground Station Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

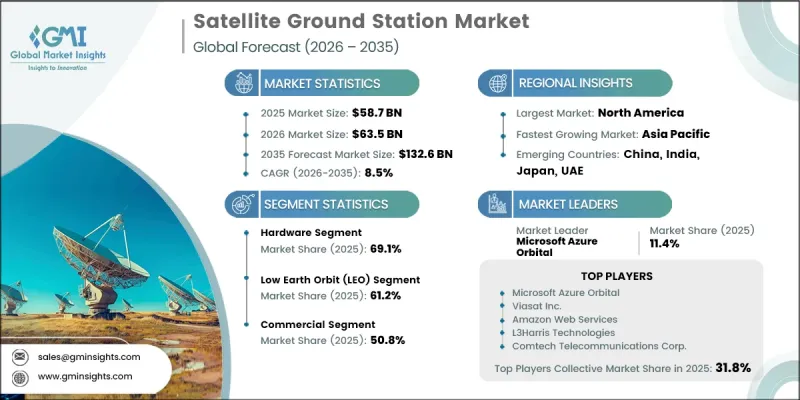

세계의 위성 지상국 시장은 2025년에 587억 달러로 평가되었고, CAGR 8.5%로 성장할 전망이며, 2035년까지 1,326억 달러에 이를 것으로 예측됩니다.

시장 성장은 위성방송 서비스의 보급 확대와 통신 효율과 데이터 처리 능력을 향상시키는 지상국 기술의 지속적인 발전에 의해 주도되고 있습니다. 또한, 위성을 이용한 원격 감지 용도에 대한 수요 증가와 우주 탐사 및 조사 활동을 촉진하기 위한 정부의 지원책도 시장 확대에 크게 기여하고 있습니다. 위성 발사가 급증하고 대용량 세계 연결에 대한 수요가 증가함에 따라 첨단 지상 인프라에 대한 수요가 더욱 가속화되고 있습니다. 또한, 지구관측 데이터의 확대와 분석 기반 용도의 확산으로 인해 상업 및 기관 부문 전반에 걸쳐 위성 지상국의 중요성이 커지고 있습니다. 고해상도, 초고해상도 및 실시간 컨텐츠 전송에 대한 의존도가 높아짐에 따라 신호 송수신에 대한 인프라 요구사항이 강화되고 있습니다. 또한, 자동추적 시스템, 클라우드 통합형 지상국 솔루션, 지속적인 위성 모니터링 및 데이터 교환을 가능하게 하는 확장성 높은 통신 네트워크에 대한 투자 확대도 시장을 더욱 뒷받침하고 있습니다. 이러한 요소들이 결합되어 위성 지상국은 전 세계 현대 우주 통신 생태계에서 필수적인 구성 요소로 자리매김하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 587억 달러 |

| 예측 시장 규모 | 1,326억 달러 |

| CAGR | 8.5% |

2025년에는 하드웨어 부문이 69.1%의 점유율을 차지했습니다. 이러한 압도적인 점유율은 안정적인 위성 통신 운영에 필수적인 안테나, RF 시스템, 위성 추적 기술 및 지원 인프라를 광범위하게 도입했기 때문입니다. 하드웨어는 정지궤도 및 저궤도 위성 시스템 모두에서 효율적인 원격 측정, 추적, 명령 및 신호 전송을 가능하게 하는 지상 부문 기능의 핵심입니다. 대규모 위성 별자리 배치 증가와 전 세계 지상 네트워크의 확장으로 인해 고급 및 고성능 하드웨어 시스템에 대한 수요가 더욱 증가하고 있습니다.

2025년에는 저궤도(LEO) 부문이 61.2%의 점유율을 차지했습니다. 이러한 선도적 위치는 광대역 연결, 지구관측 서비스 및 사물인터넷(IoT) 용도에 사용되는 LEO 위성 별자리의 급속한 확대로 인해 주도권을 확보할 수 있게 되었습니다. LEO 위성은 궤도 주기가 짧고 자주 이동하기 때문에 광범위한 지상국의 커버리지와 지속적인 추적 지원이 필요합니다. 이에 따라 통신 중단을 방지하고 효율적인 위성 핸드오버 관리를 보장하기 위해 자동화된 실시간 모니터링 기술 및 첨단 데이터 처리 시스템에 대한 투자가 가속화되고 있습니다.

북미의 위성 지상국 시장은 2025년 42.6%의 점유율을 차지했습니다. 이는 탄탄한 기술 인프라와 확대되는 위성 통신 수요에 힘입은 것입니다. 이 지역 시장 성장은 LEO 위성 네트워크의 급속한 확장과 미국 및 캐나다 전역의 광대역 및 지구관측 서비스에 대한 수요 증가에 의해 주도되고 있습니다. 이 지역은 항공우주 기술, 클라우드 기반 지상국 플랫폼의 광범위한 도입, 안전한 위성 통신 시스템에 대한 정부의 막대한 투자로 인해 세계 시장에서의 리더십을 강화하고 있습니다.

Amazon Web Services, Microsoft Azure Orbital, L3Harris Technologies, Viasat Inc. Hughes Network Systems(EchoStar), Kongsberg Satellite Services(KSAT), Swedish Space Corporation(SSC), Gilat Satellite Networks, Atlas Space Operations, RBC Signals, Comtech Telecommunications Corp., Leaf Space, QuadSAT, Northstar Earth & Space, KLEO Connect, European Space Agency(ESA) 및 Japan Aerospace Exploration Agency(JAXA) 등이 세계 위성 지상국 시장에서 활동하는 주요 기업 중 일부입니다. 위성 지상국 시장 업체들은 운영 효율성과 확장성을 강화하기 위해 자동화 및 클라우드 통합형 지상 인프라 확충에 주력하고 있습니다. 통신의 신뢰성을 높이기 위해 첨단 추적 시스템, AI를 활용한 데이터 처리, 실시간 위성 모니터링 솔루션에 투자하고 있습니다. 위성 사업자 및 클라우드 서비스 제공업체와의 전략적 제휴를 통해 서비스 제공 범위 확대 및 지상 네트워크의 신속한 구축이 가능해졌습니다. 또한, 각 업체들은 운영 비용 절감과 유연성 향상을 위해 모듈식 및 소프트웨어 정의형 지상국 아키텍처 개발에 우선순위를 두고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 솔루션 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 플랫폼 유형별(2022-2035년)

제7장 시장 추산 및 예측 : 주파수대별(2022-2035년)

제8장 시장 추산 및 예측 : 궤도 유형별(2022-2035년)

제9장 시장 추산 및 예측 : 용도별(2022-2035년)

제10장 시장 추산 및 예측 : 최종 사용자별(2022-2035년)

제11장 시장 추산 및 예측 : 지역별(2022-2035년)

제12장 기업 개요

AJY 26.06.11The Global Satellite Ground Station Market was valued at USD 58.7 billion in 2025 and is estimated to grow at a CAGR of 8.5% to reach USD 132.6 billion by 2035.

Market growth is driven by the increasing penetration of satellite-based broadcasting services and continuous advancements in ground station technologies that enhance communication efficiency and data processing capabilities. Rising demand for satellite-enabled remote sensing applications is also contributing significantly to expansion, alongside supportive government initiatives promoting space exploration and research activities. The rapid increase in satellite launches and the growing need for high-capacity global connectivity are further accelerating demand for advanced ground infrastructure. In addition, the expansion of Earth observation data, along with analytics-driven applications, is strengthening the importance of satellite ground stations across commercial and institutional sectors. Increasing reliance on high-definition, ultra-high-definition, and real-time content delivery is also reinforcing infrastructure requirements for signal transmission and reception. The market is further supported by growing investments in automated tracking systems, cloud-integrated ground station solutions, and scalable communication networks that enable continuous satellite monitoring and data exchange. These combined factors are positioning satellite ground stations as a critical component of modern space-based communication ecosystems worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $58.7 Billion |

| Forecast Value | $132.6 Billion |

| CAGR | 8.5% |

The hardware segment accounted for a share of 69.1% in 2025. This dominance is attributed to the extensive deployment of antennas, RF systems, satellite tracking technologies, and supporting infrastructure essential for reliable satellite communication operations. Hardware forms the core foundation of ground segment functionality, enabling efficient telemetry, tracking, command, and signal transmission across both geostationary and low Earth orbit satellite systems. Increasing deployment of large satellite constellations and expanding global ground networks is further strengthening demand for advanced and high-performance hardware systems.

The Low Earth Orbit segment held a 61.2% share in 2025. This leadership is driven by the rapid expansion of LEO satellite constellations used for broadband connectivity, Earth observation services, and Internet of Things applications. Due to their short orbital duration and frequent movement, LEO satellites require extensive ground station coverage and continuous tracking support. This is accelerating investment in automated, real-time monitoring technologies and advanced data processing systems to ensure uninterrupted communication and efficient satellite handover management.

North America Satellite Ground Station Market accounted for 42.6% share in 2025, supported by strong technological infrastructure and growing satellite communication requirements. Market growth in the region is driven by the rapid expansion of LEO satellite networks and increasing demand for broadband and Earth observation services across the United States and Canada. The region benefits from well-established aerospace capabilities, widespread adoption of cloud-based ground station platforms, and substantial government investment in secure satellite communication systems, strengthening its leadership in the global market.

Amazon Web Services, Microsoft Azure Orbital, L3Harris Technologies, Viasat Inc., Hughes Network Systems (EchoStar), Kongsberg Satellite Services (KSAT), Swedish Space Corporation (SSC), Gilat Satellite Networks, Atlas Space Operations, RBC Signals, Comtech Telecommunications Corp., Leaf Space, QuadSAT, Northstar Earth & Space, KLEO Connect, European Space Agency (ESA), and Japan Aerospace Exploration Agency (JAXA) are among the key players operating in the Global Satellite Ground Station Market. Companies in the Satellite Ground Station Market are focusing on expanding automated and cloud-integrated ground infrastructure to strengthen operational efficiency and scalability. They are investing in advanced tracking systems, AI-driven data processing, and real-time satellite monitoring solutions to improve communication reliability. Strategic partnerships with satellite operators and cloud service providers are enabling wider service coverage and faster deployment of ground networks. Firms are also prioritizing the development of modular and software-defined ground station architectures to reduce operational costs and increase flexibility.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Solution type trends

- 2.2.2 Platform type trends

- 2.2.3 Frequency band trends

- 2.2.4 Orbit type trends

- 2.2.5 Application trends

- 2.2.6 End-user trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased penetration of satellite-based broadcasting services.

- 3.2.1.2 Continuous technological advancements in satellite ground stations.

- 3.2.1.3 Rising satellite service demand for remote sensing applications.

- 3.2.1.4 Favorable government initiatives to support space research agencies.

- 3.2.1.5 Proliferation of Earth observation imagery and analytics solutions.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of regulations and government policies.

- 3.2.2.2 Constant bandwidth issues.

- 3.2.3 Market opportunities

- 3.2.3.1 AI-enabled autonomous ground station operations

- 3.2.3.2 Virtualized and shared ground station networks

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends (Based on paid Database)

- 3.8.1 Historical Price Analysis (2022-2025)

- 3.8.2 Price Trend Drivers

- 3.8.3 Regional Price Variations

- 3.8.4 Price Forecast (2026-2035)

- 3.9 Impact of AI & Generative AI on the Market

- 3.9.1 AI-Driven Disruption of Existing Business Models

- 3.9.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.9.3 Risks, Limitations & Regulatory Considerations

- 3.10 Capacity & Production Landscape (Driven by Primary Research)

- 3.10.1 Installed Capacity by Region & Key Producer

- 3.10.2 Capacity Utilization Rates & Expansion Pipelines

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Solution Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Antenna systems

- 5.2.2 RF systems & timing

- 5.2.3 Baseband & recording hardware

- 5.2.4 Storage & networking units

- 5.2.5 Power & racks

- 5.3 Software

- 5.3.1 Mission control & flight dynamics

- 5.3.2 Baseband/virtual modems & waveforms

- 5.3.3 Cybersecurity & key management

- 5.3.4 Network M&C/orchestration

- 5.4 Services

- 5.4.1 Direct-to-Satellite (DTS)

- 5.4.2 Satellite ground station backhaul

- 5.4.3 Managed services & system integration

Chapter 6 Market Estimates and Forecast, By Platform Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Fixed

- 6.3 Portable

- 6.4 Mobile stations

Chapter 7 Market Estimates and Forecast, By Frequency Band, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 L-Band

- 7.3 S-Band

- 7.4 C-Band

- 7.5 X-Band

- 7.6 Ku & Ka-Band

- 7.7 HF/VHF/UHF-Band

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Orbit Type, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Low Earth Orbit (LEO)

- 8.3 Medium Earth Orbit (MEO)

- 8.4 Geostationary Earth Orbit (GEO)

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Communication

- 9.3 Earth observation

- 9.4 Navigation

- 9.5 Space research

- 9.6 Satellite telemetry, tracking and control subsystems

- 9.7 Gateway & network interconnection

- 9.8 Others

Chapter 10 Market Estimates and Forecast, By End User, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 Defense

- 10.2.1 Army

- 10.2.2 Air force

- 10.2.3 Navy

- 10.3 Government

- 10.3.1 Public safety & civil agencies

- 10.3.2 Space agencies & research centers

- 10.4 Commercial

- 10.4.1 Satellite & teleport operators

- 10.4.2 Carriers & service providers

- 10.4.3 Enterprise & mobility

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 Kongsberg Satellite Services (KSAT)

- 12.1.2 Viasat Inc.

- 12.1.3 Amazon Web Services

- 12.1.4 Microsoft Azure Orbital

- 12.1.5 Swedish Space Corporation (SSC)

- 12.1.6 Comtech Telecommunications Corp.

- 12.1.7 L3Harris Technologies

- 12.2 Regional Players

- 12.2.1 Japan Aerospace Exploration Agency (JAXA)

- 12.2.2 European Space Agency (ESA)

- 12.2.3 Gilat Satellite Networks

- 12.2.4 Hughes Network Systems (EchoStar)

- 12.3 Emerging Players

- 12.3.1 RBC Signals

- 12.3.2 Atlas Space Operations

- 12.3.3 KLEO Connect

- 12.3.4 Leaf Space

- 12.3.5 Northstar Earth & Space

- 12.3.6 QuadSAT