|

시장보고서

상품코드

2038675

산업용 히트펌프 시장 : 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Industrial Heat Pump Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

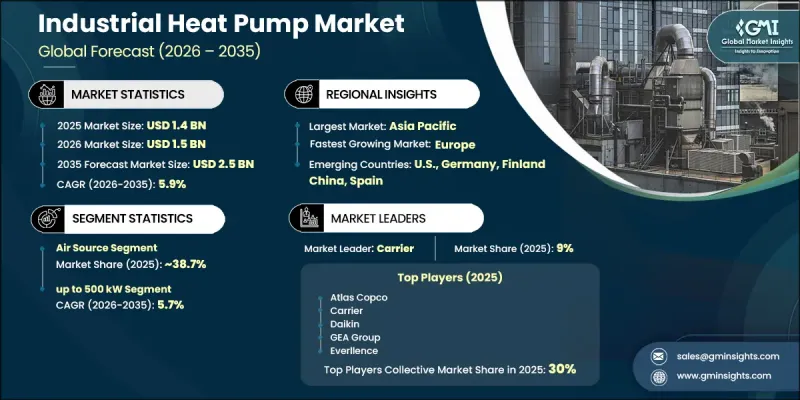

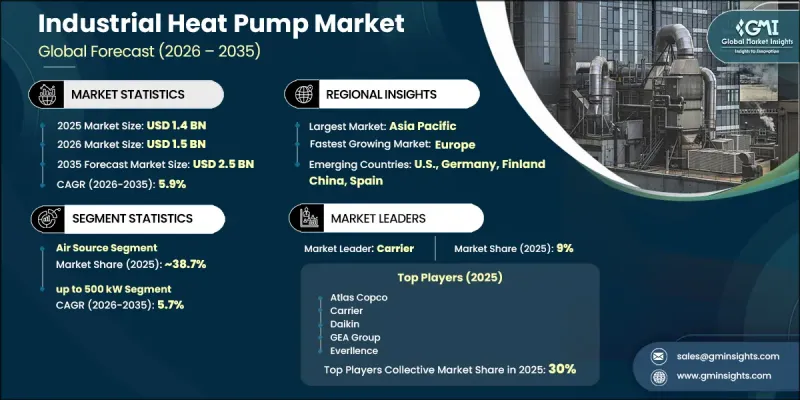

세계의 산업용 히트펌프 시장은 2025년에 14억 달러로 평가되었고, CAGR 5.9%로 성장할 전망이며, 2035년에는 25억 달러에 이를 것으로 추정되고 있습니다.

산업 분야에서 탈탄소화 및 전체 냉난방 시스템의 에너지 효율 향상에 대한 관심이 높아짐에 따라 시장이 활기를 띠고 있습니다. 산업 폐열의 회수 및 재사용을 위한 노력이 활발해지고 있는 것도 히트펌프의 도입을 더욱 촉진하고 있습니다. 히트펌프는 저급한 열을 사용 가능한 열에너지로 변환하는 효과적인 수단인 동시에 화석연료 의존도를 낮출 수 있기 때문입니다. 지속가능성 목표에 대한 관심이 높아지고, 환경 규제 강화와 탄소배출 감축 의무 도입으로 산업시설 전반에 걸쳐 도입이 가속화되고 있습니다. 전통적인 난방 기술을 에너지 효율이 높은 대체 기술로 대체하려는 움직임도 수요를 더욱 부추기고 있습니다. 또한, 신흥국의 산업 인프라 확대와 제조 공정 전반의 에너지 소비 증가도 장기적인 시장 성장에 기여하고 있습니다. 지속적인 규제 압력과 기업의 지속가능성에 대한 노력으로 인해 향후 몇 년 동안 도입률은 더욱 높아질 것으로 예측됩니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 14억 달러 |

| 예측 시장 규모 | 25억 달러 |

| CAGR | 5.9% |

지열 히트펌프 시장은 2025년 5,070만 달러 규모를 기록했으며, 산업 분야에서 탄소배출 저감에 초점을 맞추면서 냉난방 용도로 도입이 진행됨에 따라 꾸준한 성장이 예상됩니다. 이 시스템은 저온의 지열 에너지를 이용하여 산업 환경의 열전달 공정을 지원한다는 점에서 효율성과 지속가능성이 높은 평가를 받고 있습니다.

500kW-2MW 용량 부문은 2026-2035년 연평균 복합 성장률(CAGR) 5.9%를 나타낼 것으로 예측됩니다. 환경 문제에 대한 관심 증가와 탈탄소화 노력은 대규모 산업 운영을 지원할 수 있는 대용량 시스템에 대한 수요를 견인하고 있습니다. 각 제조업체들은 화석연료에 의존하는 난방에 대한 의존도를 낮추는 첨단 고출력 시스템을 개발하기 위해 연구개발, 파트너십, 제품 혁신에 대한 투자를 강화하고 있습니다.

2025년 미국의 산업용 히트펌프 시장은 85.3%의 점유율을 차지했으며, 2억 7,460만 달러 시장 규모를 기록했습니다. 이 나라의 성장은 고효율 열 시스템에 대한 산업계의 강력한 수요와 배출량 감축을 위한 엄격한 규제 프레임워크에 의해 뒷받침되고 있습니다. 또한, 대용량 산업용 히트펌프로의 전환은 저탄소 제조로의 전환과 화석연료 소비 감소를 더욱 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 규모 및 예측 : 제품별(2022-2035년)

제6장 시장 규모 및 예측 : 용량별(2022-2035년)

제7장 시장 규모 및 예측 : 온도별(2022-2035년)

제8장 시장 규모 및 예측 : 용도별(2022-2035년)

제9장 시장 규모 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

AJY 26.06.11The Global Industrial Heat Pump Market was valued at USD 1.4 billion in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 2.5 billion in 2035.

The market is gaining momentum as industries increasingly focus on decarbonizing operations and improving energy efficiency across heating and cooling systems. Rising efforts to capture and reuse industrial waste heat are further strengthening adoption, as heat pumps provide an effective way to convert low-grade heat into usable thermal energy while reducing dependence on fossil fuels. Growing emphasis on sustainability targets, coupled with stricter environmental regulations and carbon reduction mandates, is accelerating deployment across industrial facilities. The replacement of conventional heating technologies with energy-efficient alternatives is further supporting demand. Additionally, expanding industrial infrastructure in emerging economies and rising energy consumption across manufacturing processes are contributing to long-term market growth. Continuous regulatory pressure and corporate sustainability commitments are expected to further enhance adoption rates over the coming years.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.5 Billion |

| CAGR | 5.9% |

The ground source heat pump segment generated USD 50.7 million in 2025 and is projected to grow steadily as industries increase adoption for heating and cooling applications while focusing on carbon emission reduction. These systems are recognized for their efficiency and sustainability, using low-temperature geothermal energy to support thermal transfer processes across industrial environments.

The 500 kW to 2 MW capacity segment is expected to register a CAGR of 5.9% from 2026 to 2035. Rising environmental concerns and decarbonization initiatives are driving demand for high-capacity systems capable of supporting large-scale industrial operations. Manufacturers are increasingly investing in research, partnerships, and product innovation to develop advanced high-output systems that reduce reliance on fossil fuel-based heating.

United States Industrial Heat Pump Market held an 85.3% share in 2025, generating USD 274.6 million. Growth in the country is supported by strong industrial demand for efficient thermal systems and strict regulatory frameworks aimed at reducing emissions. The transition toward high-capacity industrial heat pumps is also reinforcing the shift toward low-carbon manufacturing and reduced fossil fuel consumption.

Major players operating in the Global Industrial Heat Pump Industry include Armstrong International, Atlas Copco, Carrier, Daikin Applied Europe, Johnson Controls, Mitsubishi Electric, Siemens Energy, Trane Technologies, GEA Group, and Thermax. Companies in the Industrial Heat Pump Market are prioritizing the development of high-efficiency systems that enable waste heat recovery and support large-scale industrial decarbonization goals. They are investing heavily in advanced R&D to improve system performance, capacity, and integration with existing industrial infrastructure. Strategic collaborations with industrial operators and engineering firms are being used to accelerate deployment and improve customization for sector-specific requirements. Manufacturers are also focusing on expanding product portfolios to include scalable heat pump systems suitable for diverse industrial load demands. Strengthening global supply chains and enhancing after-sales service capabilities are further helping companies improve customer retention. In addition, firms are leveraging regulatory incentives and sustainability programs to promote adoption and position their solutions as viable alternatives to conventional fossil-fuel-based heating systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid Sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Product trends

- 2.4 Capacity trends

- 2.5 Temperature trends

- 2.6 Application trends

- 2.7 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Key factors affecting the value chain

- 3.1.3 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Positive outlook toward renewable sector

- 3.2.1.2 Influx of new investments across heavy duty industrial applications

- 3.2.1.3 Encouraging regulatory framework by respective authorities to curb carbon emissions

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Significant initial deployment cost

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of industrial heat pumps

- 3.8 Emerging opportunities & trends

- 3.8.1 Digital transformation with IoT technologies

- 3.8.2 Emerging market penetration

- 3.9 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans and funding

Chapter 5 Market Size and Forecast, By Product, 2022 - 2035, (USD Million, Units)

- 5.1 Key trends

- 5.2 Air source

- 5.3 Ground source

- 5.4 Water source

- 5.5 Closed cycle mechanical heat pump

- 5.6 Open cycle mechanical vapor compression heat pump

- 5.7 Open cycle mechanical thermocompression heat pump

- 5.8 Closed cycle absorption heat pump

Chapter 6 Market Size and Forecast, By Capacity, 2022 - 2035, (USD Million, Units)

- 6.1 Key trends

- 6.2 Up to 500 kW

- 6.3 > 500 kW to 2 MW

- 6.4 2 MW - 5 MW

- 6.5 > 5 MW

Chapter 7 Market Size and Forecast, By Temperature, 2022 - 2035, (USD Million, Units)

- 7.1 Key trends

- 7.2 80 - 100 °C

- 7.3 100 - 150 °C

- 7.4 150 - 200 °C

- 7.5 > 200 °C

Chapter 8 Market Size and Forecast, By Application, 2022 - 2035, (USD Million, Units)

- 8.1 Key trends

- 8.2 Industrial

- 8.2.1 Paper

- 8.2.2 Food & beverages

- 8.2.3 Chemical

- 8.2.4 Iron & Steel

- 8.2.5 Machinery

- 8.2.6 Non-Metallic minerals

- 8.2.7 Other industries

- 8.3 District heating

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035, (USD Million, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Norway

- 9.3.3 Denmark

- 9.3.4 Finland

- 9.3.5 Sweden

- 9.3.6 Germany

- 9.3.7 Poland

- 9.3.8 Spain

- 9.3.9 Austria

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 Australia

- 9.4.4 South Korea

- 9.5 Middle East and Africa

- 9.5.1 Saudi Arabia

- 9.5.2 Turkey

- 9.5.3 South Africa

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Mexico

Chapter 10 Company Profiles

- 10.1 AGO Energie + Anlagen

- 10.2 Armstrong International

- 10.3 Atlas Copco

- 10.4 Baker Hughes

- 10.5 Carrier

- 10.6 Daikin Applied Europe

- 10.7 Dalrada Technology Group

- 10.8 Ecop

- 10.9 Enerin

- 10.10 Everllence

- 10.11 GEA Group

- 10.12 Hien New Energy Equipment

- 10.13 Johnson Controls

- 10.14 Mitsubishi Electric

- 10.15 Ochsner

- 10.16 Oilon Group

- 10.17 Siemens Energy

- 10.18 Thermax

- 10.19 Trane Technologies

- 10.20 Turboden