|

시장보고서

상품코드

2038683

배양육 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Cultured Meat Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

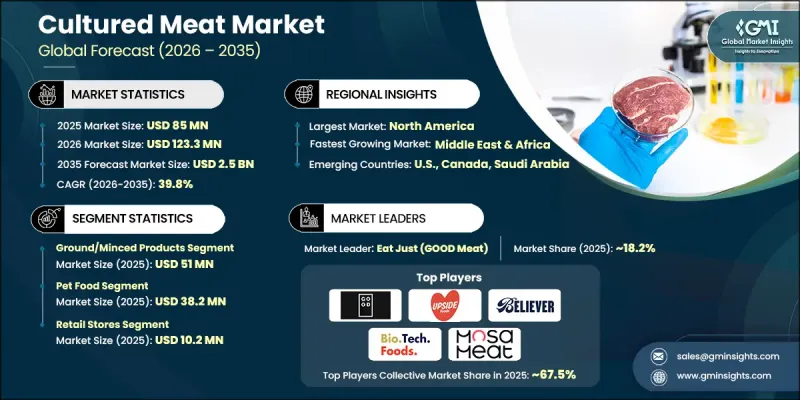

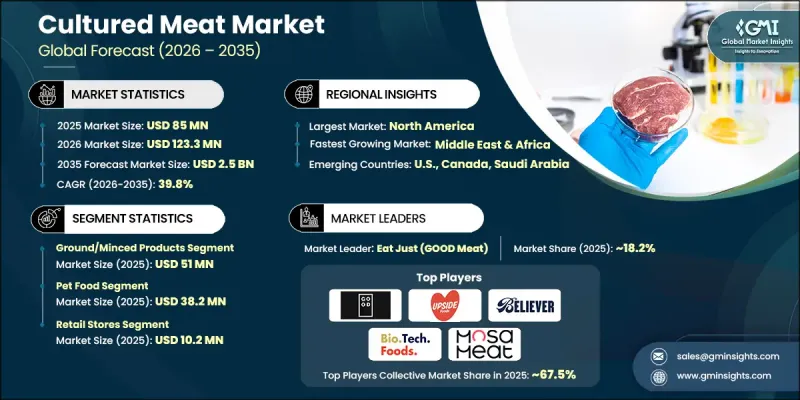

세계의 배양육 시장은 2025년에 8,500만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 39.8%로 성장할 전망이며, 25억 달러에 이를 것으로 추정되고 있습니다.

주요 경제권의 규제 당국이 소비자 대상 제품 출시를 순차적으로 승인함에 따라, 업계는 파일럿 규모의 개발 단계에서 초기 단계의 상업화 단계로 전환하고 있습니다. FDA와 USDA 등 당국의 가금류 유래 배양 제품의 조기 승인은 제품 안전 기준에 대한 신뢰를 높이고, 투자자의 진입을 촉진하며, 산업 전반의 생산 능력 확대를 지원하고 있습니다. 동시에 LCA(Life Cycle Assessment) 결과에서 배양육이 기존 축산업에 비해 온실가스 배출량, 토지 사용량, 물 소비량을 크게 줄일 수 있다는 결과가 일관되게 나타나면서 환경적 압박도 채택을 가속화하고 있습니다. 이러한 측정 가능한 지속가능성의 이점은 세계 단백질 시장에서 배양육의 장기적인 입지를 강화하고 있습니다. 기술의 발전은 또한 비용 구조를 변화시키고 있으며, 무혈청 배지의 개발, 세포주 개발의 개선 및 고처리량 바이오리액터의 발전으로 Kg당 생산비용이 꾸준히 감소하여 기존 육류에 대한 경쟁력이 향상되고 있습니다. 또한, 윤리적이고 투명하며 안전한 단백질 대체품에 대한 소비자의 관심이 높아지면서 소매 및 외식 산업 채널 모두에서 수요의 모멘텀이 더욱 강화되고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 8,500만 달러 |

| 예측 시장 규모 | 25억 달러 |

| CAGR | 39.8% |

2025년 기준, 다진 고기 및 다진 육류 제품 카테고리는 5,100만 달러를 차지했습니다. 이 부문은 성형육에 비해 제조 공정이 비교적 간단하고 생산 규모 확대가 용이하여 시장을 선도하고 있습니다. 조직 구조로 성형이 용이하기 때문에 생산자는 식감과 관능적 품질을 유지하면서 더 작은 규모의 바이오리액터에서 효율적으로 운영할 수 있습니다. 또한 햄버거, 미트볼, 만두, 너겟 등 널리 소비되는 형태에 적합하다는 점도 소비자들의 폭넓은 수용을 뒷받침하고 있습니다. 이러한 특성으로 인해 제조업체는 초기 단계의 가격 수준에 대응할 수 있는 대량 수요 부문을 타겟으로 예측 가능한 소비 패턴을 확보할 수 있습니다.

반려동물 사료 부문은 2025년 3,820만 달러에 달했습니다. 기업이 초기에 인체용 식품에 적용하고 주류 소비 채널을 우선시하기 때문에 이 카테고리는 배양육 시장에서 중요한 위치를 차지하고 있습니다. 초기 규제 당국의 승인, 파일럿 시식 및 제한적인 소매 도입은 주로 인간의 소비에 초점을 맞추어 안전성, 맛, 질감 일관성을 대규모로 검증하는 데 중점을 두었습니다. 이러한 초점은 광범위한 지속가능성 트렌드와 윤리적 단백질 대체품에 대한 소비자 수요 증가와 맞물려 배양육이 기존의 동물성 단백질 제품을 대체할 수 있는 실용적인 대안으로 자리 잡을 수 있도록 돕고 있습니다.

북미의 배양육 시장은 2025년 2,720만 달러 규모에 달했습니다. 이는 세포농업 스타트업의 강력한 생태계, 막대한 벤처캐피털의 유입, 그리고 FDA와 USDA와 같은 기관의 초기 규제 개입에 힘입은 바 큽니다. 이 지역의 성장은 대규모 시설 투자와 외식업계의 지속적인 시범사업이 주도하고 있으며, 이는 소비자 수용성을 검증하고 상업화를 위한 길을 열어주는 역할을 하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 형태별(2022-2035년)

제7장 시장 추산 및 예측 : 소스별(2022-2035년)

제8장 시장 추산 및 예측 : 유통 채널별(2022-2035년)

제9장 시장 추산 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

AJY 26.06.11The Global Cultured Meat Market was valued at USD 85 million in 2025 and is estimated to grow at a CAGR of 39.8% to reach USD 2.5 billion by 2035.

The industry is transitioning from pilot-scale development toward early-stage commercialization as regulatory agencies in major economies begin granting approvals for consumer-facing product launches. Early approvals for poultry-derived cultivated products by authorities such as the FDA and USDA have strengthened confidence in product safety standards, encouraging greater investor participation and supporting capacity expansion across the sector. At the same time, environmental pressures are accelerating adoption, as lifecycle assessments consistently show that cultured meat can significantly reduce greenhouse gas emissions, land usage, and water consumption compared to conventional livestock production. These measurable sustainability benefits are reinforcing its long-term positioning within global protein markets. Technological progress is also reshaping cost structures, with advancements in serum-free media, improved cell line development, and high-throughput bioreactors steadily lowering production costs per kilogram and improving competitiveness against conventional meat. In addition, rising consumer interest in ethical, transparent, and safer protein alternatives is further strengthening demand momentum across both retail and foodservice channels.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $85 Million |

| Forecast Value | $2.5 Billion |

| CAGR | 39.8% |

The ground and minced product category accounted for USD 51 million in 2025. This segment leads due to its lower production complexity and faster scalability compared to structured meat cuts. It is easier to form into tissue structures, allowing producers to operate efficiently with smaller bioreactor capacities while maintaining texture and sensory quality. Its suitability for widely consumed formats such as burgers, meatballs, dumplings, and nuggets also supports broader consumer acceptance. These attributes enable manufacturers to target high-volume demand segments that can accommodate early-stage pricing levels while ensuring predictable consumption patterns.

The pet food segment reached USD 38.2 million in 2025. This category holds a meaningful position in the cultured meat market as companies initially prioritize human food applications and mainstream consumption channels. Early regulatory approvals, pilot tastings, and limited retail introductions have largely focused on human consumption to validate safety, flavor, and texture consistency at scale. This focus aligns with broader sustainability narratives and increasing consumer demand for ethical protein alternatives, supporting the establishment of cultured meat as a viable substitute for conventional animal-derived protein products.

North America Cultured Meat Market generated USD 27.2 million in 2025, supported by a strong ecosystem of cellular agriculture startups, substantial venture capital inflows, and early regulatory engagement from agencies such as the FDA and USDA. Regional growth is further driven by large-scale facility investments and ongoing pilot initiatives in foodservice environments, which are helping validate consumer acceptance and support the commercialization pathway.

Key players operating in the Global Cultured Meat Industry include Aleph Farms, Believer Meats (formerly Future Meat Technologies), Avant Meats, Mosa Meat, Upside Foods, Finless Foods, Meatable, Eat Just (GOOD Meat), HigherSteaks, BioFood Systems, Balletic Foods, Biotech Foods, and BlueNalu. Companies in the cultured meat market are focusing on strategic partnerships with food manufacturers, biotechnology firms, and research institutions to accelerate commercialization and scale production capabilities. They are investing heavily in bioprocess optimization, cost reduction technologies, and serum-free culture media innovations to improve efficiency. Many players are expanding pilot production facilities to validate large-scale manufacturing processes while ensuring regulatory compliance. Strong emphasis is placed on securing early regulatory approvals across multiple regions to facilitate market entry. Firms are also prioritizing consumer education and branding strategies to build trust around safety and sustainability. Additionally, targeted collaborations with foodservice operators and retail chains are helping strengthen distribution networks and enhance market visibility, while continuous R&D investments are improving texture, flavor, and product consistency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Form

- 2.2.4 Source

- 2.2.5 Distribution Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising shift toward plant-based and flexitarian diets

- 3.2.1.2 Increasing demand for functional and protein-rich beverages

- 3.2.1.3 Convenience-driven consumption patterns

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High product cost and price sensitivity

- 3.2.2.2 Intense competition and brand differentiation pressure

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion through emerging markets and affordability strategies

- 3.2.3.2 Innovation in functional blends and personalized nutrition

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Protein Drink Mixes

- 5.3 Meal Replacement Mixes

- 5.4 Energy and Sports Drink Mixes

- 5.5 Functional Drink Mixes

Chapter 6 Market Estimates and Forecast, By Form, 2022 - 2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Powder

- 6.3 Liquid

Chapter 7 Market Estimates and Forecast, By Source, 2022 - 2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Soy-Based

- 7.3 Almond-Based

- 7.4 Pea-Based

- 7.5 Rice-Based

- 7.6 Hemp-Based

- 7.7 Mixed-Source

- 7.8 Coconut Based

- 7.9 Fruit based

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Online retail

- 8.3 Offline

- 8.3.1 Hypermarkets and Supermarkets

- 8.3.2 Convenience Stores

- 8.3.3 Specialty Stores

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 True Nutrition

- 10.2 Plant fusion

- 10.3 Glanbia Nutritionals

- 10.4 Vegan Drink Company

- 10.5 Garden of life

- 10.6 Vega

- 10.7 Sunwarrior

- 10.8 Nuzest

- 10.9 Orgain

- 10.10 Strive