|

시장보고서

상품코드

2038760

물류 로봇 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Logistics Robots Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

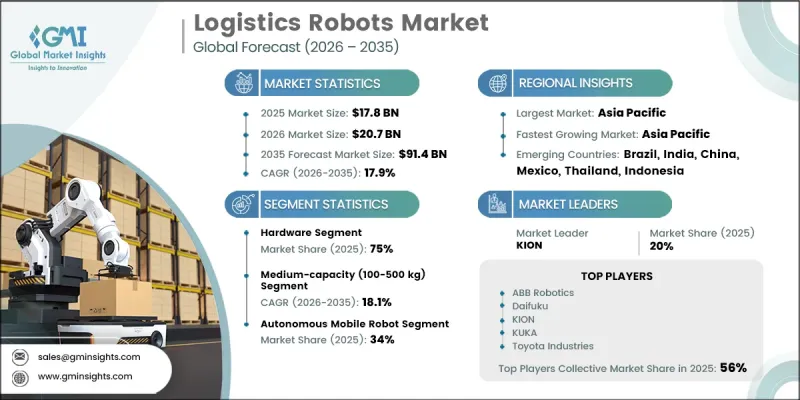

세계의 물류 로봇 시장은 2025년에 178억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 17.9%로 성장할 전망이며, 914억 달러에 이를 것으로 예측됩니다.

이 분야는 자동화에 대한 수요 증가, 납기 단축에 대한 압박, 그리고 공급망의 고도의 디지털화에 의해 빠르게 진화하고 있습니다. 이 산업은 지리적 집적, 전략적 공급업체와의 관계, 강력한 수직적 통합을 특징으로 하는 복잡한 생태계로 정의됩니다. 로봇 기술이 성숙해짐에 따라 물류 기업들은 높아지는 소비자의 기대에 부응하고 업무의 비효율성을 줄이기 위해 자율 시스템으로 전환을 가속화하고 있습니다. 투자회수기간(ROI) 단축과 회수기간 단축으로 창고 및 물류센터 전체에 지능형 로봇 시스템 도입이 확대되고 있습니다. 이러한 자동화의 물결은 처리 능력 향상, 정확도 향상, 인력 의존도 감소를 통해 물류 인프라를 재구성하고 있으며, 궁극적으로 선진국과 신흥 시장 전반의 성장을 가속하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 178억 달러 |

| 예측 시장 규모 | 914억 달러 |

| CAGR | 17.9% |

2025년 기준, 하드웨어 부문은 75%의 점유율을 차지했습니다. 로봇 플랫폼, 기계 부품 및 모빌리티 시스템은 물류 로봇 솔루션의 기본 계층을 형성하여 창고 및 라스트 마일 환경에서 원활한 운영을 가능하게 합니다. 로봇 동력 시스템에 대한 기술 발전과 연구 이니셔티브로 인해 하드웨어 비용 구조가 변화하고 있지만, 물류 작업에서 사람의 개입은 여전히 총 비용의 대부분을 차지하고 있습니다.

자율 이동 로봇(AMR) 부문은 2025년 34%의 점유율을 차지했습니다. AMR은 인공지능, 시각적 SLAM, 적응형 센서 기술을 활용한 첨단 내비게이션 시스템을 통해 기존 무인운반차(AGV)에 비해 효율성이 크게 향상되었습니다. 이러한 기능을 통해 복잡하고 역동적인 환경에서 실시간 의사결정을 내릴 수 있으며, 이 부문은 시험 운영 단계에서 대규모 상업적 배포로 전환하고 있습니다.

중국의 물류 로봇 시장은 2026-2035년 연평균 복합 성장률(CAGR) 18.6%를 나타낼 것으로 예측되며, 견조한 성장 전망을 보여주고 있습니다. 광범위한 제조거점과 정부의 적극적인 자동화 추진 노력에 힘입어, 이 나라는 지역 시장에서 지배적인 지위를 유지하고 있습니다. 이러한 선도적 위치는 창고, 풀필먼트, 물류 프로세스 전반에 걸쳐 로봇 시스템을 광범위하게 도입하여 효율성을 높이고 인력에 대한 의존도를 낮춤으로써 강화되고 있습니다. 중국 시장의 강점은 생산과 소비의 세계 주요 허브로서의 역할을 반영하고 있으며, 로봇공학과 인공지능을 도입한 고도로 발달된 자동화된 창고 시설, 스마트 물류센터, 그리고 첨단 배송 인프라 네트워크에 의해 뒷받침되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 컴포넌트별(2022-2035년)

제6장 시장 추산 및 예측 : 유형별(2022-2035년)

제7장 시장 추산 및 예측 : 용도별(2022-2035년)

제8장 시장 추산 및 예측 : 적재 용량별(2022-2035년)

제9장 시장 추산 및 예측 : 최종 용도별(2022-2035년)

제10장 시장 추산 및 예측 : 지역별(2022-2035년)

제11장 기업 개요

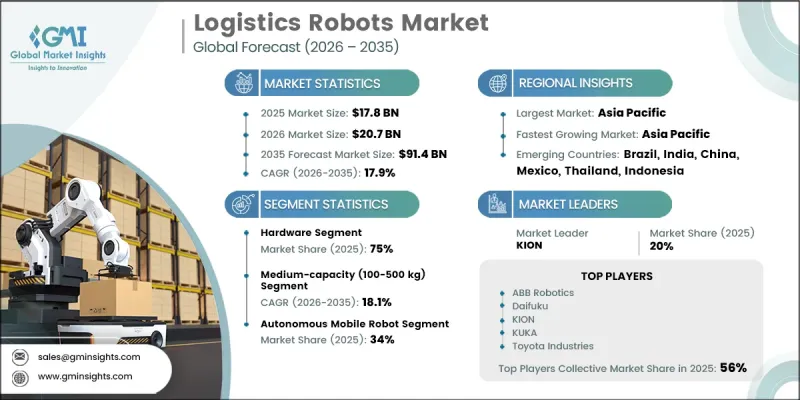

AJY 26.06.11The Global Logistics Robots Market was valued at USD 17.8 billion in 2025 and is estimated to grow at a CAGR of 17.9% to reach USD 91.4 billion by 2035.

This sector is evolving rapidly, shaped by growing demand for automation, tighter delivery timelines, and advanced supply chain digitization. The industry is defined by its intricate ecosystem, which is marked by geographic clustering, strategic supplier relationships, and strong vertical integration. As robotics technologies mature, logistics firms are increasingly transitioning toward autonomous systems to meet rising consumer expectations and reduce operational inefficiencies. Accelerated ROI and shrinking payback windows are prompting broader deployment of intelligent robotics systems across warehouse and distribution centers. This wave of automation is reshaping logistics infrastructure by enabling higher throughput, improved accuracy, and leaner workforce dependencies, ultimately fueling growth across developed and emerging markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $17.8 Billion |

| Forecast Value | $91.4 Billion |

| CAGR | 17.9% |

The hardware segment held a 75% share in 2025. Robotic platforms, mechanical components, and mobility systems form the foundational layer of logistics robotics solutions, enabling seamless operation in warehouse and last-mile environments. Technological advancements and research initiatives into robotics power systems are reshaping the hardware cost structures, although human involvement in logistics operations still accounts for a large portion of total expenses.

The autonomous mobile robots (AMRs) segment held a 34% share in 2025. AMRs offer significant efficiency gains over traditional automated guided vehicles due to advanced navigation systems powered by artificial intelligence, visual SLAM, and adaptive sensor technology. These capabilities allow for real-time decision-making in complex, dynamic environments, moving the segment from pilot phases into large-scale commercial deployments.

China Logistics Robots Market is expected to register a CAGR of 18.6% between 2026 and 2035, highlighting its strong growth outlook. Backed by an extensive manufacturing base and proactive government initiatives promoting automation, the country maintains a dominant position in the regional landscape. This leadership is reinforced by widespread adoption of robotic systems across warehousing, fulfillment operations, and logistics processes, enabling higher efficiency and reduced reliance on manual labor. China's market strength reflects its role as a major global hub for production and consumption, supported by a well-developed network of automated storage facilities, intelligent distribution centers, and advanced delivery frameworks that incorporate robotics and artificial intelligence.

Key industry players shaping the competitive landscape of the Global Logistics Robots Market include ABB, Yaskawa Electric, Toyota/Bastian, Omron, Daifuku, Amazon Robotics, KUKA/Swisslog, KION/Dematic, Honeywell, and AutoStore. To reinforce their position, logistics robotics companies are prioritizing AI-powered automation, real-time data analytics, and modular system designs tailored to various logistics use cases. Strategic mergers and partnerships enable technology sharing and geographic expansion, while R&D investments are yielding scalable platforms for multi-application functionality. Leading firms are also customizing robotic fleets to suit e-commerce, third-party logistics, and retail warehouse environments, ensuring long-term client retention and improved operational ROI. Global players are further strengthening their presence through localized production, expanded service networks, and integrated digital platforms that enable seamless logistics orchestration and predictive maintenance.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Type

- 2.2.4 Application

- 2.2.5 Payload Capacity

- 2.2.6 End use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Exponential growth in e-commerce & omnichannel fulfillment demands

- 3.2.1.2 Severe labor shortages & rising warehousing labor costs

- 3.2.1.3 Advancements in AI, computer vision & autonomous navigation technologies

- 3.2.1.4 Adoption of robotics-as-a-service (RaaS) business models

- 3.2.1.5 Push for operational efficiency & supply chain resilience

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial capital expenditure & ROI uncertainties

- 3.2.2.2 Integration complexity with legacy warehouse management systems

- 3.2.2.3 Lack of interoperability between different robotic vendor systems

- 3.2.2.4 Facility infrastructure constraints (floor quality, wireless connectivity, power)

- 3.2.3 Market opportunities

- 3.2.3.1 Untapped SME warehouse automation market

- 3.2.3.2 Expansion into cold chain & temperature-controlled logistics

- 3.2.3.3 Last-mile delivery automation using drones & autonomous vehicles

- 3.2.3.4 Retrofitting brownfield warehouses with modular robotic solutions

- 3.2.3.5 AI-driven predictive maintenance & fleet optimization services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pricing Analysis (Driven by Primary Research)

- 3.4.1 Historical Price Trend Analysis

- 3.4.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 US- Robotics safety, automation & workplace regulations

- 3.5.1.2 Canada - Automation safety & AI governance framework

- 3.5.2 Europe

- 3.5.2.1 Germany- EU Machinery Regulation & Industry 4.0 compliance

- 3.5.2.2 UK- Post-Brexit automation & AI regulations

- 3.5.2.3 France- AI regulation & sustainability mandates

- 3.5.2.4 Italy- Industrial automation & workplace safety compliance

- 3.5.3 Asia Pacific

- 3.5.3.1 China- Robotics standards & smart logistics policies

- 3.5.3.2 India- Industrial automation & digital logistics policies

- 3.5.3.3 Japan- Robotics leadership & safety regulations

- 3.5.3.4 Australia- Workplace safety & automation governance

- 3.5.4 LATAM

- 3.5.4.1 Mexico- Industrial automation standards & compliance

- 3.5.4.2 Argentina- National industrial safety & automation policies

- 3.5.5 MEA

- 3.5.5.1 South Africa- Industrial safety & automation regulations

- 3.5.6 Saudi Arabia- Vision 2030 & smart logistics regulations

- 3.5.1 North America

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Patent Landscape (Driven by Primary Research)

- 3.9 Trade Data Analysis (Based on Paid Database)

- 3.9.1 Import/Export Volume & Value Trends

- 3.9.2 Key Trade Corridors & Tariff Impact

- 3.10 Impact of AI & Generative AI on the Market (Driven by Primary Research)

- 3.10.1 AI-Driven Disruption of Existing Business Models

- 3.10.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.10.3 Risks, Limitations & Regulatory Considerations

- 3.11 Capacity & Production Landscape (Driven by Primary Research)

- 3.11.1 Production Capacity by Region & Key Producer

- 3.11.2 Capacity Utilization Rates & Expansion Pipelines

- 3.12 Technology and innovation landscape

- 3.12.1 Current technological trends

- 3.12.2 Emerging technologies

- 3.13 Use cases & success stories

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

- 3.15 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.15.1 Base Case - key macro & industry variables driving CAGR

- 3.15.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Company Tier Benchmarking

- 4.5.1 Tier Classification Criteria & Qualifying Thresholds

- 4.5.2 Tier Positioning Matrix by Revenue, Geography & Innovation

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Robotic platforms & chassis

- 5.2.2 Sensors & perception systems

- 5.2.3 Actuators & manipulation systems

- 5.2.4 Others

- 5.3 Software

- 5.3.1 Robot operating systems

- 5.3.2 Fleet management software

- 5.3.3 Warehouse management integration

- 5.3.4 Others

- 5.4 Services

- 5.4.1 Professional

- 5.4.2 Managed

Chapter 6 Market Estimates & Forecast, By Type, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Automated guided vehicles

- 6.3 Autonomous mobile robots

- 6.4 Robot arms

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Palletizing & de-palletizing

- 7.3 Pick & place

- 7.4 Transportation

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Payload Capacity, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Low capacity (Up to 100 kg)

- 8.3 Medium capacity (100-500 kg)

- 8.4 High capacity (Above 500 kg)

Chapter 9 Market Estimates & Forecast, By End use, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 E-commerce

- 9.3 Healthcare

- 9.4 Retail

- 9.5 Food & beverages

- 9.6 Automotive

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.3.9 Denmark

- 10.3.10 Poland

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Israel

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 ABB

- 11.1.2 Amazon Robotics

- 11.1.3 AutoStore

- 11.1.4 Daifuku

- 11.1.5 Honeywell

- 11.1.6 KION/Dematic

- 11.1.7 KUKA/Swisslog

- 11.1.8 Omron

- 11.1.9 Toyota/Bastian

- 11.1.10 Yaskawa Electric

- 11.2 Regional Players

- 11.2.1 Bastian Solutions

- 11.2.2 Geek+

- 11.2.3 GreyOrange

- 11.2.4 Locus Robotics

- 11.2.5 Vecna Robotics

- 11.3 Emerging Players

- 11.3.1 Berkshire Grey

- 11.3.2 Covariant

- 11.3.3 Exotec

- 11.3.4 River Systems

- 11.3.5 VisionNav Robotics