|

시장보고서

상품코드

2038803

폼 플라스틱 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Foam Plastics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

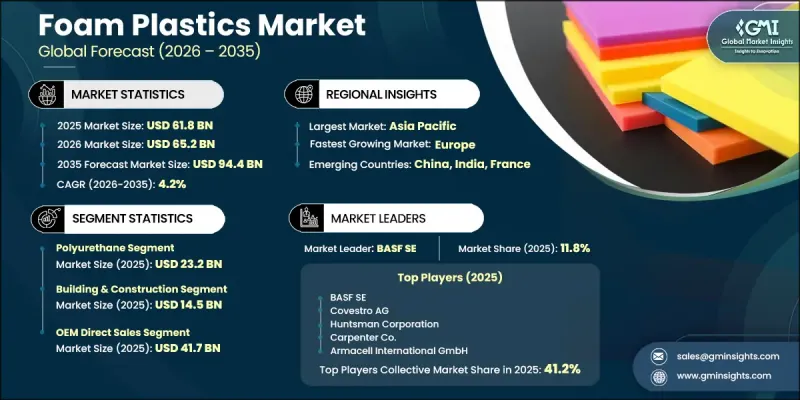

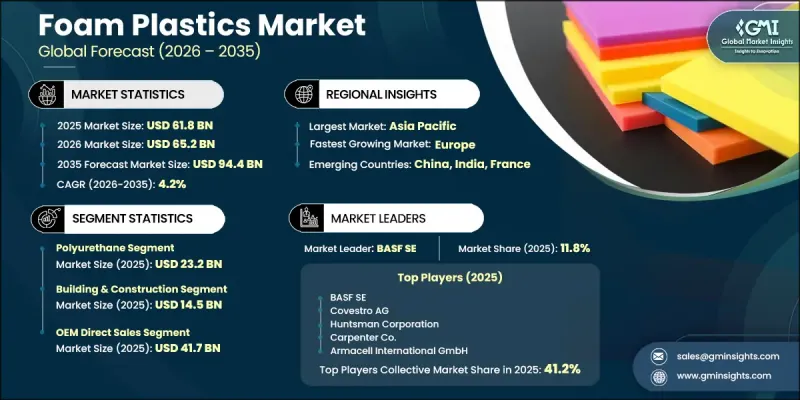

세계의 폼 플라스틱 시장은 2025년에 618억 달러로 평가되었고 CAGR 4.2%로 성장하여 2035년까지 944억 달러에 이를 것으로 추정되고 있습니다.

폼 플라스틱은 우수한 단열 성능과 다용도 기계적 특성을 가진 셀 구조의 경량 고분자 소재입니다. 이러한 재료는 화학적 또는 기계적 발포 기술을 사용하여 용융 수지에 가스를 도입하여 제조되며, 최종 용도의 필요에 따라 개방형 또는 폐쇄형 셀 구조로 만들어집니다. 내열성, 완충성, 부력, 에너지 흡수성을 겸비한 독특한 특성으로 건설, 포장, 자동차, 가구, 신발, 스포츠 산업에서 없어서는 안 될 소재가 되었습니다. 또한, 습기, 화학물질, 환경에 의한 마모에 대한 내성이 뛰어나 주거, 상업, 산업 환경의 실내 및 실외 모두에서 활용되고 있습니다. 압출 발포, 사출 성형, 비드 발포 등 제조 기술의 발전으로 밀도 및 셀 구조의 제어 정밀도가 향상되었습니다. 또한, 나노기술의 통합과 바이오 폴리머에 대한 새로운 혁신은 성능을 향상시키는 동시에 지속가능성 목표를 지원하고 있습니다. 에너지 절약형 건축 및 경량 자동차 부품에 대한 수요 증가로 인해 예측 기간 동안 세계 시장에서의 채택이 계속 가속화되어 시장 규모가 크게 확대될 것으로 예측됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 618억 달러 |

| 예측 시장 규모 | 944억 달러 |

| CAGR | 4.2% |

폴리우레탄 부문은 2025년 232억 달러에 달했습니다. 다양한 산업 분야의 연질 및 경질 폼 응용 분야에서 폭넓게 사용되면서 탄탄한 시장 지위를 확보하고 있습니다. 유연성 폴리우레탄 폼은 편안함, 탄력성, 내구성으로 인해 매트리스, 시트, 쿠션 제품에 널리 사용되고 있습니다. 한편, 경질 폴리우레탄 폼은 내열성이 우수하여 냉동 시스템, 건축 외피, 냉장 창고 인프라의 단열재로 널리 사용되고 있습니다. 이 부문은 물 발포 및 이산화탄소 발포와 같은 친환경 발포 기술의 지속적인 발전의 혜택을 누리고 있습니다. 이러한 기술은 까다로운 산업 및 상업용 용도에서 요구되는 고성능 특성을 유지하면서 환경에 미치는 영향을 줄이는 데 도움이 됩니다.

건축 및 건설 응용 분야는 세계 인프라 개발에서 고성능 단열재에 대한 수요가 증가함에 따라 2025년 145억 달러에 달했습니다. 폼 기반 단열 제품은 벽체 캐비티, 지붕 시스템, 기초 구조에 널리 사용되며, 높은 내열성과인치당 R값이 우수하여 기존 대체품에 비해 에너지 효율이 높으며, 기존 제품에 비해 에너지 효율이 높습니다. 또한, 이들 자재는 외벽 및 슬래브 하부까지 연속적인 단열 시스템 구축이 가능하여 열교 저감 및 건물 전체 효율 향상에 기여하고 있습니다. 에너지 규제와 그린빌딩 기준이 강화되는 가운데, 개발업체와 건설업체들이 에너지 절약, 거주자의 쾌적성, 장기적인 구조적 성능을 향상시키는 자재를 우선시하게 되면서 그 채택이 더욱 가속화되고 있습니다.

북미 폼 플라스틱 시장은 주거, 상업 및 인프라 개조 프로젝트에서 건설 활동의 강력한 확장에 힘입어 2025년 201억 달러에서 2035년까지 312억 달러로 성장할 것으로 예측됩니다. 미국과 캐나다 전역에 걸쳐 에너지 효율에 초점을 맞춘 규제 프레임워크가 구축되어 신축 및 개보수 공사 모두에서 첨단 단열재 사용을 장려하고 있습니다. 또한, 식품 및 제약 산업을 지원하는 이 지역의 잘 구축된 콜드체인 물류 네트워크도 수요를 촉진하고 있습니다. 이 분야에서는 냉장 창고, 운송 차량, 운송 컨테이너에서 발포 단열재가 필수적입니다. 이러한 요인들이 복합적으로 작용하여 고성능 폼 플라스틱 솔루션에 대한 지속적인 시장 성장과 안정적인 수요를 창출하고 있습니다.

코베스트로 AG, BASF SE, 듀폰, 오웬스 코닝, 쉴드 에어 코퍼레이션, 알마셀 인터내셔널 GmbH, 카펜터, 헌츠먼 코퍼레이션, 로저스 코퍼레이션, 도레이 플라스틱(미국), 토로셀렌, 조테폼스 plc, 세키스이화학공업(주), JSP 코퍼레이션, 제너럴 플라스틱 제조 GmbH, Zote Forms plc, Sekisui Chemical Industry Corporation, JSP Corporation 및 General Plastic Manufacturing社는 폼 플라스틱 산업을 선도하는 주요 기업들입니다. 폼 플라스틱 시장에서 활동하는 기업들은 혁신, 지속가능성에 대한 노력, 전략적 사업 확장을 결합하여 시장에서의 입지를 강화하고 있습니다. 각 업체들은 열효율과 내구성 향상, 환경 부하 감소를 실현한 첨단 소재를 도입하기 위해 연구개발에 많은 투자를 하고 있습니다. 많은 기업들이 세계 지속가능성 목표에 부합하기 위해 바이오 폴리머, 친환경 발포제, 재활용 기술을 채택하고 있습니다. 또한 기업들은 생산능력 확대, 전략적 파트너십 구축, 신흥 지역 시장 진출을 통해 유통망과 고객 기반을 강화하기 위해 노력하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 유형별, 2022-2035년

제6장 시장 추산 및 예측 : 용도별, 2022-2035년

제7장 시장 추산 및 예측 : 판매채널별, 2022-2035년

제8장 시장 추산 및 예측 : 지역별, 2022-2035년

제9장 기업 개요

JHS 26.06.11The Global Foam Plastics Market was valued at USD 61.8 billion in 2025 and is estimated to grow at a CAGR of 4.2% to reach USD 94.4 billion by 2035.

Foam plastics are lightweight polymer-based materials formed with a cellular structure that delivers strong insulation performance and versatile mechanical properties. These materials are produced by introducing gas into molten resin through chemical or mechanical foaming techniques, resulting in open-cell or closed-cell configurations tailored to end-use needs. Their unique combination of thermal resistance, cushioning ability, buoyancy, and energy absorption makes them essential across construction, packaging, automotive, furniture, footwear, and sports industries. They are also valued for resistance to moisture, chemicals, and environmental wear, enabling both indoor and outdoor applications across residential, commercial, and industrial environments. Advances in manufacturing technologies such as extrusion foaming, injection molding, and bead expansion have improved precision in density and cell structure control. Additionally, emerging innovations in nanotechnology integration and bio-based polymers are enhancing performance while supporting sustainability goals. Growing demand across energy-efficient construction and lightweight automotive components continues to accelerate adoption across global markets over the forecast period significantly expanding.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $61.8 Billion |

| Forecast Value | $94.4 Billion |

| CAGR | 4.2% |

The polyurethane segment reached USD 23.2 billion in 2025. Its strong market position is driven by widespread use in both flexible and rigid foam applications across multiple industries. Flexible polyurethane foams are extensively used in mattresses, seating, and cushioning products due to their comfort, resilience, and durability, while rigid polyurethane foams are widely adopted for insulation purposes in refrigeration systems, building envelopes, and cold storage infrastructure because of their superior thermal resistance. The segment benefits from ongoing advancements in environmentally friendly foaming technologies, including water-blown and carbon dioxide-blown processes, which help reduce ecological impact while preserving high-performance characteristics required in demanding industrial and commercial applications.

The building and construction applications segment reached USD 14.5 billion in 2025, owing to rising demand for high-performance insulation materials in global infrastructure development. Foam-based insulation products are widely used in wall cavities, roofing systems, and foundation structures, where their high thermal resistance and superior R-value per inch enable more efficient energy performance compared to conventional alternatives. These materials also support continuous insulation systems on exterior walls and under-slab installations, helping reduce thermal bridging and improve overall building efficiency. Increasingly stringent energy regulations and green building standards are further driving adoption as developers and contractors prioritize materials that enhance energy savings, occupant comfort, and long-term structural performance.

North American Foam Plastics Market is projected to grow from USD 20.1 billion in 2025 to USD 31.2 billion by 2035, supported by strong expansion in construction activity across residential, commercial, and infrastructure renovation projects. Regulatory frameworks focused on energy efficiency across the United States and Canada are encouraging the use of advanced insulation materials in both new builds and retrofit applications. Demand is also reinforced by the region's well-established cold chain logistics network serving food and pharmaceutical industries, where foam insulation is essential for refrigerated warehouses, transport vehicles, and shipping containers. These factors collectively contribute to sustained market growth and stable demand for high-performance foam plastic solutions.

Covestro AG, BASF SE, DuPont, Owens Corning, Sealed Air Corporation, Armacell International GmbH, Carpenter Co., Huntsman Corporation, Rogers Corporation, Toray Plastics (America), Inc., Trocellen GmbH, Zotefoams plc, Sekisui Chemical Co., Ltd., JSP Corporation, and General Plastics Mfg. Co. are among the leading participants in the foam plastics industry. Companies operating in the foam plastics market are strengthening their market position through a combination of innovation, sustainability initiatives, and strategic expansion efforts. They are heavily investing in research and development to introduce advanced materials with improved thermal efficiency, durability, and reduced environmental impact. Many players are adopting bio-based polymers, eco-friendly foaming agents, and recycling technologies to align with global sustainability goals. Companies are also expanding production capacities, forming strategic partnerships, and entering emerging regional markets to strengthen distribution networks and customer reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type

- 2.2.2 Application

- 2.2.3 Sales channel

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polyurethane

- 5.3 Polystyrene

- 5.4 Polyolefin

- 5.5 Phenolic

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Building & Construction

- 6.2.1 Roofing Insulation

- 6.2.2 Wall Insulation

- 6.2.3 Flooring Insulation

- 6.2.4 Pipe Insulation

- 6.2.5 Others

- 6.3 Packaging

- 6.3.1 Protective Packaging

- 6.3.2 Food Containers

- 6.3.3 Electronics Packaging

- 6.3.4 Others

- 6.4 Automotive

- 6.4.1 Seating & Cushions

- 6.4.2 Headliners & Interior Trim

- 6.4.3 Dashboards & Doors

- 6.4.4 Others

- 6.5 Furniture & Bedding

- 6.5.1 Upholstered Furniture

- 6.5.2 Mattresses & Toppers

- 6.5.3 Pillows

- 6.5.4 Others

- 6.6 Footwear

- 6.7 Sports & Recreational

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By Sales Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 OEM Direct Sales

- 7.3 Indirect Sales

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 BASF SE

- 9.2 Covestro AG

- 9.3 Huntsman Corporation

- 9.4 Carpenter Co.

- 9.5 Armacell International GmbH

- 9.6 Sealed Air Corporation

- 9.7 General Plastics Mfg. Co.

- 9.8 DuPont

- 9.9 Owens Corning

- 9.10 Rogers Corporation

- 9.11 Toray Plastics (America), Inc.

- 9.12 Trocellen GmbH

- 9.13 Zotefoams plc

- 9.14 Sekisui Chemical Co., Ltd.

- 9.15 JSP Corporation