|

시장보고서

상품코드

2045686

계면활성제 프리 유화 기술 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Surfactant-Free Emulsion Technology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

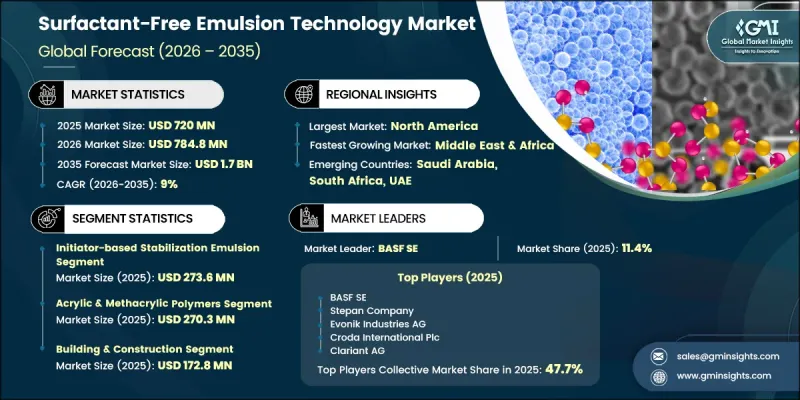

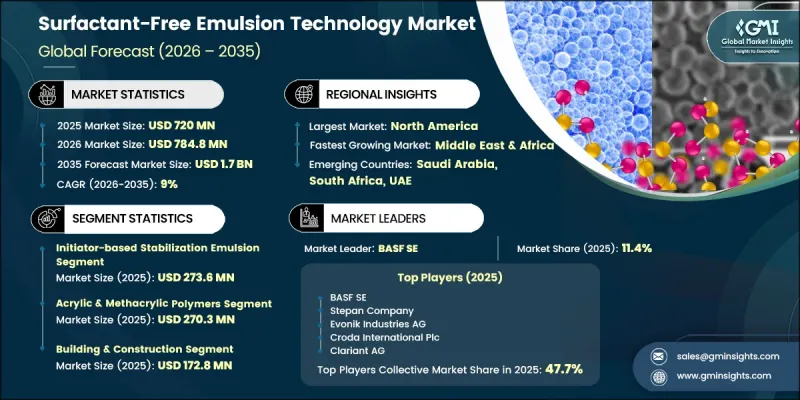

세계의 계면활성제 프리 유화 기술 시장은 2025년에 7억 2,000만 달러로 평가되었고 CAGR 9%로 성장하여 2035년까지 17억 달러에 이를 것으로 예측됩니다.

계면활성제 프리 유화 기술이란 기존의 계면활성제를 사용하지 않고 개발된 고분자 분산 시스템을 말합니다. 이들 제제에서는 이온성 개시제 잔류물, 고분자 사슬에 의한 입체 안정화, 미세 고체 입자의 안정화 등 대체 메커니즘을 통해 입자의 안정화를 도모하고 있습니다. 이 기술은 순도 향상, 계면 성능 강화 및 우수한 장기적 재료 안정성을 실현할 수 있어 빠르게 주목받고 있습니다. 더 깨끗한 배합과 오염 위험 감소에 대한 수요 증가는 여러 산업 분야에서 산업계 수요를 지속적으로 뒷받침하고 있습니다. 또한, 제조업체들은 배합의 내구성을 향상시키고, 제품의 일관성을 유지하며, 잔류성이 높은 화학 첨가물에 따른 환경 영향을 최소화하기 위해 이러한 시스템을 점점 더 많이 채택하고 있습니다. 또한, 이 기술은 다양한 기계적, 열적, 화학적 조건에서도 신뢰할 수 있는 성능을 발휘하여 고성능 소재 응용 분야에서 상업적 채택을 더욱 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 7억 2,000만 달러 |

| 예측 시장 규모 | 17억 달러 |

| CAGR | 9% |

계면활성제 프리 유화 기술 시장은 첨단 재료 성능, 제품 신뢰성 향상 및 배합 효율을 중시하는 업계 수요가 증가하고 있습니다. 페인트, 접착제, 의약품, 퍼스널케어, 특수 재료 등의 분야에서는 기계적 강도, 제품의 저장 안정성 및 표면 균일성을 향상시키기 위해 이러한 시스템을 적극적으로 도입하고 있습니다. 기존의 계면활성제를 사용하지 않음으로써 첨가제 이동 및 호환성 제한과 관련된 문제를 줄일 수 있기 때문에 이러한 에멀젼은 정밀도가 요구되는 응용 분야에 매우 적합합니다. 환경 규제 강화와 지속가능성에 대한 노력도 계면활성제 프리 배합으로의 전환을 가속화하고 있습니다. 각 업체들은 제품의 품질과 운영 효율을 유지하면서 수계로의 화학물질 배출을 줄이는 기술에 집중하고 있습니다. 중합 공정의 지속적인 발전으로 산업 규모 생산에서 입자 제어, 분산 일관성 및 배합 적응성이 더욱 향상되었습니다.

개시제 기반 안정화 부문은 기존 계면활성제 시스템에 의존하지 않고 안정적인 분산액을 제공할 수 있는 능력으로 인해 2025년 2억 7,360만 달러에 달할 것으로 예측됩니다. 동시에 제조업체들이 분자 구조, 입자 분포 및 배합 안정성에 대한 더 높은 수준의 제어를 추구함에 따라 RAFT/MADIX를 통한 에멀젼이 업계에서 큰 주목을 받고 있습니다. 이러한 진보된 접근 방식은 기능성 폴리머 및 특수 소재와의 호환성이 개선된 매우 균일한 분산액 제조를 지원합니다. 이러한 기술에 대한 수요는 특히 장기적인 안정성과 배합의 변동성을 감소시키는 고성능 코팅, 산업용 접착제 및 특수 폴리머 시스템을 필요로 하는 응용 분야에서 증가하고 있습니다. 또한, 현재 진행 중인 연구 활동은 상업적 제조 환경 전반의 프로세스 최적화 및 확장성 향상에 기여하고 있습니다.

건축 및 건설 분야는 2025년 1억 7,280만 달러 시장 규모를 창출했습니다. 이 분야 수요는 수명을 연장하고 구조적 신뢰성을 향상시키기 위한 고성능 코팅, 실란트 및 접착제 시스템의 사용 확대에 의해 뒷받침되고 있습니다. 각 제조업체들은 우수한 피막 형성성, 표면 결함에 대한 내성 및 변화하는 환경 조건에서 내구성을 향상시키는 배합에 중점을 두고 있습니다. 자동차 및 운송 산업에서도 장기적인 운영 주기 동안 성능의 일관성을 유지하는 코팅재 및 접착제에 대한 수요가 증가함에 따라 계면활성제 프리 에멀젼의 채택이 확대되고 있습니다. 이러한 산업에서는 표면 품질, 접착 성능 및 장기적인 기계적 무결성을 향상시킬 수 있는 첨단 재료 기술이 점점 더 우선시되고 있습니다.

북미 계면활성제 프리 유화 기술 시장은 2025년에 2억 2,820만 달러에 달하고, 2035년에는 5억 3,000만 달러에 달할 것으로 예측됩니다. 이 분야의 성장은 첨가제 전환이 적고 장기적인 내구성이 향상된 첨단 코팅, 특수 접착제 및 엔지니어링 소재에 대한 수요 증가에 힘입어 성장세를 보이고 있습니다. 북미 전역의 산업 제조업체들은 제품의 효율성과 성능의 일관성을 유지하면서 진화하는 환경 기준을 충족하기 위해 차세대 배합 기술에 투자하고 있습니다. 또한, 이 지역에서는 지속 가능한 제조 방식에 대한 관심 증가, 고분자 화학의 혁신, 까다로운 산업 응용 분야에 적합한 고순도 재료 시스템의 개발이 진행되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 기술별, 2022-2035년

제6장 시장 추산 및 예측 : 폴리머 유형별, 2022-2035년

제7장 시장 추산 및 예측 : 최종 사용자별, 2022-2035년

제8장 시장 추산 및 예측 : 지역별, 2022-2035년

제9장 기업 개요

JHS 26.06.11The Global Surfactant-Free Emulsion Technology Market was valued at USD 720 million in 2025 and is estimated to grow at a CAGR of 9% to reach USD 1.7 billion by 2035.

Surfactant-free emulsion technology refers to polymer dispersion systems developed without the use of traditional surface-active compounds. In these formulations, particle stabilization is achieved through alternative mechanisms, including ionic initiator residues, steric stabilization from polymer chains, and fine solid particle stabilization. The technology is gaining rapid attention due to its ability to deliver improved purity, enhanced interfacial performance, and superior long-term material stability. Growing preference for cleaner formulations and lower contamination risk continues to support industry demand across several industrial applications. In addition, manufacturers are increasingly adopting these systems to improve formulation durability, maintain product consistency, and minimize the environmental impact associated with persistent chemical additives. The technology also demonstrates reliable performance under varying mechanical, thermal, and chemical conditions, further strengthening its commercial adoption across high-performance material applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $720 Million |

| Forecast Value | $1.7 Billion |

| CAGR | 9% |

The surfactant-free emulsion technology market is experiencing increasing demand from industries focused on advanced material performance, enhanced product reliability, and formulation efficiency. Sectors including coatings, adhesives, pharmaceuticals, personal care, and specialty materials are actively integrating these systems to improve mechanical strength, product shelf stability, and surface uniformity. The absence of conventional surfactants helps reduce issues associated with additive migration and compatibility limitations, making these emulsions highly suitable for precision-driven applications. Rising environmental regulations and sustainability initiatives are also accelerating the transition toward surfactant-free formulations. Companies are concentrating on technologies that lower chemical discharge into water systems while preserving product quality and operational efficiency. Continuous advancements in polymerization processes are further improving particle control, dispersion consistency, and formulation adaptability for industrial-scale production.

The initiator-based stabilization segment reached USD 273.6 million in 2025 owing to its capability to provide stable dispersions without the dependency on traditional surfactant systems. At the same time, RAFT/MADIX-mediated emulsions are attracting significant industry attention as manufacturers pursue greater control over molecular architecture, particle distribution, and formulation stability. These advanced approaches support the production of highly uniform dispersions with improved compatibility for functional polymers and specialized materials. Demand for these technologies is particularly increasing in applications that require high-performance coatings, industrial adhesives, and specialty polymer systems with long-term stability and reduced formulation inconsistencies. Ongoing research activities are also contributing to process optimization and enhanced scalability across commercial manufacturing environments.

The building and construction segment generated USD 172.8 million in 2025. Demand within the sector is being supported by increasing use of high-performance coatings, sealants, and adhesive systems designed for long service life and improved structural reliability. Manufacturers are emphasizing formulations that deliver enhanced film formation, resistance to surface imperfections, and improved durability under changing environmental conditions. The automotive and transportation industries are also expanding the adoption of surfactant-free emulsions due to growing requirements for coatings and bonding materials that maintain performance consistency over extended operational cycles. These industries are increasingly prioritizing advanced material technologies capable of improving surface quality, adhesion performance, and long-term mechanical integrity.

North America Surfactant-Free Emulsion Technology Market reached USD 228.2 million in 2025 and is anticipated to reach USD 530 million by 2035. Growth across the region is being driven by increasing demand for advanced coatings, specialty adhesives, and engineered materials that offer lower additive migration and improved long-term durability. Industrial manufacturers throughout North America are investing in next-generation formulation technologies to meet evolving environmental standards while maintaining product efficiency and performance consistency. The region is also witnessing increased focus on sustainable manufacturing practices, innovation in polymer chemistry, and development of high-purity material systems suitable for demanding industrial applications.

Key participants operating in the Global Surfactant-Free Emulsion Technology Market include BASF, Dow, Arkema, Akzo Nobel, Covestro, JSR Corporation, Synthomer, ZEON Corporation, Allnex, Asahi Kasei, Celanese, and TCI (Tokyo Chemical Industry). Companies operating in the surfactant-free emulsion technology market are focusing on strategic initiatives aimed at strengthening product portfolios, expanding manufacturing capabilities, and enhancing technological expertise. Major industry participants are increasing investments in research and development to improve polymerization techniques, particle stabilization methods, and formulation performance. Many manufacturers are forming strategic partnerships and collaborative agreements to accelerate innovation and improve commercial scalability. Capacity expansion projects and regional distribution network enhancements are also being implemented to strengthen market reach and customer accessibility. In addition, companies are prioritizing sustainable product development to align with tightening environmental regulations and rising demand for cleaner formulations. Businesses are further concentrating on customized solutions tailored for coatings, adhesives, pharmaceuticals, and specialty materials industries to secure long-term competitive positioning and strengthen their global market presence.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Technology

- 2.2.2 Polymer type

- 2.2.3 End User

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for low-contamination polymer dispersion systems

- 3.2.1.2 Regulatory focus on reducing conventional surfactant usage

- 3.2.1.3 Performance advantages in films stability and durability

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited scalability compared with conventional emulsion processes

- 3.2.2.2 Higher formulation complexity during polymerization control stages

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into pharmaceutical and biomedical material applications

- 3.2.3.2 Adoption in high-purity coatings and specialty adhesives

- 3.2.3.3 Advancements in controlled radical polymerization techniques methods

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By polymer type

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Technology, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Raft/madix-mediated emulsion

- 5.3 Initiator-based stabilization

- 5.4 Pickering emulsion

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Polymer Type, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Acrylic & methacrylic polymers

- 6.2.1 Polyacrylates

- 6.2.2 Poly(methyl methacrylate)

- 6.2.3 Acrylic copolymers

- 6.3 Styrenic polymers

- 6.3.1 Polystyrene

- 6.3.2 Styrene-butadiene (SB latex)

- 6.3.3 Styrene-acrylonitrile

- 6.3.4 Acrylonitrile-butadiene-styrene (ABS)

- 6.4 Polyolefins

- 6.4.1 Polyethylene

- 6.4.2 Polypropylene

- 6.4.3 Ethylene-vinyl acetate (EVA)

- 6.5 Specialty polymers

- 6.5.1 Fluoropolymers (PVDF, PTFE)

- 6.5.2 Polyurethanes

- 6.5.3 Silicone polymers

- 6.5.4 Nylon resins

- 6.6 Others

- 6.6.1 Polyesters

- 6.6.2 Epoxy resins

- 6.6.3 Amino resins

- 6.6.4 Cellulosic polymers

Chapter 7 Market Estimates and Forecast, By End User, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Building & construction

- 7.2.1 Architectural coatings

- 7.2.2 Construction adhesives & sealants

- 7.2.3 Others

- 7.3 Automotive & transportation

- 7.3.1 Automotive coatings

- 7.3.2 Automotive adhesives

- 7.3.3 Others

- 7.4 Personal care & cosmetics

- 7.4.1 Cosmetics manufacturers

- 7.4.2 Personal care product formulators

- 7.4.3 Others

- 7.5 Healthcare & pharmaceuticals

- 7.5.1 Pharmaceutical companies

- 7.5.2 Drug delivery systems

- 7.5.3 Medical device coatings

- 7.5.4 Others

- 7.6 Textiles & apparel

- 7.6.1 Textile mills

- 7.6.2 Apparel manufacturers

- 7.6.3 Home furnishing

- 7.6.4 Others

- 7.7 Packaging

- 7.7.1 Flexible packaging

- 7.7.2 Rigid packaging

- 7.7.3 Others

- 7.8 Electronics & electrical

- 7.8.1 Electronic devices

- 7.8.2 Biomedical devices

- 7.8.3 Others

- 7.9 Others

- 7.9.1 Printing & imaging

- 7.9.2 Paper industry

- 7.9.3 Agriculture

- 7.9.4 Food & beverage

- 7.9.5 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 BASF

- 9.2 Dow

- 9.3 Arkema

- 9.4 Akzo Nobel

- 9.5 Covestro

- 9.6 JSR Corporation

- 9.7 Synthomer

- 9.8 ZEON Corporation

- 9.9 Allnex

- 9.10 Asahi Kasei

- 9.11 Celanese

- 9.12 TCI (Tokyo Chemical Industry)

(주말 및 공휴일 제외)