|

시장보고서

상품코드

2045835

시놉토포어(Synoptophore) 시장 : 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Synoptophore Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

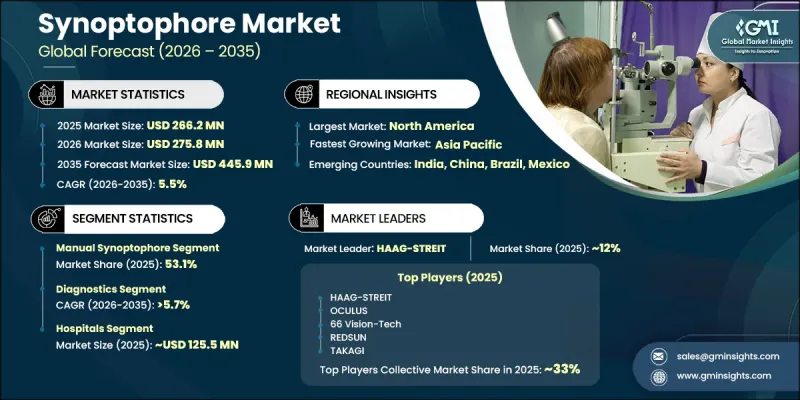

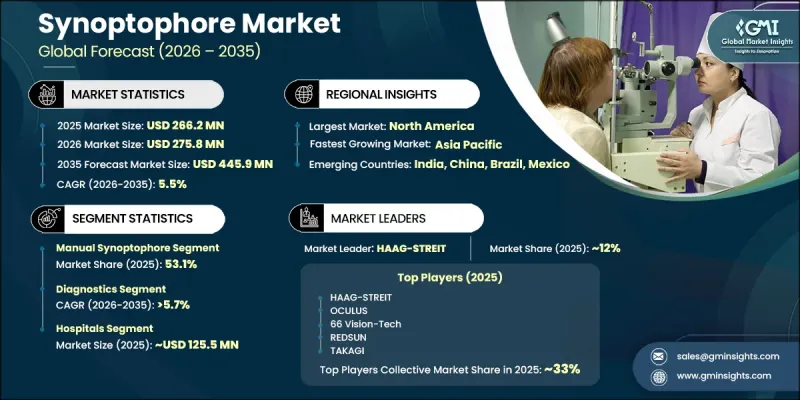

세계의 시놉토포어(Synoptophore) 시장은 2025년에 2억 6,620만 달러로 평가되었고 CAGR 5.5%를 나타내 2035년까지 4억 4,590만 달러에 이를 것으로 추정되고 있습니다.

시놉토포어(Synoptophore) 산업 전반의 성장은 의료비 증가, 안과 의료 인프라 개선, 전 세계 양안시 기능 장애의 유병률 증가에 의해 뒷받침되고 있습니다. 의료 서비스 제공업체들은 시각적 무결성 관련 질환의 조기 진단과 장기적인 관리에 더 많은 관심을 기울이고 있으며, 이로 인해 첨단 안과 진단 장비에 대한 수요가 크게 증가하고 있습니다. 시놉토포어(Synoptophore)는 양안시 기능 평가, 안구 협응력 평가 및 시각 장애 환자의 치료 관리를 돕기 위해 안과 의료시설에서 널리 사용되고 있습니다. 또한, 특히 의료 체계가 발전하는 국가에서 전문 안과 의료센터와 소아 안과 클리닉에 대한 투자가 확대되고 있는 것도 시장 성장의 원동력이 되고 있습니다. 의료 인프라에 대한 공공 및 민간 자금이 증가함에 따라 병원과 안과 클리닉은 첨단 시각 평가 기술 도입을 통해 진단 능력을 강화할 수 있게 되었습니다. 또한, 어린이 눈 건강과 조기 시력 검진 프로그램의 중요성에 대한 인식이 높아지면서 선진국과 신흥 시장 모두에서 시놉토포어(Synoptophore) 시스템 도입이 확대되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 2억 6,620만 달러 |

| 예측 금액 | 4억 4,590만 달러 |

| CAGR | 5.5% |

시놉토포어(Synoptophore)는 양안 협응 기능의 유효성을 평가하여 양안시 기능 장애를 진단하고 관리하기 위해 고안된 특수 광학기기입니다. 이 장비는 일반적으로 안과 검사 및 치료 과정에서 안위, 융합 능력 및 시각적 협응 기능을 평가하는 데 사용됩니다. 양안시 기능 이상 유병률 증가는 시놉토포어 시장에서 정확한 진단 및 치료 도구에 대한 수요를 지속적으로 견인하고 있습니다. 의료 인프라 확충과 전문 안과 의료 서비스 접근성 향상, 첨단 안과 기술의 보급을 촉진하는 것도 시장 성장을 뒷받침하고 있습니다. 예방적 안과 의료 및 조기 개입 전략에 대한 관심이 높아지면서 전 세계 병원, 안과 클리닉, 시력 훈련 센터에서 시놉토포어 장비의 도입이 더욱 활발해지고 있습니다.

2025년 기준, 수동식 시놉토포어(Synoptophore) 부문은 전 세계 시놉토포어(Synoptophore) 시장 점유율의 53.1%를 차지했습니다. 이 부문은 저렴한 가격, 조작의 편의성, 안과 의사와 시력 훈련사들 사이에서 높은 수용성으로 인해 계속해서 지배적인 위치를 유지하고 있습니다. 수동식 시스템은 신뢰할 수 있는 기계적 성능, 직관적인 작동, 최소한의 유지보수 요구 사항으로 안과 의료시설에서 널리 선호되고 있습니다. 내구성과 낮은 도입 비용으로 선진국과 개발도상국 모두에서 환자 수가 많은 의료시설, 교육 기관, 전문 시력 클리닉에 특히 적합합니다. 자동화 기술의 발전에도 불구하고, 수동식 시놉토포어(Synoptophore)는 일상적인 시력 검사 및 치료용도에서 입증된 임상적 신뢰성과 효과로 인해 여전히 높은 시장 수요를 유지하고 있습니다.

진단 분야는 2035년까지 연평균 복합 성장률(CAGR) 5.7%를 나타내 2억 5,540만 달러에 달할 것으로 예측됩니다. 진단용은 양안시 기능 평가, 시각적 협응력 평가, 소아 및 성인 환자의 임상 검사 절차를 지원하는 데 있어 중요한 역할을 하고 있기 때문에 시력 검사 시장에서 지속적으로 선두를 달리고 있습니다. 시놉토포어(Synoptophore)는 일상적인 안과 검진, 수술 전 평가 및 지속적인 시력 치료 평가에 있어 안과 및 시력 훈련 현장에서 널리 사용되고 있습니다. 정확하고 효율적인 시각적 진단 도구에 대한 수요 증가는 예측 기간 동안 이 부문의 성장을 계속 지원할 것으로 예측됩니다.

북미의 시놉토포어(Synoptophore) 시장은 2025년 1억 4,400만 달러 규모에 달했습니다. 이 지역은 선진화된 안과 의료 인프라, 확립된 소아 검진 프로그램, 양안시 기능 장애에 대한 높은 인지도를 바탕으로 탄탄한 시장 지위를 유지하고 있습니다. 북미 전역의 병원, 안과 전문 클리닉, 시기능 치료 센터는 시축이상 조기 진단과 체계적인 치료 접근법을 지속적으로 우선순위에 두고 있으며, 이는 시놉토포어 시스템에 대한 안정적인 수요를 견인하고 있습니다. 또한, 이 지역에는 유리한 보험 환급 제도와 숙련된 안과 의료 전문가를 광범위하게 확보할 수 있는 혜택이 있어 첨단 진단 장비의 도입을 더욱 촉진하고 있습니다. 소아 시각 장애의 유병률 증가와 예방적 안과 의료에 대한 관심이 높아짐에 따라 북미 시장 전체에서 전문 안과 장비에 대한 수요는 지속적으로 증가하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 용도별(2022-2035년)

제7장 시장 추산 및 예측 : 최종 용도별(2022-2035년)

제8장 시장 추산 및 예측 : 지역별(2022-2035년)

제9장 기업 개요

KTH 26.06.10The Global Synoptophore Market was valued at USD 266.2 million in 2025 and is estimated to grow at a CAGR of 5.5% to reach USD 445.9 million by 2035.

Growth across the synoptophore industry is being supported by rising healthcare expenditure, improvements in ophthalmic infrastructure, and the increasing prevalence of binocular vision disorders worldwide. Healthcare providers are placing a stronger emphasis on early diagnosis and long-term management of visual alignment conditions, which is significantly increasing demand for advanced ophthalmic diagnostic equipment. Synoptophores are widely utilized in eye care facilities to evaluate binocular vision, assess ocular coordination, and support therapeutic management for patients with vision disorders. The market is also benefiting from expanding investments in specialized eye care centers and pediatric vision clinics, particularly in developing healthcare systems. Increased public and private funding in healthcare infrastructure is enabling hospitals and ophthalmology clinics to strengthen diagnostic capabilities through the adoption of advanced vision assessment technologies. In addition, growing awareness regarding pediatric eye health and the importance of early vision screening programs is contributing to stronger adoption of synoptophore systems across both developed and emerging markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $266.2 Million |

| Forecast Value | $445.9 Million |

| CAGR | 5.5% |

A synoptophore is a specialized optical instrument designed to diagnose and manage binocular vision disorders by evaluating how effectively the eyes function together. These devices are commonly used to assess eye alignment, fusion capability, and visual coordination during ophthalmic examinations and therapeutic procedures. The rising prevalence of binocular vision abnormalities continues to drive demand for accurate diagnostic and treatment tools within the synoptophore market. Expanding healthcare infrastructure and greater accessibility to specialized eye care services are also supporting market growth by encouraging wider use of advanced ophthalmic technologies. Increased focus on preventive eye care and early intervention strategies is further contributing to the adoption of synoptophore devices across hospitals, eye clinics, and orthoptic centers globally.

The manual synoptophore segment accounted for 53.1% of the global synoptophore market share in 2025. The segment continues to maintain its dominant position due to its affordability, operational simplicity, and strong acceptance among ophthalmologists and orthoptic specialists. Manual systems are widely preferred in eye care facilities because they offer reliable mechanical performance, straightforward operation, and minimal maintenance requirements. Their durability and lower acquisition costs make them particularly suitable for high-volume healthcare settings, educational institutions, and specialized vision clinics across both developed and developing regions. Despite ongoing advancements in automated technologies, manual synoptophores continue to experience strong market demand due to their proven clinical reliability and effectiveness in routine vision assessment and therapeutic applications.

The diagnostics segment is projected to register a CAGR of 5.7% through 2035 and is expected to reach USD 255.4 million. Diagnostic applications continue to dominate the synoptophore market because these devices play a critical role in evaluating binocular vision function, assessing visual coordination, and supporting clinical examination procedures for both pediatric and adult patients. Synoptophores remain widely utilized in ophthalmology and orthoptic practices for routine eye examinations, surgical evaluations, and ongoing visual therapy assessments. Growing demand for accurate and efficient vision diagnostic tools is expected to continue supporting expansion within this segment throughout the forecast timeline.

North America Synoptophore Market generated USD 104.4 million in 2025. The region maintains a strong market position due to its advanced ophthalmic healthcare infrastructure, well-established pediatric screening programs, and high awareness regarding binocular vision disorders. Hospitals, specialty eye clinics, and vision therapy centers throughout North America continue to prioritize early diagnosis and structured treatment approaches for visual alignment conditions, driving consistent demand for synoptophore systems. The region also benefits from favorable reimbursement policies and widespread availability of trained eye care professionals, which further supports the adoption of advanced diagnostic equipment. Rising prevalence of childhood visual disorders and growing emphasis on preventive eye care continue to strengthen demand for specialized ophthalmic instruments across the North American market.

Key companies operating in the Global Synoptophore Market include DEVINE MEDITECH, HAAG-STREIT, REDSUN, NAUGRA, Roslane MEDITECH, VOWISH OPTICAL, 66 Vision-Tech, YTS Pharmaceuticals, OCULUS, and TAKAGI. Companies operating in the synoptophore industry are implementing several strategic initiatives to strengthen their competitive position and expand market presence. Leading manufacturers are investing in product innovation focused on improving diagnostic precision, user convenience, and device durability to meet evolving clinical requirements. Businesses are also increasing investments in research and development activities aimed at integrating advanced imaging capabilities, ergonomic designs, and enhanced functionality into modern synoptophore systems. Strategic collaborations with hospitals, ophthalmology clinics, and vision care centers are helping companies strengthen distribution networks and improve customer access to specialized ophthalmic equipment. In addition, manufacturers are expanding into emerging healthcare markets, enhancing professional training programs, and focusing on regulatory compliance to increase product adoption and reinforce their position within the global synoptophore market.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Advancements in automated and digital synoptophores

- 3.2.1.2 Increasing healthcare spending and improved eye care infrastructure

- 3.2.1.3 Growing prevalence of binocular vision disorders like amblyopia and strabismus

- 3.2.1.4 Growing emphasis on early diagnosis and preventive eye care

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Need for skilled professionals to operate synoptophores effectively

- 3.2.3 Opportunities

- 3.2.3.1 Digital and hybrid synoptophore development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology and innovation landscape (Driven by Primary Research)

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends (Driven by Primary Research)

- 3.7 Impact of AI & Generative AI on the Market (Driven by Primary Research)

- 3.8 Pricing analysis, 2025

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by Primary Research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Manual synoptophore

- 5.3 Automated synoptophore

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Diagnostics

- 6.3 Therapeutics

- 6.4 Hybrid

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ophthalmic centers

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 DEVINE MEDITECH

- 9.2 HAAG-STREIT

- 9.3 REDSUN

- 9.4 NAUGRA

- 9.5 Roslane MEDITECH

- 9.6 VOWISH OPTICAL

- 9.7 66 Vision-Tech

- 9.8 YTS Pharmaceuticals

- 9.9 OCULUS

- 9.10 TAKAGI