|

시장보고서

상품코드

2045845

판금 가공 서비스 시장 : 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Sheet Metal Fabrication Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

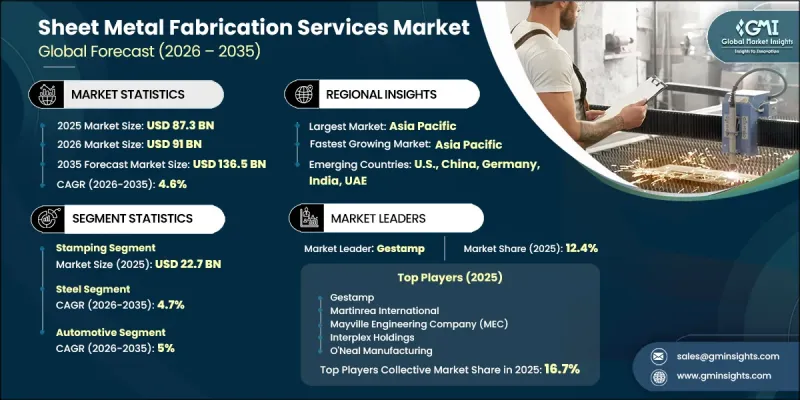

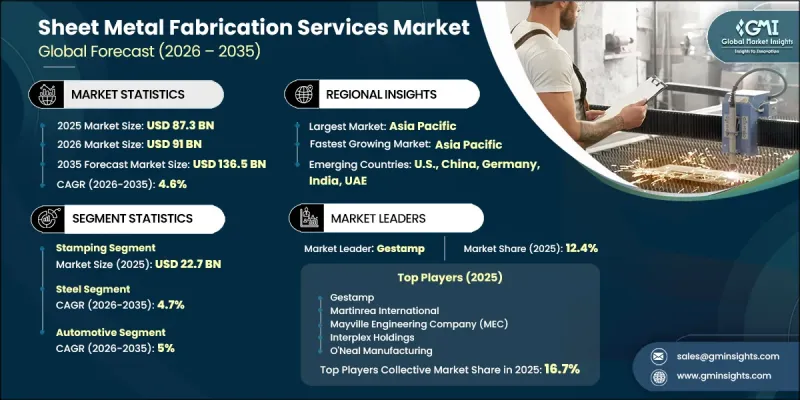

세계의 판금 가공 서비스 시장은 2025년에 873억 달러로 평가되었고 CAGR 4.6%를 나타내 2035년까지 1,365억 달러에 이를 것으로 예측됩니다.

판금 가공 서비스 산업은 자동차, 항공우주, 건설 등 주요 부문에서 가볍고 내구성이 뛰어난 소재에 대한 수요가 증가함에 따라 꾸준한 성장세를 보이고 있습니다. 이러한 산업에서는 정밀하게 설계된 부품에 대한 의존도가 높아지고 있으며, 판금 가공 서비스는 이를 효율적이고 안정적으로 제공합니다. 또한, 제조업체들이 에너지 효율을 높이고 차량 전체 무게를 줄이는 소재를 찾는 가운데, 전기 모빌리티 솔루션의 보급이 확대되고 있는 것도 수요를 더욱 가속화하고 있습니다. 이와 함께 자동 절단, 정밀 용접, 적층 가공 등 가공 기술의 발전으로 생산 효율이 크게 향상되어 재료의 낭비를 최소화하고 복잡한 형상의 개발이 가능해졌습니다. 또한, 신흥국의 인프라 프로젝트 확대도 시장 성장에 기여하고 있습니다. 주택, 상업, 산업 건설에 대한 대규모 투자로 인해 금속 가공 부품에 대한 수요가 증가하고 있기 때문입니다. 또한, 가공 기술 향상과 재료 성능 개선을 위한 지속적인 연구개발 노력은 장기적인 시장 확대를 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 873억 달러 |

| 예측 금액 | 1,365억 달러 |

| CAGR | 4.6% |

프레스 가공 부문은 2025년 227억 달러에 달했고 2035년까지 연평균 4.6%의 성장률을 나타낼 것으로 예측됩니다. 이 부문은 일관성 있고 내구성이 뛰어난 부품을 대량 생산해야 하는 다양한 산업 분야에서 폭넓게 적용되면서 지속적으로 성장하고 있습니다. 경량 및 고강도 부품에 대한 수요 증가는 스탬핑 공정의 채택을 촉진하고 있으며, 제조 기술의 지속적인 개선으로 효율성과 생산 품질이 향상되고 있습니다.

철강 부문은 2025년 54%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 4.7%를 나타낼 것으로 전망됩니다. 그 광범위한 사용은 강도, 비용 효율성 및 다양한 산업 분야에서의 적응성에 의해 주도되고 있습니다. 철강 가공 기술의 발전과 내구성과 경량화를 겸비한 소재에 대한 수요 증가는 이 부문의 성장을 더욱 촉진하고 있습니다.

미국의 판금 가공 서비스 시장은 2025년 80%의 점유율을 차지하며 190억 달러 시장 규모를 기록했습니다. 이 나라 시장 성장은 강력한 산업 발전과 탄탄한 제조거점에 의해 주도되고 있습니다. 건설, 에너지, 중공업 등 다양한 분야의 확장은 가공 서비스에 대한 지속적인 수요를 창출하고 있습니다. 전통 산업과 신흥 산업 모두에 대한 투자 증가는 시장 전망을 더욱 견고하게 만들고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 서비스 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 소재별(2022-2035년)

제7장 시장 추산 및 예측 : 최종 사용 산업별(2022-2035년)

제8장 시장 추산 및 예측 : 유통 채널별(2022-2035년)

제9장 시장 추산 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

KTH 26.06.10The Global Sheet Metal Fabrication Services Market was valued at USD 87.3 billion in 2025 and is estimated to grow at a CAGR of 4.6% to reach USD 136.5 billion by 2035.

The sheet metal fabrication services industry is witnessing steady expansion driven by the growing requirement for lightweight yet durable materials across key sectors such as automotive, aerospace, and construction. These industries increasingly depend on precision-engineered components, which fabrication services deliver with efficiency and consistency. The rising adoption of electric mobility solutions is further accelerating demand, as manufacturers seek materials that enhance energy efficiency and reduce overall vehicle weight. In parallel, advancements in fabrication technologies, including automated cutting, precision welding, and additive manufacturing, are significantly improving production efficiency, minimizing material waste, and enabling the development of complex geometries. Expanding infrastructure projects across developing economies are also contributing to market growth, as large-scale investments in residential, commercial, and industrial construction increase the need for fabricated metal components. Additionally, ongoing research and development efforts aimed at enhancing fabrication techniques and improving material performance continue to support long-term market expansion.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $87.3 Billion |

| Forecast Value | $136.5 Billion |

| CAGR | 4.6% |

The stamping segment accounted for USD 22.7 billion in 2025 and is expected to grow at a CAGR of 4.6% through 2035. This segment continues to gain traction due to its extensive application across multiple industries that require high-volume production of consistent and durable components. Increasing demand for lightweight and strong parts is supporting the adoption of stamping processes, while continuous improvements in manufacturing technologies are enhancing efficiency and output quality.

The steel segment held a 54% share in 2025 and is anticipated to grow at a CAGR of 4.7% from 2026 to 2035. Its widespread use is driven by its strength, cost-effectiveness, and adaptability across various industries. Advancements in steel processing and the growing need for materials that balance durability with reduced weight are further supporting segment growth.

United States Sheet Metal Fabrication Services Market held 80% share, generating USD 19 billion in 2025. Market growth in the country is fueled by strong industrial development and a well-established manufacturing base. Expansion across multiple sectors, including construction, energy, and heavy industries, continues to create sustained demand for fabrication services. Increasing investments in both traditional and emerging industries are further strengthening the market outlook.

Key companies operating in the Global Sheet Metal Fabrication Services Market include BTD Manufacturing, Gestamp, Interplex Holdings, Kapco Global, Martinrea International, Mayville Engineering Company (MEC), MW Industries, All Metals Fabrication, Ironform Corporation, Manor Tool & Manufacturing, Noble Industries, O'Neal Manufacturing Services, Ryerson Advanced Processing, Standard Iron & Wire Works, Approved Sheet Metal (ASM), Buckeye Shapeform, Capps Manufacturing, Kencoa Aerospace LLC, Laserage Technology Corporation, V&F Sheet Metal, and Xometry. Companies in the sheet metal fabrication services market are focusing on strategic investments in advanced manufacturing technologies to enhance efficiency and precision. Many players are adopting automation, digital manufacturing systems, and smart production processes to reduce operational costs and improve turnaround times. Expanding production capabilities and geographic presence through partnerships, acquisitions, and facility upgrades is also a key approach to strengthen market positioning. Firms are prioritizing research and development to introduce innovative fabrication techniques and improve material performance.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Service Type

- 2.2.3 Material

- 2.2.4 End Use Industry

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Service provider

- 3.2 Value Chain Analysis

- 3.2.1 Raw material suppliers

- 3.2.2 Fabrication service providers

- 3.2.3 Distribution and logistics

- 3.2.4 End-use customers

- 3.2.5 Profit margin analysis by value chain stage

- 3.3 Pricing analysis, 2025 (driven by primary research)

- 3.3.1 Historical price trend analysis

- 3.3.2 Pricing strategy by player type

- 3.3.3 Price variation by product type & technology generation

- 3.3.4 Consumer price sensitivity analysis

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.4.3 Market opportunities

- 3.5 Growth potential analysis

- 3.6 Regulatory landscape

- 3.6.1 Global regulatory framework for manufacturing and industrial safety

- 3.6.2 North America - OSHA standards and industry regulations

- 3.6.3 Environmental compliance and sustainability mandates

- 3.6.4 Compliance requirements

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Technological and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Future market trends

- 3.11 Impact of AI & generative ai on the market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 GenAI use cases & adoption roadmap by segment

- 3.11.3 Risks, limitations & regulatory considerations

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Service Type, 2022 - 2035 ($Billion)

- 5.1 Key trends

- 5.2 Cutting

- 5.3 Punching

- 5.4 Stamping

- 5.5 Forming

- 5.6 Bending

- 5.7 Welding

- 5.8 Finishing

- 5.9 Others

Chapter 6 Market Estimates & Forecast, By Material, 2022 - 2035 ($Billion)

- 6.1 Key trends

- 6.2 Steel

- 6.3 Aluminum

- 6.4 Silver

- 6.5 Others (copper, brass, stainless steel etc.)

Chapter 7 Market Estimates & Forecast, By End Use Industry, 2022 - 2035 ($Billion)

- 7.1 Key trends

- 7.2 Automotive

- 7.2.1 Light vehicles

- 7.2.2 Commercial vehicles

- 7.2.3 Electric vehicles

- 7.3 Aerospace & Space

- 7.3.1 Commercial aerospace

- 7.3.2 Defense aerospace

- 7.4 Industrial Machinery

- 7.4.1 Manufacturing equipment

- 7.4.2 Material handling systems

- 7.4.3 Processing machinery

- 7.5 Construction

- 7.6 Electronics

- 7.7 Data Centers

- 7.8 Others (telecommunication etc.)

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Billion)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 BTD Manufacturing

- 10.1.2 Gestamp

- 10.1.3 Interplex Holdings

- 10.1.4 Kapco Global

- 10.1.5 Martinrea International

- 10.1.6 Mayville Engineering Company (MEC)

- 10.1.7 MW Industries

- 10.2 Regional Key Players

- 10.2.1 All Metals Fabrication

- 10.2.2 Ironform Corporation

- 10.2.3 Manor Tool & Manufacturing

- 10.2.4 Noble Industries

- 10.2.5 O'Neal Manufacturing Services

- 10.2.6 Ryerson Advanced Processing

- 10.2.7 Standard Iron & Wire Works

- 10.3 Emerging Niche Specialist

- 10.3.1 Approved Sheet Metal (ASM)

- 10.3.2 Buckeye Shapeform

- 10.3.3 Capps Manufacturing

- 10.3.4 Kencoa Aerospace LLC

- 10.3.5 Laserage Technology Corporation

- 10.3.6 V&F Sheet Metal

- 10.3.7 Xometry