|

시장보고서

상품코드

2061293

승용차용 HVAC 서비스 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Passenger Vehicles HVAC Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

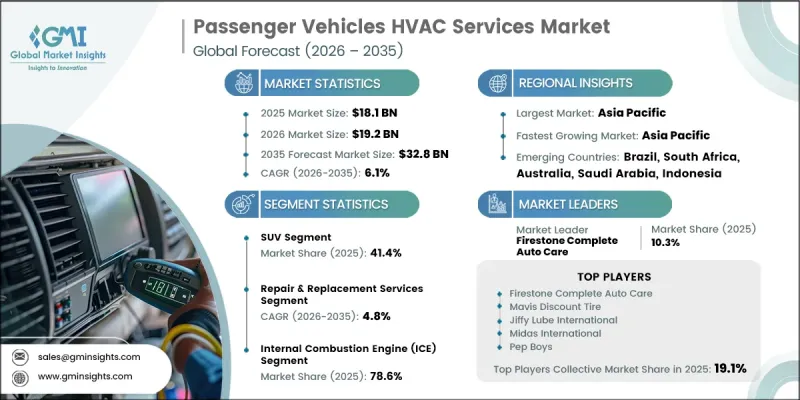

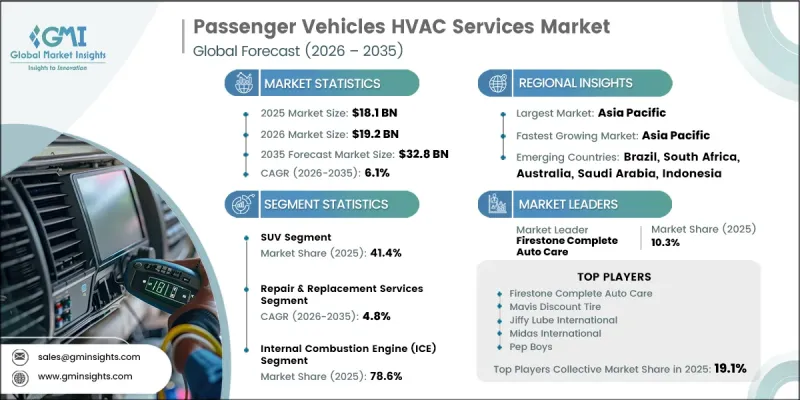

세계의 승용차용 HVAC 서비스 시장은 2025년에 181억 달러로 평가되고 CAGR 6.1%로 성장하며, 2035년까지 328억 달러에 달할 것으로 추정되고 있습니다.

승용차용 HVAC 서비스 업계의 성장은 차내의 뛰어난 쾌적성, 공기 순환 개선, 그리고 효율적인 온도 관리에 대한 소비자의 기대가 높아짐에 따라 주도되고 있습니다. 차량 소유주들은 차량 내부의 환경 품질을 더욱 중요하게 여기게 되면서, 전문적인 HVAC 점검, 유지보수 및 수리 서비스에 대한 수요를 촉진하고 있습니다. 첨단 공조 관리 시스템을 탑재한 기술적으로 첨단인 승용차의 보급이 확대되면서 전 세계의 서비스 수요가 더욱 증가하고 있습니다. 또한 차량의 효율성과 탑승자의 건강에 대한 관심이 높아짐에 따라 최적의 성능과 신뢰성을 확보하기 위해 HVAC 시스템의 유지보수 빈도가 증가하고 있습니다. 자동차 서비스 제공업체들은 점점 더 복잡해지는 HVAC 기술에 대응하기 위해 역량을 확대함으로써 이에 부응하고 있습니다. 승용차에 첨단 열 관리 솔루션이 지속적으로 도입됨에 따라 예방 정비, 진단 및 시스템 최적화 서비스에 대한 수요는 꾸준히 증가할 것으로 예상됩니다. 자동차 보유 대수의 증가, 기술의 고도화, 그리고 쾌적성과 공기질에 대한 소비자의 관심이 높아지는 요인이 맞물리면서, 전 세계 승용차용 HVAC 서비스 시장에는 계속해서 유망한 성장 기회가 창출되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 181억 달러 |

| 예측액 | 328억 달러 |

| CAGR | 6.1% |

전기자동차 및 하이브리드 승용차의 보급이 지속적으로 확대되고 있는 것은 승용차용 HVAC 서비스 시장의 발전에 큰 영향을 미치고 있습니다. 기존 차량 플랫폼과 비교했을 때, 전기화 차량은 에너지 효율을 극대화하고 차량 전체의 성능을 지원하도록 설계된, 매우 첨단인 열 관리 기술을 채택하고 있습니다. 이러한 시스템에는 전문적인 정비 기술, 첨단 진단 능력, 그리고 전용 유지보수 절차가 필요합니다. 세계 시장에서 전동 모빌리티의 성장세가 가속화됨에 따라 서비스 제공업체들은 차세대 공조 및 열 관리 시스템을 지원하기 위해 필요한 기술 역량과 인프라에 대한 투자를 점점 더 늘리고 있습니다. 이러한 변화는 자동차 애프터마켓 전반에 걸쳐 전문적인 HVAC 정비 서비스에 대한 수요 증가에 기여하고 있습니다.

SUV 부문은 41.4%의 시장 점유율을 차지하고 있으며, 2026-2035년 연평균 성장률(CAGR) 7.6%로 성장할 것으로 전망됩니다. 선진국과 신흥 국가의 자동차 시장을 막론하고, 스포츠 유틸리티 차량(SUV)에 대한 소비자들의 강한 선호가 이 부문의 성장을 지속적으로 지원하고 있습니다. 차내 공간이 넓고 공조 제어 시스템이 더 정교하므로 SUV는 일반적으로 다른 많은 승용차 카테고리보다 더 많은 HVAC 유지보수 및 서비스 요구 사항을 필요로 합니다. 이러한 시스템의 복잡화에 따라 정기 점검, 진단 및 수리 서비스에 대한 수요가 증가하고 있으며, 이는 시장에서 해당 부문의 선도적 입지를 더욱 공고히 하고 있습니다.

2025년에는 개인 차량 소유자 부문이 62%의 점유율을 차지했습니다. 전 세계에서 엄청난 수의 개인 소유 승용차가 존재하며, 이는 HVAC 유지보수 및 성능 최적화 서비스에 대한 안정적인 수요를 지속적으로 견인하고 있습니다. 차량 소유주들은 승객의 쾌적성, 차내 공기질, 그리고 장기적인 운영 효율을 확보하기 위해 공조 시스템 유지보수의 중요성을 점점 더 인식하고 있습니다. 차내 환경의 질과 차량 정비에 대한 베스트 프랙티스에 대한 인식이 높아짐에 따라 개인 소비자들의 정기적인 정비가 더욱 활성화되고 있습니다. 동시에, 상업용 운송, 렌터카 사업, 공유 모빌리티 서비스에서 승용차 이용이 확대됨에 따라 차량 관리 사업자가 중요한 성장 부문으로 부상하고 있습니다. 차량의 가동률과 승객 만족도를 유지해야 할 필요성이, 차량 운용 전반에 걸친 HVAC 서비스 수요 증가에 기여하고 있습니다.

2025년, 중국의 승용차용 HVAC 서비스 시장은 47.2%의 점유율을 차지하며 39억 달러의 시장 규모를 기록했습니다. 이 국가의 시장내 주도적 지위는 막대한 승용차 보유 대수, 가속화되는 도시 개발, 그리고 견고한 자동차 제조 부문에 의해 지원되고 있습니다. 대도시권 및 개발도상 도시 지역의 자동차 보유 대수 증가는 HVAC 시스템의 유지보수 및 성능 관리 서비스에 대한 막대한 수요를 창출하고 있습니다. 가처분 소득의 증가, 모빌리티 수요의 확대, 그리고 승용차 이용의 지속적인 증가가 시장 확대에 더욱 기여하고 있습니다. 이러한 요인들로 인해 차량의 수명 주기 전반에 걸쳐 신뢰성 높은 HVAC 성능을 보장하기 위해 설계된 예방 정비 프로그램, 수리 서비스 및 첨단 진단 솔루션에 대한 지속적인 수요가 촉진되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 차량별, 2022-2035년

제6장 시장 추산·예측 : 서비스별, 2022-2035년

제7장 시장 추산·예측 : 추진력별, 2022-2035년

제8장 시장 추산·예측 : 최종 사용별, 2022-2035년

제9장 시장 추산·예측 : 지역별, 2022-2035년

제10장 기업 개요

KSA 26.06.25The Global Passenger Vehicles HVAC Services Market was valued at USD 18.1 billion in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 32.8 billion by 2035.

Growth across the passenger vehicles HVAC services industry is driven by increasing consumer expectations for superior cabin comfort, improved air circulation, and efficient temperature management within vehicles. Vehicle owners are placing greater importance on interior environmental quality, encouraging demand for professional HVAC inspection, maintenance, and repair services. The growing penetration of technologically advanced passenger vehicles equipped with sophisticated climate management systems is further strengthening service requirements worldwide. In addition, rising awareness regarding vehicle efficiency and passenger well-being is prompting more frequent maintenance of HVAC systems to ensure optimal performance and reliability. Automotive service providers are responding by expanding their capabilities to address increasingly complex HVAC technologies. As passenger vehicles continue to incorporate advanced thermal management solutions, demand for preventive maintenance, diagnostics, and system optimization services is expected to rise steadily. The combination of expanding vehicle ownership, increasing technological sophistication, and growing consumer focus on comfort and air quality continues to create favorable growth opportunities for the global passenger vehicles HVAC services market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $18.1 Billion |

| Forecast Value | $32.8 Billion |

| CAGR | 6.1% |

The ongoing expansion of electric and hybrid passenger vehicle adoption is significantly influencing the evolution of the passenger vehicles HVAC services market. Compared to traditional vehicle platforms, electrified vehicles utilize highly advanced thermal management technologies designed to maximize energy efficiency and support overall vehicle performance. These systems require specialized servicing expertise, advanced diagnostic capabilities, and dedicated maintenance procedures. As electrified mobility gains momentum across global markets, service providers are increasingly investing in the technical skills and infrastructure required to support next-generation climate control and thermal management systems. This shift is contributing to rising demand for specialized HVAC servicing across the automotive aftermarket.

The SUV segment accounted for 41.4% share and is expected to grow at a CAGR of 7.6% from 2026 to 2035. Strong consumer preference for sport utility vehicles across developed and emerging automotive markets continues to support segment growth. Due to their larger cabin dimensions and more sophisticated climate control configurations, SUVs generally require greater HVAC maintenance and servicing requirements than many other passenger vehicle categories. The increased complexity of these systems contributes to higher demand for routine inspections, diagnostics, and repair services, reinforcing the segment's leadership position within the market.

The individual vehicle owners segment held a 62% share in 2025. A substantial global population of privately owned passenger vehicles continues to drive consistent demand for HVAC maintenance and performance optimization services. Vehicle owners increasingly recognize the importance of maintaining climate control systems to ensure passenger comfort, interior air quality, and long-term operational efficiency. Rising awareness of cabin environment quality and vehicle maintenance best practices is further encouraging routine servicing among private consumers. At the same time, fleet operators are emerging as a significant growth segment, supported by the expanding use of passenger vehicles across commercial transportation, rental operations, and shared mobility services. The need to maintain vehicle uptime and passenger satisfaction is contributing to increased HVAC service demand across fleet applications.

China Passenger Vehicles HVAC Services Market accounted for 47.2% share and generated USD 3.9 billion in 2025. The country's market leadership is supported by its extensive passenger vehicle population, accelerating urban development, and robust automotive manufacturing sector. Growing vehicle ownership levels across metropolitan and developing urban areas are creating substantial demand for HVAC system maintenance and performance management services. Rising disposable incomes, expanding mobility requirements, and continued growth in passenger vehicle utilization are further contributing to market expansion. These factors are driving sustained demand for preventive maintenance programs, repair services, and advanced diagnostic solutions designed to ensure reliable HVAC performance throughout the vehicle lifecycle.

Key companies operating in the Global Passenger Vehicles HVAC Services Industry include Firestone Complete Auto Care, Jiffy Lube International, Midas International, Pep Boys, Monro, Mavis Discount Tire, and 1-800-Radiator & A/C. Companies participating in the passenger vehicles HVAC services market are implementing a variety of strategies to strengthen their competitive position and expand market reach. Industry participants are investing in advanced diagnostic technologies, technician training programs, and specialized service capabilities to support increasingly sophisticated vehicle climate control systems. Network expansion through new service locations, franchise development, and strategic partnerships remains a key growth approach. Many providers are also enhancing customer engagement through digital scheduling platforms, preventive maintenance programs, and service package offerings designed to improve customer retention. In addition, businesses are focusing on expanding their expertise in servicing electric and hybrid vehicle HVAC systems while improving operational efficiency and service quality. These initiatives are helping companies enhance brand recognition, increase market share, and strengthen long-term customer relationships across the global passenger vehicles HVAC services market.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Service

- 2.2.4 Propulsion

- 2.2.5 End use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Adoption of Electric and Hybrid Vehicles

- 3.2.1.2 Increasing Focus on Passenger Comfort and Air Quality

- 3.2.1.3 Growth in Automotive Aftermarket Services

- 3.2.1.4 Stringent Environmental and Efficiency Regulations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Cost of Advanced HVAC Systems Servicing

- 3.2.2.2 Shortage of Skilled Technicians for EV HVAC Systems

- 3.2.2.3 Complexity of Thermal Management in Electrified Vehicles

- 3.2.2.4 Variability in Service Standards Across Regions

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of EV Fleet and Thermal Management Needs

- 3.2.3.2 Growth in Predictive Maintenance and Connected Services

- 3.2.3.3 Increasing Demand in Emerging Markets

- 3.2.3.4 Retrofit and Upgrade Services for Existing Vehicles

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing Analysis (Driven by primary research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 U.S. Environmental Protection Agency

- 3.6.1.2 National Highway Traffic Safety Administration

- 3.6.1.3 Federal Communications Commission

- 3.6.2 Europe

- 3.6.2.1 Federal Ministry for Digital and Transport

- 3.6.2.2 Federal Motor Transport Authority

- 3.6.2.3 France: Ministry for the Ecological Transition

- 3.6.2.4 French Environment and Energy Management Agency

- 3.6.3 Asia Pacific

- 3.6.3.1 Ministry of Industry and Information Technology

- 3.6.3.2 Ministry of Ecology and Environment

- 3.6.4 Latin America

- 3.6.4.1 National Land Transportation Agency

- 3.6.4.2 National Traffic Department

- 3.6.4.3 Secretariat of Infrastructure, Communications and Transport

- 3.6.5 Middle East & Africa

- 3.6.5.1 Ministry of Energy and Infrastructure

- 3.6.5.2 Emirates Authority for Standardization and Metrology

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by primary research)

- 3.10 Cost breakdown analysis

- 3.11 Impact of AI and Generative AI on the Market

- 3.11.1 AI Driven Disruption of Existing Business Models

- 3.11.2 GenAI Use Cases and Adoption Roadmap by Segment

- 3.11.3 Risks Limitations and Regulatory Considerations

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.13.1 Base Case- Key Macro & Industry Variables Driving CAGR

- 3.13.2 Optimistic Scenarios- Favorable macro and industry tailwinds

- 3.13.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022 - 2035 (USD Mn, Units)

- 5.1 Key trends

- 5.2 SUV

- 5.3 Sedan

- 5.4 Hatchback

Chapter 6 Market Estimates & Forecast, By Service, 2022 - 2035 (USD Mn, Units)

- 6.1 Key trends

- 6.2 Preventive Maintenance Services

- 6.3 Diagnostic Services

- 6.4 Repair & Replacement Services

- 6.5 Installation & Retrofit Services

- 6.6 Software & Calibration Services

Chapter 7 Market Estimates & Forecast, By Propulsion, 2022 - 2035 (USD Mn, Units)

- 7.1 Key trends

- 7.2 Battery Electric Vehicles (BEVs)

- 7.3 Plug-in Hybrid Electric Vehicles (PHEVs)

- 7.4 Hybrid Electric Vehicles (HEVs)

- 7.5 Internal Combustion Engine (ICE)

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035 (USD Mn, Units)

- 8.1 Key trends

- 8.2 Individual Vehicle Owners

- 8.3 Fleet Operators

- 8.4 Ride-Hailing & Mobility Companies

- 8.5 Public Transport Authorities

- 8.6 Logistics & Delivery Operators

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Norway

- 9.3.8 Netherlands

- 9.3.9 Sweden

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Singapore

- 9.4.7 Thailand

- 9.4.8 Indonesia

- 9.4.9 Vietnam

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Turkey

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Firestone Complete Auto Care

- 10.1.2 Jiffy Lube International

- 10.1.3 Midas International

- 10.1.4 Pep Boys

- 10.1.5 Monro

- 10.1.6 Meineke Car Care Centers

- 10.1.7 Goodyear Auto Service

- 10.1.8 Bosch Car Service

- 10.1.9 Euromaster

- 10.1.10 Halfords Autocentres

- 10.1.11 Driven Brands

- 10.1.12 1-800-Radiator & A/C

- 10.1.13 LKQ

- 10.2 Regional Players

- 10.2.1 Mahindra First Choice Services

- 10.2.2 Carnation Auto

- 10.2.3 Autobacs Seven

- 10.2.4 Yellow Hat

- 10.2.5 Sun Auto Tire & Service

- 10.2.6 ATS Euromaster

- 10.2.7 Norauto

- 10.2.8 Feu Vert

- 10.3 Emerging Players

- 10.3.1 RepairPal

- 10.3.2 GoMechanic

- 10.3.3 SparesHub