|

시장보고서

상품코드

2071181

혐기성 소화 장비 시장 : 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Anaerobic Digestion Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

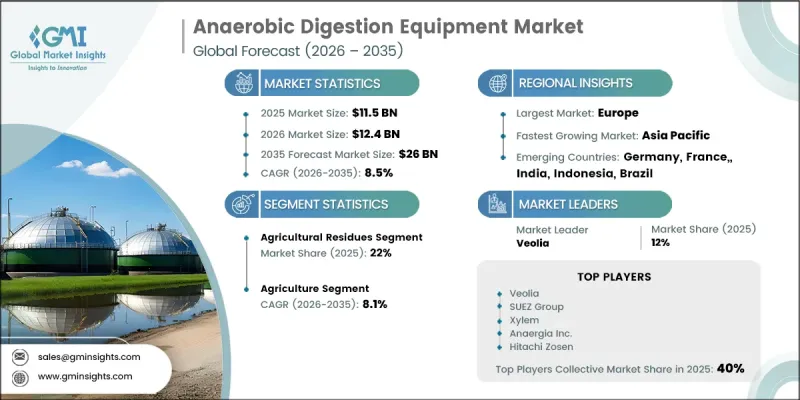

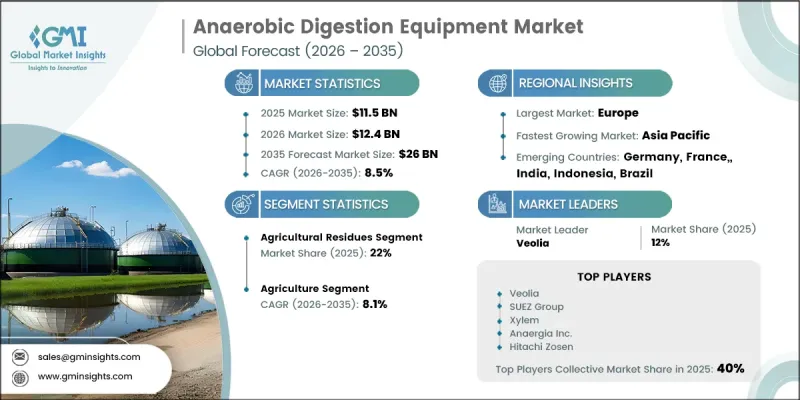

세계의 혐기성 소화 장비 시장은 2025년에 115억 달러 규모가 되어, CAGR 8.5%로 성장하여 2035년까지 260억 달러에 이를 것으로 추정되고 있습니다.

지금까지 시장의 발전은 유럽의 농업 활동에서 생산되는 바이오가스와 북미 전역의 폐수 처리 용도에 힘입어 이루어져 왔습니다. 그러나 현재 이 업계는 더욱 광범위한 확장 단계에 접어들었으며, 식품 폐기물, 도시 고형 폐기물(MSW), 산업 폐수의 활용이 증가하고 있는 점이 신규 장비 도입에 크게 기여하고 있습니다. 동시에, 바이오메탄 정제 기술이 수익 성장의 주요 원천으로 부상하고 있어, 장비 제조업체와 프로젝트 개발자에게 더 많은 비즈니스 기회를 창출하고 있습니다. 투자 활동은 지리적으로 더욱 다양해지고 있으며, 아시아태평양은 정부 주도의 노력을 통해 여러 국가가 대규모 시설 도입을 가속화하고 있어, 혐기성 소화 장비 조달 분야에서 점점 더 중요한 시장으로 부상하고 있습니다. 에너지 안보에 대한 관심이 높아지는 가운데, 혐기성 소화는 단순한 폐기물 관리 방안에서 재생 가능 가스 생산 전략의 중요한 구성 요소로 변모하고 있습니다. 매립 처리장에 유기성 폐기물을 투기하는 것을 줄이는 것을 목적으로 한 규제 조치로 인해, 혐기성 소화 시스템에 대한 지속적인 수요가 계속해서 발생하고 있습니다. 유럽, 북미, 아시아태평양을 포함한 주요 지역에서 지원적인 정책 체계가 장기적인 시장 전망을 더욱 명확하게 하고 있습니다. 견실한 펀더멘털을 갖추고 있음에도 불구하고, 혐기성 소화 사업에는 여러 수익원이 있으며, 각각이 서로 다른 위험 특성과 계약 구조를 가지고 있기 때문에 프로젝트 자금 조달은 여전히 복잡한 상황에 놓여 있습니다. 이러한 과제를 해결하기 위해 프로젝트 이해관계자들은 프로젝트 위험을 줄이고 자금 조달 전망을 개선하는 데 도움이 되는 장기 재생 가능 가스 공급 계약, 통합형 엔지니어링 및 운영 서비스 모델, 그리고 유틸리티체와의 제휴를 점점 더 많이 도입하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 115억 달러 |

| 예측 금액 | 260억 달러 |

| CAGR | 8.5% |

농업 잔여물 부문은 2025년에 22%의 시장 점유율을 차지하고, 2035년까지 연평균 성장률(CAGR) 7.7%로 성장할 것으로 전망됩니다. 이 부문은 농업 활동 및 농산물 가공 과정에서 발생하는 바이오매스 자원을 풍부하게 활용할 수 있기 때문에 주도적인 위치를 유지하고 있습니다. 이러한 원료는 널리 도입된 혐기성 소화 기술과 매우 잘 어울리며, 상업 규모 및 산업 규모의 시설 확장을 지속적으로 뒷받침하고 있습니다. 자원 활용을 극대화하고 농업 폐기물을 활용한 재생에너지 발전량을 늘리기 위한 노력이 활발해지고 있는 만큼, 이러한 자재를 효율적으로 처리하기 위한 장비에 대한 수요는 앞으로도 지속될 것으로 예측됩니다.

에너지 및 유틸리티 부문은 2025년에 18%의 점유율을 차지하고 있으며, 2035년까지 연평균 성장률(CAGR) 8.6%로 성장할 것으로 전망됩니다. 이 부문에는 재생 가능 가스 생산, 발전 및 폐기물로부터 에너지를 회수하는 통합 사업에 특화된 시설이 포함됩니다. 재생에너지 인프라에 대한 투자 확대와 저탄소 에너지 솔루션에 대한 수요 증가가 맞물리면서, 유틸리티 규모의 프로젝트 전반에 걸쳐 첨단 혐기성 소화 기술의 도입이 촉진되고 있습니다. 탈탄소화와 에너지 다각화에 대한 관심이 높아짐에 따라, 예측 기간 동안 해당 부문의 성장 전망은 더욱 밝아질 것으로 예측됩니다.

북미의 혐기성 소화 장비 시장은 2025년에 27%의 점유율을 차지하고, 2035년까지 연평균 성장률(CAGR) 7.5%로 성장할 것으로 전망됩니다. 미국은 재생 가능 천연가스 생산, 폐기물 관리의 현대화, 그리고 청정 에너지 인프라에 대한 투자 증가에 힘입어 계속해서 지역 수요의 최대 견인차 역할을 하고 있습니다. 탄소 배출량 감축과 재생 가능 연료 도입 촉진을 목적으로 한 우호적인 규제 조치가 시장 진출기업들에게 매력적인 기회를 지속적으로 창출하고 있습니다. 바이오가스 정제 기술, 폐기물 발전 프로젝트, 농업 폐기물 처리 시설에 대한 지속적인 투자가 해당 지역 전체의 장기적인 시장 성장을 뒷받침할 것으로 예측됩니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 규모 및 예측 : 원료별, 2022-2035년

제6장 시장 규모 및 예측 : 기기별, 2022-2035년

제7장 시장 규모 및 예측 : 기술별, 2022-2035년

제8장 시장 규모 및 예측 : 용도별, 2022-2035년

제9장 시장 규모 및 예측 : 최종 용도별, 2022-2035년

제10장 시장 규모 및 예측 : 지역별, 2022-2035년

제11장 기업 개요

JHS 26.07.01The Global Anaerobic Digestion Equipment Market was valued at USD 11.5 billion in 2025 and is estimated to grow at a CAGR of 8.5% to reach USD 26 billion by 2035.

Historically, market development was supported by biogas production from agricultural activities in Europe and wastewater treatment applications across North America. However, the industry is now entering a broader phase of expansion, with increasing utilization of food waste, municipal solid waste (MSW), and industrial wastewater streams contributing significantly to new capacity installations. At the same time, biomethane upgrading technologies are becoming a major source of revenue growth, creating additional opportunities for equipment manufacturers and project developers. Investment activity is becoming more geographically diversified, with Asia Pacific emerging as an increasingly important market for anaerobic digestion equipment procurement as several countries accelerate the deployment of large-scale facilities through government-supported initiatives. The growing emphasis on energy security has transformed anaerobic digestion from a waste management solution into a critical component of renewable gas production strategies. Regulatory efforts aimed at reducing organic waste disposal in landfills continue to generate sustained demand for anaerobic digestion systems. Across major regions, including Europe, North America, and Asia Pacific, supportive policy frameworks are providing greater long-term market visibility. Despite favorable fundamentals, project financing remains complex due to the multiple revenue streams associated with anaerobic digestion operations, each carrying different risk characteristics and contractual structures. To address these challenges, project stakeholders are increasingly adopting long-term renewable gas supply agreements, integrated engineering and operational service models, and utility partnerships that help reduce project risks and improve financing prospects.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $11.5 Billion |

| Forecast Value | $26 Billion |

| CAGR | 8.5% |

The agricultural residues segment accounted for 22% share in 2025 and is expected to grow at a CAGR of 7.7% through 2035. The segment maintains a leading position due to the abundant availability of biomass resources generated from agricultural activities and agro-processing operations. These feedstocks are highly compatible with widely deployed anaerobic digestion technologies and continue to support the expansion of both commercial and industrial-scale facilities. Growing efforts to maximize resource utilization and improve renewable energy generation from agricultural waste streams are expected to sustain demand for equipment designed to process these materials efficiently.

The energy and utilities segment held an 18% share in 2025 and is projected to grow at a CAGR of 8.6% through 2035. The segment includes facilities dedicated to renewable gas production, power generation, and integrated waste-to-energy operations. Increasing investment in renewable energy infrastructure, combined with rising demand for low-carbon energy solutions, is driving the adoption of advanced anaerobic digestion technologies across utility-scale projects. The growing focus on decarbonization and energy diversification is expected to further strengthen the segment's growth outlook over the forecast period.

North America Anaerobic Digestion Equipment Market accounted for 27% share in 2025 and is anticipated to grow at a CAGR of 7.5% through 2035. The United States remains the largest contributor to regional demand, supported by increasing investments in renewable natural gas production, waste management modernization, and clean energy infrastructure. Favorable regulatory initiatives aimed at reducing carbon emissions and improving renewable fuel adoption continue to create attractive opportunities for market participants. Ongoing investments in biogas upgrading technologies, waste-to-energy projects, and agricultural waste processing facilities are expected to support long-term market growth throughout the region.

Major companies operating in the global anaerobic digestion equipment market include Veolia, SUEZ Group, Xylem, Anaergia Inc., EnviTec Biogas, Weltec Biopower GmbH, Nature Energy Biogas, and Andritz. Companies operating in the anaerobic digestion equipment market are implementing several strategic initiatives to strengthen their competitive position and expand market share. Key strategies include investing in advanced digestion technologies that improve operational efficiency, biomethane yields, and overall system performance. Market participants are increasingly focusing on integrated solutions that combine engineering, procurement, construction, and long-term operational services to provide end-to-end project support. Strategic collaborations with utilities, municipalities, agricultural operators, and industrial facilities are helping companies secure long-term contracts and expand their customer base. In addition, businesses are increasing investments in research and development to enhance feedstock flexibility and optimize renewable gas production.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Feedstock trends

- 2.1.3 Equipment trends

- 2.1.4 Technology trends

- 2.1.5 Application trends

- 2.1.6 End use trends

- 2.1.7 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Anaerobic digestion process & equipment ecosystem analysis

- 3.2.1 AD process stages & equipment mapping

- 3.2.2 Value chain analysis

- 3.2.3 Ecosystem Participant roles & margin distribution

- 3.3 Technology & innovation landscape

- 3.3.1 Emerging digester configurations

- 3.3.2 Biogas upgrading technology advances

- 3.3.3 Smart digester & IoT-enabled monitoring innovations

- 3.3.4 Co-digestion technology advances & multi-feedstock systems

- 3.4 Regulatory landscape

- 3.4.1 Renewable energy directives & biogas incentive policies (EU RED III, US IRA)

- 3.4.2 Waste management & organic waste diversion regulations

- 3.4.3 Biosolids (Digestate) land application standards

- 3.4.4 Carbon credits, REC schemes & biomethane certification frameworks

- 3.4.5 Regional regulatory framework

- 3.5 Industry impact forces

- 3.5.1 Growth drivers

- 3.5.1.1 Increasing demand for renewable energy generation and waste-to-energy solutions

- 3.5.1.2 Rising focus on organic waste management and reduction of landfill usage

- 3.5.1.3 Supportive government policies, incentives, and sustainability targets promoting biogas

- 3.5.2 Industry pitfalls and challenges

- 3.5.2.1 High initial capital investment and complex project financing

- 3.5.2.2 Permitting timelines and feedstock supply reliability

- 3.5.3 Market opportunities

- 3.5.3.1 Integration of AI and data analytics in diabetes management

- 3.5.3.2 Expansion of remote patient monitoring (RPM) and telehealth

- 3.5.1 Growth drivers

- 3.6 Growth potential analysis

- 3.7 Porter's analysis

- 3.7.1 Bargaining power of suppliers

- 3.7.2 Bargaining power of buyers

- 3.7.3 Threat of new entrants

- 3.7.4 Threat of substitute

- 3.7.5 Intensity of competitive rivalry

- 3.8 PESTEL analysis

- 3.8.1 Political factors

- 3.8.2 Economic factors

- 3.8.3 Social factors

- 3.8.4 Technological factors

- 3.8.5 Environmental factors

- 3.8.6 Legal factors

- 3.9 Impact of AI and Generative AI on the market (Driven by primary research)

- 3.9.1 AI-Driven disruption of existing digester operations & design models

- 3.9.2 GenAI use cases & adoption roadmap

- 3.9.3 Risks, limitations & regulatory considerations for AI in biogas facilities

- 3.10 Capacity & Production Landscape (Driven by Primary Research)

- 3.10.1 Installed AD capacity by region

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Key developments

- 4.3.1 Key partnerships & collaborations

- 4.3.2 Major M&A activities

- 4.3.3 Product innovations & launches

- 4.3.4 Market expansion strategies

- 4.4 Competitive positioning matrix

Chapter 5 Market Size and Forecast, By Feedstock, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Agricultural Residues

- 5.3 Food Waste

- 5.4 Animal Manure

- 5.5 Municipal Solid Waste

- 5.6 Industrial Waste

- 5.7 Sewage Sludge

- 5.8 Energy Crops

- 5.9 Others

Chapter 6 Market Size and Forecast, By Equipment, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Feedstock pretreatment

- 6.3 Digestors/reactors systems

- 6.4 Biogas handling & storage

- 6.5 Biogas upgrading

- 6.6 CHP & power generation equipment

- 6.7 Digestate processing

- 6.8 Monitoring & control systems

- 6.9 Others

Chapter 7 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Wet anaerobic digestion

- 7.3 Dry anaerobic digestion

- 7.4 Two-phase anaerobic digestion

- 7.5 Batch anaerobic digestion

- 7.6 Others

Chapter 8 Market Size and Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Power generation (Electricity Only)

- 8.3 CHP

- 8.4 Biomethane

- 8.5 Biofertilizer production

- 8.6 Wastewater treatment

- 8.7 Others

Chapter 9 Market Size and Forecast, By End Use, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Agriculture

- 9.3 Municipal & wastewater treatment

- 9.4 Energy & utilities

- 9.5 Food & beverages

- 9.6 Chemical industry

- 9.7 Pharmaceutical industry

- 9.8 Waste management

- 9.9 Others

Chapter 10 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Netherlands

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Indonesia

- 10.4.5 Australia

- 10.5 Middle East & Africa

- 10.5.1 Saudi Arabia

- 10.5.2 UAE

- 10.5.3 South Africa

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Argentina

Chapter 11 Company Profiles

- 11.1 2G Energy

- 11.2 Anaergia

- 11.3 Andritz

- 11.4 BioFerm Energy Systems

- 11.5 BTA International GmbH

- 11.6 BTS Biogas

- 11.7 Clarke Energy

- 11.8 DVO

- 11.9 Eisenmann

- 11.10 EnviTec Biogas

- 11.11 Hitachi Zosen

- 11.12 Nature Energy Biogas

- 11.13 Paques

- 11.14 PlanET Biogas Group

- 11.15 Qila Energy

- 11.16 SUEZ Group

- 11.17 Veolia

- 11.18 Weltec Biopower GmbH

- 11.19 Xylem