|

시장보고서

상품코드

2071195

군용 항공기용 아비오닉스 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2026-2035년)Military Aircraft Avionics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

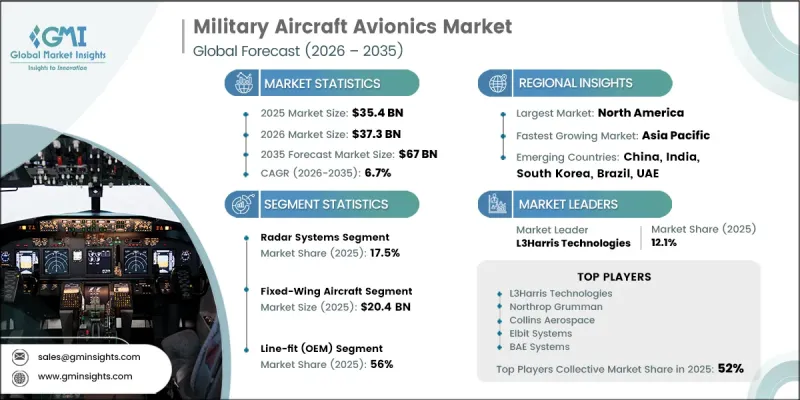

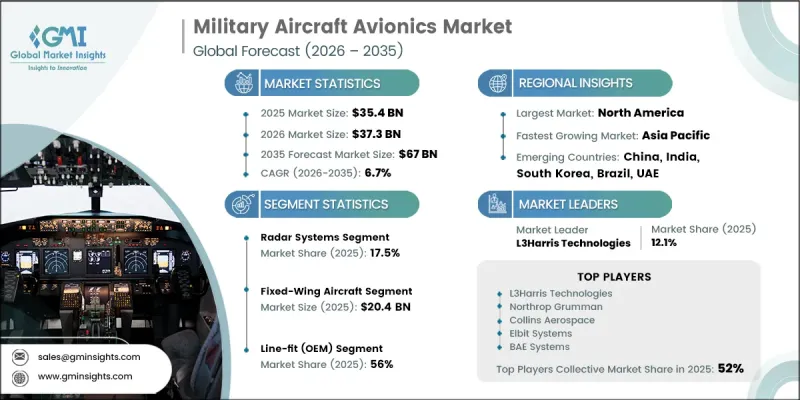

세계의 군용 항공기용 아비오닉스 시장은 2025년에 354억 달러 규모에 달하고, CAGR 6.7%로 성장하여 2035년까지 670억 달러에 달할 것으로 추정됩니다.

전 세계 군용 항공기용 아비오닉스 산업은 군용 항공기 함대의 작전 효율 향상을 목표로 한 대규모 현대화 계획에 힘입어 성장하고 있습니다. 전 세계의 국방 기관들은 임무 수행 능력, 운용 안전성 및 전투 준비 태세를 향상시키기 위해 첨단 항공전자 기술에 대한 투자를 확대하고 있습니다. 통합형 센서 플랫폼, 상황 인식 능력 강화, 안전한 통신 인프라 및 네트워크 기반 운영 프레임워크에 대한 수요가 증가함에 따라 시장 확대가 지속적으로 촉진되고 있습니다. 차세대 전투기, 무인항공기 시스템 및 디지털로 연결된 군사 플랫폼의 배치 확대는 첨단 항공전자 아키텍처에 대한 수요를 더욱 가속화하고 있습니다. 또한, 전자전 대응 능력, 고장 내성이 뛰어난 항법 기술, 상호 운용이 가능한 임무 시스템에 대한 중요성이 커지고 있는 점도 첨단 항공전자 솔루션의 조달을 뒷받침하고 있습니다. 군에서 정보 우위와 실시간 전장 연결성을 우선시하는 가운데, 항공전자 시스템은 선진국 및 신흥국의 방위 시장을 막론하고 방위 항공 자산의 현대화 과정에서 점점 더 핵심적인 역할을 수행하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 354억 달러 |

| 예측 금액 | 670억 달러 |

| CAGR | 6.7% |

전 세계 군용 항공기용 아비오닉스 장비 시장은 세계 각국 공군에서 운용 중인 노후화된 항공기들을 현대화하려는 지속적인 수요에 힘입어 성장하고 있습니다. 현재 운용 중인 군용기의 상당 부분은 기존의 구형 항공전자 기술에 의존하고 있어, 진화하는 운용 요건을 충족하기 위해서는 이를 교체하거나 기능을 강화해야 합니다. 이러한 추세에 따라, 업그레이드된 임무 관리 시스템, 항법 기술, 비행 제어 솔루션 및 통신 인프라에 대한 지속적인 수요가 발생하고 있습니다. 또한, 전자전 능력과 보안 통신 네트워크에 대한 투자 증가는 항공전자 장비 제조업체들에게 계속해서 비즈니스 기회를 창출하고 있습니다. 방위 기관들은 고도화된 위협 탐지, 신호 관리, 생존성 향상 및 운용상의 회복력에 점점 더 중점을 두고 있으며, 이는 기존 및 신규 배치 군용기 모두에 더욱 정교한 항공전자 플랫폼의 통합을 촉진하고 있습니다.

감시·정찰 시스템 분야는 2026년부터 2035년까지 연평균 성장률(CAGR) 9.2%로 성장할 것으로 예상됩니다. 이 부문의 성장은 유인 및 무인항공기 플랫폼 모두에서 공중 정보·감시·정찰 능력 강화에 초점을 맞춘 국방 투자 증가에 힘입어 이루어지고 있습니다. 첨단 감지 기술, 통합 데이터 수집 시스템 및 실시간 감시 기능이 점점 더 다양한 군사 항공 자산에 탑재되고 있습니다. 지속적인 정보 수집, 목표 식별, 작전 상황 인식 및 임무 지원 기능의 중요성이 높아짐에 따라, 방위 분야 전반에 걸쳐 차세대 감시·정찰용 항공전자 솔루션의 도입이 가속화되고 있습니다.

2025년, 고정익 항공기 부문의 시장 규모는 204억 달러에 달했습니다. 이 부문이 주도적인 위치를 차지하고 있는 배경에는 군용 고정익 플랫폼과 관련된 광범위한 항공전자 장비 요구 사항이 있습니다. 이러한 항공기에는 일반적으로 임무 관리 기술, 레이더 솔루션, 통신 네트워크, 항법 장치, 전자전 능력, 조종석 디스플레이 인터페이스 등 광범위한 첨단 시스템이 탑재되어 있습니다. 플랫폼당 탑재되는 항공전자 장비의 양이 매우 많기 때문에 다른 항공기 범주와 비교했을 때 조달 비용이 대폭 증가합니다. 또한, 규모가 각기 다른 군사 조직 전반에 걸쳐 고정익 항공기가 널리 배치되어 있기 때문에 전 세계 주요 방위 시장에서 항공전자 장비의 업그레이드, 교체 및 신규 시스템 도입에 대한 수요가 꾸준히 유지되고 있습니다.

2025년, 북미 군용 항공기용 아비오닉스 장비 시장은 38.1%의 점유율을 차지했습니다. 이 지역은 세계에서 가장 선진적인 방위 항공 인프라 중 하나를 자랑하며, 주요 항공전자 장비 제조업체들의 강력한 입지, 풍부한 군용기 보유 대수, 그리고 현대화 프로그램에 중점을 둔 지속적인 국방 지출에 힘입어 성장하고 있습니다. 첨단 항공 역량, 디지털 전투 기술, 그리고 차세대 항공우주 플랫폼에 대한 지속적인 투자가 해당 지역 시장에서 선도적인 입지를 공고히 하고 있습니다. 기술적으로 선진적인 군용 항공 프로그램의 집중과 지속적인 조달 이니셔티브를 통해, 북미는 세계 방위 산업에서 고부가가치 항공전자 시스템의 수요, 혁신 및 도입에 있어 주요 중심지로서의 입지를 계속해서 공고히 하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 시스템 유형별, 2022-2035년

제6장 시장 추정 및 예측 : 항공기 유형별, 2022-2035년

제7장 시장 추정 및 예측 : 피트별, 2022-2035년

제8장 시장 추정 및 예측 : 지역별, 2022-2035년

제9장 기업 개요

KSM 26.07.03The Global Military Aircraft Avionics Market was valued at USD 35.4 billion in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 67 billion by 2035.

Growth across the global military aircraft avionics industry is fueled by extensive modernization initiatives aimed at enhancing the operational effectiveness of military aviation fleets. Defense organizations worldwide are investing in advanced avionics technologies to improve mission performance, operational safety, and combat readiness. Increasing demand for integrated sensor platforms, enhanced situational awareness capabilities, secure communications infrastructure, and network-enabled operational frameworks continues to support market expansion. The rising deployment of next-generation fighter aircraft, unmanned aerial systems, and digitally connected military platforms is further accelerating demand for sophisticated avionics architectures. In addition, growing emphasis on electronic warfare readiness, resilient navigation technologies, and interoperable mission systems is encouraging procurement of advanced avionics solutions. As military forces prioritize information superiority and real-time battlefield connectivity, avionics systems are becoming increasingly central to the modernization of defense aviation assets across developed and emerging defense markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $35.4 Billion |

| Forecast Value | $67 Billion |

| CAGR | 6.7% |

The global Military Aircraft Avionics Market is driven by the ongoing need to modernize aging aircraft fleets operating within air forces around the world. A significant share of military aircraft currently in service relies on legacy avionics technologies that require replacement or enhancement to meet evolving operational requirements. This trend is generating sustained demand for upgraded mission management systems, navigation technologies, flight control solutions, and communication infrastructure. Furthermore, increasing investments in electronic warfare capabilities and protected communication networks continue to create opportunities for avionics manufacturers. Defense agencies are placing greater emphasis on advanced threat detection, signal management, survivability enhancement, and operational resilience, which is driving the integration of more sophisticated avionics platforms into both existing and newly deployed military aircraft.

The surveillance and reconnaissance systems segment is expected to grow at a CAGR of 9.2% during 2026-2035. Growth within this category is being supported by rising defense investments focused on strengthening airborne intelligence, surveillance, and reconnaissance capabilities across both manned and unmanned aircraft platforms. Advanced sensing technologies, integrated data collection systems, and real-time monitoring capabilities are increasingly being incorporated into a wider range of military aviation assets. The growing importance of persistent intelligence gathering, target identification, operational awareness, and mission support functions is accelerating the adoption of next-generation surveillance and reconnaissance avionics solutions throughout the defense sector.

The fixed-wing aircraft segment accounted for USD 20.4 billion in 2025. The segment's leadership position is supported by the extensive avionics requirements associated with fixed-wing military platforms. These aircraft typically incorporate a broad range of advanced systems, including mission management technologies, radar solutions, communication networks, navigation equipment, electronic warfare capabilities, and cockpit display interfaces. The high concentration of avionics content per platform significantly increases procurement value compared to other aircraft categories. Additionally, the widespread deployment of fixed-wing fleets across military organizations of varying sizes ensures consistent demand for avionics upgrades, replacements, and new system installations across major defense markets worldwide.

North America Military Aircraft Avionics Market held a 38.1% share in 2025. The region benefits from one of the world's most advanced defense aviation infrastructures, supported by a strong presence of leading avionics manufacturers, extensive military aircraft inventories, and sustained defense expenditures focused on modernization programs. Continuous investment in advanced aviation capabilities, digital warfare technologies, and next-generation aerospace platforms reinforces regional market leadership. The concentration of technologically advanced military aviation programs and ongoing procurement initiatives continues to position North America as a major center for demand, innovation, and deployment of high-value avionics systems within the global defense industry.

Key companies operating in the Global Military Aircraft Avionics Market include RTX Corporation, Collins Aerospace, L3Harris Technologies, Northrop Grumman, Thales Group, Elbit Systems, Safran Electronics & Defense, BAE Systems, Leonardo S.p.A., Saab AB, Lockheed Martin, Israel Aerospace Industries (IAI), Mercury Systems, Curtiss-Wright, Hensoldt AG, Bharat Electronics Limited (BEL), Aselsan, Honeywell International, and Mitsubishi Electric. Companies operating in the Military Aircraft Avionics Market are strengthening their competitive positions through sustained investments in advanced avionics technologies, digital mission systems, and next-generation electronic warfare capabilities. Strategic partnerships with defense agencies, aircraft manufacturers, and system integrators remain a key approach for securing long-term contracts and expanding market presence. Market participants are increasingly focusing on developing modular, interoperable, and software-driven avionics architectures that support evolving military requirements and platform modernization initiatives. Significant resources are also being directed toward research and development to enhance sensor integration, cybersecurity capabilities, mission computing performance, and secure communications technologies.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 System type trends

- 2.2.2 Aircraft type trends

- 2.2.3 Fit trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing modernization and upgrade of legacy military aircraft fleets

- 3.2.1.2 Rising demand for advanced situational awareness and sensor integration systems

- 3.2.1.3 Growing adoption of network-centric and interoperable avionics architectures

- 3.2.1.4 Increasing focus on electronic warfare (EW) and secure communication systems

- 3.2.1.5 Expansion of next-generation fighter and unmanned aerial vehicle (UAV) programs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High integration complexity of advanced avionics systems across platforms

- 3.2.2.2 Stringent regulatory and certification requirements for avionics systems

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of advanced digital twin and predictive maintenance systems in military aviation

- 3.2.3.2 Expansion of space-based communication and satellite integration in avionics systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By System Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Flight control & flight management systems

- 5.2.1 Autopilot systems

- 5.2.2 Digital flight control systems (DFCS)

- 5.2.3 Aircraft monitoring systems

- 5.2.4 Others

- 5.3 Communication systems

- 5.3.1 Military tactical radios

- 5.3.2 Secure communication systems (COMSEC)

- 5.3.3 Satellite communication (SATCOM) terminals

- 5.3.4 Cockpit communication systems

- 5.3.5 Others

- 5.4 Navigation systems

- 5.4.1 Global navigation satellite systems (GNSS/GPS)

- 5.4.2 Inertial navigation systems (INS)

- 5.4.3 Integrated GPS/INS & multi-sensor navigation

- 5.4.4 Others

- 5.5 Surveillance & reconnaissance systems

- 5.5.1 Electro-optical/infrared (EO/IR) sensor systems

- 5.5.2 Airborne surveillance & ISR collection systems

- 5.5.3 Others

- 5.6 Radar systems

- 5.6.1 Maritime surveillance radar

- 5.6.2 Active electronically scanned array (AESA) radar

- 5.6.3 Synthetic aperture radar (SAR)

- 5.6.4 Others

- 5.7 Mission computers & embedded electronics

- 5.7.1 Mission processors & avionics computers

- 5.7.2 Data processing & bus management systems

- 5.7.3 Embedded mission electronics

- 5.7.4 Others

- 5.8 Cockpit & display systems

- 5.8.1 Head-up displays (HUD)

- 5.8.2 Multifunction displays (MFD)

- 5.8.3 Helmet-mounted displays & sights (HMD/HMS)

- 5.8.4 Others

- 5.9 Electronic warfare systems

- 5.9.1 Radar warning receivers (RWR)

- 5.9.2 Electronic countermeasure (ECM) systems

- 5.9.3 Electronic support measures (ESM)

- 5.9.4 Directed infrared countermeasures (DIRCM)

- 5.9.5 Others

- 5.10 Health monitoring & diagnostic systems

- 5.11 Avionics integration & upgrade services

- 5.12 Others

Chapter 6 Market Estimates and Forecast, By Aircraft Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Fixed-wing aircraft

- 6.2.1 Fighter & multirole combat aircraft (4th generation)

- 6.2.2 5th generation stealth fighter aircraft

- 6.2.3 Military transport & airlifter aircraft

- 6.2.4 Maritime patrol aircraft (MPA)

- 6.2.5 Others

- 6.3 Rotary-wing aircraft (military helicopters)

- 6.3.1 Attack helicopters

- 6.3.2 Special operations helicopters

- 6.3.3 Others

- 6.4 Unmanned aerial vehicles (UAVs/UAS)

- 6.4.1 Combat UAVs

- 6.4.2 High-altitude long-endurance (HALE) surveillance UAVs

- 6.4.3 Medium-altitude long-endurance (MALE) UAVs

- 6.4.4 Tactical & mini UAVs

- 6.4.5 Others

Chapter 7 Market Estimates and Forecast, By Fit, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Line-fit (OEM)

- 7.3 Retrofit / aftermarket

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 L3Harris Technologies

- 9.1.2 Northrop Grumman

- 9.1.3 Collins Aerospace

- 9.1.4 Elbit Systems

- 9.1.5 BAE Systems

- 9.2 Regional key players

- 9.2.1 North America

- 9.2.1.1 RTX Corporation

- 9.2.1.2 Lockheed Martin

- 9.2.1.3 Mercury Systems

- 9.2.1.4 Curtiss-Wright

- 9.2.1.5 Honeywell International

- 9.2.2 Asia Pacific

- 9.2.2.1 Bharat Electronics Limited (BEL)

- 9.2.2.2 Mitsubishi Electric Corporation

- 9.2.3 Europe

- 9.2.3.1 Thales Group

- 9.2.3.2 Safran Electronics & Defense

- 9.2.3.3 Leonardo S.p.A.

- 9.2.3.4 Saab AB

- 9.2.3.5 HENSOLDT AG

- 9.2.4 Middle East & Africa

- 9.2.4.1 Israel Aerospace Industries (IAI)

- 9.2.4.2 Aselsan

- 9.2.1 North America