|

시장보고서

상품코드

2071203

수요반응 시장 : 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Demand Response Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

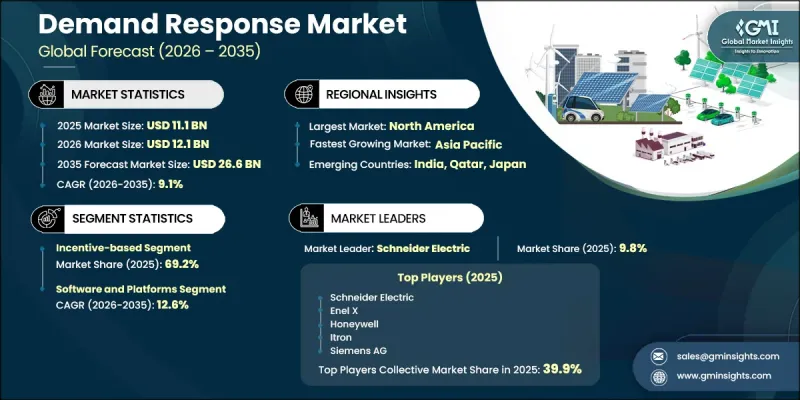

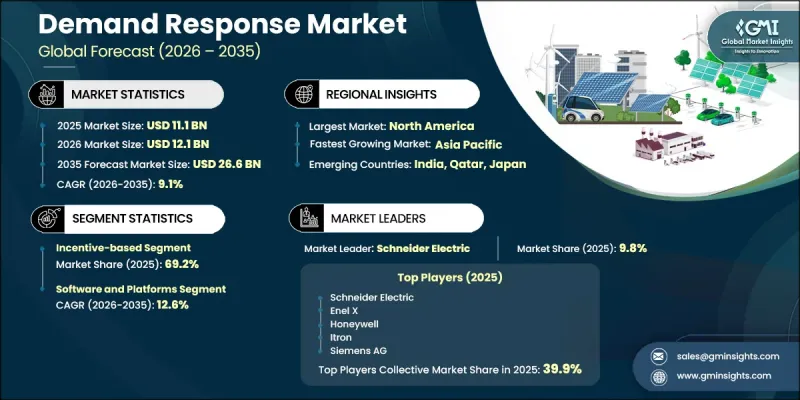

세계 수요반응 시장은 2025년에 111억 달러 규모가 되어, CAGR 9.1%로 성장하여 2035년까지 266억 달러에 이를 것으로 추정되고 있습니다.

이러한 성장은 에너지 공급 사업자들이 전력망 전반에 걸쳐 더 높은 유연성, 효율성, 신뢰성을 추구하는 가운데, 현대 전력 시스템이 지속적으로 변화하고 있음을 반영하고 있습니다. 프로그램 참여 현황을 살펴보면, 상업 및 산업 부문의 소비자가 여전히 가장 큰 비중을 차지하고 있지만, 연결형 에너지 관리 기술과 첨단 에너지 집계 솔루션의 보급이 확대됨에 따라 주거 부문에서의 도입도 탄력을 받고 있습니다. IoT 지원 플랫폼과 인공지능(AI) 기반 최적화 도구의 도입으로, 기존 수요 관리 방식을 대체하는 주목할 만한 업계의 변화가 진행되고 있습니다. 그 결과, 수요반응은 단순히 에너지 비용을 절감할 뿐만 아니라 경제적 가치를 창출할 수 있는 전략적 전력망 자원으로서 점점 더 널리 인식되고 있습니다. 수요반응 이니셔티브에 참여하면 소비자에게 측정 가능한 경제적 이익을 가져다주고, 전기 요금 절감에 기여할 뿐만 아니라 새로운 수익 기회를 창출합니다. 그러나 이를 도입하려면 고도의 계측 시스템, 자동 제어, 통신 기술 및 지원 인프라에 대한 투자가 필요한 경우가 많아, 스마트 에너지 기반이 충분히 갖춰지지 않은 조직의 경우 재정적인 부담이 될 수 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 111억 달러 |

| 예측 금액 | 266억 달러 |

| CAGR | 9.1% |

인센티브형 수요반응(IBDR) 부문은 2025년에 69.2%의 시장 점유율을 차지했습니다. 이러한 프로그램에서 참가자들은 전력 계통에 부하가 걸리는 시기나 수요 피크 시간대에 전력 소비를 줄이거나 시간대를 조정하는 대가로 금전적 보상을 받습니다. 보상 체계에는 직접적인 인센티브, 실적에 따른 지급, 또는 전기 요금 할인 등이 포함됩니다. 이 부문은 상당한 부하 조정 능력을 갖춘 대규모 전력 소비자의 적극적인 참여에 힘입어 계속해서 주도적인 위치를 유지하고 있으며, 인센티브형 수요반응은 현대 전력 계통 관리 전략에서 중요한 요소로 자리 잡고 있습니다.

가격 연동형 수요반응(PBDR) 부문은 2025년에 30.8%의 시장 점유율을 차지했습니다. 이러한 성장은 주택 및 상업 고객 부문 전반에 걸쳐 역동적인 전력 가격 책정 모델의 도입이 확대되고 있는 데 기인합니다. 이러한 프로그램은 가격 신호의 변화에 따라 소비자가 전력 사용 패턴을 조정하도록 유도함으로써, 전력 회사의 직접적인 개입 없이도 보다 효율적인 에너지 소비를 가능하게 합니다. 이 부문은 첨단 계량 인프라(AMI)의 지속적인 도입으로 큰 혜택을 보고 있으며, 이를 통해 전력 회사는 정교한 요금 체계를 도입하고 실시간 에너지 관리 기능을 통해 고객 참여도를 높일 수 있습니다.

유럽 수요반응 시장은 2025년에 15%의 시장 점유율을 차지하고, 2035년까지 연평균 성장률(CAGR) 9.8%로 성장할 것으로 전망됩니다. 해당 지역은 시장 진출기업을 장려하고, 상호 운용성을 향상시키며, 표준화된 운영 체계를 확립하기 위한 지원적인 규제 동향의 혜택을 계속해서 누리고 있습니다. 시장의 접근성, 참여 자격 요건, 데이터 공유 프로토콜에 초점을 맞춘 최근의 정책 이니셔티브는 수요반응 사업자와 에너지 애그리게이터가 보다 통합된 환경을 구축하는 데 기여하고 있습니다. 이러한 추세는 지역 전력 시장 전반에 걸쳐 더 광범위한 도입을 촉진하는 동시에, 업계의 장기적인 성장과 송전망 현대화를 위한 노력을 뒷받침할 것으로 기대됩니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 규모 및 예측 : 서비스 유형별, 2022-2035년

제6장 시장 규모 및 예측 : 기술별, 2022-2035년

제7장 시장 규모 및 예측 : 컴포넌트별, 2022-2035년

제8장 시장 규모 및 예측 : 전개 형태별, 2022-2035년

제9장 시장 규모 및 예측 : 커뮤니케이션별, 2022-2035년

제10장 시장 규모 및 예측 : 용도별, 2022-2035년

제11장 시장 규모 및 예측 : 최종 사용자별, 2022-2035년

제12장 시장 규모 및 예측 : 지역별, 2022-2035년

제13장 기업 개요

JHS 26.07.01The Global Demand Response Market was valued at USD 11.1 billion in 2025 and is estimated to grow at a CAGR of 9.1% to reach USD 26.6 billion by 2035.

The growth reflects the ongoing transformation of modern power systems as energy providers seek greater flexibility, efficiency, and reliability across electricity networks. Commercial and industrial consumers continue to represent the largest share of program participation, while residential adoption is gaining momentum due to the wider availability of connected energy management technologies and advanced energy aggregation solutions. A notable industry shift is occurring through the adoption of IoT-enabled platforms and artificial intelligence-based optimization tools, which are replacing traditional demand management approaches. As a result, demand response is increasingly being viewed as a strategic grid resource capable of generating economic value rather than solely reducing energy costs. Participation in demand response initiatives offers measurable financial benefits to consumers, helping reduce electricity expenses while creating additional revenue opportunities. However, implementation often requires investment in advanced metering systems, automated controls, communication technologies, and supporting infrastructure, which can present financial challenges for organizations without established smart energy foundations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $11.1 Billion |

| Forecast Value | $26.6 Billion |

| CAGR | 9.1% |

The incentive-based demand response (IBDR) segment held a 69.2% share in 2025. Under these programs, participants receive financial compensation in exchange for reducing or shifting electricity consumption during periods of grid stress or peak demand. Compensation mechanisms may include direct incentives, performance-based payments, or energy bill benefits. The segment continues to maintain its leading position due to strong participation from large-scale energy consumers capable of delivering substantial load flexibility, making incentive-based demand response an important component of modern grid management strategies.

The price-based demand response (PBDR) segment held a 30.8% share in 2025. Growth is driven by the expanding adoption of dynamic electricity pricing models across residential and commercial customer segments. These programs encourage consumers to modify electricity usage patterns in response to changing price signals, enabling more efficient energy consumption without direct intervention from utilities. The segment benefits significantly from the continued rollout of advanced metering infrastructure, which allows utilities to implement sophisticated pricing structures and improve customer engagement through real-time energy management capabilities.

Europe Demand Response Market accounted for 15% share in 2025 and is forecast to grow at a CAGR of 9.8% through 2035. The region continues to benefit from supportive regulatory developments designed to enhance market participation, improve interoperability, and establish standardized operating frameworks. Recent policy initiatives focused on market accessibility, qualification requirements, and data-sharing protocols are helping create a more integrated environment for demand response providers and energy aggregators. These developments are expected to facilitate broader adoption across regional electricity markets while supporting long-term industry expansion and grid modernization efforts.

Key companies operating in the Global Demand Response Industry include Eaton, Oracle Utilities, ABB, Next Kraftwerke, Honeywell, Schneider Electric, GE Vernova, Enel X, Landis+Gyr, Tesla Energy, Siemens AG, Johnson Controls, Centrica Business Solutions, Uplight, and Itron. Leading participants in the demand response market are adopting a variety of strategies to strengthen their competitive position and expand market share. Companies are investing heavily in advanced software platforms, artificial intelligence capabilities, predictive analytics, and cloud-based energy management solutions to enhance operational efficiency and customer value. Strategic partnerships with utilities, technology providers, and energy service organizations are helping businesses broaden their market reach and accelerate solution deployment. Many firms are also pursuing acquisitions and regional expansion initiatives to strengthen their customer base and diversify service offerings. Investments in smart grid integration, distributed energy resource management, and virtual power plant technologies continue to support innovation across the sector.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Service type trends

- 2.4 Technology trends

- 2.5 Components trends

- 2.6 Deployment trends

- 2.7 Communication trends

- 2.8 Application trends

- 2.9 End user trends

- 2.10 Region trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.2.1 North America

- 3.2.2 Europe

- 3.2.3 Asia Pacific

- 3.2.4 Middle East & Africa

- 3.2.5 Latin America

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Impact of AI & generative AI on the market

- 3.7.1 Predictive maintenance & fault detection

- 3.7.2 Grid optimization & load forecasting

- 3.7.3 Digital twin simulation & testing

- 3.7.4 Risks, limitations & regulatory considerations

- 3.8 Emerging opportunities & trends

- 3.8.1 Digitalization & IoT integration

- 3.8.2 Emerging market penetration

- 3.9 Overall investment scenario and future outlook

Chapter 4 Competitive landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Service type, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Incentive-based DR

- 5.3 Price-based DR

Chapter 6 Market Size and Forecast, By Technology, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 Advanced metering infrastructure (AMI)

- 6.3 Energy management systems (EMS)

- 6.4 Automated demand response (ADR)

- 6.5 Smart thermostats & HVAC control

- 6.6 IoT & AI-based DR platforms

- 6.7 Virtual power plant (VPP) platforms

- 6.8 Others

Chapter 7 Market Size and Forecast, By Component, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 Software & platforms

- 7.3 Hardware

- 7.4 Services

Chapter 8 Market Size and Forecast, By Deployment, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 Cloud-based

- 8.3 On-premises

- 8.4 Hybrid

Chapter 9 Market Size and Forecast, By Communication, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 Wired

- 9.3 Wireless

Chapter 10 Market Size and Forecast, By Application, 2022 - 2035 (USD Billion)

- 10.1 Key trends

- 10.2 Peak load management

- 10.3 Grid reliability & scalability

- 10.4 Energy cost optimization

- 10.5 Renewable integration

- 10.6 Ancillary services & frequency reg.

- 10.7 Others

Chapter 11 Market Size and Forecast, By End user, 2022 - 2035 (USD Billion)

- 11.1 Key trends

- 11.2 Industrial

- 11.3 Commercial

- 11.4 Residential

- 11.5 Utilities

Chapter 12 Market Size and Forecast, By Region, 2022 - 2035 (USD Billion)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 UK

- 12.3.2 Germany

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 South Korea

- 12.4.3 Japan

- 12.4.4 India

- 12.4.5 Australia

- 12.4.6 Southeast Asia

- 12.5 Middle East & Africa

- 12.5.1 Saudi Arabia

- 12.5.2 UAE

- 12.5.3 Qatar

- 12.5.4 South Africa

- 12.6 Latin America

- 12.6.1 Brazil

- 12.6.2 Mexico

- 12.6.3 Argentina

Chapter 13 Company Profiles

- 13.1 ABB

- 13.2 Centrica Business Solutions

- 13.3 CPower Energy Management

- 13.4 Eaton

- 13.5 Enel X

- 13.6 EnergyHub

- 13.7 GE Vernova

- 13.8 Honeywell

- 13.9 Itron

- 13.10 Johnson Controls

- 13.11 Landis+Gyr

- 13.12 Leap

- 13.13 Next Kraftwerke

- 13.14 OhmConnect

- 13.15 Oracle Utilities

- 13.16 Schneider Electric

- 13.17 Siemens AG

- 13.18 Tesla Energy

- 13.19 Uplight

- 13.20 Voltus Inc.