|

시장보고서

상품코드

2071242

중장비 텔레매틱스 시장 : 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Heavy Equipment Telematics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

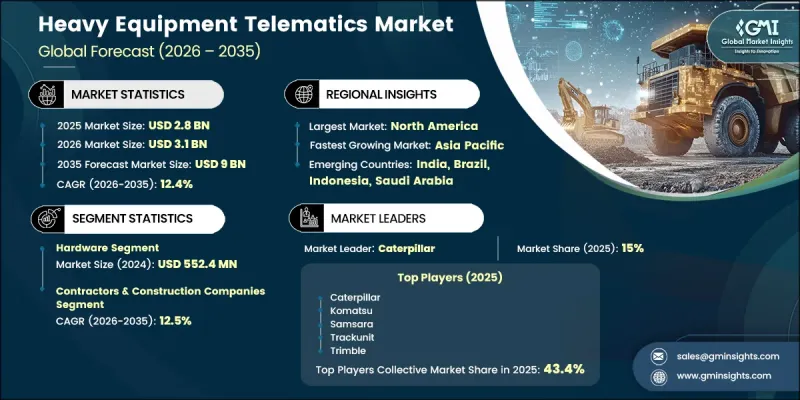

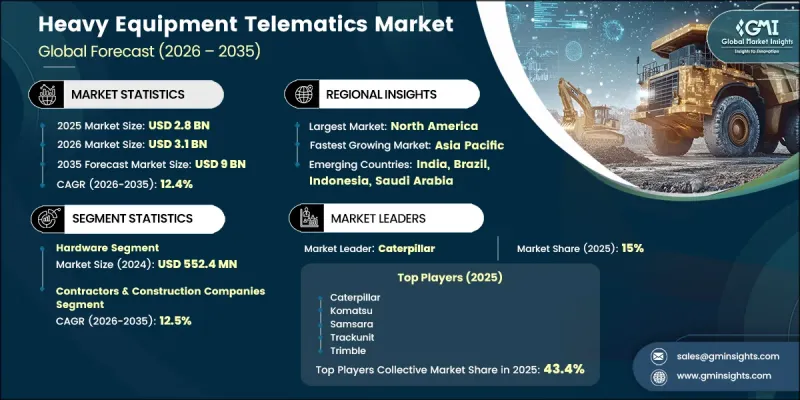

세계 중장비 텔레매틱스 시장은 2025년에 28억 달러 규모가 되어, 2035년까지 연평균 복합 성장률(CAGR) 12.4%로 성장하여 90억 달러에 이를 것으로 추정되고 있습니다.

시장 확대는 커넥티드 기기 기술의 보급 확대, 규제 감독 강화, 그리고 건설, 광업, 인프라, 산업 분야에서의 실시간 차량 정보에 대한 수요 증가에 힘입어 이루어지고 있습니다. 기업들은 자산 가동률 향상, 장비 성능 최적화, 가동 중단 시간 단축, 그리고 예측 유지보수 전략 지원을 위해 텔레매틱스 플랫폼에 대한 의존도를 높이고 있습니다. 여러 지역에서 대규모 인프라 투자가 이어지는 가운데, 장비의 가동 상황을 시각화하는 것은 더 이상 경쟁 우위라기보다는 필수적인 요건이 되었습니다. 배출가스 모니터링, 운영 보고, 작업장 안전에 관한 규제 요건 역시 텔레매틱스 솔루션의 도입을 가속화하고 있습니다. 커넥티드 시스템은 자동 데이터 수집, 위치 추적, 가동 상태 모니터링 및 운영자 성과 분석을 제공하여, 조직이 규정 준수 절차를 간소화하고 운영 효율성을 높이는 데 도움을 줍니다. 또한, 작업장 안전, 장비 관리 책임 및 디지털 차량 관리에 대한 중요성이 커짐에 따라, 첨단 텔레매틱스 기술에 대한 수요가 더욱 증가하고 있습니다. 기업들이 생산성 향상과 운영 비용 절감을 동시에 도모하려는 가운데, 텔레매틱스 솔루션은 전 세계 중장비 차량 관리 전략에서 점점 더 중요한 요소로 자리 잡고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 28억 달러 |

| 예측 금액 | 90억 달러 |

| CAGR | 12.4% |

하드웨어 분야는 2035년까지 연평균 성장률(CAGR) 9.8%를 기록하며 성장할 것으로 전망됩니다. 하드웨어 솔루션에는 텔레매틱스 제어 장치, 위치 추적 장치, 차량 진단 시스템, 통신 게이트웨이, 자산 모니터링 장비, 그리고 가혹한 산업 환경에서의 운용을 염두에 두고 설계된 커넥티드 센서 기술 등이 포함됩니다. 이 분야는 연결성 실현에 있어 여전히 중요한 역할을 하고 있지만, 새로운 기기 플랫폼에 텔레매틱스 기능이 직접 통합되는 추세가 강해지고 있어 성장률은 비교적 완만해지고 있습니다. 신규로 제조되는 기계에 연결 기능이 기본 사양으로 탑재됨에 따라, 시장 수익은 점차 소프트웨어 기반 솔루션 및 구독형 서비스로 전환되고 있습니다.

도급업체 부문은 2035년까지 연평균 성장률(CAGR) 12.5%를 나타낼 것으로 예측되며, 이는 시장 전체의 성장률과 밀접하게 연동되어 있습니다. 도급업체는 텔레매틱스 솔루션의 가장 광범위한 고객 기반을 구성하며, 인프라 개발, 상업용 건축, 주택 프로젝트 및 전문 산업 서비스에 종사하는 조직이 포함됩니다. 차량 가시화, 프로젝트 효율화, 장비 추적 및 자원 최적화에 대한 수요가 증가함에 따라, 이 부문 전반에 걸쳐 텔레매틱스 기술의 적극적인 도입이 계속해서 촉진되고 있습니다.

2025년, 북미 중장비 텔레매틱스 시장은 37.8%의 점유율을 차지했습니다. 이 지역 시장 주도력은 중장비 차량 전체에 걸친 광범위한 디지털화, 클라우드 기반 차량 관리 플랫폼의 높은 보급률, 그리고 운영 성과, 배기가스 관리, 작업장 안전에 관한 확립된 규제 요건에 의해 뒷받침되고 있습니다. 또한, 이 지역은 성숙한 기술 생태계와 커넥티드 기기 솔루션에 대한 적극적인 투자의 혜택을 누리고 있으며, 이러한 요인들이 건설, 광업, 물류 및 산업 분야에서의 텔레매틱스 도입을 지속적으로 주도하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제공별, 2022-2035년

제6장 시장 추산 및 예측 : 용도별, 2022-2035년

제7장 시장 추산 및 예측 : 연결성별, 2022-2035년

제8장 시장 추산 및 예측 : 기기 카테고리별, 2022-2035년

제9장 시장 추산 및 예측 : 판매채널별, 2022-2035년

제10장 시장 추산 및 예측 : 최종 용도별, 2022-2035년

제11장 시장 추산 및 예측 : 지역별, 2022-2035년

제12장 기업 개요

JHS 26.07.01The Global Heavy Equipment Telematics Market was valued at USD 2.8 billion in 2025 and is estimated to grow at a CAGR of 12.4% to reach USD 9 billion by 2035.

Market expansion is fueled by the growing adoption of connected equipment technologies, increasing regulatory oversight, and rising demand for real-time fleet intelligence across construction, mining, infrastructure, and industrial operations. Businesses are increasingly relying on telematics platforms to improve asset utilization, optimize equipment performance, reduce downtime, and support predictive maintenance strategies. As large-scale infrastructure investments continue across multiple regions, visibility into equipment operations has become an essential requirement rather than a competitive advantage. Regulatory requirements related to emissions monitoring, operational reporting, and workplace safety are also accelerating the deployment of telematics solutions. Connected systems provide automated data collection, location tracking, utilization monitoring, and operator performance insights, helping organizations streamline compliance processes and improve operational efficiency. In addition, growing emphasis on workplace safety, equipment accountability, and digital fleet management is strengthening demand for advanced telematics technologies. As organizations seek to improve productivity while reducing operating costs, telematics solutions are becoming an increasingly important component of heavy equipment fleet management strategies worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.8 Billion |

| Forecast Value | $9 Billion |

| CAGR | 12.4% |

The hardware segment is projected to grow at a CAGR of 9.8% through 2035. Hardware solutions include telematics control units, location tracking devices, onboard diagnostic systems, communication gateways, asset monitoring equipment, and connected sensor technologies designed to operate in demanding industrial environments. While the segment continues to play a critical role in enabling connectivity, its growth rate is comparatively moderate due to the increasing integration of telematics functionality directly into new equipment platforms. As connected capabilities become standard features in newly manufactured machinery, market revenue is gradually shifting toward software-based solutions and subscription-driven service offerings.

The contractor segment is expected to grow at a CAGR of 12.5% through 2035, closely aligned with overall market growth. Contractors constitute the broadest customer base for telematics solutions, encompassing organizations involved in infrastructure development, commercial construction, residential projects, and specialized industrial services. The increasing need for fleet visibility, project efficiency, equipment tracking, and resource optimization continues to support strong adoption of telematics technologies across this segment.

North America Heavy Equipment Telematics Market held a 37.8% share in 2025. Market leadership is supported by widespread digitalization across heavy equipment fleets, high adoption of cloud-based fleet management platforms, and well-established regulatory requirements related to operational performance, emissions management, and workplace safety. The region also benefits from a mature technology ecosystem and strong investment in connected equipment solutions, which continue to drive telematics deployment across construction, mining, logistics, and industrial sectors.

Major companies operating in the global heavy equipment telematics market include Caterpillar, Komatsu, Trackunit, Trimble, Samsara, John Deere, Volvo Construction Equipment, ORBCOMM, Topcon, CalAmp, CNH Industrial, Liebherr, Hitachi Construction Machinery, J C Bamford (JCB), Actia, DSA Daten- und Systemtechnik, MiX Telematics, Machinemax, and DPL Telematics. Companies operating in the heavy equipment telematics market are adopting a range of strategies to strengthen their market position and expand their customer base. Key initiatives include investing in advanced telematics platforms that incorporate artificial intelligence, predictive analytics, remote diagnostics, and real-time fleet monitoring capabilities. Market participants are increasingly focusing on software innovation and subscription-based business models to generate recurring revenue streams and improve customer retention. Strategic partnerships with equipment manufacturers, fleet operators, and technology providers are helping companies enhance solution interoperability and accelerate market penetration. Investments in cloud-based platforms, IoT connectivity, and data analytics are enabling businesses to deliver more comprehensive fleet management solutions.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Offering

- 2.2.3 Application

- 2.2.4 Connectivity

- 2.2.5 Equipment Category

- 2.2.6 Sales Channel

- 2.2.7 End Use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Regulatory Mandates for Emissions Monitoring & Safety Compliance

- 3.2.1.2 Rising Demand for Operational Efficiency & Asset Utilization Optimization

- 3.2.1.3 OEM Integration of Smart Systems & Factory-Installed Telematics

- 3.2.1.4 Growth in Equipment Rental & Leasing Models Requiring Fleet Tracking

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Upfront Deployment Costs & ROI Uncertainty for Small Contractors

- 3.2.2.2 Integration Challenges with Legacy Equipment Lacking Diagnostic Capabilities

- 3.2.3 Market opportunities

- 3.2.3.1 AI-Based Predictive Maintenance Premium Services

- 3.2.3.2 Telematics-as-a-Service

- 3.2.3.3 Integration with Autonomous Equipment & Remote Operation in Hazardous Environments

- 3.2.1 Growth drivers

- 3.3 Technology and innovation landscape

- 3.3.1 Current technological trends

- 3.3.2 Emerging technologies

- 3.4 Growth potential analysis

- 3.5 Pricing Analysis (Driven by Primary Research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 US - OSHA Safety Standards

- 3.6.1.2 US - FCC Equipment Authorization

- 3.6.1.3 Canada - ISED Radio Standards Specifications (RSS)

- 3.6.2 Europe

- 3.6.2.1 EU - General Data Protection Regulation (GDPR)

- 3.6.2.2 EU - Machinery Regulation (EU) 2023/1230

- 3.6.3 Asia Pacific

- 3.6.3.1 China - MIIT Type Approval

- 3.6.3.2 Japan - Radio Law Certification (MIC)

- 3.6.4 LATAM

- 3.6.4.1 Brazil - ANATEL Certification

- 3.6.4.2 Mexico - IFT Homologation

- 3.6.5 MEA

- 3.6.5.1 UAE - TDRA Certification

- 3.6.5.2 Saudi Arabia - CST Type Approval

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis (Driven by Primary Research)

- 3.11 Impact of AI & generative AI on the market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 GenAI use cases & adoption roadmap by segment

- 3.11.3 Risks, limitations & regulatory considerations

- 3.12 Cybersecurity & Functional Safety Analysis

- 3.13 Infrastructure & Deployment Landscape

- 3.13.1 Scalability Constraints & Infrastructure Investment Trends

- 3.13.2 Connectivity Coverage Gaps (Cellular vs. Satellite)

- 3.13.3 OEM Factory-Install Rates vs. Aftermarket Retrofit Rates

- 3.14 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.14.1 Base Case- Key Macro & Industry Variables Driving CAGR

- 3.14.2 Optimistic Scenarios- Favorable macro and industry tailwinds

- 3.14.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Offering, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Telematics Control Units (TCUs)

- 5.2.2 GPS Receivers

- 5.2.3 Sensors

- 5.2.4 Display Units

- 5.2.5 Connectivity Modules

- 5.3 Software

- 5.3.1 Fleet Management Platforms

- 5.3.2 Data Analytics & Reporting

- 5.3.3 Others

- 5.4 Services

- 5.4.1 Professional services

- 5.4.1.1 Installation & Integration

- 5.4.1.2 Maintenance & Support

- 5.4.1.3 Consulting & Training

- 5.4.2 Managed services

- 5.4.1 Professional services

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Fleet Management & Performance Reporting

- 6.3 Navigation & Asset Tracking

- 6.4 Fuel Management

- 6.5 Equipment Maintenance & Diagnostics

- 6.6 Fleet Safety & Compliance

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Connectivity, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Cellular

- 7.2.1 3G/4G LTE

- 7.2.2 5G

- 7.3 Satellite

Chapter 8 Market Estimates and Forecast, By Equipment Category, 2022 - 2035 ($ Mn, Fleet Size)

- 8.1 Key trends

- 8.2 Earthmoving Equipment

- 8.3 Material Handling Equipment

- 8.4 Road Construction Equipment

- 8.5 Hauling Equipment

- 8.6 Forestry Equipment

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Sales Channel, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 OEM/factory-installed

- 9.3 Aftermarket

Chapter 10 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 Rental & Leasing Companies

- 10.3 Contractors & Construction Companies

- 10.4 Mining Companies

- 10.5 Agriculture & Forestry Companies

- 10.6 Government & Municipal Agencies

- 10.7 Others

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Fleet Size)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Poland

- 11.3.8 Norway

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 Indonesia

- 11.4.6 South Korea

- 11.4.7 Thailand

- 11.4.8 Vietnam

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global players

- 12.1.1 Samsara

- 12.1.2 Trimble

- 12.1.3 Geotab

- 12.1.4 Caterpillar

- 12.1.5 Komatsu

- 12.1.6 Deere & Company

- 12.1.7 ORBCOMM

- 12.1.8 Topcon

- 12.1.9 CalAmp

- 12.1.10 Volvo Construction Equipment

- 12.1.11 CNH Industrial

- 12.1.12 Liebherr

- 12.1.13 Hitachi Construction Machinery

- 12.2 Regional players

- 12.2.1 Trackunit

- 12.2.2 J C Bamford

- 12.2.3 Actia

- 12.2.4 DSA Daten- und Systemtechnik

- 12.2.5 MiX Telematics

- 12.3 Emerging players

- 12.3.1 Machinemax

- 12.3.2 DPL Telematics