|

시장보고서

상품코드

2071249

지속가능한 선박 연료 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2026-2035년)Sustainable Marine Fuels Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

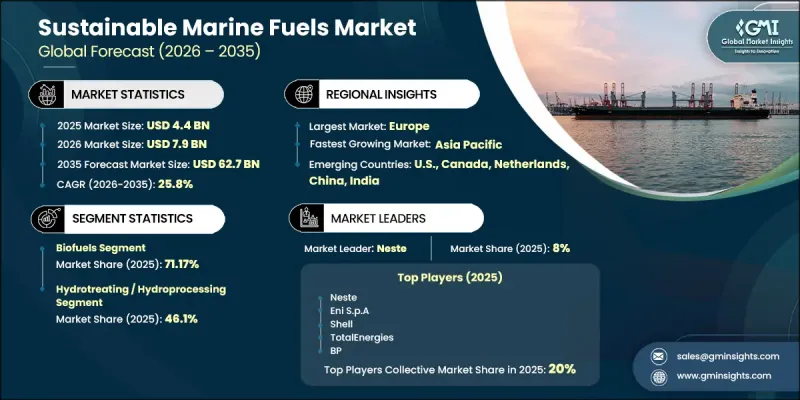

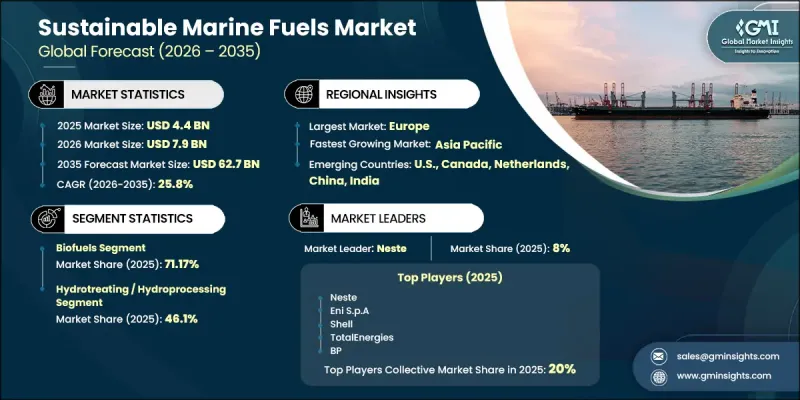

지속가능한 선박 연료 세계 시장은 2025년에 44억 달러 규모에 달하고, 2035년까지 CAGR 25.8%로 성장하여 627억 달러에 달할 것으로 추정됩니다.

지속가능한 선박 연료 산업 전반의 성장은 전 세계적인 배출 규제 강화, 온실가스 배출 강도 감축 의무 목표, 그리고 해운 업계 전반의 운영 및 조달 전략을 재편하고 있는 탄소 가격 책정 메커니즘의 확대에 영향을 받고 있습니다. 공급망에서 발생하는 배출량이 기업의 탄소 중립 프레임워크에 점점 더 많이 반영됨에 따라, 화주들의 탈탄소화 노력이 수요를 더욱 부추기고 있습니다. 이러한 변화는 수요 안정화와 인프라 투자 지원으로 이어지는 장기적인 연료 조달 계약을 촉진하고 있습니다. 그 결과, 해운 사업자들은 진화하는 환경 기준을 더욱 철저히 준수하는 한편, 저배출 연료의 안정적인 공급을 확보하기 위해 산업 파트너들과의 협력을 더욱 강화하고 있습니다. 지속가능한 선박 연료로의 전환은 해운 밸류체인 전반에 걸친 협력 관계의 강화에 힘입어 추진되고 있으며, 연료 생산자, 물류 사업자 및 이해관계자들이 공동으로 저탄소 연료 생태계의 확대를 지원하고 있습니다. 이러한 구조적 촉진요인들이 복합적으로 작용하여, 예측 기간 동안 선박용 연료 조달 패턴이 대폭 재편될 것으로 예상됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 초기 시장 규모 | 44억 달러 |

| 예측액 | 627억 달러 |

| CAGR | 25.8% |

바이오 기반 선박용 연료 부문은 71.17%의 시장 점유율을 차지하며 31억 3,000만 달러의 매출을 기록했고, 연평균 성장률(CAGR) 16.3%로 성장했습니다. 이 부문이 주도적인 위치를 차지하고 있는 주요 이유는, 기존의 선박용 엔진 시스템 및 연료 공급 인프라와의 호환성이 높아, 선박을 대대적으로 개조할 필요 없이 도입할 수 있다는 점에 있습니다. 이러한 운영상의 유연성 덕분에 바이오 기반 연료는 전 세계 선박 함대를 대상으로 한 해운 부문의 탈탄소화를 위한 가장 현실적인 단기적 방안 중 하나가 되고 있습니다.

수소 처리 및 수소 정제 기술 부문은 2025년에 46.1%의 점유율을 차지하며 2억 3,000만 달러 규모의 시장을 기록했습니다. 이러한 공정은 수소를 기반으로 한 정제 방법을 통해 지질계 원료를 저탄소 선박용 연료로 전환함으로써, 재생 디젤형 연료의 생산을 뒷받침하고 있습니다. 다양한 원료를 표준화된 연료 제품으로 효율적으로 전환할 수 있는 능력 덕분에, 대규모의 지속가능한 연료 생산 시스템 내에서 그 활용이 확대되고 있습니다.

북미의 지속가능한 선박 연료 시장은 2025년에 22.45%의 점유율을 차지하고, 시장 규모는 9억 9,000만 달러에 달하며, 2035년까지 연평균 성장률(CAGR) 23.2%로 성장할 것으로 전망됩니다. 미국은 저탄소 해운으로의 전환을 가속화하기 위해 마련된 정책 체계에 힘입어, 해당 지역의 주요 성장 동력이 되고 있습니다. 청정 연료 인프라에 대한 투자 증가와 상업 해운 및 국방 관련 해양 활동에서의 도입 확대가 해당 지역의 시장 성장을 더욱 뒷받침하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 규모 및 예측 : 연료 유형별, 2022-2035년

제6장 시장 규모 및 예측 : 변환 프로세스별, 2022-2035년

제7장 시장 규모 및 예측 : 용도별, 2022-2035년

제8장 시장 규모 및 예측 : 지역별, 2022-2035년

제9장 기업 개요

KSMThe Global Sustainable Marine Fuels Market was valued at USD 4.4 billion in 2025 and is estimated to grow at a CAGR of 25.8% to reach USD 62.7 billion by 2035.

Growth across the sustainable marine fuels industry is influenced by tightening global emissions regulations, mandatory greenhouse gas intensity reduction targets, and increasing carbon pricing mechanisms that are reshaping operational and procurement strategies across the shipping sector. Decarbonization commitments from cargo owners are further reinforcing demand, as supply chain emissions are increasingly incorporated into corporate net-zero frameworks. This shift is encouraging long-term fuel procurement agreements that help stabilize demand and support infrastructure investment. As a result, shipping operators are increasingly aligning with industrial partners to secure reliable access to low-emission fuel supplies while improving compliance with evolving environmental standards. The transition toward sustainable marine fuels is also being reinforced by growing collaboration across the maritime value chain, where fuel producers, logistics operators, and cargo stakeholders are jointly supporting the scale-up of low-carbon fuel ecosystems. These combined structural drivers are expected to significantly reshape marine fuel sourcing patterns over the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.4 Billion |

| Forecast Value | $62.7 Billion |

| CAGR | 25.8% |

The bio-based marine fuels segment held a 71.17% share, generating USD 3.13 billion, while expanding at a CAGR of 16.3%. Their leadership position is largely attributed to their compatibility with existing marine engine systems and fuel distribution infrastructure, enabling adoption without requiring major vessel modifications. This operational flexibility has made bio-based fuels one of the most practical short-term pathways for maritime decarbonization across global shipping fleets.

The hydrotreatment and hydroprocessing technologies segment held a 46.1% share in 2025, generating USD 2.03 billion. These processes convert lipid-based raw materials into low-carbon marine fuels through hydrogen-based refining methods, supporting the production of renewable diesel-type fuels. Their ability to efficiently transform diverse feedstocks into standardized fuel products has strengthened their adoption within large-scale sustainable fuel production systems.

North America Sustainable Marine Fuels Market held 22.45% share in 2025, valued at USD 0.99 billion, and is projected to grow at a CAGR of 23.2% through 2035. The United States serves as the key growth engine in the region, supported by policy frameworks designed to accelerate the transition toward low-emission maritime operations. Increasing investments in clean fuel infrastructure and expanding adoption across commercial shipping and defense-related maritime activities are further reinforcing regional market growth.

Key companies operating in the global sustainable marine fuels market include Shell, BP, Exxon Mobil Corporation, Chevron Corporation, TotalEnergies, Repsol, Eni S.p.A, Neste Corporation, World Energy, Cargill, Bunker Holding, FincoEnergies, Gevo, GoodFuels, Argent Energy, Moeve, Evergent Technologies, Kvasir Technologies, Steeper Energy, and Sunpine AB. Companies operating in the sustainable marine fuels market are focusing on strengthening their competitive positioning through large-scale investments in production capacity, long-term supply agreements, and strategic partnerships across the maritime value chain. Many market participants are prioritizing the expansion of biofuel and synthetic fuel production facilities to meet rising demand from shipping operators transitioning toward low-carbon operations. Collaboration with cargo owners and logistics providers is becoming increasingly important to secure offtake agreements and stabilize revenue streams. Firms are also investing heavily in research and development to improve fuel efficiency, feedstock flexibility, and production scalability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Fuel type trends

- 2.1.3 Conversion process trends

- 2.1.4 Application trends

- 2.1.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Feedstock availability & sourcing analysis

- 3.1.2 Supply chain resilience & risk factors

- 3.1.3 Distribution network analysis

- 3.1.4 Disruptions

- 3.2 Regulatory landscape

- 3.2.1 IMO GHG Strategy & fuel EU maritime regulation

- 3.2.2 Regional Regulatory mandates (EU ETS, US EPA, IACS)

- 3.2.3 Carbon Intensity Indicator (CII) & EEXI compliance

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's Analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL Analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Environmental factors

- 3.6.6 Legal factors

- 3.7 Emerging opportunities & trends

- 3.8 Digitalization & IoT integration

- 3.9 Investment analysis & future prospects

- 3.10 Technology & innovation landscape

- 3.10.1 AI-Driven Disruption of bunkering, logistics & fleet management

- 3.10.2 GenAI use cases & adoption roadmap by fuel segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Impact of AI & Generative AI on the market (Solution Core)

- 3.11.1 AI-driven production optimization

- 3.11.2 Predictive maintenance & fault detection

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, 2025

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Middle East & Africa

- 4.2.1.5 Latin America

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 key developments

- 4.5.1 Merger & acquisition

- 4.5.2 Partnership & collaboration

- 4.5.3 New product launched

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Fuel type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Biofuel

- 5.2.1 Biodiesel

- 5.2.2 HVO /Renewable Diesel

- 5.2.3 Bio-Oil

- 5.2.4 Biocrude

- 5.3 Green Methanol

- 5.4 Green Ammonia

- 5.5 Green Hydrogen

- 5.6 Bio-LNG / RNG

- 5.7 Others

Chapter 6 Market Size and Forecast, By Conversion process, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Transesterification

- 6.3 Electrolysis-based synthesis

- 6.4 Fischer-tropsch synthesis (FTS)

- 6.5 Hydrotreating / hydroprocessing

- 6.6 Anaerobic digestion

- 6.7 Others

Chapter 7 Market Size and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Commercial Vessels

- 7.2.1 Cargo vessels

- 7.2.2 Tankers

- 7.2.3 Passenger vessels

- 7.2.4 Working vessels

- 7.3 Defense vessels

- 7.3.1 Naval surface ships

- 7.3.2 Amphibious & support vessels

- 7.4 Others

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Norway

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Netherlands

- 8.3.5 UK

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Singapore

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 Argent Energy

- 9.2 BP

- 9.3 Bunker Holding

- 9.4 Cargill

- 9.5 Chevron Corporation

- 9.6 Eni S.p.A

- 9.7 Evergent Technologies

- 9.8 Exxon Mobil Corporation

- 9.9 FincoEnergies

- 9.10 Gevo

- 9.11 GoodFuels

- 9.12 Kvasir Technologies

- 9.13 Moeve

- 9.14 Neste Corporation

- 9.15 Shell plc

- 9.16 Steeper Energy

- 9.17 Sunpine AB

- 9.18 Repsol

- 9.19 TotalEnergies

- 9.20 World Energy