|

시장보고서

상품코드

2071267

변전소 자동화 시장 : 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Substation Automation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

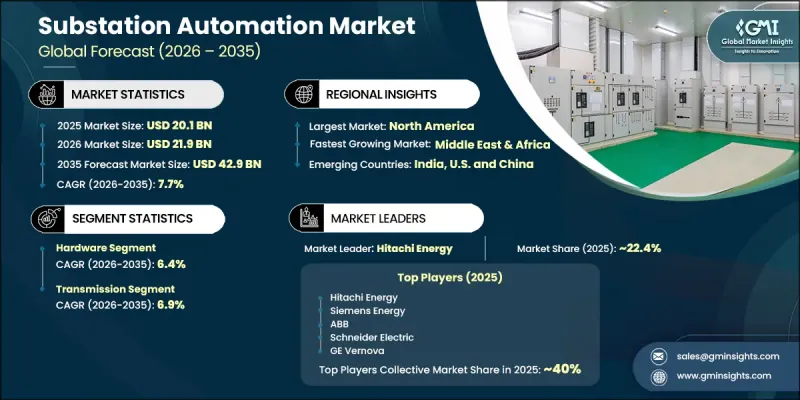

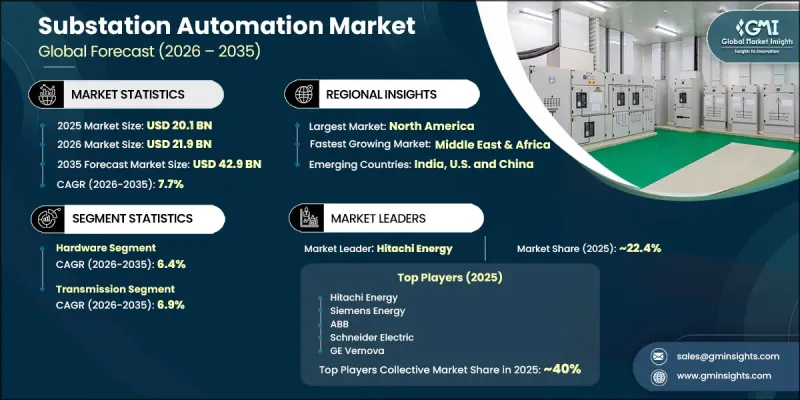

세계의 변전소 자동화 시장은 2025년에 201억 달러 규모가 되어, CAGR 7.7%로 성장하여 2035년까지 429억 달러에 이를 것으로 예측됩니다.

변전소 자동화 업계의 성장은 디지털 그리드 인프라로의 광범위한 전환과 표준화된 자동화 아키텍처의 채택 확대에 힘입어 이루어지고 있습니다. 전력망 현대화를 촉진하는 규제 조치, 재생에너지 원천의 통합 진전, 그리고 사이버 보안 요건의 강화로 인해 첨단 자동화 기술에 대한 지속적인 수요가 발생하고 있습니다. 전력 회사는 운영 효율성과 네트워크 신뢰성을 높이기 위해 지능형 모니터링, 실시간 시스템 제어 및 자동화된 전력망 관리 기능을 점점 더 우선시하고 있습니다. 동시에, 분산형 에너지 자원의 확대에 따라 배전 체계가 재구축되면서, 보다 고도화된 통신·제어 시스템의 필요성이 커지고 있습니다. 현대 전력 네트워크의 복잡성이 증가함에 따라, 동적인 전력 관리, 고도화된 운영 가시화, 그리고 전력망 자산 간의 원활한 연동을 지원하는 응답성이 뛰어난 자동화 플랫폼이 요구되고 있습니다. 전력 회사들이 노후화된 인프라를 지속적으로 교체해 나가는 가운데, 변전소 자동화 솔루션에 대한 투자는 전 세계의 장기적인 전력망 혁신 전략에서 계속해서 중요한 요소가 될 것으로 보입니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 201억 달러 |

| 예측 금액 | 429억 달러 |

| CAGR | 7.7% |

하드웨어 부문은 44%의 점유율을 차지하고 있으며, 2035년까지 연평균 성장률(CAGR) 6.4%로 성장할 것으로 전망됩니다. 하드웨어 구성 요소는 전력망 전체에 걸쳐 감시, 보호, 통신 및 제어 기능을 가능하게 함으로써 변전소 자동화 시스템의 기반을 형성하고 있습니다. 고급 디지털 통신 아키텍처로의 전환이 진행되는 가운데, 가혹한 전력 환경에서의 운용을 염두에 두고 설계된 지능형 필드 디바이스, 고성능 통신 장비 및 신뢰성이 높은 네트워크 인프라에 대한 수요가 꾸준히 증가하고 있습니다. 시스템의 상호 운용성, 운영 신뢰성 및 실시간 데이터 교환에 대한 중요성이 커짐에 따라, 전력망 전반에 걸친 차세대 하드웨어 기술에 대한 투자가 지속적으로 촉진되고 있습니다.

설치 유형별로는 송전 변전소 부문이 2025년에 54%의 점유율을 차지하고, 2026년부터 2035년까지 연평균 성장률(CAGR) 6.9%로 성장할 것으로 전망됩니다. 송전 수준의 시설에 도입되는 자동화 시스템에는 대규모 송전 운영을 뒷받침하기 위해 고도로 선진적인 보호, 감시 및 통신 기능이 필요합니다. 이러한 설비에는 고도의 네트워크 연동 요건이 수반되므로, 시스템의 안정성, 신뢰성 및 운영상의 보안을 확보할 수 있는 고성능 소프트웨어 및 하드웨어 솔루션이 필요합니다. 송전 인프라 프로젝트의 규모와 복잡성으로 인해, 투자 수준은 다른 변전소 부문에 비해 여전히 상당히 높은 편이며, 시장 전체의 수익에 크게 기여하고 있습니다.

북미 변전소 자동화 시장은 2025년에 32.6%의 점유율을 차지하고, 2035년까지 연평균 성장률(CAGR) 6.9%로 성장할 것으로 전망됩니다. 이 지역의 성장은 광범위한 전력 사업 현대화 계획, 규제 준수 요건, 그리고 송전망의 복원력과 신뢰성 향상을 목표로 한 투자 증가에 힘입어 이루어지고 있습니다. 미국은 지속적인 인프라 개선과 전력 시스템의 성능 및 보안을 규정하는 엄격한 운영 기준에 힘입어, 시장 발전의 주요 견인차 역할을 계속하고 있습니다. 또한, 사이버 보안 규제의 발전에 따라 전력 사업자들은 첨단 모니터링, 통신 및 자동화 기술에 대한 투자를 늘리도록 장려받고 있으며, 이로 인해 지역 전체에서 변전소 자동화 솔루션에 대한 수요가 더욱 강화되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 규모 및 예측 : 컴포넌트별, 2022-2035년

제6장 시장 규모 및 예측 : 변전소 유형별, 2022-2035년

제7장 시장 규모 및 예측 : 설치 유형별, 2022-2035년

제8장 시장 규모 및 예측 : 최종 사용자별, 2022-2035년

제9장 시장 규모 및 예측 : 지역별, 2022-2035년

제10장 기업 개요

JHS 26.07.01The Global Substation Automation Market was valued at USD 20.1 billion in 2025 and is estimated to grow at a CAGR of 7.7% to reach USD 42.9 billion by 2035.

Growth in the substation automation industry is fueled by the widespread transition toward digital grid infrastructure and increasing adoption of standardized automation architectures. Regulatory initiatives promoting grid modernization, rising integration of renewable energy sources, and stronger cybersecurity requirements are creating sustained demand for advanced automation technologies. Utilities are increasingly prioritizing intelligent monitoring, real-time system control, and automated grid management capabilities to improve operational efficiency and network reliability. At the same time, the expansion of distributed energy resources is reshaping power distribution frameworks and increasing the need for more sophisticated communication and control systems. The growing complexity of modern electricity networks requires highly responsive automation platforms that support dynamic power management, advanced operational visibility, and seamless coordination across grid assets. As utilities continue upgrading aging infrastructure, investment in substation automation solutions is expected to remain a key component of long-term grid transformation strategies worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $20.1 Billion |

| Forecast Value | $42.9 Billion |

| CAGR | 7.7% |

The hardware segment held a 44% share and is forecast to grow at a 6.4% CAGR through 2035. Hardware components form the foundation of substation automation systems by enabling monitoring, protection, communication, and control functions throughout electrical networks. The ongoing migration toward advanced digital communication architectures is generating consistent demand for intelligent field devices, high-performance communication equipment, and reliable networking infrastructure designed to operate in demanding utility environments. Increasing emphasis on system interoperability, operational reliability, and real-time data exchange continues to support investment in next-generation hardware technologies across utility networks.

By installation type, the transmission substations segment held a 54% share in 2025 and is projected to grow at a CAGR of 6.9% during 2026-2035. Automation systems deployed in transmission-level facilities require highly advanced protection, monitoring, and communication capabilities to support large-scale power transfer operations. These installations involve sophisticated network coordination requirements and demand high-performance software and hardware solutions capable of ensuring system stability, reliability, and operational security. Due to the scale and complexity of transmission infrastructure projects, investment levels remain substantially higher than those associated with other substation categories, contributing significantly to overall market revenue.

North America Substation Automation Market accounted for 32.6% share in 2025 and is expected to grow at a CAGR of 6.9% through 2035. Regional growth is being supported by extensive utility modernization initiatives, regulatory compliance requirements, and increasing investments aimed at improving grid resilience and reliability. The United States remains the primary contributor to market development, driven by ongoing infrastructure upgrades and stringent operational standards governing power system performance and security. In addition, evolving cybersecurity regulations are encouraging utilities to increase spending on advanced monitoring, communication, and automation technologies, further strengthening demand for substation automation solutions across the region.

Key participants operating in the global substation automation market include ABB, Arcteq Relays, Belden, Brush Group, Eaton, GE Vernova, Hitachi Energy, Hyosung Heavy Industries, INTECH Automation & Intelligence, Larsen & Toubro, Lauritz Knudsen Electrical & Automation, Mipro, NARI Technology, NovaTech Automation, Schneider Electric, Schweitzer Engineering Laboratories, Siemens Energy, TBEA, Trilliant Holdings, and Yokogawa Electric. Companies active in the substation automation industry are implementing a range of strategic initiatives to reinforce their competitive position and expand market presence. Leading organizations are investing heavily in research and development to enhance digital automation capabilities, improve cybersecurity features, and increase system interoperability. Strategic partnerships with utilities, technology providers, and infrastructure developers are helping companies broaden their customer reach and accelerate project deployment. Market participants are also focusing on portfolio expansion through product innovation, advanced software integration, and intelligent grid management solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.8.3.1 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Component trends

- 2.4 Substation type trends

- 2.5 Installation type trends

- 2.6 End user trends

- 2.7 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Technology & Innovation Landscape

- 3.5.1 Digital Substation Architecture (IEC 61850 Process Bus & Station Bus)

- 3.5.2 Merging Units & Sampled Value Technology

- 3.5.3 Wide Area Monitoring Systems (WAMS) & Synchrophasor Technology

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

- 3.8 Impact of AI & generative AI on the market

- 3.8.1 AI-driven disruption of existing business models

- 3.8.2 GenAI use cases & adoption roadmap by segment

- 3.8.2.1 Predictive maintenance & fault detection

- 3.8.3 Risks, limitations & regulatory considerations

- 3.9 Cybersecurity Landscape in Substation Automation

- 3.9.1 threat vector analysis - OT/IT convergence risks in substation environments

- 3.9.2 cybersecurity incident history & impact on grid operations

- 3.9.3 NERC CIP & IEC 62351 compliance gap analysis by region

- 3.9.4 cybersecurity solution adoption trends - firewalls, IDS/IPS, encryption in substations

- 3.9.5 vendor cybersecurity capability benchmarking

- 3.10 Emerging opportunities & trends

- 3.11 Investment analysis & future outlook

- 3.11.1 Global capital expenditure in grid modernization & substation upgrades

- 3.11.2 Venture capital & strategic investment in substation technology startups

- 3.11.3 Public funding - government infrastructure programs (IRA, EU green deal, etc.)

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive positioning matrix

- 4.4 Key Developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans and funding

Chapter 5 Market Size and Forecast, By Component, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.4 Services

Chapter 6 Market Size and Forecast, By Substation Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Transmission

- 6.3 Distribution

Chapter 7 Market Size and Forecast, By Installation Type, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 New

- 7.3 Retrofit

Chapter 8 Market Size and Forecast, By End User, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Utilities

- 8.3 Oil & Gas

- 8.4 Metals & Mining

- 8.5 Transportation

- 8.6 Others

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 France

- 9.3.3 Germany

- 9.3.4 Italy

- 9.3.5 Russia

- 9.3.6 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Australia

- 9.4.3 India

- 9.4.4 Japan

- 9.4.5 South Korea

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 Turkey

- 9.5.4 South Africa

- 9.5.5 Egypt

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Argentina

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 Arcteq Relays

- 10.3 Belden

- 10.4 Brush Group

- 10.5 Eaton

- 10.6 GE Vernova

- 10.7 Hitachi Energy

- 10.8 Hyosung Heavy Industries

- 10.9 INTECH Automation & Intelligence

- 10.10 Larsen & Toubro

- 10.11 Lauritz Knudsen Electrical & Automation

- 10.12 Mipro

- 10.13 NARI Technology

- 10.14 NovaTech Automation

- 10.15 Schneider Electric

- 10.16 Schweitzer Engineering Laboratories

- 10.17 Siemens Energy

- 10.18 TBEA

- 10.19 Trilliant Holdings

- 10.20 Yokogawa Electric