|

시장보고서

상품코드

2071274

팬 코일 유닛 시장 : 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Fan Coil Unit Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

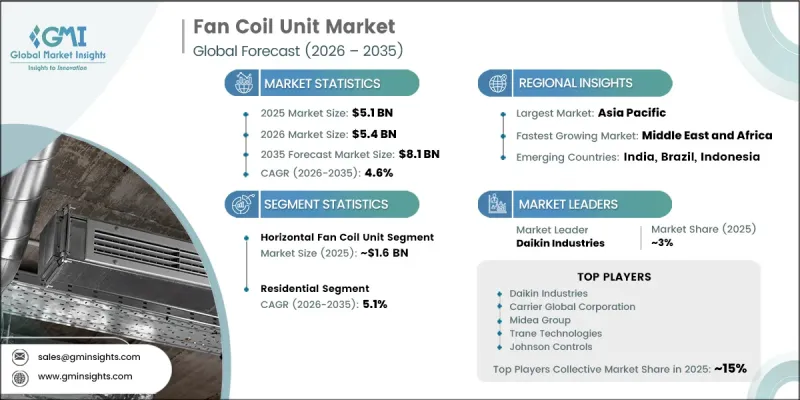

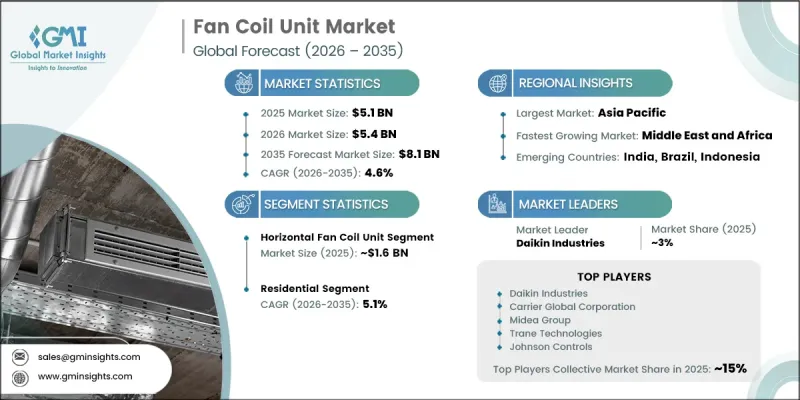

세계의 팬 코일 유닛 시장은 2025년에 51억 달러 규모가 되어, CAGR 4.6%로 확대되어 2035년까지 81억 달러에 이를 것으로 예측됩니다.

이러한 성장은 에너지 성능에 관한 규제 강화, 고밀도 건물에서의 도입 확대, 그리고 정밀한 열 관리가 필요한 데이터센터와 같은 기술 집약형 시설에서 수요 증가에 힘입어 이루어지고 있습니다. 팬 코일 유닛은 모듈식 구조, 온수 시스템과의 호환성, 그리고 효율적인 구역별 온도 제어 기능을 통해 광범위한 HVAC 생태계에서 필수적인 구성 요소로 자리매김하고 있습니다. 기존의 AC 모터 시스템에서 전자 정류 모터 기술로의 전환이 진행되고 있으며, 이는 제품 설계와 시장 경쟁에 변화를 가져오고 있습니다. EC 모터의 채택이 확산되고 있는 것은 그 뛰어난 효율성 때문이며, 특히 부분 부하 조건에서 뛰어난 성능을 발휘하기 때문입니다. 부분 부하는 사람이 이용하는 건물에서 주로 나타나는 가동 상태입니다. 여러 지역에서 시행되고 있는 규제상의 인센티브와 에너지 기준의 개정이 이러한 전환을 더욱 가속화하고 있으며, 이는 가격 체계에 영향을 미치는 동시에 제조업체들이 모든 용도에서 시스템의 성능과 효율 기준을 향상시키도록 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 51억 달러 |

| 예측 금액 | 81억 달러 |

| CAGR | 4.6% |

수평형 팬 코일 유닛 시장은 2025년에 16억 달러 규모에 달하고, 2035년까지 연평균 성장률(CAGR) 2.6%로 성장할 것으로 전망됩니다. 이 부문은 특히 호텔·리조트, 의료, 소매, 사무실 환경 등 천장에 은밀하게 설치해야 하는 상업 건축 프로젝트에서 널리 채택되고 있습니다. 도입 실적은 견조하지만, 시장이 성숙 단계에 접어들었기 때문에 성장세는 여전히 완만합니다. 이미 확립된 기술이 제조업체 간의 치열한 가격 경쟁을 초래하고 있는 것이 원인입니다. 제품 등급에 관계없이 성능 기준이 계속해서 수렴되고 있기 때문에 경쟁사와의 차별화는 점점 더 어려워지고 있습니다.

주택용 부문은 2025년에 59.9%의 시장 점유율을 차지하고, 2026년부터 2035년까지 연평균 성장률(CAGR) 5.1%로 성장할 것으로 전망됩니다. 주택 분야 수요는 도시 지역의 주택 개발 증가, 공동주택의 확대, 그리고 구형 냉방 시스템에서 고효율 대체 시스템으로의 교체 추세가 진행되고 있는 데 힘입어 지탱되고 있습니다. 또한, 신흥 경제국에서의 공공주택 사업 및 인프라 개발 프로그램도 성장의 원동력이 되고 있습니다. 인구 밀도가 높은 도시 지역에서는 집중형 냉방 인프라에 연결된 통합형 온수 시스템이 그 효율성과 장기적인 비용 이점으로 인해 점차 보급되고 있습니다.

미국 팬 코일 유닛 시장은 2025년에 11억 달러에 달하고, 2035년까지 연평균 성장률(CAGR) 3.6%를 기록하며 성장할 것으로 전망됩니다. 시장 확대는 엄격한 에너지 효율 규제에 힘입어 이루어지고 있으며, 이에 따라 구형 HVAC 시스템을 첨단 에너지 효율이 높은 대체 시스템으로 교체하는 속도가 빨라지고 있습니다. 캐나다에서는 건축물의 에너지 기준이 발전함에 따라, 특히 고층 주택이나 의료시설에서 고효율 팬 코일 시스템의 도입이 확대되고 있으며, 지속 가능한 건축 기법에 주력하고 있는 주요 주에서는 이러한 시스템의 도입이 활발히 이루어지고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 배치별, 2022-2035년

제6장 시장 추산 및 예측 : 제품 유형별, 2022-2035년

제7장 시장 추산 및 예측 : 모터 유형별, 2022-2035년

제8장 시장 추산 및 예측 : 공기 흐름별, 2022-2035년

제9장 시장 추산 및 예측 : 최종 용도별, 2022-2035년

제10장 시장 추산 및 예측 : 용도별, 2022-2035년

제11장 시장 추산 및 예측 : 유통 채널별, 2022-2035년

제12장 시장 추산 및 예측 : 지역별, 2022-2035년

제13장 기업 개요

JHS 26.07.01The Global Fan Coil Unit Market was valued at USD 5.1 billion in 2025 and is estimated to grow at a CAGR of 4.6% to reach USD 8.1 billion by 2035.

Growth is driven by stricter energy performance mandates, increasing deployment in high-density buildings, and rising demand from technology-intensive facilities such as data centers requiring precise thermal management. Fan coil units are becoming a critical component within the broader HVAC ecosystem due to their modular structure, hydronic system compatibility, and ability to deliver efficient zone-based temperature control. The ongoing transition from traditional AC motor systems to electronically commutated motor technologies is reshaping product design and market competitiveness. EC motor adoption is gaining momentum due to superior efficiency, especially under partial load conditions, which represent the primary operating state in occupied buildings. Regulatory incentives and updated energy codes across multiple regions are further accelerating this shift, influencing pricing structures and encouraging manufacturers to enhance system performance and efficiency standards across applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.1 Billion |

| Forecast Value | $8.1 Billion |

| CAGR | 4.6% |

The horizontal fan coil unit segment accounted for USD 1.6 billion in 2025 and is projected to grow at a CAGR of 2.6% through 2035. This segment is widely deployed in commercial construction projects where concealed ceiling installations are required, particularly in hospitality, healthcare, retail, and office environments. Despite its strong adoption base, growth remains moderate due to its maturity level, with established technologies leading to intense pricing pressure among manufacturers. Competitive differentiation is increasingly limited as performance standards across product tiers continue to converge.

The residential segment held 59.9% share in 2025 and is expected to grow at a CAGR of 5.1% during 2026-2035. Residential demand is supported by rising urban housing development, expansion of multi-family living spaces, and increasing replacement of older cooling systems with more efficient alternatives. Growth is also driven by public housing initiatives and infrastructure development programs across emerging economies. In dense urban settings, integrated hydronic systems connected to centralized cooling infrastructure are gaining traction due to their efficiency and long-term cost benefits.

United States Fan Coil Unit Market reached USD 1.1 billion in 2025 and is projected to grow at a CAGR of 3.6% through 2035. Market expansion is supported by strict energy efficiency regulations that are accelerating the replacement of outdated HVAC systems with advanced, energy-saving alternatives. In Canada, evolving building energy standards are driving adoption of efficient fan coil systems, particularly in high-rise residential and healthcare infrastructure, with strong implementation observed in key provinces focused on sustainable construction practices.

Key companies operating in the global fan coil unit market include Carrier Global Corporation, Trane Technologies, Daikin Industries, Johnson Controls International, Mitsubishi Electric Corporation, Aermec, Systemair AB, Price Industries, TROX GmbH, Galletti S.p.A., Dunham-Bush, Capital Coil & Air, Ice Air, Climate Control Group, The Whalen Company, Engineered Comfort, Unico System, Climetec Manufacturing Limited, USA Coil & Air, Krueger HVAC, and Zehnder Rittling. Market participants are focusing on strengthening their competitive position through advancements in energy-efficient technologies and next-generation HVAC system integration. Companies are investing heavily in EC motor-based designs to improve operational efficiency and reduce energy consumption. Expansion of smart HVAC solutions with digital controls and IoT-enabled monitoring systems is enhancing product differentiation. Manufacturers are also emphasizing modular and customizable designs to meet the evolving requirements of commercial and residential applications. Strategic collaborations with construction firms and HVAC contractors are improving project penetration.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Business trends

- 2.3 Regional

- 2.4 Configuration

- 2.5 Product type

- 2.6 Motor type

- 2.7 Air flow

- 2.8 End use

- 2.9 Application

- 2.10 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Manufacturers

- 3.1.3 Distributors

- 3.1.4 Retailers

- 3.1.5 Profit margin analysis

- 3.1.6 Value addition at each stage

- 3.1.7 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Data Center Proliferation & AI Infrastructure

- 3.2.1.2 Expansion of Healthcare Facilities

- 3.2.1.3 Energy Efficiency Mandates Driving Replacement and Upgrade Cycles

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High Initial Manufacturing & Installation Costs

- 3.2.2.2 Regulatory and Compliance Complexity

- 3.2.3 Opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing analysis (driven by primary research)

- 3.5.1 Historical price trend analysis by product category

- 3.5.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.6 Trade data analysis (based on paid data sources)

- 3.6.1 Import/export volume & value trends

- 3.6.2 Key trade corridors & tariff impact

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Impact of AI & generative AI on the market

- 3.10.1 AI-driven disruption of existing business models

- 3.10.2 GenAI use cases & adoption roadmap by segment

- 3.10.3 Risks, limitations & regulatory considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Configuration, 2022 - 2035, (USD Billion) (Units)

- 5.1 Key trends

- 5.2 Two pipe fan coil unit

- 5.3 Four pipe fan coil unit

Chapter 6 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Units)

- 6.1 Key trends

- 6.2 Horizontal fan coil unit

- 6.3 Vertical fan coil unit

- 6.4 Console fan coil unit

- 6.5 Cassette fan coil unit

- 6.6 EC motor fan coil unit

Chapter 7 Market Estimates & Forecast, By Motor Type, 2022 - 2035, (USD Billion) (Units)

- 7.1 Key trends

- 7.2 AC Motor

- 7.3 EC Motor

Chapter 8 Market Estimates & Forecast, By Air Flow, 2022 - 2035, (USD Billion) (Units)

- 8.1 Key trends

- 8.2 Below 500 m3/h

- 8.3 500 m3/h - 1000 m3/h

- 8.4 1000 m3/h - 1500 m3/h

- 8.5 1500 m3/h - 2000 m3/h

- 8.6 Above 2000 m3/h

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Billion) (Units)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

- 9.3.1 Office spaces

- 9.3.2 Hotels

- 9.3.3 Restaurants

- 9.3.4 Hospitals

- 9.3.5 Retail

- 9.3.6 Logistics

- 9.3.7 Others

- 9.4 Industrial

Chapter 10 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Units)

- 10.1 Key trends

- 10.2 New construction

- 10.3 Retrofit/replacement

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Units)

- 11.1 Key trends

- 11.2 Direct sales

- 11.3 Indirect sales

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Sweden

- 12.3.7 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.4.6 Indonesia

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 Middle East and Africa

- 12.6.1 Saudi Arabia

- 12.6.2 UAE

- 12.6.3 South Africa

Chapter 13 Company Profiles

- 13.1 Global Players

- 13.1.1 Carrier Global Corporation

- 13.1.2 Daikin Industries

- 13.1.3 Johnson Controls International

- 13.1.4 Mitsubishi Electric Corporation

- 13.1.5 Trane Technologies

- 13.1.6 Aermec

- 13.2 Regional Players

- 13.2.1 Galletti S.p.A.

- 13.2.2 Capital Coil & Air

- 13.2.3 Climate Control Group

- 13.2.4 Climetec Manufacturing Limited

- 13.2.5 Dunham-Bush

- 13.2.6 Engineered Comfort

- 13.2.7 Ice Air

- 13.2.8 Krueger HVAC

- 13.3 Emerging Players & Innovators

- 13.3.1 Price Industries

- 13.3.2 Systemair AB

- 13.3.3 The Whalen Company

- 13.3.4 TROX GmbH

- 13.3.5 Unico System

- 13.3.6 USA Coil & Air

- 13.3.7 Zehnder Rittling