|

시장보고서

상품코드

2071313

압축 공기 처리 장비 시장 : 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Compressed Air Treatment Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

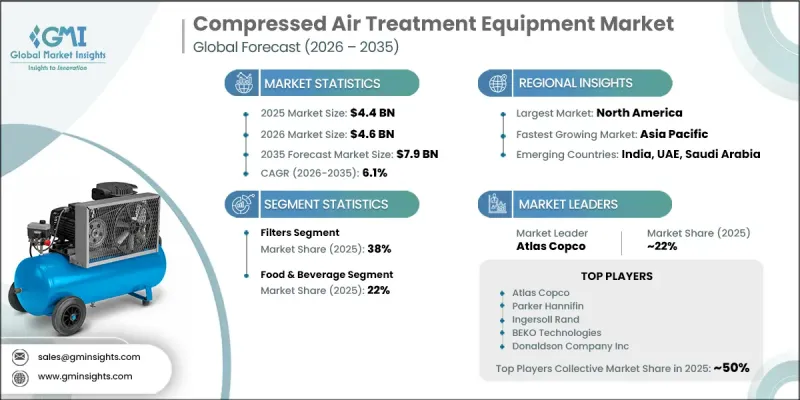

세계의 압축 공기 처리 장비 시장은 2025년에 44억 달러로 평가되었고 CAGR 6.1%로 성장하여 2035년까지 79억 달러에 이를 것으로 추정되고 있습니다.

시장 확대는 운영의 신뢰성을 확보하기 위해 깨끗하고 건조하며 불순물이 없는 압축 공기가 필수적인 산업 제조 환경 전반에 걸친 안정적인 수요에 힘입어 이루어지고 있습니다. 제약, 반도체, 식품 가공, 일반 제조 등의 업계에서는 제품 품질을 유지하고 엄격한 공정 기준을 충족하기 위해 여전히 첨단 공기 처리 시스템에 의존하고 있습니다. 또한, 자동화 및 인더스트리 4.0의 도입이 지속적으로 확대되고 있는 점도 성장을 뒷받침하고 있으며, 이에 따라 실시간 성능 추적, 예측 유지보수, 원격 진단이 가능한 지능형 센서 탑재형 공기 처리 시스템에 대한 수요가 증가하고 있습니다. 한편, 개발도상 지역에서는 자본 비용에 대한 민감도가 제품 도입 양상에 영향을 미치고 있어, 많은 구매자들이 고사양 구성보다는 초기 비용이 낮은 시스템을 우선시하고 있습니다. 일반적으로 10년 이상에 달하는 장비의 사용 수명 또한 교체 주기의 장기화로 이어지고 있으며, 이는 비용에 민감한 시장에서 재구매 수요를 구조적으로 억제하고 있습니다. 또한, 전기차(EV) 제조로의 전환에 따라 생산 공정이 기존의 공압식 방식보다 전기 시스템이나 로봇 시스템에 더 많이 의존하게 됨에 따라, 산업용 공기 수요 패턴도 서서히 변화하고 있습니다. 전반적으로 볼 때, 이 시장은 꾸준한 산업적 필요성과 진화하는 기술적 효율화 추세 간의 균형을 반영하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 44억 달러 |

| 예측 금액 | 79억 달러 |

| CAGR | 6.1% |

2025년에는 필터 부문이 시장 점유율의 38%를 차지하고, 시장 규모는 17억 달러에 달하며, 2035년까지 주요 제품 카테고리로 남아 있을 것으로 예측됩니다. 이 부문에는 고체 입자, 액체 에어로졸, 유증기, 미생물 불순물 등의 오염 물질을 제거하고, 산업 전반에 걸쳐 일관된 공기 청정도를 확보하기 위해 설계된 여러 가지 여과 기술이 포함되어 있습니다. 여과는 하류 장비를 보호하고 정밀한 제조 환경 전반에 걸쳐 생산 품질 기준을 유지하는 데 필수적인 역할을 하고 있기 때문에 수요는 계속해서 견조한 양상을 보이고 있습니다.

식품 및 음료 부문은 2025년에 22%의 시장 점유율을 차지하며 9억 6,700만 달러에 달했습니다. 이 부문은 2035년까지 연평균 성장률(CAGR) 6.5%를 기록하며 성장할 것으로 예상되며, 시장 전체가 확대되는 가운데 시장 점유율을 23%로 확대할 것으로 전망됩니다. 식품 및 음료 생산 환경에서는 압축 공기가 제품과 직접 접촉하는 공정, 건조 원료의 공기 이송, 충전, 포장, 밀봉, CIP 시스템 작동 등 여러 중요한 공정과 일부 보조 기능에 널리 사용되고 있습니다.

북미의 압축 공기 처리 장비 시장은 2025년에 38%의 점유율을 기록했으며, 시장 규모는 16억 달러에 달했습니다. 이 지역의 성장은 견고한 산업 인프라, 광범위한 제조 활동, 그리고 주요 부문에서 첨단 공기 처리 시스템의 높은 보급률에 힘입어 이루어지고 있습니다. 특히 제약, 식품 제조, 첨단 제조 등 엄격한 공기 품질 기준이 요구되는 업계에서는 수요가 계속해서 견조한 모습을 보이고 있습니다. 산업 현대화의 지속과 고정밀 제조 시설의 확장이 해당 지역 시장 성장을 더욱 뒷받침하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품 유형별, 2022-2035년

제6장 시장 추산 및 예측 : 용도별, 2022-2035년

제7장 시장 추산 및 예측 : 최종 사용 산업별, 2022-2035년

제8장 시장 추산 및 예측 : 유통 채널별, 2022-2035년

제9장 시장 추산 및 예측 : 지역별, 2022-2035년

제10장 기업 개요

JHS 26.07.01The Global Compressed Air Treatment Equipment Market was valued at USD 4.4 billion in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 7.9 billion by 2035.

Market expansion is driven by consistent demand across industrial manufacturing environments where clean, dry, and contaminant-free compressed air is essential for operational reliability. Industries such as pharmaceuticals, semiconductors, food processing, and general manufacturing continue to depend on advanced air treatment systems to maintain product quality and meet stringent process standards. Growth is further supported by the ongoing adoption of automation and Industry 4.0 practices, which are increasing the need for intelligent, sensor-enabled air treatment systems capable of real-time performance tracking, predictive maintenance, and remote diagnostics. At the same time, capital sensitivity in developing regions is influencing product adoption patterns, with many buyers prioritizing lower upfront-cost systems over advanced configurations. Equipment longevity, typically spanning over a decade, also leads to extended replacement cycles, which structurally moderates repeat demand in cost-sensitive markets. Additionally, the transition toward electric vehicle manufacturing is gradually reshaping industrial air demand patterns, as production processes become more reliant on electric and robotic systems rather than traditional pneumatic applications. Overall, the market reflects a balance between steady industrial necessity and evolving technological efficiency trends.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.4 Billion |

| Forecast Value | $7.9 Billion |

| CAGR | 6.1% |

The filters segment accounted for 38% share in 2025, reaching a value of USD 1.7 billion, and is expected to remain the leading product category through 2035. This segment includes multiple filtration technologies designed to eliminate contaminants such as solid particles, liquid aerosols, oil vapors, and microbial impurities, ensuring consistent air purity across industrial applications. Demand remains strong due to the essential role filtration plays in protecting downstream equipment and maintaining production quality standards across sensitive manufacturing environments.

The food and beverage segment held a 22% share in 2025, reaching USD 967 million. This segment is anticipated to grow at a CAGR of 6.5% through 2035, increasing its share to 23% within an overall expanding market. In food and beverage production environments, compressed air is used across multiple critical operations, including direct product contact processes, pneumatic conveying of dry ingredients, filling, packaging, sealing, and CIP system activation, along with several supporting functions.

North America Compressed Air Treatment Equipment Market held a 38% share in 2025, valued at USD 1.6 billion. The region's growth is supported by strong industrial infrastructure, extensive manufacturing activity, and high adoption of advanced air treatment systems across key sectors. Demand remains particularly strong in industries requiring highly controlled air quality standards, including pharmaceuticals, food production, and advanced manufacturing. Continued industrial modernization and expansion of high-precision manufacturing facilities are further reinforcing regional market growth.

Key companies operating in the global compressed air treatment equipment market include Ingersoll Rand Inc., Atlas Copco AB, SMC Corporation, Parker Hannifin Corporation, Donaldson Company, Inc., Kaeser Kompressoren SE, BEKO Technologies GmbH, Sullair LLC, Pneumatech, Van Air Systems, Mikropor Makina Sanayi ve Ticaret A.S., Nano-Purification Solutions, Omega Air d.o.o., Hangzhou Jiayuan Industrial Co., Ltd., Zeks Compressed Air Solutions, and Shanli Environmental Protection Technology. Companies operating in the compressed air treatment equipment market are focusing on strengthening their competitive position through continuous technological advancement and product innovation. A key strategy involves integrating smart monitoring systems, IoT connectivity, and predictive maintenance capabilities to improve operational efficiency and reduce downtime. Manufacturers are also expanding their product portfolios to address diverse industrial requirements, ranging from standard filtration and drying systems to highly specialized contamination control solutions. Strategic investments in energy-efficient and low-maintenance systems are helping companies align with sustainability goals while reducing lifecycle costs for end users.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Business trends

- 2.3 Regional

- 2.4 Product type

- 2.5 Application

- 2.6 End-use industry

- 2.7 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Manufacturers

- 3.1.3 Distributors

- 3.1.4 End users

- 3.1.5 Profit margin analysis

- 3.1.6 Value addition at each stage

- 3.1.7 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Semiconductor and electronics manufacturing expansion

- 3.2.1.2 EU energy efficiency directive compliance mandate

- 3.2.1.3 Pharmaceutical and healthcare GMP air quality mandates

- 3.2.1.4 Industrial IoT and smart connected treatment equipment

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High capital cost and long replacement cycles in price-sensitive markets

- 3.2.2.2 Energy transition reducing compressed air demand in certain end-uses

- 3.2.2.3 Technical complexity of retrofitting legacy systems

- 3.2.3 Opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing analysis (driven by primary research)

- 3.5.1 Historical price trend analysis by product category

- 3.5.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.6 Trade data analysis (based on paid data sources)

- 3.6.1 Import/export volume & value trends

- 3.6.2 Key trade corridors & tariff impact

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Impact of AI & generative AI on the market

- 3.10.1 AI-driven disruption of existing business models

- 3.10.2 GenAI use cases & adoption roadmap by segment

- 3.10.3 Risks, limitations & regulatory considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Units)

- 5.1 Key trends

- 5.2 Filters

- 5.2.1 Particulate Filters/Pre-filters

- 5.2.2 Coalescing Filters

- 5.2.3 Activated Carbon/Adsorber Filters

- 5.2.4 High Temperature After Filters

- 5.2.5 Sterile Air Filters

- 5.2.6 Centrifugal/Moisture Separators

- 5.3 Dryers

- 5.3.1 Refrigerated Dryers

- 5.3.2 Desiccant Air Dryers

- 5.3.3 Membrane Dryers

- 5.3.4 Deliquescent Dryers

- 5.4 Aftercoolers

- 5.4.1 Air-Cooled Aftercoolers

- 5.4.2 Water-Cooled Aftercoolers

- 5.5 Condensate Management Systems

- 5.5.1 Electronic/Level-Controlled Condensate Drains

- 5.5.2 Oil-Water Separators

- 5.5.3 Emulsion Splitting/Active Separation Systems

Chapter 6 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Units)

- 6.1 Key trends

- 6.2 Plant Air/Shop Air

- 6.3 Instrument Air

- 6.4 Process Air

- 6.5 Breathing Air

Chapter 7 Market Estimates & Forecast, By End-Use Industry, 2022 - 2035, (USD Billion) (Units)

- 7.1 Key trends

- 7.2 Food & Beverage

- 7.3 Automotive

- 7.4 Healthcare & Pharmaceuticals

- 7.5 Chemical & Petrochemical

- 7.6 Semiconductor & Electronics

- 7.7 Oil & Gas

- 7.8 Pulp & Paper

- 7.9 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Units)

- 8.1 Key trends

- 8.2 Direct Sales

- 8.3 Indirect Sales

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Sweden

- 9.3.7 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Atlas Copco AB

- 10.1.2 Donaldson Company Inc

- 10.1.3 Parker Hannifin Corporation

- 10.1.4 Kaeser Kompressoren SE

- 10.1.5 BEKO Technologies GmbH

- 10.1.6 Ingersoll Rand Inc

- 10.1.7 Hitachi Global Air Power

- 10.1.8 SMC Corporation

- 10.1.9 Kaishan Group

- 10.2 Regional Players

- 10.2.1 BOGE Kompressoren, Otto Boge GmbH & Co. KG

- 10.2.2 DALGAKIRAN Kompressor

- 10.2.3 Fusheng Group

- 10.2.4 Mikropor Inc

- 10.2.5 Van Air Systems

- 10.2.6 Omega Air

- 10.2.7 Festo SE & Co. KG

- 10.3 Emerging Players & Innovators

- 10.3.1 ELGi Equipments Ltd

- 10.3.2 Lingyu Air Separation Equipment

- 10.3.3 Schulz S.A.

- 10.3.4 RENNER Kompressoren GmbH