|

시장보고서

상품코드

2071344

양면형 태양광 모듈 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Bifacial Solar PV Module Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

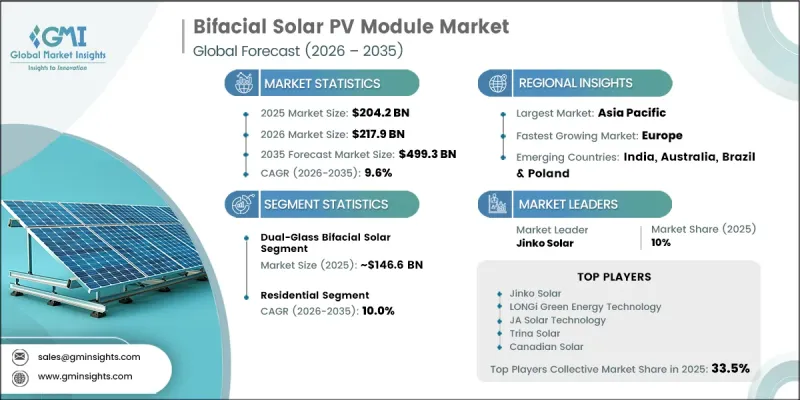

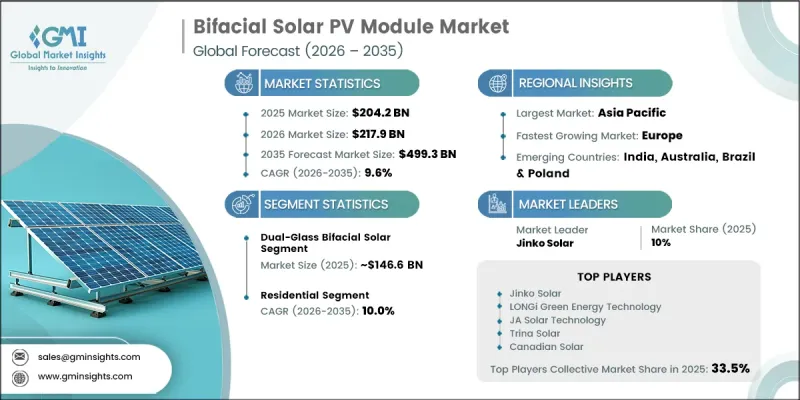

세계의 양면형 태양광 모듈 시장은 2025년에 2,042억 달러 규모에 이르고, CAGR 9.6%로 성장하여 2035년까지 4,993억 달러에 달할 것으로 추정되고 있습니다.

이러한 확대는 세계 태양광 발전 업계의 구조적 변화를 반영하는 것으로, 기존 시장과 신흥 재생에너지 시장 모두에서 양면 수광 기술이 기존의 단면 수광 모듈을 점차 대체하고 있습니다. 이러한 성장은 주로 발전량 증가, 균등화 발전 비용(LCOE)의 지속적인 하락, 그리고 주요 지역에서 재생에너지 도입을 촉진하는 지원적인 정책 체계에 힘입은 것입니다. 양면 수광 모듈은 전면과 후면 양쪽에서 태양 복사를 포착하여 전력을 생산하기 때문에 기존 패널에 비해 전체적인 발전량을 향상시킵니다. 대규모 태양광 발전 프로젝트의 도입 확대, 기업의 재생에너지 조달 노력, 그리고 각국의 탈탄소화 전략이 수요를 더욱 가속화하고 있습니다. 양면 수광 시스템의 성능 효율은 설치 장소에 따라 달라지는 지표면의 반사율, 모듈의 설치 각도, 어레이 간격, 환경적 오염 상태 등 설치 요인의 영향을 받습니다. 양면 수광 시스템은 이중 유리 구조나 재료 사용량 증가로 인해 일반적으로 초기 투자 비용이 높지만, 내구성과 발전량이 향상됨에 따라 전 세계 태양광 발전 시장 전반에서 보급이 확대되고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 2,042억 달러 |

| 예측액 | 4,993억 달러 |

| CAGR | 9.6% |

2025년, 양면형 듀얼 글라스 태양광 모듈 부문은 71.8%의 시장 점유율을 차지했으며, 해당 시장 규모는 약 1,466억 달러에 달했습니다. 이러한 선도적인 위상은 다른 설계에 비해 뛰어난 구조적 견고성과 환경적 스트레스에 대한 내성 향상 덕분에 뒷받침되고 있습니다. 양면 유리 구조는 습기 침투 및 자외선에 의한 열화에 대한 보호 성능이 향상되어, 가동 수명 연장에 기여하고 있습니다. 이러한 장점 덕분에, 장기적인 성능의 신뢰성과 긴 수명이 중요한 투자 판단 기준이 되는 대규모 태양광 발전 설비에서 이 모듈이 우선적으로 선택되고 있습니다.

주택 부문은 2025년에 33.5%의 점유율을 차지하고, 시장 규모는 684억 달러에 달하며, 2035년까지 연평균 성장률(CAGR) 10%를 나타낼 것으로 예측됩니다. 주택용 시장에서 양면형 모듈의 도입률은 뒷면에서 들어오는 빛을 제한하는 설치상의 제약으로 인해, 유틸리티 규모의 도입에 비해 상대적으로 낮은 수준입니다. 그러나 설치 업체들이 성능상의 이점을 효과적으로 실현할 수 있는 지상 설치형 주택 시스템, 태양광 카포트 구조, 그리고 평지붕 설치에 양면형 기술을 점점 더 많이 도입함에 따라, 도입은 꾸준히 증가하고 있습니다. 에너지 효율과 분산형 태양광 발전에 대한 소비자의 관심이 높아지고 있는 점도 이 부문의 성장을 더욱 뒷받침하고 있습니다.

2025년, 북미의 양면형 태양광 모듈 시장은 8.7%의 점유율을 기록했습니다. 미국은 태양광 발전 설비 용량의 꾸준한 증가와 재생에너지 투자를 촉진하는 유리한 정책 체계에 힘입어, 계속해서 해당 지역의 주요 시장으로 자리매김하고 있습니다. 유틸리티 규모의 태양광 발전 도입 확대와 기업의 청정 에너지 조달 증가가 맞물리면서, 해당 지역 전체에서 양면형 기술에 대한 지속적인 수요를 계속해서 견인하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 규모와 예측 : 두께별, 2022-2035년

제6장 시장 규모와 예측 : 유형별, 2022-2035년

제7장 시장 규모와 예측 : 용도별, 2022-2035년

제8장 시장 규모와 예측 : 기술별, 2022-2035년

제9장 시장 규모와 예측 : 프레임 유형별, 2022-2035년

제10장 시장 규모와 예측 : 설치별, 2022-2035년

제11장 시장 규모와 예측 : 지역별, 2022-2035년

제12장 기업 개요

LSH 26.07.02The Global Bifacial Solar PV Module Market was valued at USD 204.2 billion in 2025 and is estimated to grow at a CAGR of 9.6% to reach USD 499.3 billion by 2035.

The expansion reflects a structural transformation in the global solar industry, where bifacial technologies are increasingly replacing traditional monofacial modules across both established and emerging renewable energy markets. Growth is primarily supported by higher rear-side energy generation, continuous reductions in the levelized cost of electricity, and supportive policy frameworks promoting renewable energy adoption across major regions. Bifacial modules generate electricity by capturing solar radiation from both the front and rear surfaces, improving overall energy yield compared to conventional panels. Increasing adoption of large-scale solar projects, corporate renewable procurement commitments, and national decarbonization strategies are further accelerating demand. Performance efficiency in bifacial systems is influenced by installation factors such as ground reflectivity, module elevation, array spacing, and environmental soiling conditions, which vary across deployment sites. Although bifacial systems typically involve higher upfront investment due to dual-glass construction and enhanced material usage, their improved durability and energy output are supporting wider adoption across global solar markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $204.2 Billion |

| Forecast Value | $499.3 Billion |

| CAGR | 9.6% |

The dual-glass bifacial solar module segment held a 71.8% share in 2025, equivalent to approximately USD 146.6 billion. Its leadership position is supported by superior structural integrity and enhanced resistance to environmental stress compared to alternative designs. The dual-glass configuration offers improved protection against moisture ingress and ultraviolet degradation, contributing to longer operational lifespans. These advantages make it a preferred choice for large-scale solar installations where long-term performance reliability and extended service life are critical investment considerations.

The residential application segment accounted for 33.5% share in 2025, valued at USD 68.4 billion, and is expected to grow at a CAGR of 10% through 2035. Residential adoption of bifacial modules is comparatively lower than utility-scale deployments due to installation constraints that limit rear-side light capture. However, adoption continues to grow steadily as installers increasingly incorporate bifacial technologies into ground-mounted home systems, solar carport structures, and flat-roof installations where performance benefits can still be effectively realized. Rising consumer interest in energy efficiency and distributed solar generation is further supporting segment growth.

North America Bifacial Solar PV Module Market held an 8.7% share in 2025. The United States remains the leading market in the region, supported by strong solar capacity additions and favorable policy frameworks encouraging renewable energy investment. Expanding utility-scale solar deployment, coupled with rising corporate clean energy procurement, continues to drive sustained demand for bifacial technologies across the region.

Major companies operating in the global bifacial solar PV module market include LONGi Green Energy Technology, Jinko Solar, Trina Solar, JA Solar Technology, Canadian Solar, First Solar, Hanwha Q CELLS, Vikram Solar, Silfab Solar, Astronergy, Seraphim Solar, Sharp Corporation, AE Solar, Axitec, Boviet Solar, Bluesun Solar, Sunergy, Primroot, Yingli Solar, and 3Sun. Companies operating in the bifacial solar PV module market are focusing on strengthening their competitive position through continuous technological innovation, efficiency improvements, and large-scale production expansion. A key strategy involves enhancing module efficiency through advanced cell architectures, improved light capture designs, and optimized rear-side energy generation capabilities. Manufacturers are also investing in vertical integration to control supply chains, reduce production costs, and improve quality consistency. Strategic partnerships with utility developers, EPC contractors, and renewable energy investors are helping companies secure long-term project pipelines. Geographic expansion into high-growth solar markets is further supporting revenue diversification and market penetration.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Market estimates & forecast parameters

- 1.3 Forecast

- 1.3.1 Key trends for market estimates

- 1.3.1.1 Quantified market impact analysis

- 1.3.2 Mathematical impact of growth parameters on forecast

- 1.3.3 Scenario analysis framework

- 1.3.1 Key trends for market estimates

- 1.4 Primary research and validation

- 1.4.1 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.2 Sources, by region

- 1.6 Research trail & scoring components

- 1.6.1 Research trail components

- 1.6.2 Scoring components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

- 1.8 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Thickness trends

- 2.4 Type trends

- 2.5 Application trends

- 2.6 Technology trends

- 2.7 Frame type trends

- 2.8 Mounting trends

- 2.9 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.2.1 North America

- 3.2.2 Europe

- 3.2.3 Asia Pacific

- 3.2.4 Middle East & Africa

- 3.2.5 Latin America

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of bifacial solar PV module

- 3.8 Trade data analysis (Driven by Primary Research)

- 3.8.1 Import/export volume & value trends (Driven by Primary Research)

- 3.8.2 Key trade corridors & tariff impact (Driven by Primary Research)

- 3.9 Impact of AI & Generative AI on the market (Driven by Primary Research)

- 3.9.1 Predictive maintenance & fault detection

- 3.9.2 Grid optimization & load forecasting

- 3.9.3 Digital twin simulation & testing

- 3.9.4 Risks, limitations & regulatory considerations

- 3.10 Emerging opportunities & trends

- 3.10.1 Digitalization & IoT integration

- 3.10.2 Emerging market penetration

- 3.11 Investment analysis and future outlook

Chapter 4 Competitive landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Thickness, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 < 2 mm

- 5.3 2 mm to 3 mm

- 5.4 > 3 mm

Chapter 6 Market Size and Forecast, By Type, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 Dual-glass bifacial solar

- 6.3 Glass-backsheet bifacial solar

Chapter 7 Market Size and Forecast, By Application, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial & industrial

- 7.4 Utility

Chapter 8 Market Size and Forecast, By Technology, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 Passivated emitter rear contact (PERC)

- 8.3 TOPCon

- 8.4 Heterojunction (HJT)

Chapter 9 Market Size and Forecast, By Frame Type, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 Framed

- 9.3 Frameless

Chapter 10 Market Size and Forecast, By Mounting, 2022 - 2035 (USD Billion)

- 10.1 Key trends

- 10.2 Ground mounted

- 10.3 Rooftop

Chapter 11 Market Size and Forecast, By Region, 2022 - 2035 (USD Billion)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 Spain

- 11.3.3 Netherlands

- 11.3.4 Poland

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Australia

- 11.4.3 India

- 11.4.4 Japan

- 11.5 Middle East & Africa

- 11.5.1 UAE

- 11.5.2 Turkey

- 11.5.3 Egypt

- 11.6 Latin America

- 11.6.1 Brazil

- 11.6.2 Chile

Chapter 12 Company Profiles

- 12.1 3Sun

- 12.2 AE Solar

- 12.3 Astronergy

- 12.4 Axitec

- 12.5 Bluesun Solar

- 12.6 Boviet Solar

- 12.7 Canadian Solar

- 12.8 First Solar

- 12.9 Hanwha Q CELLS

- 12.10 JA Solar Technology

- 12.11 Jinko Solar

- 12.12 LONGi Green Energy Technology

- 12.13 Primroot

- 12.14 Seraphim Solar

- 12.15 Sharp Corporation

- 12.16 Silfab Solar

- 12.17 Sunergy

- 12.18 Trina Solar

- 12.19 Vikram Solar

- 12.20 Yingli Solar