|

시장보고서

상품코드

2071352

자율운항선박 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2026-2035년)Autonomous Ships Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

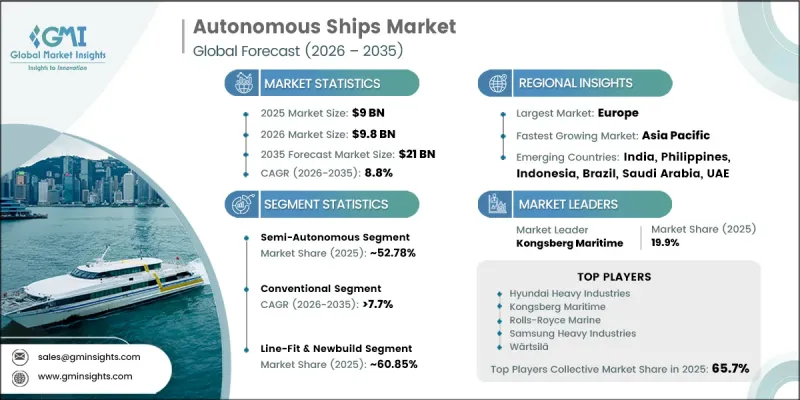

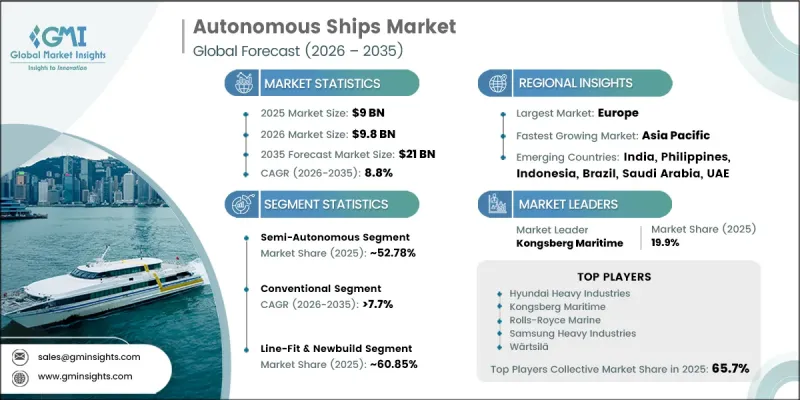

세계의 자율운항선박 시장은 2025년에 90억 달러 규모에 달하고, CAGR 8.8%로 성장하여 2035년까지 210억 달러에 달할 것으로 추정됩니다.

해상 무역의 현대화, 해양 인프라의 확대, 그리고 지능형 물류 시스템의 발전에 따라 기존의 해운 업무가 고도로 최적화된 자율형 선단 생태계로 재정의되면서, 시장은 구조적인 변화를 겪고 있습니다. 자율선박은 화물 운송, 해양 에너지 사업, 해군의 감시, 연안 물류 네트워크, 해양 조사 임무, 항만 운영 등 다양한 분야에서 점점 더 널리 활용되고 있습니다. 해운 사업자들은 AI를 활용한 항해 시스템, 위성 통신 기술, 첨단 항로 최적화 도구, 저배출 추진 시스템을 도입하여 운항 효율 향상, 수명 주기 비용 절감, 그리고 해상 운영에서의 데이터 기반 의사결정 개선을 도모하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 초기 시장 규모 | 90억 달러 |

| 예측액 | 210억 달러 |

| CAGR | 8.8% |

시장의 성장은 진화하는 국제 규제 체계, 지속가능성 노력, 그리고 전 세계적인 디지털 해운 이니셔티브의 영향을 크게 받고 있습니다. 해사 당국이 도입한 기준과 지역별 배출 감축 정책에 따라 스마트 해사 기술의 도입이 가속화되고 있습니다. 탄소 중립 목표 달성과 주요 무역 지역에서의 그린 해운 회랑 도입을 위한 압력이 높아지면서, 전기, 하이브리드, 수소 및 LNG를 동력원으로 하는 자율 항해 선박으로의 전환이 가속화되고 있습니다. 동시에, 신흥 경제국에서는 무역 효율과 국제 경쟁력을 높이기 위해 해상 인프라 구축을 추진하고, 자동화에 대응한 해운 시스템을 단계적으로 도입하고 있습니다. 이러한 규제 및 환경 측면의 변화는 조달 전략을 재구축하고, 선단 갱신 주기를 가속화하며, 지능형 항만 생태계 및 연결형 해양 인프라에 대한 투자를 촉진하고 있습니다.

2025년에는 반자율주행 부문이 52.78%의 점유율을 차지했으며, 2035년까지 연평균 성장률(CAGR) 8.6%로 성장할 것으로 전망됩니다. 해운 사업자들이 첨단 자동화 기능과 선상 인적 감시를 결합한 시스템을 점점 더 선호함에 따라, 이 부문은 계속해서 주도적인 위치를 유지하고 있습니다. 이러한 구성은 운항 안전성을 높이고, 규정 준수를 지원하며, 항해 위험을 줄이는 동시에, 상업용 해운 및 해양 사업 전반에 걸쳐 자율 기술을 단계적으로 통합할 수 있게 합니다. 자동화와 수동 제어의 균형을 중시하는 접근 방식 덕분에 전 세계 선단에서의 도입이 더욱 가속화되고 있습니다.

기존 추진 시스템 부문은 2025년에 53%의 시장 점유율을 차지했으며, 2026년부터 2035년까지 연평균 성장률(CAGR) 7.7%로 성장할 것으로 전망됩니다. 이러한 우위는 주로 전 세계가 확립된 선박용 연료 시스템에 의존하고 있으며, 기존 방식의 연료 공급 인프라가 널리 구축되어 있다는 점에 기인합니다. 기존의 선박용 엔진은 운영상의 신뢰성, 장거리 항해 능력, 그리고 비교적 간단한 유지보수 요건 덕분에 화물선, 유조선, 해양 지원선, 지역 화물 운송선에서 계속해서 널리 사용되고 있습니다. 또한, 설비 투자 부담이 적고 기존 항만 인프라와 호환성이 있기 때문에 기존의 추진 시스템은 전 세계 해운 사업자들에게 여전히 선호되는 선택지로 남아 있습니다.

독일의 자율운항선박 시장은 2025년에 33.6%의 점유율을 차지하며 11억 달러 규모의 시장 규모를 기록했습니다. 이 나라의 성장은 첨단 해양 공학 기술, 견고한 산업 기반, 그리고 디지털 해양 기술에 대한 투자 확대에 힘입어 이루어지고 있습니다. 독일은 해운 효율과 공급망 성과를 향상시키기 위해 스마트 항만 인프라, AI를 활용한 항행 시스템, 자동화된 하역 솔루션, 통합 물류 네트워크의 개발을 적극적으로 추진하고 있습니다. 유서 깊은 조선사, 선박 자동화 기술 제공업체, 연구 기관의 존재가 자율형 선박 시스템 및 해운 분야의 디지털 전환에 있어 혁신을 더욱 가속화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 유형별, 2022-2035년

제6장 시장 추정 및 예측 : 추진별, 2022-2035년

제7장 시장 추정 및 예측 : 설치별, 2022-2035년

제8장 시장 추정 및 예측 : 최종사용별, 2022-2035년

제9장 시장 추정 및 예측 : 지역별, 2022-2035년

제10장 기업 개요

KSM 26.07.03The Global Autonomous Ships Market was valued at USD 9 billion in 2025 and is estimated to grow at a CAGR of 8.8% to reach USD 21 billion by 2035.

The market is undergoing a structural shift as maritime trade modernization, offshore infrastructure expansion, and the evolution of intelligent logistics systems redefine traditional shipping operations into highly optimized autonomous fleet ecosystems. Autonomous vessels are being increasingly utilized across cargo transportation, offshore energy activities, naval surveillance, coastal logistics networks, marine research missions, and port operations. Shipping operators are deploying AI-enabled navigation systems, satellite-based communication technologies, advanced route optimization tools, and low-emission propulsion architectures to enhance operational efficiency, reduce lifecycle costs, and improve data-driven decision-making in maritime operations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9 Billion |

| Forecast Value | $21 Billion |

| CAGR | 8.8% |

Market growth is strongly influenced by evolving international regulatory frameworks, sustainability commitments, and global digital shipping initiatives. Standards introduced by maritime authorities and regional emission reduction policies are accelerating the adoption of smart maritime technologies. Increasing pressure to meet decarbonization targets and implement green shipping corridors across major trade regions is encouraging the shift toward electric, hybrid, hydrogen-powered, and LNG-based autonomous vessels. At the same time, emerging economies are upgrading maritime infrastructure and gradually introducing automation-ready shipping systems to improve trade efficiency and global competitiveness. These regulatory and environmental transitions are reshaping procurement strategies, accelerating fleet renewal cycles, and driving investments in intelligent port ecosystems and connected maritime infrastructure.

The semi-autonomous segment held a 52.78% share in 2025 and is expected to grow at a CAGR of 8.6% through 2035. This segment continues to dominate as shipping operators increasingly favor systems that combine advanced automation capabilities with human oversight onboard. Such configurations enhance operational safety, support regulatory compliance, reduce navigational risk, and allow gradual integration of autonomous technologies across commercial shipping and offshore operations. The balanced approach between automation and manual control is further strengthening adoption across global fleets.

The conventional propulsion segment accounted for 53% share in 2025 and is projected to grow at a CAGR of 7.7% from 2026 to 2035. This dominance is primarily supported by the global reliance on established marine fuel systems and the extensive availability of conventional fueling infrastructure. Conventional marine engines remain widely used across cargo vessels, tankers, offshore support ships, and regional freight carriers due to their operational dependability, long-distance capability, and relatively simple maintenance requirements. In addition, lower capital investment requirements and compatibility with existing port infrastructure continue to make conventional propulsion systems a preferred choice among shipping operators worldwide.

Germany Autonomous Ships Market held a 33.6% share in 2025 and generated USD 1.1 billion. The country's growth is driven by its advanced maritime engineering capabilities, strong industrial base, and increasing investments in digital maritime technologies. Germany is actively developing smart port infrastructure, AI-driven navigation systems, automated cargo handling solutions, and integrated logistics networks to enhance shipping efficiency and supply chain performance. The presence of established shipbuilding firms, marine automation technology providers, and research institutions is further accelerating innovation in autonomous vessel systems and maritime digital transformation.

Key companies operating in the Global Autonomous Ships Market include Rolls-Royce Marine, Wartsila, Kongsberg Maritime, ABB Marine, Hyundai Heavy Industries, Samsung Heavy Industries, Mitsui E&S, Ocean Infinity, Ocius Technology, and Thales. Companies operating in the autonomous ships market are focusing on advanced technology integration, strategic collaborations, and large-scale digital transformation initiatives to strengthen their competitive positioning. Continuous investment in artificial intelligence, machine learning, sensor fusion systems, and satellite communication technologies is enabling the development of more reliable and efficient autonomous navigation platforms. Partnerships with shipbuilders, defense organizations, and port authorities are helping accelerate real-world deployment and testing of autonomous vessels. Companies are also prioritizing modular system designs that allow gradual automation upgrades within existing fleets. Expansion into emerging maritime economies, participation in smart port development projects, and long-term service contracts are further reinforcing market presence. In addition, firms are enhancing cybersecurity capabilities, improving remote fleet management systems, and offering lifecycle support services to ensure operational reliability, regulatory compliance, and sustained adoption of autonomous shipping technologies across global maritime networks.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast Model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Propulsion

- 2.2.4 Fit

- 2.2.5 End use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Demand for Maritime Automation and Operational Efficiency

- 3.2.1.2 Expansion of Global Maritime Trade and Logistics Networks

- 3.2.1.3 Advancements in Artificial Intelligence and Navigation Technologies

- 3.2.1.4 Stringent Emission Regulations and Maritime Decarbonization Goals

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Initial Capital Investment Requirements

- 3.2.2.2 Cybersecurity Risks and Data Vulnerabilities

- 3.2.3 Market opportunities

- 3.2.3.1 Development of Green and Zero-Emission Autonomous Vessels

- 3.2.3.2 Increasing Adoption in Defense and Naval Applications

- 3.2.3.3 Expansion of Autonomous Coastal and Short-Sea Shipping

- 3.2.3.4 Integration of Maritime-as-a-Service (MaaS) Models

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and Innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 U.S.: US Coast Guard Autonomous Vessel Guidelines, NOAA Maritime Digital Navigation Initiatives.

- 3.5.1.2 Canada: Transport Canada Remote and Autonomous Vessel Testing Framework

- 3.5.2 Europe

- 3.5.2.1 Norway: Norwegian Maritime Authority Autonomous Fjord Navigation Regulations

- 3.5.2.2 United Kingdom: Maritime Autonomous Surface Ships (MASS) Regulatory Framework

- 3.5.2.3 Finland: One Sea Ecosystem and Smart Shipping Regulations

- 3.5.3 Asia Pacific

- 3.5.3.1 China: Intelligent Shipping Development Action Plan

- 3.5.3.2 Japan: Autonomous Ship Demonstration and Smart Maritime Initiative

- 3.5.3.3 South Korea: KASS Smart Shipping and Autonomous Vessel Certification Programs

- 3.5.3.4 Singapore: Maritime and Port Authority Smart Port and Autonomous Vessel Regulation

- 3.5.4 Latin America

- 3.5.4.1 Brazil: Smart Port Modernization and Autonomous Coastal Shipping Policies

- 3.5.4.2 Mexico: Port Digitalization and Maritime Automation programs

- 3.5.4.3 Chile: Autonomous Maritime Monitoring and Smart Logistics Framework

- 3.5.5 MEA

- 3.5.5.1 United Arab Emirates: Smart Ports and Autonomous Marine Transport Strategy

- 3.5.5.2 Saudi Arabia: Vision 2030 Maritime Digitalization Framework

- 3.5.5.3 South Africa: Green Maritime Transport and Port Automation Strategy

- 3.5.1 North America

- 3.6 Trade data analysis (Driven by Paid Research)

- 3.6.1 Import/export volume & value trends

- 3.6.2 Key trade corridors & tariff impact

- 3.7 Cost breakdown analysis

- 3.8 Patent Landscape (Driven by Primary Research)

- 3.9 Impact of AI & Generative AI on the Market (Driven by Primary Research)

- 3.9.1 AI-Driven Disruption of Existing Business Models

- 3.9.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.9.3 Risks, Limitations & Regulatory Considerations

- 3.10 Capacity & production landscape (Driven by Primary Research)

- 3.10.1 Installed capacity by region & key producer

- 3.10.2 Capacity utilization rates & expansion pipelines

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.12.1 Base Case - Key Macro & Industry Variables Driving CAGR

- 3.12.2 Optimistic Scenarios - Favourable macro and industry tailwinds

- 3.12.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Company market share analysis

- 4.1.1 North America

- 4.1.2 Europe

- 4.1.3 Asia Pacific

- 4.1.4 Latin America

- 4.1.5 MEA

- 4.2 Competitive analysis of major market players

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New Product Launches

- 4.4.4 Expansion Plans and funding

- 4.5 Company Tier Benchmarking

- 4.5.1 Tier Classification Criteria & Qualifying Thresholds

- 4.5.2 Tier Positioning Matrix by Revenue, Geography & Innovation

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Semi-Autonomous

- 5.3 Fully Autonomous

- 5.4 Remotely Operated

Chapter 6 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Fully Electric

- 6.3 Hybrid

- 6.4 Conventional

Chapter 7 Market Estimates & Forecast, By Fit, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Line-fit & Newbuild

- 7.3 Retrofit

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Commercial

- 8.2.1 Passenger Ship

- 8.2.2 Container Ships

- 8.2.3 Tankers

- 8.2.4 Others

- 8.3 Military & Defense

- 8.3.1 Submarines

- 8.3.2 Aircraft Carriers

- 8.3.3 Destroyers

- 8.3.4 Frigates

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Philippines

- 9.4.7 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 ABB Marine & Ports

- 10.1.2 Elbit Systems

- 10.1.3 Hyundai Heavy Industries (HD Hyundai)

- 10.1.4 Kongsberg Maritime

- 10.1.5 L3Harris Technologies

- 10.1.6 Oceanalpha

- 10.1.7 Saildrone

- 10.1.8 Samsung Heavy Industries

- 10.1.9 Sea Machines Robotics

- 10.1.10 Wartsila

- 10.2 Regional Players

- 10.2.1 Austal

- 10.2.2 BAE Systems

- 10.2.3 ECA Group (Exail)

- 10.2.4 Maritime Robotics

- 10.2.5 Ocean Infinity

- 10.2.6 Ocius Technology

- 10.2.7 ST Engineering Marine

- 10.2.8 Textron Systems

- 10.2.9 Thales

- 10.2.10 XOCEAN

- 10.3 Emerging Players

- 10.3.1 AutoNaut

- 10.3.2 Navtor

- 10.3.3 Ocean Aero

- 10.3.4 Robosys Automation

- 10.3.5 Subsea Tech