|

시장보고서

상품코드

2071354

인공와우 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2026-2035년)Cochlear Implants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

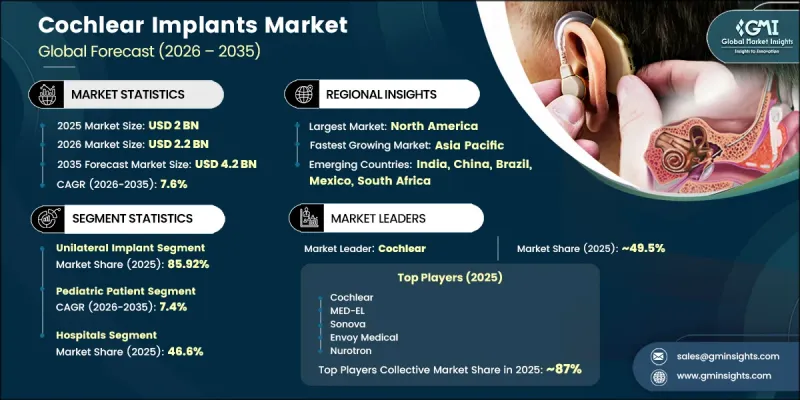

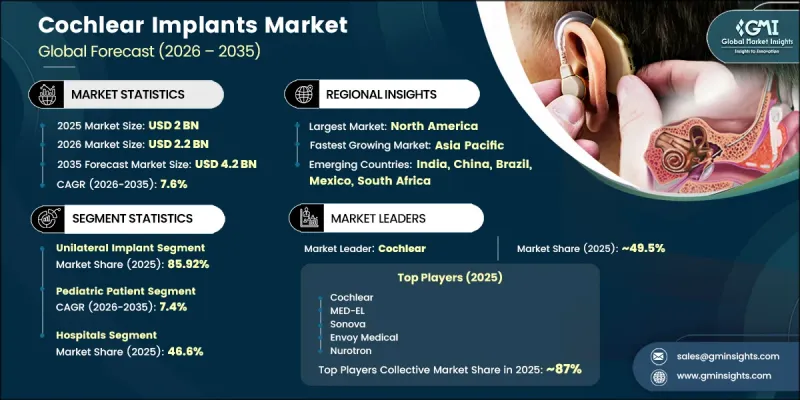

세계의 인공와우 시장은 2025년에 20억 달러 규모에 달하고, CAGR 7.6%로 성장하여 2035년까지 42억 달러에 달할 것으로 추정됩니다.

시장 성장을 뒷받침하고 있는 요인은 전 세계 중증 난청 유병률의 증가, 청력 검사 프로그램의 확대, 그리고 환자의 치료 성과와 기기의 성능을 향상시키고 있는 임플란트 기술의 지속적인 발전입니다. 인공와우 시스템이 연결성, 음향 처리 능력, 장기적인 기능성을 향상시킨 고도로 정교한 청각 솔루션으로 진화함에 따라, 업계는 큰 변화를 겪고 있습니다. 조기 청각 개입에 대한 인식 제고, 인공와우 수술에 대한 수용성 확대, 그리고 보험 적용 범위 확대가 선진국 및 신흥국 시장의 성장을 뒷받침하고 있습니다. 또한, 노화에 따른 청력 저하로 고통받는 고령 인구의 증가와 인생의 초기 단계에서 청각 장애가 발견되는 사례가 늘어나는 등 인구 동향도 수요를 뒷받침하고 있습니다. 의료 인프라의 개선, 전문적인 청각 관리 서비스에 대한 접근성 향상, 그리고 임상 적용 기준의 확대로 인해 대상 환자층이 더욱 확대되고 있습니다. 의료 종사자들이 청각 장애의 조기 진단과 치료를 지속적으로 중시하는 가운데, 인공와우 수술은 청각 기능 회복과 삶의 질 향상을 위해 점점 더 중요한 해결책으로 자리 잡고 있으며, 예측 기간 동안 지속적인 시장 성장을 위한 유리한 환경이 조성되어 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 초기 시장 규모 | 20억 달러 |

| 예측액 | 42억 달러 |

| CAGR | 7.6% |

2025년에는 단측 임플란트 부문이 시장 점유율의 85.92%를 차지했으며, 그 규모는 17억 2,000만 달러에 달했습니다. 단측 수술은 임상 현장에서 폭넓게 수용되고, 확립된 보험 급여 체계, 그리고 풍부한 외과적 전문 지식을 바탕으로 전 세계적으로 계속해서 주도적인 위치를 차지하고 있습니다. 이러한 성장을 뒷받침하고 있는 요인은 중증 청각 장애를 가진 환자층의 확대, 치료 접근성 향상, 그리고 적응증의 점진적인 확대입니다. 또한, 임플란트의 성능과 수술 성과가 지속적으로 향상되고 있는 점도, 성숙한 의료 시장과 발전 중인 의료 시장 모두에서 이 부문의 지속적인 성장에 기여하고 있습니다.

병원 부문은 46.6%의 점유율을 차지했으며, 2025년에는 9억 3,000만 달러의 매출을 올렸습니다. 병원이 주도적인 위치를 차지하고 있는 것은, 고도의 진단 능력, 다학제적 평가 과정, 외과적 전문 지식, 그리고 인공와우 이식 수술 후 재활 서비스 등, 인공와우 이식 수술에 필요한 종합적인 임상 인프라가 잘 갖춰져 있음을 반영합니다. 의료기관은 환자 평가, 이식 수술 및 장기적인 경과 관찰의 주요 거점으로서 계속해서 역할을 수행하고 있으며, 시장 전체의 매출에 크게 기여하고 있습니다.

북미의 인공와우 시장은 40.87%의 점유율을 차지하고 있으며, 2035년까지 연평균 성장률(CAGR) 6.8%로 성장할 것으로 전망됩니다. 시장의 성숙화로 인해 성장률은 비교적 완만하지만, 해당 지역은 선진적인 의료 시스템, 충실한 보험 환급 제도, 청력 회복 기술에 대한 폭넓은 인지도, 그리고 유리한 규제 측면의 지원 덕분에 계속해서 혜택을 누리고 있습니다. 미국은 청각 의료에 대한 지속적인 투자, 치료 접근성 확대, 그리고 임플란트 기술 및 임상 실무의 지속적인 발전에 힘입어, 이 지역의 매출에서 여전히 가장 큰 기여를 하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 제품별, 2022-2035년

제6장 시장 추정 및 예측 : 환자 유형별, 2022-2035년

제7장 시장 추정 및 예측 : 최종사용별, 2022-2035년

제8장 시장 추정 및 예측 : 지역별, 2022-2035년

제9장 기업 개요

KSM 26.07.03The Global Cochlear Implants Market was valued at USD 2 billion in 2025 and is estimated to grow at a CAGR of 7.6% to reach USD 4.2 billion by 2035.

Market growth is fueled by the increasing incidence of severe hearing impairment worldwide, expanding hearing assessment programs, and continuous advancements in implant technologies that are enhancing patient outcomes and device performance. The industry is undergoing a significant transformation as cochlear implant systems evolve into highly sophisticated auditory solutions featuring improved connectivity, sound processing capabilities, and long-term functionality. Rising awareness regarding early hearing intervention, growing acceptance of cochlear implantation procedures, and broader reimbursement availability are supporting market expansion across developed and emerging economies. Demand is also being strengthened by demographic trends, including the growing elderly population affected by age-related hearing decline and the increasing identification of hearing disorders at earlier stages of life. Improvements in healthcare infrastructure, greater accessibility to specialized hearing care services, and expanding clinical eligibility criteria are further increasing the addressable patient population. As healthcare providers continue to emphasize early diagnosis and treatment of hearing disorders, cochlear implantation is becoming an increasingly important solution for restoring hearing function and improving quality of life, creating a favorable environment for sustained market growth over the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2 Billion |

| Forecast Value | $4.2 Billion |

| CAGR | 7.6% |

The unilateral implant segment accounted for 85.92% share in 2025, representing USD 1.72 billion. Unilateral procedures continue to dominate global adoption due to their widespread clinical acceptance, established reimbursement support, and extensive availability of surgical expertise. Growth is being supported by an expanding patient base affected by severe hearing impairment, increasing treatment accessibility, and the gradual broadening of candidacy requirements. Continued improvements in implant performance and surgical outcomes are also contributing to the sustained expansion of this segment across both mature and developing healthcare markets.

The hospitals segment held a 46.6% share, generating USD 0.93 billion in 2025. The dominance of hospitals reflects the comprehensive clinical infrastructure required for cochlear implantation procedures, including advanced diagnostic capabilities, multidisciplinary evaluation processes, surgical expertise, and post-implant rehabilitation services. Healthcare institutions continue to serve as the primary centers for patient assessment, implantation procedures, and long-term follow-up care, supporting their significant contribution to overall market revenue.

North America Cochlear Implants Market held a 40.87% share, growing at a CAGR of 6.8% through 2035. Although growth remains comparatively moderate due to market maturity, the region continues to benefit from advanced healthcare systems, strong reimbursement frameworks, widespread awareness of hearing restoration technologies, and favorable regulatory support. The United States remains the largest contributor to regional revenue, supported by ongoing investments in hearing healthcare, expanding treatment accessibility, and continued advancements in implant technologies and clinical practices.

Key companies operating in the global cochlear implants market include MED-EL, Neubio AG, Cochlear Limited, Sonova, Nurotron, Beyond Cochlear Implants, Demant A/S, and Envoy Medical. Companies active in the cochlear implants market are implementing a variety of strategic initiatives to strengthen their competitive position and expand market reach. Product innovation remains a primary focus, with manufacturers investing in advanced sound processing technologies, wireless connectivity features, and enhanced implant performance to improve patient outcomes. Organizations are increasing research and development spending to introduce next-generation hearing solutions and broaden clinical indications. Strategic partnerships with healthcare providers, research institutions, and rehabilitation centers are helping companies expand referral networks and improve patient access. Geographic expansion into underserved regions is also a key priority, supported by efforts to enhance distribution channels and strengthen local market presence. Additionally, companies are focusing on reimbursement advocacy, clinician training programs, and patient awareness initiatives to increase adoption rates and support long-term market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Patient type trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Reimbursement scenario

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 LAMEA

- 3.6 Technology landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Market size in terms of volume, 2022 - 2035 (Units)

- 3.7.1 Global

- 3.7.2 North America

- 3.7.3 Europe

- 3.7.4 Asia Pacific

- 3.7.5 Latin America

- 3.7.6 MEA

- 3.8 Consumer pathway

- 3.9 Pricing analysis, 2024

- 3.10 Consumer insights

- 3.11 Policy landscape

- 3.11.1 Risk management analysis

- 3.11.2 Research and development

- 3.11.3 Operations

- 3.11.4 Marketing and sales

- 3.11.5 Quality

- 3.11.6 Intellectual property rights

- 3.11.7 Regulatory

- 3.11.8 Information technology

- 3.11.9 Climate

- 3.11.10 Financial

- 3.12 Future market trends

- 3.13 Supply chain dynamics & manufacturing analysis

- 3.14 Pipeline analysis

- 3.15 Porter's analysis

- 3.16 PESTEL analysis

- 3.17 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Unilateral implants

- 5.3 Bilateral implants

Chapter 6 Market Estimates and Forecast, By Patient Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Adult

- 6.3 Pediatric

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 ENT clinics

- 7.4 Ambulatory surgical centers

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Cochlear

- 9.2 Envoy Medical

- 9.3 MED-EL

- 9.4 Nurotron

- 9.5 Sonova