|

시장보고서

상품코드

2071384

포켓 도어 시장 : 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Pocket Door Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

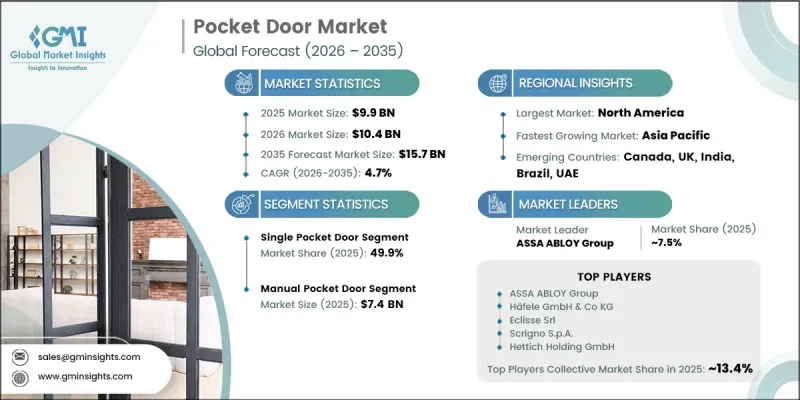

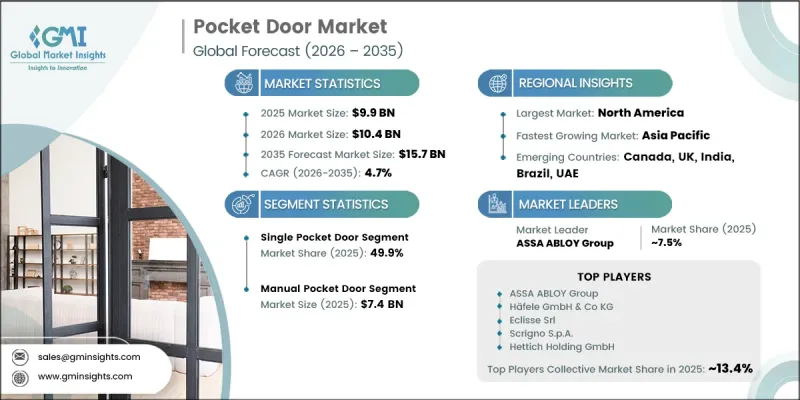

세계의 포켓 도어 시장은 2025년에 99억 달러 규모로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 4.7%로 성장하여 157억 달러에 이를 것으로 추정되고 있습니다.

이 시장의 성장은 전 세계의 주거 및 상업 건축 프로젝트에서 공간 절약형 실내 도어 시스템의 채택이 확대되고 있는 데 힘입고 있습니다. 수요를 견인하는 주요 요인은 북미, 유럽, 아시아태평양의 인구 밀집 도시권에서 평균 주거 면적이 지속적으로 축소되고 있다는 점이며, 이로 인해 효율적인 공간 활용이 설계상 중요한 고려 사항이 되고 있습니다. 그 결과, 미적 매력을 유지하면서 유효 바닥 면적을 극대화하기 위해 현대적인 건축 레이아웃에 포켓 도어가 점점 더 많이 도입되고 있습니다. 유연한 실내 레이아웃에 대한 수요가 증가하는 데다, 개보수 및 리모델링에 대한 투자 확대까지 더해져 시장 확대가 계속해서 뒷받침되고 있습니다. 또한, 설치 가치를 높여주는 대형 사이즈나 기술적으로 정교한 시스템을 포함한 프리미엄 도어 솔루션에 대한 선호도가 높아지고 있는 점도 업계에 호재가 되고 있습니다. 의료, 호스피탈리티, 복합 애플리케이션 개발 등의 상업 분야에서는 효율적인 공간 계획과 합리적인 인테리어 디자인의 중요성으로 인해 안정적인 수요가 지속되고 있습니다. 동시에, 성숙한 주택 시장에서 진행되는 리모델링 프로젝트는 신축 공사와는 별개의 새로운 기회를 창출하고 있으며, 전 세계 포켓도어 업계 전반의 장기적인 성장을 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 99억 달러 |

| 예측 금액 | 157억 달러 |

| CAGR | 4.7% |

2025년, 싱글 포켓 도어 부문은 49억 달러를 기록하며 시장 점유율의 49.9%를 차지했습니다. 이는 표준 주택 건설 프로젝트에서 널리 채택되고 있음을 반영합니다. 이러한 확고한 시장 지위는 실용적인 기능성, 합리적인 가격, 효율적인 공간 활용이 여전히 주요 구매 결정 기준으로 작용하는 다양한 실내 공간에서 폭넓게 활용되고 있다는 점에 힘입고 있습니다. 이 부문은 다양한 주택 프로젝트의 요구 사항과 예산 수준에 적합하기 때문에 계속해서 가장 많은 설치 대수를 유지하고 있습니다.

수동식 미닫이문 시스템 부문은 2025년에 74억 달러의 매출을 기록하며 시장 점유율의 74.3%를 차지했습니다. 이러한 압도적인 지위는 주로 자동식 제품에 비해 설치 비용이 저렴하고, 조작이 간편하며, 유지보수가 거의 필요하지 않기 때문인 것으로 보입니다. 이러한 장점들 덕분에 주택, 상업시설, 공공시설 등 각 분야에서 여전히 높은 보급률을 유지하고 있습니다. 많은 시장, 특히 비용 효율성과 설치 용이성을 중시하는 시장에서는 수동식 시스템이 여전히 선호되는 선택지로 남아 있으며, 예측 기간 동안 꾸준한 수요가 지속될 것으로 전망됩니다.

미국의 포켓 도어 시장은 2025년에 25억 달러를 기록하며 시장 점유율의 79.5%를 차지했습니다. 이 나라의 성장은 견조한 주택 건설 활동, 리모델링 지출 증가, 그리고 공간을 최적화한 인테리어 레이아웃에 대한 수요 증가에 힘입어 이루어지고 있습니다. 신축 주택에서 오픈 컨셉의 평면도가 인기를 끌면서, 포켓 도어 시스템의 도입을 더욱 촉진하고 있습니다. 또한, 의료시설, 호텔·리조트 시설, 공공 인프라 프로젝트에서 접근성을 중시하는 건축 요건이 이러한 솔루션에 대한 꾸준한 수요를 지속적으로 창출하고 있으며, 이는 지역 전체 시장 확대를 뒷받침하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 제품 유형별(2022-2035년)

제6장 시장 추정 및 예측 : 소재별(2022-2035년)

제7장 시장 추정 및 예측 : 메커니즘별(2022-2035년)

제8장 시장 추정 및 예측 : 설치 유형별(2022-2035년)

제9장 시장 추정 및 예측 : 최종 용도별(2022-2035년)

제10장 시장 추정 및 예측 : 유통 채널별(2022-2035년)

제11장 시장 추정 및 예측 : 지역별(2022-2035년)

제12장 기업 개요

KTHThe Global Pocket Door Market was valued at USD 9.9 billion in 2025 and is estimated to grow at a CAGR of 4.7% to reach USD 15.7 billion by 2035.

Market growth is supported by the increasing adoption of space-saving interior door systems across both residential and commercial construction projects worldwide. A key factor driving demand is the ongoing reduction in average living space within densely populated urban areas across North America, Europe, and Asia Pacific, making efficient space utilization a critical design consideration. As a result, pocket doors are increasingly being incorporated into modern architectural layouts to maximize usable floor area while maintaining aesthetic appeal. Rising demand for flexible interior configurations, combined with growing investments in renovation and remodeling activities, continues to support market expansion. The industry is also benefiting from increasing preference for premium door solutions, including larger-format and technologically advanced systems that contribute to higher installation values. Commercial sectors such as healthcare, hospitality, and mixed-use developments continue to generate steady demand due to the importance of efficient space planning and streamlined interior design. At the same time, renovation projects across mature housing markets are creating additional opportunities independent of new construction activity, supporting long-term growth across the global pocket door industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.9 Billion |

| Forecast Value | $15.7 Billion |

| CAGR | 4.7% |

The single pocket door segment accounted for USD 4.9 billion in 2025, representing 49.9% share, reflecting the widespread adoption across standard residential construction projects. Its strong market position is supported by broad usage across various interior spaces where practical functionality, affordability, and efficient space management remain key purchasing considerations. The segment continues to maintain the largest installation base due to its suitability for a wide range of residential project requirements and budget levels.

The manual pocket door systems segment generated USD 7.4 billion in 2025 and represented 74.3% share. Their dominant position is largely attributed to lower installation costs, straightforward operation, and reduced maintenance requirements compared with automated alternatives. These advantages continue to support strong adoption across residential, commercial, and institutional environments. In many markets, particularly those prioritizing cost efficiency and ease of installation, manual systems remain the preferred choice and are expected to sustain substantial demand throughout the forecast period.

United States Pocket Door Market accounted for USD 2.5 billion in 2025, representing 79.5% share. Growth in the country is being driven by robust residential construction activity, increasing renovation spending, and rising demand for space-optimized interior layouts. The growing popularity of open-concept floor plans across newly constructed homes is further contributing to the adoption of pocket door systems. Additionally, accessibility-focused building requirements across healthcare facilities, hospitality properties, and public infrastructure projects continue to create consistent demand for these solutions, supporting market expansion across the region.

Key companies operating in the global pocket door market include Hettich Holding GmbH & Co. oHG, Johnson Hardware, Hafele GmbH & Co KG, Eclisse Srl, ASSA ABLOY Group, Raydoor Inc., Linvisibile S.r.l., Ferrero Legno S.p.A., Andersen Corporation, JB Kind Ltd., Bertolotto Porte S.r.l., LPD Doors Ltd., Scrigno S.p.A., Portman Doors Ltd., and Cavity Sliders. Companies operating in the pocket door market are focusing on product innovation, portfolio diversification, and strategic partnerships to strengthen their market presence and competitive positioning. Manufacturers are investing in advanced hardware systems, premium design options, and automated door technologies to address evolving consumer preferences and increase average product value. Many companies are expanding distribution networks and strengthening relationships with architects, contractors, builders, and interior designers to improve market penetration. Investments in sustainable materials, enhanced durability, and space-efficient product designs are also becoming key competitive differentiators. In addition, businesses are pursuing acquisitions, collaborations, and regional expansion initiatives to broaden their customer base and access emerging construction markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Material

- 2.2.4 Mechanism

- 2.2.5 Installation type

- 2.2.6 End-user

- 2.2.7 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid urbanization & shrinking living spaces driving space-saving solutions

- 3.2.1.2 Rising residential & commercial construction activity globally

- 3.2.1.3 Growing adoption of minimalist & open-concept interior design

- 3.2.1.4 Increasing demand for ADA-compliant & barrier-free accessibility solutions

- 3.2.1.5 Smart home integration & demand for motorized door systems

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Intense competition from barn doors & bifold door alternatives

- 3.2.2.2 Raw material price volatility (timber, aluminum, glass)

- 3.2.2.3 Lack of consumer awareness in middle-income & developing markets

- 3.2.2.4 Variability in installer skill levels leading to inconsistent outcomes

- 3.2.3 Opportunities

- 3.2.3.1 Rising demand for acoustic/soundproof pocket door systems

- 3.2.3.2 Micro-apartment & compact urban housing boom creating structural demand

- 3.2.3.3 Growing adoption of fire-rated pocket doors in commercial buildings

- 3.2.3.4 Eco-friendly & recycled material innovations aligning with green building codes

- 3.2.3.5 Untapped demand in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Trade data analysis (HS Code 4418.2)

- 3.7.1 Import/export volume & value trends

- 3.7.2 Key trade corridors & tariff impact

- 3.8 Pricing analysis

- 3.8.1 Historical price trend analysis (driven by primary research)

- 3.8.2 Pricing strategy by player type (premium / value / mass market)

- 3.9 Impact of AI & generative AI on the market

- 3.9.1 AI-driven disruption of existing business models

- 3.9.2 GenAI use cases & adoption roadmap by segment

- 3.9.3 Risks, limitations & regulatory considerations

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Single pocket door

- 5.3 Double pocket door

- 5.4 Unilateral pocket door

Chapter 6 Market Estimates & Forecast, By Material, 2022 - 2035, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Wood

- 6.3 Glass

- 6.4 Aluminum/metal

- 6.5 Vinyl/plastic

- 6.6 Others (steel, fiberglass)

Chapter 7 Market Estimates & Forecast, By Mechanism, 2022 - 2035, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Manual

- 7.3 Automatic

Chapter 8 Market Estimates & Forecast, By Installation Type, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 New construction

- 8.3 Retrofit/renovation

Chapter 9 Market Estimates & Forecast, By End-Use, 2022 - 2035, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

- 9.4 Industrial

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 Online

- 10.2.1 E-commerce websites

- 10.2.2 Company-owned websites

- 10.3 Offline

- 10.3.1 Specialty stores

- 10.3.2 Departmental stores

- 10.3.3 Others

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Indonesia

- 11.4.7 Malaysia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Top Global Players

- 12.1.1 ASSA ABLOY Group

- 12.1.2 Eclisse Srl

- 12.1.3 Hafele GmbH

- 12.1.4 Johnson Hardware

- 12.1.5 Scrigno S.p.A.

- 12.2 Regional Champions

- 12.2.1 Anderson Corporation

- 12.2.2 Portman Doors

- 12.2.3 JB Kind

- 12.2.4 Ferrero Legno

- 12.2.5 Cavity Sliders

- 12.3 Emerging Players

- 12.3.1 Raydoor Inc.

- 12.3.2 Bertolotto Porte

- 12.3.3 LPD Doors

- 12.3.4 Linvisibile

- 12.3.5 Hettich Holding