|

시장보고서

상품코드

1774599

수면무호흡증 기기 시장 : 제품별, 연령층별, 성별, 최종사용자별, 지역별 - 예측(-2032년)Sleep Apnea Devices Market by Product: Therapeutic (PAP [CPAP, APAP, BPAP], Oral Appliances, Masks), Diagnostic (PSG, Home Sleep Testing, Oximeter), Age, Gender, End User (Sleep Clinics, Hospitals, Home Care Settings) - Global Forecast to 2032 |

||||||

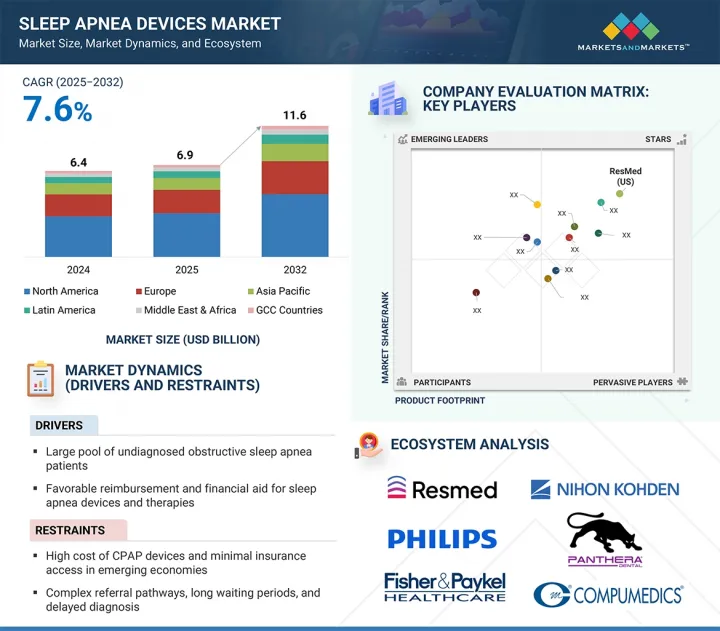

수면무호흡증 기기 시장 규모는 2025년에 69억 3,000만 달러로 추정되며, 예측 기간 동안 CAGR 7.6%로 성장하여 2032년에는 116억 1,000만 달러에 달할 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2024-2032년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2024-2032년 |

| 검토 단위 | 금액(10억 달러) |

| 부문 | 제품별, 연령층별, 성별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

수면무호흡증 기기는 수면 검사실, 임상 환경, 병원, 재택의료 등 다양한 곳에서 활용되며 수면 의료에 필수적인 요소로 자리 잡고 있습니다. 환자가 비침습적 대체 치료법을 찾는 경향이 증가함에 따라 지속적 양압기(CPAP) 및 양압기(BiPAP) 시장이 크게 성장하고 있습니다. 또한 신흥 시장, 특히 아시아태평양은 수면무호흡증에 대한 인식이 높아지고 의료 서비스에 대한 접근성이 개선되면서 유망한 성장 기회를 제공하고 있습니다.

시장은 치료 기기와 진단 기기의 두 가지 주요 부문으로 나뉩니다. 이 중 치료 기기 부문은 향후 예측 기간 동안 가장 큰 성장을 보일 것으로 예상됩니다. 이 부문에는 폐쇄성 수면무호흡증(OSA) 등의 치료에 일반적으로 사용되는 양압기(PAP) 등 다양한 제품이 포함됩니다. 또한, 효과적인 치료에 필수적인 페이스 마스크와 이러한 기기의 기능성과 편의성을 높여주는 다양한 액세서리도 포함됩니다. 수면 호흡 장애 상태를 관리하기 위해 고안된 구강 기기 역시 다른 혁신적인 치료 도구와 함께 이 부문에 포함됩니다. 치료 기기 부문의 예상 성장률은 주로 수면 관련 장애의 진단율 증가에 기인합니다. 이러한 진단율의 증가는 환자가 보다 쉽고 편리하게 진단을 받을 수 있는 가정용 수면 검사의 보급이 확대되고 있는 것이 주요 요인으로 작용하고 있습니다. 이러한 진단 방법을 통해 수면 문제를 발견하는 사람들이 늘어남에 따라 효과적인 치료 솔루션에 대한 수요가 급증하고 시장이 더욱 발전할 것으로 예상됩니다.

최종사용자(병원, 홈케어, 수면클리닉, 외래진료센터, 일차진료센터, 기타) 중 홈케어 설정 부문이 가장 빠른 속도로 성장할 것으로 예상됩니다. 재택의료 솔루션에 대한 관심이 높아지면서 의료 진단 및 치료 환경이 크게 변화하고 있습니다. 특히 재택 수면무호흡증 검사의 가용성 및 접근성 향상은 이러한 변화에 중요한 역할을 하고 있습니다. 이러한 기술 혁신은 수면 관련 장애를 앓고 있는 사람들이 보다 쉽고 편리하게 검사를 받을 수 있도록 도와줄 뿐만 아니라, 적시에 진단을 받을 수 있도록 돕고 있습니다. 그 결과, 환자들은 이전보다 훨씬 더 빨리 적절한 치료를 받을 수 있게 되었습니다. 이러한 추세는 환자들에게 도움이 될 뿐만 아니라, 인지도를 높이고 더 많은 사람들이 수면무호흡증 문제를 해결하기 위해 도움을 요청하도록 유도함으로써 전체 시장 확대에 기여하고 있으며, 궁극적으로 더 건강한 인구를 육성하는 데에도 기여하고 있습니다.

세계 시장은 5개 주요 지역(북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카)으로 구분됩니다. 아시아태평양은 예측 기간 동안 가장 높은 성장률을 보일 것으로 예상됩니다. 이러한 추세는 많은 제품 출시와 혁신적인 기기에 대한 규제 승인으로 인해 시장 제공이 강화되고 이 지역에서의 확장을 촉진하고 있기 때문입니다.

세계의 수면무호흡증 기기 시장에 대해 조사했으며, 제품별, 연령별, 성별, 최종사용자별, 지역별 동향, 시장 진입 기업 프로파일 등의 정보를 정리하여 전해드립니다.

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 주요 인사이트

제5장 시장 개요

- 소개

- 시장 역학

- 업계 동향

- 가격 분석

- 밸류체인 분석

- 공급망 분석

- 미충족 수요/최종사용자 기대

- Porter's Five Forces 분석

- 주요 이해관계자와 구입 기준

- 생태계 분석

- 규제 분석

- 특허 분석

- 인접 시장 분석

- 고객의 비즈니스에 영향을 미치는 동향/혼란

- 2025-2026년의 주요 회의와 이벤트

- 기술 분석

- 무역 분석

- 투자와 자금 조달 시나리오

- AI/생성형 AI가 수면무호흡증 기기 시장에 미치는 영향

- 2025년 미국 관세가 수면무호흡증 기기 시장에 미치는 영향

제6장 수면무호흡증 기기 시장(제품별)

- 소개

- 치료 기기

- 진단 기기

제7장 수면무호흡증 기기 시장(연령층별)

- 소개

- 소아

- 40세 미만

- 40-60세

- 60세 이상

제8장 수면무호흡증 기기 시장(성별)

- 소개

- 남성 환자

- 여성 환자

제9장 수면무호흡증 기기 시장(최종사용자별)

- 소개

- 병원

- 재택 케어

- 수면 클리닉

- 외래 진료 센터

- 프라이머리 센터

- 기타

제10장 수면무호흡증 기기 시장(지역별)

- 소개

- 북미

- 북미의 거시경제 전망

- 미국

- 캐나다

- 유럽

- 유럽의 거시경제 전망

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타

- 아시아태평양

- 아시아태평양의 거시경제 전망

- 중국

- 일본

- 호주

- 기타

- 라틴아메리카

- 라틴아메리카의 거시경제 전망

- 브라질

- 멕시코

- 기타

- 중동 및 아프리카

- 중동 및 아프리카의 거시경제 전망

- GCC 국가

- 기타

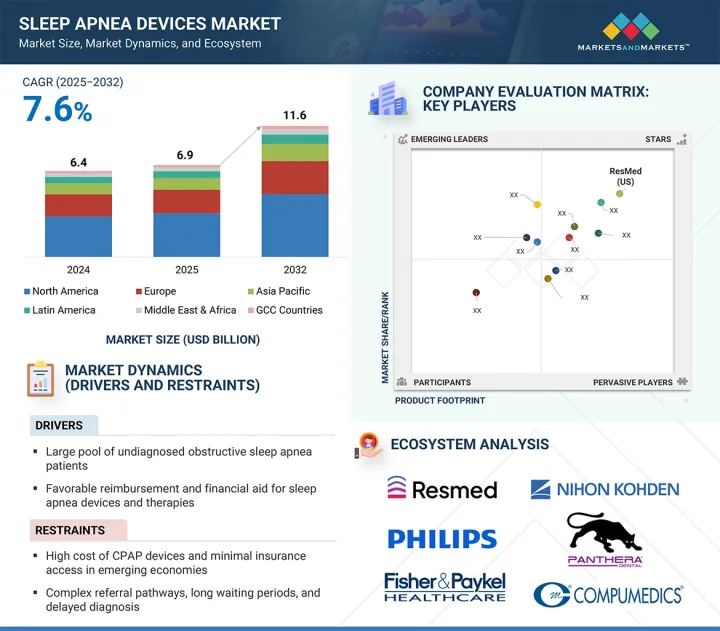

제11장 경쟁 구도

- 소개

- 주요 진출 기업의 전략/강점

- 매출 분석, 2020-2024년

- 시장 점유율 분석, 2024년

- 기업 평가 매트릭스 : 주요 진출 기업, 2024년

- 기업 평가 매트릭스 : 스타트업/중소기업, 2024년

- 기업 평가와 재무 지표

- 브랜드/제품 비교

- 경쟁 시나리오

제12장 기업 개요

- 주요 진출 기업

- RESMED

- KONINKLIJKE PHILIPS N.V.

- FISHER & PAYKEL HEALTHCARE LIMITED

- INSPIRE MEDICAL SYSTEMS, INC.

- SOMNOMED

- OPENAIRWAY

- COMPUMEDICS LIMITED

- LOWENSTEIN MEDICAL SE & CO. KG

- DRIVE DEVILBISS INTERNATIONAL

- BMC

- BRAEBON MEDICAL CORPORATION

- DYNAFLEX

- PANTHERA DENTAL

- MYERSON LLC

- PROSOMNUS SLEEP TECHNOLOGIES

- 기타 기업

- NIDEK MEDICAL INDIA

- TOMED GMBH

- LIVANOVA PLC

- INVACARE HOLDINGS CORPORATION

- MPOWRX HEALTH & WELLNESS PRODUCTS INC.

- NIHON KOHDEN CORPORATION

- SICAT GMBH & CO. KG

- VIVOS THERAPEUTICS, INC.

- AIRWAY MANAGEMENT

- APNEA SCIENCES

제13장 부록

ksm 25.07.29The sleep apnea devices market is valued at an estimated USD 6.93 billion in 2025 and is projected to reach USD 11.61 billion by 2032 at a CAGR of 7.6% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2023-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Units Considered | Value (USD billion) |

| Segments | Product, Age Group, Gender, and End User |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and Middle East & Africa |

Sleep apnea devices have become essential components in sleep medicine, utilized across avarious settings, including sleep laboratories, clinical environments, hospitals, and home care. As patients increasingly seek non-invasive therapeutic alternatives, the market for Continuous Positive Airway Pressure (CPAP) and Bilevel Positive Airway Pressure (BiPAP) machines is experiencing significant growth. Furthermore, emerging markets, particularly within the Asia Pacific region, present promising opportunities for expansion, driven by heightened awareness of sleep apnea and improved access to healthcare services.

"Therapeutic devices segment accounted for the highest growth rate in the sleep apnea devices market, by product, during the forecast period.

The market is divided into two main segments: therapeutic devices and diagnostic devices. Among these, the therapeutic devices segment is projected to experience the most significant growth during the upcoming forecast period. This segment encompasses a variety of products, including positive airway pressure (PAP) devices, which are commonly used to treat conditions such as obstructive sleep apnea (OSA). Additionally, it includes facial interfaces, also known as masks, that are essential for ensuring the effective delivery of therapy, as well as various accessories that enhance the functionality and comfort of these devices. Oral appliances designed to manage sleep-disordered breathing conditions also fall under this segment, along with other innovative therapeutic tools. The anticipated growth of the therapeutic devices segment is primarily driven by an increase in diagnosis rates for sleep-related disorders. This rise in diagnoses is largely supported by the growing adoption of home sleep tests, which provide a more accessible and convenient means for patients to undergo evaluation. As more individuals become aware of their sleep issues through these diagnostic methods, the demand for effective therapeutic solutions is expected to surge, further propelling the market forward.

"The home care settings segment accounted for the highest growth rate in the sleep apnea devices market, by end user, during the forecast period."

Among end users-hospitals, home care settings, sleep clinics, ambulatory care centers, primary centers, and others-the home care settings segment is projected to grow at the fastest rate. The growing trend towards home-based healthcare solutions is significantly transforming the landscape of medical diagnostics and treatment. In particular, the enhanced availability and accessibility of at-home sleep apnea testing is playing a crucial role in this shift. These innovations not only facilitate easier and more convenient testing for individuals suffering from sleep-related disorders but also lead to timely diagnoses. As a result, patients are able to receive appropriate treatment much faster than before. This trend is not only beneficial for patients but is also contributing to the overall expansion of the market by increasing awareness and encouraging more people to seek help for their sleep apnea concerns, ultimately fostering a healthier population.

"The Asia Pacific is expected to be the fastest-growing region in the sleep apnea devices market."

The global market for human identification technologies is segmented into five key regions: North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa. The Asia Pacific region is projected to experience the most significant growth rate throughout the forecast period. This trend can be attributed to the high volume of product launches and the regulatory approvals for innovative devices, which are enhancing market offerings and driving expansion in the area.

The break-up of the profile of primary participants in the sleep apnea devices market:

- By Company Type: Tier 1 - 5%, Tier 2 - 55%, and Tier 3 -40%

- By Designation: C-level - 37%, D-level - 48%, and Others - 15%

- By Region: North America - 56%, Europe - 20%, Asia Pacific - 17%, Rest of the World - 7%

The key players in this market are ResMed (US), Koninklijke Philips N.V. (Netherlands), Fisher & Paykel Healthcare Limited (New Zealand), Inspire Medical Systems, Inc. (US), SomnoMed (Australia), Openairway (Canada), Compumedics Limited (Australia), Lowenstein Medical SE & Co. KG (Germany), Drive DeVilbiss International (US), BMC (China), BRAEBON Medical Corporation (Canada), DynaFlex (US), Panthera Dental (Canada), Myerson LLC (US), ProSomnus Sleep Technologies (US), Nidek Medical India (India), Tomed GmbH (Germany), LivaNova PLC (UK), Invacare Holdings Corporation (US), MPowrx Health & Wellness Products Inc. (Canada), Nihon Kohden Corporation (Japan), SICAT GmbH & Co. Kg (Germany), Vivos Therapeutics, Inc. (US), Airway Management (US), and Apnea Sciences (US).

Research Coverage:

This research report categorizes the sleep apnea devices market by product [Therapeutic devices (PAP devices, facial interfaces, accessories, oral appliances, other therapeutic devices), Diagnostic devices (PSG Devices, home sleep testing devices, oximeters, actigraphy systems, sleep screening devices)], by end user [hospitals, home care settings, sleep clinics, ambulatory care centers, primary centers, and other end users], by age group [pediatric, below 40 years, 40-60 years, and above 60 years], by gender [male patients and female patients], and by region [North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa]. The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, opportunities, and challenges influencing the growth of the sleep apnea devices market. A detailed analysis of the key industry players has been done to provide insights into their business overview, solutions, key strategies, acquisitions, and agreements. New product & service launches and recent developments associated with the sleep apnea devices market. This report covers a competitive analysis of upcoming startups in the sleep apnea devices market ecosystem.

Reasons to buy this report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall sleep apnea devices market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, opportunities, and challenges.

The report provides insights on the following pointers:

- Analysis of key drivers (large pool of undiagnosed obstructive sleep apnea patients, favorable reimbursement and financial aid for sleep apnea devices and therapies, growing awareness about effects of untreated sleep apnea among patients, rising use of oral appliances among patients with mild-to-moderate sleep apnea, increased investments and funding to develop advanced sleep apnea products), restraints (high cost of CPAP devices and minimal insurance access in emerging economies, complex referral pathways, long waiting periods, and delayed diagnosis, and use of alternative therapies and medications for sleep apnea), opportunities (rising demand for cost-effective home sleep apnea tests, increasing focus on telemedicine, mHealth, and artificial intelligence, high growth opportunities for sleep apnea manufacturers in emerging economies) and challenges (poor patient compliance with CPAP therapy) influencing the growth of the sleep apnea devices market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the sleep apnea devices market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the sleep apnea devices market across varied regions.

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the sleep apnea devices market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players such as ResMed (US), Koninklijke Philips N.V. (Netherlands), and Fisher & Paykel Healthcare Limited (New Zealand).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 RESEARCH DESIGN

- 2.1.2 SECONDARY DATA

- 2.1.2.1 List of key secondary sources

- 2.1.2.2 Key data from secondary sources

- 2.1.2.3 Objectives of secondary research

- 2.1.3 PRIMARY DATA

- 2.1.3.1 List of key primaries

- 2.1.3.2 Objectives of primary research

- 2.1.3.3 Key industry insights

- 2.1.3.4 Key data from primary sources

- 2.1.3.5 Breakdown of primary interviews

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.1.1 Company revenue estimation approach

- 2.2.1.2 Company presentations and primary interviews

- 2.2.1.3 Patient-based approach for sleep apnea oral appliances market sizing

- 2.2.1.4 Disease burden approach for PAP devices market sizing

- 2.2.1.5 Growth forecast

- 2.2.1.6 CAGR projections

- 2.2.2 TOP-DOWN APPROACH

- 2.2.1 BOTTOM-UP APPROACH

- 2.3 DATA TRIANGULATION

- 2.4 MARKET SHARE ANALYSIS

- 2.5 STUDY ASSUMPTIONS

- 2.5.1 MARKET ASSUMPTIONS

- 2.5.2 GROWTH RATE ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

- 2.7 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 SLEEP APNEA DEVICES MARKET OVERVIEW

- 4.2 SLEEP APNEA DEVICES MARKET, BY PRODUCT

- 4.3 NORTH AMERICA: SLEEP APNEA DEVICES MARKET, BY PRODUCT AND COUNTRY

- 4.4 SLEEP APNEA DEVICES MARKET: REGIONAL MARKET SHARE

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Large pool of undiagnosed obstructive sleep apnea (OSA) patients

- 5.2.1.2 Favorable reimbursement and financial aid for sleep apnea devices and therapies

- 5.2.1.3 Growing awareness about effects of untreated sleep apnea among patients

- 5.2.1.4 Rising use of oral appliances among patients with mild-to-moderate sleep apnea

- 5.2.1.5 Increased investments and funding to develop advanced sleep apnea products

- 5.2.2 RESTRAINTS

- 5.2.2.1 High cost of CPAP devices and minimal insurance access in emerging economies

- 5.2.2.2 Complex referral pathways, long waiting periods, and delayed diagnosis

- 5.2.2.3 Use of alternative therapies and medications for sleep apnea

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Rising demand for cost-effective home sleep apnea tests

- 5.2.3.2 Increasing focus on telemedicine, mHealth, and artificial intelligence

- 5.2.3.3 High growth opportunities for sleep apnea manufacturers in emerging economies

- 5.2.4 CHALLENGES

- 5.2.4.1 Poor patient compliance with CPAP therapy

- 5.2.1 DRIVERS

- 5.3 INDUSTRY TRENDS

- 5.3.1 RISING ADOPTION OF ADVANCED SLEEP APNEA DIAGNOSTIC AND THERAPEUTIC TECHNOLOGIES

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE TREND OF SLEEP APNEA DEVICES, BY REGION, 2023-2025

- 5.4.2 AVERAGE SELLING PRICE TREND OF SLEEP APNEA DEVICES, BY PRODUCT TYPE, 2023-2025

- 5.4.3 AVERAGE SELLING PRICE TREND OF SLEEP APNEA ORAL APPLIANCES, BY KEY PLAYER, 2023-2025

- 5.5 VALUE CHAIN ANALYSIS

- 5.6 SUPPLY CHAIN ANALYSIS

- 5.7 UNMET NEEDS/END-USER EXPECTATIONS

- 5.8 PORTER'S FIVE FORCES ANALYSIS

- 5.8.1 THREAT OF NEW ENTRANTS

- 5.8.2 THREAT OF SUBSTITUTES

- 5.8.3 BARGAINING POWER OF SUPPLIERS

- 5.8.4 BARGAINING POWER OF BUYERS

- 5.8.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.9 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.9.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.9.2 KEY BUYING CRITERIA

- 5.10 ECOSYSTEM ANALYSIS

- 5.10.1 ROLE IN ECOSYSTEM

- 5.11 REGULATORY ANALYSIS

- 5.11.1 REGULATORY FRAMEWORK

- 5.11.1.1 North America

- 5.11.1.1.1 US

- 5.11.1.1.1.1 Reimbursement scenario in US

- 5.11.1.1.2 Canada

- 5.11.1.1.1 US

- 5.11.1.2 Europe

- 5.11.1.3 Asia Pacific

- 5.11.1.3.1 Japan

- 5.11.1.3.2 China

- 5.11.1.3.3 India

- 5.11.1.3.4 Australia

- 5.11.1.1 North America

- 5.11.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.11.1 REGULATORY FRAMEWORK

- 5.12 PATENT ANALYSIS

- 5.12.1 INSIGHTS ON PATENT PUBLICATION TRENDS (TOP APPLICANTS/ JURISDICTION)

- 5.13 ADJACENT MARKET ANALYSIS

- 5.14 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.15 KEY CONFERENCES & EVENTS, 2025-2026

- 5.16 TECHNOLOGY ANALYSIS

- 5.16.1 KEY TECHNOLOGIES

- 5.16.1.1 PAP devices

- 5.16.2 ADJACENT TECHNOLOGIES

- 5.16.2.1 Oral appliances

- 5.16.3 COMPLEMENTARY TECHNOLOGIES

- 5.16.3.1 Daytime-Nighttime appliances

- 5.16.1 KEY TECHNOLOGIES

- 5.17 TRADE ANALYSIS

- 5.17.1 IMPORT DATA FOR HS CODE 901849, 2020-2024

- 5.17.2 EXPORT DATA FOR HS CODE 901849, 2020-2024

- 5.18 INVESTMENT & FUNDING SCENARIO

- 5.19 IMPACT OF AI/GEN AI ON SLEEP APNEA DEVICES MARKET

- 5.19.1 MARKET POTENTIAL FOR SLEEP APNEA ORAL APPLIANCES

- 5.19.2 FUTURE OF GENERATIVE AI IN SLEEP APNEA DEVICES MARKET

- 5.20 IMPACT OF 2025 US TARIFF ON SLEEP APNEA DEVICES MARKET

- 5.20.1 INTRODUCTION

- 5.20.2 KEY TARIFF RATES

- 5.20.3 PRICE IMPACT ANALYSIS

- 5.20.4 IMPACT ON COUNTRY/REGION

- 5.20.4.1 North America

- 5.20.4.1.1 US

- 5.20.4.2 Europe

- 5.20.4.2.1 Germany

- 5.20.4.2.2 UK and France

- 5.20.4.3 Asia Pacific

- 5.20.4.3.1 China

- 5.20.4.3.2 Japan

- 5.20.4.3.3 India

- 5.20.4.1 North America

- 5.20.5 IMPACT ON END-USE INDUSTRIES

- 5.20.5.1 Hospitals

- 5.20.5.2 Sleep clinics

- 5.20.5.3 Ambulatory surgery centers

- 5.20.5.4 Primary centres

- 5.20.5.5 Home care centers

- 5.20.5.6 Urgent care centers

6 SLEEP APNEA DEVICES MARKET, BY PRODUCT

- 6.1 INTRODUCTION

- 6.2 THERAPEUTIC DEVICES

- 6.2.1 PAP DEVICES

- 6.2.1.1 CPAP devices

- 6.2.1.1.1 Technological advancements and better reimbursement facilities to boost segment growth

- 6.2.1.2 APAP devices

- 6.2.1.2.1 Better customization facility to augment market growth

- 6.2.1.3 BPAP devices

- 6.2.1.3.1 Increased product recalls and more complex operations to lower adoption

- 6.2.1.1 CPAP devices

- 6.2.2 FACIAL INTERFACES

- 6.2.2.1 Masks

- 6.2.2.1.1 Full-face masks

- 6.2.2.1.1.1 Full-face masks to be most effective for mouth breathers

- 6.2.2.1.2 Nasal pillow masks

- 6.2.2.1.2.1 Greater patient compliance to support segment growth

- 6.2.2.1.3 Nasal masks

- 6.2.2.1.3.1 Ease of use and reduced claustrophobic nature to aid adoption

- 6.2.2.1.1 Full-face masks

- 6.2.2.2 Cushions

- 6.2.2.2.1 Better insurance coverage to propel segment growth

- 6.2.2.1 Masks

- 6.2.3 ACCESSORIES

- 6.2.3.1 Humidifier accessories

- 6.2.3.1.1 Humidifiers to open airways, decrease congestion, and encourage clearer breathing

- 6.2.3.2 Power accessories

- 6.2.3.2.1 Power accessories to manage uninterrupted sleep apnea therapy without power supply

- 6.2.3.3 Transportation accessories

- 6.2.3.3.1 Rising need to carry sleep apnea devices while traveling to spur segment growth

- 6.2.3.4 Communication accessories

- 6.2.3.4.1 Need for easy teleconsultations for remote patients to fuel segment growth

- 6.2.3.5 Chin restraints

- 6.2.3.5.1 Growing need for obstructive sleep apnea management with therapeutic devices to drive segment

- 6.2.3.6 Other accessories

- 6.2.3.1 Humidifier accessories

- 6.2.4 ORAL APPLIANCES

- 6.2.4.1 Mandibular advancement devices

- 6.2.4.1.1 Low-cost devices with maximum anterior tongue space to drive segment

- 6.2.4.2 Tongue-retaining devices

- 6.2.4.2.1 Need for more affordable and comfortable treatment options to support segment growth

- 6.2.4.3 Daytime-Nighttime appliances

- 6.2.4.3.1 Increased focus on comfortable, non-surgical, and low-risk treatments to drive segment

- 6.2.4.1 Mandibular advancement devices

- 6.2.5 OTHER THERAPEUTIC DEVICES

- 6.2.1 PAP DEVICES

- 6.3 DIAGNOSTIC DEVICES

- 6.3.1 PSG DEVICES

- 6.3.1.1 Ambulatory PSG devices

- 6.3.1.1.1 Need for cost-effective and technologically advanced ambulatory devices to propel segment growth

- 6.3.1.2 Clinical PSG devices

- 6.3.1.2.1 Labor-intensive and expensive procedures to limit segment

- 6.3.1.1 Ambulatory PSG devices

- 6.3.2 HOME SLEEP TESTING DEVICES

- 6.3.2.1 Increased need for cost-effective and comfortable home sleep testing devices to augment segment growth

- 6.3.3 OXIMETERS

- 6.3.3.1 Fingertip oximeters

- 6.3.3.1.1 Lack of precise reading due to injury or slow blood flow to limit segment growth

- 6.3.3.2 Handheld oximeters

- 6.3.3.2.1 Easy customizations and ease of distant reading to spur segment growth

- 6.3.3.3 Wrist-worn oximeters

- 6.3.3.3.1 Small size and easy portability for overnight monitoring to propel segment growth

- 6.3.3.4 Tabletop oximeters

- 6.3.3.4.1 Higher cost and fewer applications for personal use to decrease market share

- 6.3.3.1 Fingertip oximeters

- 6.3.4 ACTIGRAPHY SYSTEMS

- 6.3.4.1 Increased research on sleep and wake patterns to drive market

- 6.3.5 SLEEP SCREENING DEVICES

- 6.3.5.1 Increasing preference for home-based sleep apnea testing to propel market growth

- 6.3.1 PSG DEVICES

7 SLEEP APNEA DEVICES MARKET, BY AGE GROUP

- 7.1 INTRODUCTION

- 7.2 PEDIATRIC

- 7.2.1 PREVALENCE OF OBESITY, CRANIOFACIAL ABNORMALITIES, AND NEUROMUSCULAR DISORDERS TO PROPEL MARKET GROWTH

- 7.3 BELOW 40 YEARS

- 7.3.1 LOWER PREVALENCE OF SLEEP APNEA IN YOUNGER AGE GROUPS TO LIMIT MARKET GROWTH

- 7.4 40-60 YEARS

- 7.4.1 UNDERDIAGNOSIS AND UNHEALTHY LIFESTYLE TO AID MARKET GROWTH

- 7.5 ABOVE 60 YEARS

- 7.5.1 HIGH OCCURRENCE OF CHRONIC MEDICAL CONDITIONS AND SLEEP-RELATED DISORDERS TO DRIVE MARKET

8 SLEEP APNEA DEVICES MARKET, BY GENDER

- 8.1 INTRODUCTION

- 8.2 MALE PATIENTS

- 8.2.1 HIGHER PREVALENCE OF SLEEP-RELATED BREATHING DISORDERS TO BOOST MARKET GROWTH

- 8.3 FEMALE PATIENTS

- 8.3.1 IMPROVED RECOGNITION AND DIAGNOSIS OF OBSTRUCTIVE SLEEP APNEA TO AID MARKET GROWTH

9 SLEEP APNEA DEVICES MARKET, BY END USER

- 9.1 INTRODUCTION

- 9.2 HOSPITALS

- 9.2.1 INCREASED POPULARITY PRIVATE HOSPITALS WITH ADVANCED INFRASTRUCTURE TO AUGMENT MARKET GROWTH

- 9.3 HOME CARE SETTINGS

- 9.3.1 INCREASING PATIENT PREFERENCE FOR HOME-BASED SLEEP TESTS TO FUEL MARKET GROWTH

- 9.4 SLEEP CLINICS

- 9.4.1 INCREASING NEED FOR ADVANCED DIAGNOSTIC DEVICES AND SLEEP SPECIALISTS TO SUPPORT MARKET GROWTH

- 9.5 AMBULATORY CARE CENTERS

- 9.5.1 RISING ADOPTION OF PORTABLE DIAGNOSTIC DEVICES TO IMPROVE DIAGNOSIS AND TREATMENT IN OUTPATIENT SETTINGS

- 9.6 PRIMARY CENTERS

- 9.6.1 PRIMARY CENTERS TO CONDUCT FOLLOW-UP CARE AND COORDINATE PATIENTS WITH SLEEP SPECIALISTS

- 9.7 OTHER END USERS

10 SLEEP APNEA DEVICES MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 10.2.2 US

- 10.2.2.1 US to dominate North American sleep apnea devices market during forecast period

- 10.2.3 CANADA

- 10.2.3.1 Increasing number of research grants and health programs to propel market growth

- 10.3 EUROPE

- 10.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 10.3.2 GERMANY

- 10.3.2.1 High prevalence of obstructive sleep apnea and increased geriatric population to fuel market growth

- 10.3.3 UK

- 10.3.3.1 Rising awareness among patients about sleep apnea to support market growth

- 10.3.4 FRANCE

- 10.3.4.1 Rising geriatric population and obesity rates to favor market growth

- 10.3.5 ITALY

- 10.3.5.1 Favorable initiatives by dental associations and increased awareness about obstructive sleep apnea to drive market

- 10.3.6 SPAIN

- 10.3.6.1 Social awareness initiatives by regional organizations regarding obstructive sleep apnea to aid market growth

- 10.3.7 REST OF EUROPE

- 10.4 ASIA PACIFIC

- 10.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 10.4.2 CHINA

- 10.4.2.1 Growing prevalence of obesity and diabetes in adults to propel market growth

- 10.4.3 JAPAN

- 10.4.3.1 Favorable reimbursement scenario and high demand for cloud-connected sleep apnea therapeutic devices to aid market growth

- 10.4.4 AUSTRALIA

- 10.4.4.1 Increasing number of sleep clinics to augment market growth

- 10.4.5 REST OF ASIA PACIFIC

- 10.5 LATIN AMERICA

- 10.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 10.5.2 BRAZIL

- 10.5.2.1 Favorable reimbursement policies and increased awareness about sleeping disorders to drive market

- 10.5.3 MEXICO

- 10.5.3.1 Poor healthcare infrastructure and lack of public health initiatives to limit market growth

- 10.5.4 REST OF LATIN AMERICA

- 10.6 MIDDLE EAST & AFRICA

- 10.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 10.6.2 GCC COUNTRIES

- 10.6.2.1 Kingdom of Saudi Arabia

- 10.6.2.1.1 High obesity rates among women to propel market growth

- 10.6.2.2 UAE

- 10.6.2.2.1 Greater focus on early diagnosis and healthcare infrastructural advancements to drive market

- 10.6.2.3 Rest of GCC countries

- 10.6.2.1 Kingdom of Saudi Arabia

- 10.6.3 REST OF MIDDLE EAST & AFRICA

11 COMPETITIVE LANDSCAPE

- 11.1 INTRODUCTION

- 11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 11.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN SLEEP APNEA DEVICES MARKET

- 11.3 REVENUE ANALYSIS, 2020-2024

- 11.4 MARKET SHARE ANALYSIS, 2024

- 11.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 11.5.1 STARS

- 11.5.2 EMERGING LEADERS

- 11.5.3 PERVASIVE PLAYERS

- 11.5.4 PARTICIPANTS

- 11.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 11.5.5.1 Company footprint

- 11.5.5.2 Region footprint

- 11.5.5.3 Product footprint

- 11.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 11.6.1 PROGRESSIVE COMPANIES

- 11.6.2 RESPONSIVE COMPANIES

- 11.6.3 DYNAMIC COMPANIES

- 11.6.4 STARTING BLOCKS

- 11.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 11.6.5.1 Detailed list of key startups/SMEs

- 11.6.5.2 Competitive benchmarking of key startups/SMEs

- 11.7 COMPANY VALUATION & FINANCIAL METRICS

- 11.7.1 FINANCIAL METRICS

- 11.7.2 COMPANY VALUATION

- 11.8 BRAND/PRODUCT COMPARISON

- 11.9 COMPETITIVE SCENARIO

- 11.9.1 PRODUCT LAUNCHES & APPROVALS

- 11.9.2 DEALS

- 11.9.3 EXPANSIONS

- 11.9.4 OTHER DEVELOPMENTS

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 RESMED

- 12.1.1.1 Business overview

- 12.1.1.2 Products offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Product launches

- 12.1.1.3.2 Deals

- 12.1.1.3.3 Expansions

- 12.1.1.4 MnM view

- 12.1.1.4.1 Key strengths

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses & competitive threats

- 12.1.2 KONINKLIJKE PHILIPS N.V.

- 12.1.2.1 Business overview

- 12.1.2.2 Products offered

- 12.1.2.3 MnM view

- 12.1.2.3.1 Key strengths

- 12.1.2.3.2 Strategic choices

- 12.1.2.3.3 Weaknesses & competitive threats

- 12.1.3 FISHER & PAYKEL HEALTHCARE LIMITED

- 12.1.3.1 Business overview

- 12.1.3.2 Products offered

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Product launches

- 12.1.3.4 MnM view

- 12.1.3.4.1 Key strengths

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses & competitive threats

- 12.1.4 INSPIRE MEDICAL SYSTEMS, INC.

- 12.1.4.1 Business overview

- 12.1.4.2 Products offered

- 12.1.4.3 MnM view

- 12.1.4.3.1 Key strengths

- 12.1.4.3.2 Strategic choices

- 12.1.4.3.3 Weaknesses & competitive threats

- 12.1.5 SOMNOMED

- 12.1.5.1 Business overview

- 12.1.5.2 Products offered

- 12.1.5.3 MnM view

- 12.1.5.3.1 Key strengths

- 12.1.5.3.2 Strategic choices

- 12.1.5.3.3 Weaknesses & competitive threats

- 12.1.6 OPENAIRWAY

- 12.1.6.1 Business overview

- 12.1.6.2 Products offered

- 12.1.7 COMPUMEDICS LIMITED

- 12.1.7.1 Business overview

- 12.1.7.2 Products offered

- 12.1.7.3 Recent developments

- 12.1.7.3.1 Product approvals

- 12.1.8 LOWENSTEIN MEDICAL SE & CO. KG

- 12.1.8.1 Business overview

- 12.1.8.2 Products offered

- 12.1.9 DRIVE DEVILBISS INTERNATIONAL

- 12.1.9.1 Business overview

- 12.1.9.2 Products offered

- 12.1.10 BMC

- 12.1.10.1 Business overview

- 12.1.10.2 Products offered

- 12.1.11 BRAEBON MEDICAL CORPORATION

- 12.1.11.1 Business overview

- 12.1.11.2 Products offered

- 12.1.12 DYNAFLEX

- 12.1.12.1 Business overview

- 12.1.12.2 Products offered

- 12.1.12.3 Recent developments

- 12.1.12.3.1 Deals

- 12.1.13 PANTHERA DENTAL

- 12.1.13.1 Business overview

- 12.1.13.2 Products offered

- 12.1.13.3 Recent developments

- 12.1.13.3.1 Deals

- 12.1.13.3.2 Other developments

- 12.1.14 MYERSON LLC

- 12.1.14.1 Business overview

- 12.1.14.2 Products offered

- 12.1.15 PROSOMNUS SLEEP TECHNOLOGIES

- 12.1.15.1 Business overview

- 12.1.15.2 Products offered

- 12.1.15.3 Recent developments

- 12.1.15.3.1 Deals

- 12.1.1 RESMED

- 12.2 OTHER PLAYERS

- 12.2.1 NIDEK MEDICAL INDIA

- 12.2.2 TOMED GMBH

- 12.2.3 LIVANOVA PLC

- 12.2.4 INVACARE HOLDINGS CORPORATION

- 12.2.5 MPOWRX HEALTH & WELLNESS PRODUCTS INC.

- 12.2.6 NIHON KOHDEN CORPORATION

- 12.2.7 SICAT GMBH & CO. KG

- 12.2.8 VIVOS THERAPEUTICS, INC.

- 12.2.9 AIRWAY MANAGEMENT

- 12.2.10 APNEA SCIENCES

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS