|

시장보고서

상품코드

1777935

컴퓨터 지원 엔지니어링(CAE) 시장 : 제공 제품별, 전개 모드별, 조직 규모별, 업계별, 지역별 - 예측(-2030년)Computer-aided Engineering (CAE) Market by Software (FEA, CFD, Multibody Dynamics (MBD), Electromagnetics, Optimization & Simulation), Service, Vertical (Automotive, A&D, Healthcare & Life Sciences, Energy & Process), Region - Global Forecast to 2030 |

||||||

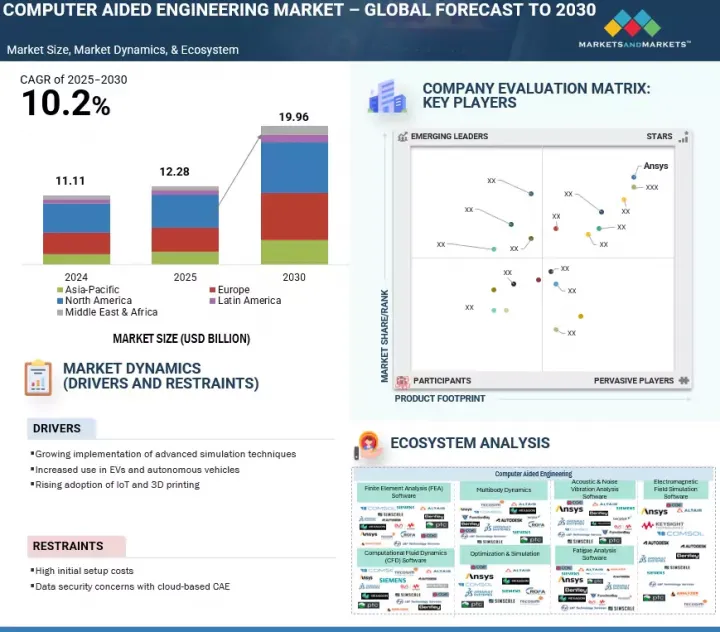

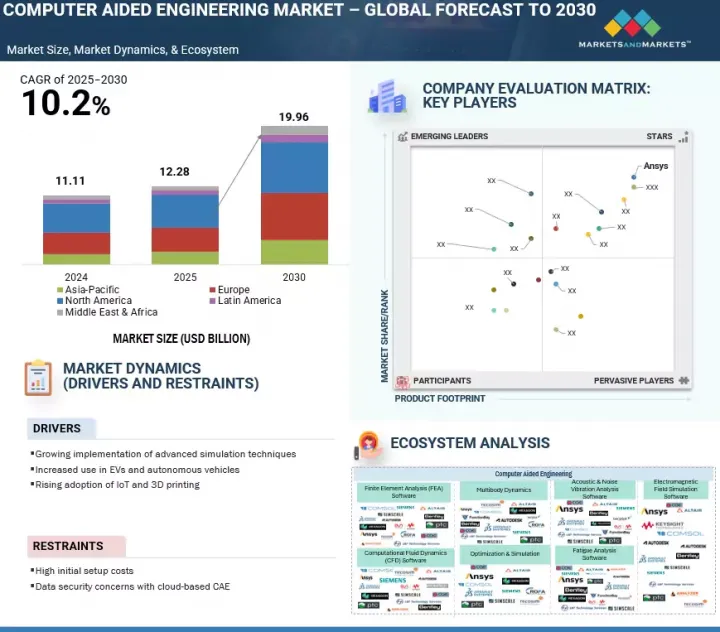

세계의 컴퓨터 지원 엔지니어링(CAM) 시장 규모는 2025년 122억 8,000만 달러에서 2030년에는 199억 6,000만 달러로 성장하고, 예측 기간 중 연평균 복합 성장률(CAGR)은 10.2%를 보일 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2019-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 검토 단위 | 금액(100만 달러/10억 달러) |

| 부문별 | 제공 제품별, 전개 모드별, 조직 규모별, 업계별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카 |

주요 시장 성장 촉진요인은 시뮬레이션 기반 제품 개발의 채택이 증가하고 있다는 점입니다. 이를 통해 엔지니어들은 개발 사이클의 초기 단계에서 설계를 가상적으로 테스트, 최적화, 검증할 수 있습니다. 특히 자동차, 항공우주, 전자기기 등 산업에서는 비용이 많이 드는 물리적 프로토타입의 필요성이 감소하고, 시장 출시까지의 시간이 단축되며, 제품 성능이 향상됩니다.

"산업별로는 법 집행 분야가 예측 기간 동안 가장 높은 CAGR을 기록할 것으로 예상됩니다."

의료 기기 설계, 생체역학 모델링, 개인 맞춤형 헬스케어 솔루션에서 시뮬레이션 활용이 증가하고 있으며, CAE 툴은 임플란트, 보철물, 수술기구의 안전성, 유효성 및 규제 준수를 보장하기 위한 가상 테스트에 활용되고 있습니다. 기술 혁신, 환자 맞춤형 치료, 헬스케어 기술에 대한 R&D 투자에 대한 중요성이 강조되면서 이 분야에서의 CAE 도입이 가속화되고 있습니다.

"지역별로는 북미가 가장 큰 시장 점유율을 차지할 것으로 추정됩니다."

북미는 강력한 기술 기반, 시뮬레이션 툴의 조기 도입, Ansys, MathWorks, Altair와 같은 주요 플레이어의 집중으로 인해 CAE 시장을 선도하고 있습니다. 이 지역은 시뮬레이션 기반 제품 개발이 중요한 자동차, 항공우주, 헬스케어 분야에서 대규모 투자가 이루어지고 있습니다. 또한, 스마트 제조 및 디지털 엔지니어링에 대한 정부의 지원은 미국과 캐나다의 CAE 수요를 더욱 촉진하고 있습니다.

이 보고서는 CAE 시장을 소프트웨어 툴(유한요소해석(FEA), 수치유체역학(CFD), 다중체역학(MBD), 최적화 및 시뮬레이션, 전자기학(EM), 음향 및 소음진동, 피로해석 등 기타 소프트웨어 유형)과 서비스(컨설팅 및 교육, 구축 및 통합, 컨설팅 및 교육, 도입 및 통합)로 구분하여 분석합니다. 컨설팅 및 교육, 도입 및 통합, 지원 및 유지보수)로 분류하여 시장 규모를 예측하고 있습니다. 도입 형태별로는 클라우드와 온프레미스로 구분됩니다. 조직 규모별로는 중소기업(SMEs)과 대기업(Large Enterprises)으로 구분되며, CAE 시장 대상 업종으로는 자동차, 항공우주/방산, 전자/반도체, 중장비, 헬스케어/생명과학, AEC(건축, 엔지니어링, 건설), 에너지/프로세스, 에너지/공정, 의료/생명과학, AEC(건축, 엔지니어링, 건설)로 분류됩니다. 건설), 에너지/공정, 해양/선박, 기타 업종(광업, 교육, 운송/물류)이 포함됩니다. 지역별로는 북미, 유럽, 아시아 태평양, 중동 및 아프리카, 라틴 아메리카로 구분됩니다.

또한 시장 주요 기업의 상세한 경쟁 분석, 기업 프로필, 제품 및 사업 제공에 대한 주요 견해, 최근 동향, 주요 시장 전략에 대한 정보를 제공합니다.

이 보고서에서는 CAE 시장을 소프트웨어 도구(유한 요소 분석(FEA), 수치 유체 역학(CFD), 다중 체동역학(MBD), 최적화 및 시뮬레이션, 전자기학(EM), 음향·소음 진동 분석 및 피로 분석 등 기타 소프트웨어 유형)와 서비스(컨설팅 및 교육, 도입 및 통합, 지원 및 유지보수)로 분류하여 시장 규모를 예측하고 있습니다. 도입 형태별로 시장은 클라우드와 온프레미스로 분류됩니다. 조직 규모별로는 중소기업(SME)와 대기업(Large Enterprises)로 나뉩니다. CAE 시장의 대상 산업에는 자동차, 항공우주 및 방위, 전자 및 반도체, 중장비, 헬스케어 및 생명과학, AEC(건축, 공학, 건설), 에너지 및 프로세스, 온쇼어 및 오프쇼어, 기타 산업(광업, 교육, 운송 및 물류)이 포함됩니다. 시장은 지역별로 북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카로 구분됩니다.

또한, 시장의 주요 기업에 대한 상세한 경쟁 분석, 기업 프로필, 제품 및 사업 제공에 대한 주요 견해, 최근 동향, 주요 시장 전략도 수록되어 있습니다.

이 보고서는 다음과 같은 사항에 대한 통찰을 제공합니다:

- 성장 촉진요인

- 고급 시뮬레이션 기술의 도입 확대

- 전기차(EV) 및 자율주행 차량에서의 활용 증가

- IoT 및 3D 프린팅 기술의 도입 확대

- 성장 저해요인

- 높은 초기 설정 비용

- 클라우드 기반 CAE에서의 데이터 보안 문제

- 기회

- AI를 활용한 시뮬레이션과 생성적 디자인

- CAE와 디지털 트윈 및 인더스트리 4.0과의 통합

- 과제

- 다중물리학 시뮬레이션의 복잡성

- 플랫폼 간 상호 운용성 문제

- 제품 개발/혁신: CAE 시장에서의 미래 기술, 연구 개발 활동, 신규 제품 및 서비스 출시와 관련된 상세한 분석 및 통찰력

- 시장 개척: 유리한 시장에 대한 포괄적인 정보 - 다양한 지역의 CAE 시장을 분석하고 있습니다.

- 시장 다각화: CAE 시장 내 신제품 및 서비스, 미개척 지역, 최근 동향, 투자 관련 상세한 정보를 제공합니다.

- 경쟁사 평가: Ansys(미국), Autodesk(미국), Dassault Systemes(프랑스), Hexagon AB(스웨덴), Siemens(독일), MathWorks(미국), PTC(미국), COMSOL(스웨덴), Keysight(미국), Honeywell(미국), Bentley Systems(미국), Emerson(미국), AspenTech(미국), CAE, Inc.(캐나다), SimScale(독일), Gamma Technologies(미국), Tecosim(독일), Echleon CAE(독일), ESPL(인도), BETA CAE Systems(스위스), Prometech Software(일본), Rescale(미국), ESRD(미국), nTopology(미국), SimulationPlus(미국), Rafinex(룩셈부르크), AirShaper(벨기에), ToffeeX(영국) 등이 CAE 시장에 진출해 있습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 프리미엄 인사이트

제5장 시장 개요와 업계 동향

- 서론

- 시장 역학

- 생성형 AI가 컴퓨터 지원 엔지니어링(CAE) 시장에 미치는 영향

- 가격 분석

- 기술 분석

- 고객의 비즈니스에 영향을 미치는 동향/혼란

- 사례 연구 분석

- 컴퓨터 지원 엔지니어링 진화

- 밸류체인 분석

- 생태계 분석

- Porter의 Five Forces 분석

- 주요 이해관계자와 구입 기준

- 특허 분석

- 규제 상황

- 2025년 주요 컨퍼런스 및 이벤트

- 투자 및 자금조달 시나리오

- 2025년 미국 관세의 영향 - 컴퓨터 지원 엔지니어링(CAE) 시장

제6장 컴퓨터 지원 엔지니어링(CAE) 시장(제공 제품별)

- 서론

- 소프트웨어 툴

- 서비스

제7장 컴퓨터 지원 엔지니어링(CAE) 시장(전개 모드별)

- 서론

- 클라우드

- On-Premise

제8장 컴퓨터 지원 엔지니어링(CAE) 시장(조직 규모별)

- 서론

- 중소기업

- 대기업

제9장 컴퓨터 지원 엔지니어링(CAE) 시장(업계별)

- 서론

- 자동차

- 항공우주 및 방위

- 헬스케어 및 생명과학

- 일렉트로닉스 및 반도체

- 건축, 엔지니어링 및 건설(AEC)

- 해양 및 오프쇼어

- 중공업 장비

- 에너지 및 프로세스

- 기타

제10장 컴퓨터 지원 엔지니어링(CAE) 시장(지역별)

- 서론

- 북미

- 북미 : 거시경제 전망

- 북미 : 컴퓨터 지원 엔지니어링(CAE) 시장 성장 촉진요인

- 미국

- 캐나다

- 유럽

- 유럽 : 거시경제 전망

- 유럽 : 컴퓨터 지원 엔지니어링(CAE) 시장 성장 촉진요인

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타

- 아시아태평양

- 아시아태평양 : 거시경제 전망

- 아시아태평양 : 컴퓨터 지원 엔지니어링(CAE) 시장 성장 촉진요인

- 중국

- 일본

- 인도

- 싱가포르

- 기타

- 중동 및 아프리카

- 중동 및 아프리카 : 거시경제 전망

- 중동 및 아프리카 : 컴퓨터 지원 엔지니어링(CAE) 시장 성장 촉진요인

- GCC 국가

- 남아프리카

- 기타

- 라틴아메리카

- 라틴아메리카 : 거시경제 전망

- 라틴아메리카 : 컴퓨터 지원 엔지니어링(CAE) 시장 성장 촉진요인

- 브라질

- 멕시코

- 기타

제11장 경쟁 구도

- 주요 시장 진출기업의 전략/강점, 2022년-2024년

- 매출 분석, 2020년-2024년

- 시장 점유율 분석, 2024년

- 브랜드 비교

- 기업 평가와 재무 지표

- 기업 평가 매트릭스 : 주요 시장 진출기업, 2024년

- 기업 평가 매트릭스 : 스타트업/중소기업, 2024년

- 경쟁 시나리오

제12장 기업 개요

- 주요 시장 진출기업

- DASSAULT SYSTEMES

- MATHWORKS

- SIEMENS+ALTAIR

- ANSYS+SYNOPSYS

- KEYSIGHT

- HEXAGON AB(MSC SOFTWARE)

- AUTODESK

- CAE

- EMERSON

- COMSOL

- PTC

- HONEYWELL

- BETA CAE SYSTEMS(CADENCE)

- ASPENTECH

- 기타 기업

- SIMSCALE

- TECOSIM

- PROMETECH SOFTWARE

- GAMMA TECHNOLOGIES

- ECHLEON CAE

- ESPL

- RESCALE

- ESRD

- NTOPOLOGY

- SIMULATIONSPLUS

- RAFINEX

- AIRSHAPER

- TOFFEEX

제13장 인접 시장

제14장 부록

LSH 25.08.01The CAE market is projected to grow from USD 12.28 billion in 2025 to USD 19.96 billion by 2030 at a CAGR of 10.2% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2019-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million/USD Billion) |

| Segments | By Offering, Deployment Mode, Organization Size, Vertical, and Region. |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, and Latin America |

A key market driver is the rising adoption of simulation-driven product development, which enables engineers to virtually test, optimize, and validate designs early in the development cycle. This reduces the need for costly physical prototypes, shortens time to market, and enhances product performance, especially in industries like automotive, aerospace, and electronics.

"By vertical, the law enforcement segment is projected to register the highest CAGR during the forecast period."

This growth is driven by the increasing use of simulation in medical device design, biomechanical modeling, and personalized healthcare solutions. CAE tools are being adopted for virtual testing of implants, prosthetics, and surgical equipment to ensure safety, efficacy, and regulatory compliance. The growing emphasis on innovation, patient-specific treatments, and R&D investments in healthcare technology is accelerating CAE adoption in this vertical.

"By region, North America is estimated to account for the largest market share."

North America leads the CAE market due to its strong technological infrastructure, early adoption of simulation tools, and a high concentration of key players such as Ansys, MathWorks, and Altair. The region benefits from significant investments in the automotive, aerospace, and healthcare sectors, where simulation-driven product development is critical. Additionally, government support for smart manufacturing and digital engineering initiatives further fuels CAE demand across the US and Canada.

Breakdown of Primaries

The study contains insights from various industry experts, from component suppliers to Tier 1 companies and OEMs. The break-up of the primaries is as follows:

- By Company Type: Tier 1 - 40%, Tier 2 - 35%, and Tier 3 - 25%

- By Designation: C-level - 45%, Directors - 35%, and Managers - 20%

- By Region: North America - 55%, Europe - 25%, Asia Pacific - 15%, RoW - 5%

The key players in the CAE market include Ansys (US), Autodesk (US), Dassault Systemes (France), Hexagon AB (Sweden), Siemens (Germany), MathWorks (US), PTC (US), COMSOL (Sweden), Keysight US), Honeywell (US), Bentley Systems (US), Emerson (US), AspenTech (US), CAE, Inc. (Canada), SimScale (Germany), and others.

The study includes an in-depth competitive analysis of the key players in the CAE market, their company profiles, recent developments, and key market strategies.

Research Coverage

The report segments the CAE market and forecasts its size by offering into Software Tools [Finite Element Analysis (FEA), Computational Fluid Dynamics (CFD), Multibody Dynamics (MBD), Optimization & Simulation, Electromagnetics (EM), and other software types, such as Acoustic & Noise Vibration Analysis and Fatigue Analysis] and Services (Consulting & Training, Deployment & Integration, Support & Maintenance). By deployment mode, the market is divided into Cloud and On-premises. Based on organization size, the market is segmented into Small and Medium Enterprises (SMEs) and Large Enterprises. The verticals covered in the CAE market include Automotive, Aerospace & Defense, Electronics & Semiconductors, Heavy Machinery Equipment, Healthcare & Life Sciences, AEC (Architecture, Engineering, and Construction), Energy & Process, Marine & Offshore, and Other Verticals (Mining, Education, and Transportation & Logistics). The market is segmented by region into North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America.

The study also includes an in-depth competitive analysis of the market's key players, their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report

The report will help the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall CAE market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (growing implementation advanced simulation techniques, increased use in EVs and autonomous vehicles, rising adoption of IoT and 3D printing), restraints (high initial setup costs, data security concerns with cloud-based CAE), opportunities (AI-powered simulation and generative design, integration of CAE with digital twin and Industry 4.0), and challenges (complexity of multiphysics simulations, interoperability issues across platforms).

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the CAE market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the CAE market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the CAE market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as Ansys (US), Autodesk (US), Dassault Systemes (France), Hexagon AB (Sweden), Siemens (Germany), MathWorks (US), PTC (US), COMSOL (Sweden), Keysight US), Honeywell (US), Bentley Systems (US), Emerson (US), AspenTech (US), CAE, Inc. (Canada), SimScale (Germany), Gamma Technologies (US), Tecosim (Germany), Echleon CAE (Germany), ESPL (India), BETA CAE Systems (Switzerland), Prometech Software (Japan), Rescale (US), ESRD (US), nTopology (US), SimulationPlus (US), Rafinex (Luxembourg), AirShaper (Belgium), and ToffeeX (UK), among others, in the CAE market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 YEARS CONSIDERED

- 1.3.3 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Breakup of primaries

- 2.1.2.2 Key industry insights

- 2.2 MARKET BREAKUP AND DATA TRIANGULATION

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 TOP-DOWN APPROACH

- 2.3.2 BOTTOM-UP APPROACH

- 2.4 MARKET FORECAST

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN COMPUTER-AIDED ENGINEERING MARKET

- 4.2 COMPUTER-AIDED ENGINEERING MARKET, BY OFFERING

- 4.3 COMPUTER-AIDED ENGINEERING MARKET, BY SOFTWARE TOOL

- 4.4 COMPUTER-AIDED ENGINEERING MARKET, BY DEPLOYMENT MODE

- 4.5 COMPUTER-AIDED ENGINEERING MARKET, BY ORGANIZATION SIZE

- 4.6 COMPUTER-AIDED ENGINEERING MARKET, BY VERTICAL

- 4.7 MARKET INVESTMENT SCENARIO

5 MARKET OVERVIEW AND INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Increasing implementation of advanced simulation techniques

- 5.2.1.2 Growing use in EVs and autonomous vehicles

- 5.2.1.3 Rising adoption of IoT and 3D printing

- 5.2.2 RESTRAINTS

- 5.2.2.1 High initial setup costs

- 5.2.2.2 Data security concerns with cloud-based CAE

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 AI-powered simulation and generative design

- 5.2.3.2 Integration with digital twin and Industry 4.0

- 5.2.4 CHALLENGES

- 5.2.4.1 Complexity of multiphysics simulations

- 5.2.4.2 Interoperability issues across platforms

- 5.2.4.3 Shortage of skilled simulation professionals

- 5.2.1 DRIVERS

- 5.3 IMPACT OF GENERATIVE AI ON COMPUTER-AIDED ENGINEERING MARKET

- 5.3.1 GENERATIVE AI

- 5.3.2 TOP USE CASES AND MARKET POTENTIAL IN CAE MARKET

- 5.3.3 IMPACT OF GENERATIVE AI ON INTERCONNECTED AND ADJACENT ECOSYSTEMS

- 5.3.3.1 Computer-aided design (CAD)

- 5.3.3.2 Product lifecycle management (PLM)

- 5.3.3.3 High-performance computing (HPC) & cloud computing

- 5.3.3.4 Additive manufacturing (3D printing)

- 5.3.3.5 Digital twin and industrial IoT (IIoT)

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE OF SOFTWARE TOOLS, BY KEY PLAYER, 2024

- 5.4.2 INDICATIVE PRICING ANALYSIS, BY OFFERING, 2024

- 5.5 TECHNOLOGY ANALYSIS

- 5.5.1 KEY TECHNOLOGIES

- 5.5.2 ADJACENT TECHNOLOGIES

- 5.5.3 COMPLEMENTARY TECHNOLOGIES

- 5.6 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.7 CASE STUDY ANALYSIS

- 5.7.1 ADVANCED CFD SIMULATIONS ELEVATE SKI LIFT SAFETY AND EFFICIENCY FOR DOPPELMAYR

- 5.7.2 POLIMI MOTORCYCLE FACTORY LEVERAGES 3DEXPERIENCE FOR RACING SUCCESS

- 5.7.3 DOCUSIGN ESIGNATURE UPHELD IN COURT AS LEGAL AND ENFORCEABLE IN COMMON LAW JURISDICTIONS

- 5.8 EVOLUTION OF COMPUTER-AIDED ENGINEERING

- 5.8.1 INTRODUCTION

- 5.8.2 EARLY DAYS OF CAE TOOLS

- 5.8.3 EVOLUTION AND ADVANCEMENT IN CAE TOOLS

- 5.8.4 MODERN CAE SOLUTIONS AND THEIR IMPACT

- 5.8.5 CONCLUSION

- 5.9 VALUE CHAIN ANALYSIS

- 5.10 ECOSYSTEM ANALYSIS

- 5.11 PORTER'S FIVE FORCES ANALYSIS

- 5.11.1 THREAT OF NEW ENTRANTS

- 5.11.2 BARGAINING POWER OF SUPPLIERS

- 5.11.3 BARGAINING POWER OF BUYERS

- 5.11.4 THREAT OF SUBSTITUTES

- 5.11.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.12 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.12.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.12.2 BUYING CRITERIA

- 5.13 PATENT ANALYSIS

- 5.14 REGULATORY LANDSCAPE

- 5.14.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.14.2 REGULATORY FRAMEWORK

- 5.14.2.1 German Civil Code

- 5.14.2.2 Simulation Interoperability Standards Organization (SISO)

- 5.14.2.3 International Nursing Association for Clinical Simulation and Learning (INACSL)

- 5.14.2.4 European Chemicals Agency (ECHA)

- 5.14.2.5 Open Geospatial Consortium (OGC)

- 5.15 KEY CONFERENCES AND EVENTS, 2025

- 5.16 INVESTMENT AND FUNDING SCENARIO

- 5.17 IMPACT OF 2025 US TARIFF - COMPUTER-AIDED ENGINEERING MARKET

- 5.17.1 INTRODUCTION

- 5.17.2 KEY TARIFF RATES

- 5.17.3 PRICE IMPACT ANALYSIS

- 5.17.4 IMPACT ON COUNTRY/REGION

- 5.17.4.1 North America

- 5.17.4.1.1 US

- 5.17.4.1.2 Canada

- 5.17.4.1.3 Mexico

- 5.17.4.2 Europe

- 5.17.4.2.1 Germany

- 5.17.4.2.2 France

- 5.17.4.2.3 UK

- 5.17.4.3 Asia Pacific

- 5.17.4.3.1 China

- 5.17.4.3.2 India

- 5.17.4.3.3 Japan

- 5.17.4.1 North America

- 5.17.5 IMPACT ON END-USE INDUSTRIES

6 COMPUTER-AIDED ENGINEERING MARKET, BY OFFERING

- 6.1 INTRODUCTION

- 6.1.1 OFFERING: COMPUTER-AIDED ENGINEERING MARKET DRIVERS

- 6.2 SOFTWARE TOOLS

- 6.2.1 ENHANCING PRODUCT DEVELOPMENT WITH ADVANCED CAE SOFTWARE TOOLS

- 6.2.2 FINITE ELEMENT ANALYSIS (FEA)

- 6.2.3 COMPUTATIONAL FLUID DYNAMICS (CFD)

- 6.2.4 MULTIBODY DYNAMICS

- 6.2.5 OPTIMIZATION & SIMULATION

- 6.2.6 ELECTROMAGNETICS (EM)

- 6.2.7 OTHER SOFTWARE TOOLS

- 6.3 SERVICES

- 6.3.1 MAXIMIZING ENGINEERING EFFICIENCY WITH COMPREHENSIVE CAE SERVICES

- 6.3.2 CONSULTING & TRAINING

- 6.3.3 DEPLOYMENT & INTEGRATION

- 6.3.4 SUPPORT & MAINTENANCE

7 COMPUTER-AIDED ENGINEERING MARKET, BY DEPLOYMENT MODE

- 7.1 INTRODUCTION

- 7.1.1 DEPLOYMENT MODE: COMPUTER-AIDED ENGINEERING MARKET DRIVERS

- 7.2 CLOUD

- 7.2.1 ENABLING SCALABILITY AND COLLABORATION THROUGH CLOUD DEPLOYMENT

- 7.3 ON-PREMISES

- 7.3.1 ENSURING CONTROL AND CUSTOMIZATION WITH ON-PREMISES DEPLOYMENT

8 COMPUTER-AIDED ENGINEERING MARKET, BY ORGANIZATION SIZE

- 8.1 INTRODUCTION

- 8.1.1 ORGANIZATION SIZE: COMPUTER-AIDED ENGINEERING MARKET DRIVERS

- 8.2 SMES

- 8.2.1 DRIVING INNOVATION AND COST EFFICIENCY IN SMES THROUGH CAE

- 8.3 LARGE ENTERPRISES

- 8.3.1 ENHANCING PRODUCT DEVELOPMENT AND INNOVATION IN LARGE ENTERPRISES THROUGH CAE

9 COMPUTER-AIDED ENGINEERING MARKET, BY VERTICAL

- 9.1 INTRODUCTION

- 9.1.1 VERTICAL: COMPUTER-AIDED ENGINEERING MARKET DRIVERS

- 9.2 AUTOMOTIVE

- 9.2.1 DRIVING EFFICIENCY IN AUTOMOTIVE DESIGN USING CAE TOOLS

- 9.3 AEROSPACE & DEFENSE

- 9.3.1 ACCELERATING AEROSPACE INNOVATION WITH CAE-POWERED DESIGN AND SIMULATION

- 9.4 HEALTHCARE & LIFE SCIENCES

- 9.4.1 STRENGTHENING SAFETY, REDUCING DEVELOPMENT CYCLE, AND SUPPORTING REGULATORY APPROVAL WITH CAE

- 9.5 ELECTRONICS & SEMICONDUCTOR

- 9.5.1 DRIVING PRECISION IN ELECTRONICS & SEMICONDUCTORS THROUGH SIMULATION

- 9.6 ARCHITECTURE, ENGINEERING & CONSTRUCTION (AEC)

- 9.6.1 ENHANCING DESIGN AND STRUCTURAL INTEGRITY IN AEC INDUSTRY USING CAE TOOLS

- 9.7 MARINE & OFFSHORE

- 9.7.1 SIMULATING HARSH ENVIRONMENTS FOR SAFER AND EFFICIENT MARINE & OFFSHORE OPERATIONS

- 9.8 HEAVY INDUSTRIAL EQUIPMENT

- 9.8.1 ENGINEERING DURABILITY AND PERFORMANCE OF HEAVY INDUSTRIAL EQUIPMENT USING CAE

- 9.9 ENERGY & PROCESS

- 9.9.1 DRIVING OPERATIONAL EXCELLENCE IN ENERGY & PROCESS INDUSTRY THROUGH MULTIPHYSICS SIMULATION

- 9.10 OTHER VERTICALS

10 COMPUTER-AIDED ENGINEERING MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 NORTH AMERICA: MACROECONOMIC OUTLOOK

- 10.2.2 NORTH AMERICA: COMPUTER-AIDED ENGINEERING MARKET DRIVERS

- 10.2.3 US

- 10.2.3.1 Increasing adoption across high-tech manufacturing sectors to drive market

- 10.2.4 CANADA

- 10.2.4.1 Rising demand in engineering-intensive industries to drive market

- 10.3 EUROPE

- 10.3.1 EUROPE: MACROECONOMIC OUTLOOK

- 10.3.2 EUROPE: COMPUTER-AIDED ENGINEERING MARKET DRIVERS

- 10.3.3 UK

- 10.3.3.1 Growing implementation in high-precision industries to drive market

- 10.3.4 GERMANY

- 10.3.4.1 Growing use in automotive, machinery, aerospace, and industrial equipment sectors to drive market

- 10.3.5 FRANCE

- 10.3.5.1 Rising demand in innovation-driven industries to fuel market

- 10.3.6 ITALY

- 10.3.6.1 Increasing adoption in design and manufacturing ecosystem to drive market

- 10.3.7 REST OF EUROPE

- 10.4 ASIA PACIFIC

- 10.4.1 ASIA PACIFIC: MACROECONOMIC OUTLOOK

- 10.4.2 ASIA PACIFIC: COMPUTER-AIDED ENGINEERING MARKET DRIVERS

- 10.4.3 CHINA

- 10.4.3.1 Accelerating CAE adoption in China's ambitious manufacturing drive

- 10.4.4 JAPAN

- 10.4.4.1 Strong adoption in engineering sectors to drive demand

- 10.4.5 INDIA

- 10.4.5.1 Expanding engineering R&D ecosystem and strong government support to drive market

- 10.4.6 SINGAPORE

- 10.4.6.1 Strategic deployment in smart manufacturing, aerospace MRO, urban planning, and precision electronics to drive market

- 10.4.7 REST OF ASIA PACIFIC

- 10.5 MIDDLE EAST & AFRICA

- 10.5.1 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

- 10.5.2 MIDDLE EAST & AFRICA: COMPUTER-AIDED ENGINEERING MARKET DRIVERS

- 10.5.3 GCC COUNTRIES

- 10.5.3.1 UAE

- 10.5.3.1.1 Increasing adoption to power innovation and smart industry to drive market

- 10.5.3.2 KSA

- 10.5.3.2.1 Growing implementation to support Vision 2030 and industrial growth to drive market

- 10.5.3.3 Rest of GCC Countries

- 10.5.3.1 UAE

- 10.5.4 SOUTH AFRICA

- 10.5.4.1 Rising adoption to strengthen engineering and industrial innovation to drive market

- 10.5.5 REST OF MIDDLE EAST & AFRICA

- 10.6 LATIN AMERICA

- 10.6.1 LATIN AMERICA: MACROECONOMIC OUTLOOK

- 10.6.2 LATIN AMERICA: COMPUTER-AIDED ENGINEERING MARKET DRIVERS

- 10.6.3 BRAZIL

- 10.6.3.1 Increasing focus on advanced manufacturing and infrastructure innovation to drive market

- 10.6.4 MEXICO

- 10.6.4.1 Increasing CAE integration to support automotive and electronics leadership

- 10.6.5 REST OF LATIN AMERICA

11 COMPETITIVE LANDSCAPE

- 11.1 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2024

- 11.2 REVENUE ANALYSIS, 2020-2024

- 11.3 MARKET SHARE ANALYSIS, 2024

- 11.4 BRAND COMPARISON

- 11.5 COMPANY VALUATION AND FINANCIAL METRICS

- 11.5.1 COMPANY VALUATION

- 11.5.2 FINANCIAL METRICS

- 11.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 11.6.1 STARS

- 11.6.2 EMERGING LEADERS

- 11.6.3 PERVASIVE PLAYERS

- 11.6.4 PARTICIPANTS

- 11.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 11.6.5.1 Company footprint

- 11.6.5.2 Region footprint

- 11.6.5.3 Offering footprint

- 11.6.5.4 Vertical footprint

- 11.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 11.7.1 PROGRESSIVE COMPANIES

- 11.7.2 RESPONSIVE COMPANIES

- 11.7.3 DYNAMIC COMPANIES

- 11.7.4 STARTING BLOCKS

- 11.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 11.7.5.1 Detailed list of key startups/SMEs

- 11.7.5.2 Competitive benchmarking of key startups

- 11.8 COMPETITIVE SCENARIO

- 11.8.1 PRODUCT LAUNCHES/ENHANCEMENTS

- 11.8.2 DEALS

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 DASSAULT SYSTEMES

- 12.1.1.1 Business overview

- 12.1.1.2 Products/Solutions/Services offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Deals

- 12.1.1.4 MnM view

- 12.1.1.4.1 Right to win

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses and competitive threats

- 12.1.2 MATHWORKS

- 12.1.2.1 Business overview

- 12.1.2.2 Products/Solutions/Services offered

- 12.1.2.3 Recent developments

- 12.1.2.3.1 Product launches/enhancements

- 12.1.2.3.2 Deals

- 12.1.2.4 MnM view

- 12.1.2.4.1 Right to win

- 12.1.2.4.2 Strategic choices

- 12.1.2.4.3 Weaknesses and competitive threats

- 12.1.3 SIEMENS+ALTAIR

- 12.1.3.1 Business overview

- 12.1.3.2 Products/Solutions/Services offered

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Product launches/enhancements

- 12.1.3.3.2 Deals

- 12.1.3.4 MnM view

- 12.1.3.4.1 Right to win

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses and competitive threats

- 12.1.4 ANSYS+SYNOPSYS

- 12.1.4.1 Business overview

- 12.1.4.2 Products/Solutions/Services offered

- 12.1.4.3 Recent developments

- 12.1.4.3.1 Product launches/enhancements

- 12.1.4.3.2 Deals

- 12.1.4.4 MnM view

- 12.1.4.4.1 Right to win

- 12.1.4.4.2 Strategic choices

- 12.1.4.4.3 Weaknesses and competitive threats

- 12.1.5 KEYSIGHT

- 12.1.5.1 Business overview

- 12.1.5.2 Products/Solutions/Services offered

- 12.1.5.3 Recent developments

- 12.1.5.3.1 Product launches/enhancements

- 12.1.5.3.2 Deals

- 12.1.5.4 MnM view

- 12.1.5.4.1 Right to win

- 12.1.5.4.2 Strategic choices

- 12.1.5.4.3 Weaknesses and competitive threats

- 12.1.6 HEXAGON AB (MSC SOFTWARE)

- 12.1.6.1 Business overview

- 12.1.6.2 Products/Solutions/Services offered

- 12.1.6.3 Recent developments

- 12.1.6.3.1 Product launches/enhancements

- 12.1.6.3.2 Deals

- 12.1.7 AUTODESK

- 12.1.7.1 Business overview

- 12.1.7.2 Products/Solutions/Services offered

- 12.1.7.3 Recent developments

- 12.1.7.3.1 Product launches/enhancements

- 12.1.7.3.2 Deals

- 12.1.8 CAE

- 12.1.8.1 Business overview

- 12.1.8.2 Products/Solutions/Services offered

- 12.1.8.3 Recent developments

- 12.1.8.3.1 Product launches/enhancements

- 12.1.8.3.2 Deals

- 12.1.9 EMERSON

- 12.1.9.1 Business overview

- 12.1.9.2 Products/Solutions/Services offered

- 12.1.9.3 Recent developments

- 12.1.9.3.1 Product launches/enhancements

- 12.1.9.3.2 Deals

- 12.1.10 COMSOL

- 12.1.10.1 Business overview

- 12.1.10.2 Products/Solutions/Services offered

- 12.1.10.3 Recent developments

- 12.1.10.3.1 Product launches/enhancements

- 12.1.11 PTC

- 12.1.12 HONEYWELL

- 12.1.13 BETA CAE SYSTEMS (CADENCE)

- 12.1.14 ASPENTECH

- 12.1.1 DASSAULT SYSTEMES

- 12.2 OTHER KEY PLAYERS

- 12.2.1 SIMSCALE

- 12.2.2 TECOSIM

- 12.2.3 PROMETECH SOFTWARE

- 12.2.4 GAMMA TECHNOLOGIES

- 12.2.5 ECHLEON CAE

- 12.2.6 ESPL

- 12.2.7 RESCALE

- 12.2.8 ESRD

- 12.2.9 NTOPOLOGY

- 12.2.10 SIMULATIONSPLUS

- 12.2.11 RAFINEX

- 12.2.12 AIRSHAPER

- 12.2.13 TOFFEEX

13 ADJACENT MARKETS

- 13.1 INTRODUCTION TO ADJACENT MARKETS

- 13.1.1 LIMITATIONS

- 13.2 SIMULATION SOFTWARE MARKET

- 13.3 COMPUTER-AIDED MANUFACTURING (CAM) MARKET

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 CUSTOMIZATION OPTIONS

- 14.4 RELATED REPORTS

- 14.5 AUTHOR DETAILS