|

시장보고서

상품코드

1780342

금속화 연포장 시장 예측(-2030년) : 재료 유형별, 구조별, 포장 유형별, 최종 용도 산업별, 지역별Metalized Flexible Packaging Market by Material Type, Structure, Packaging Type, End-Use Industry & Region - Global Forecast to 2030 |

||||||

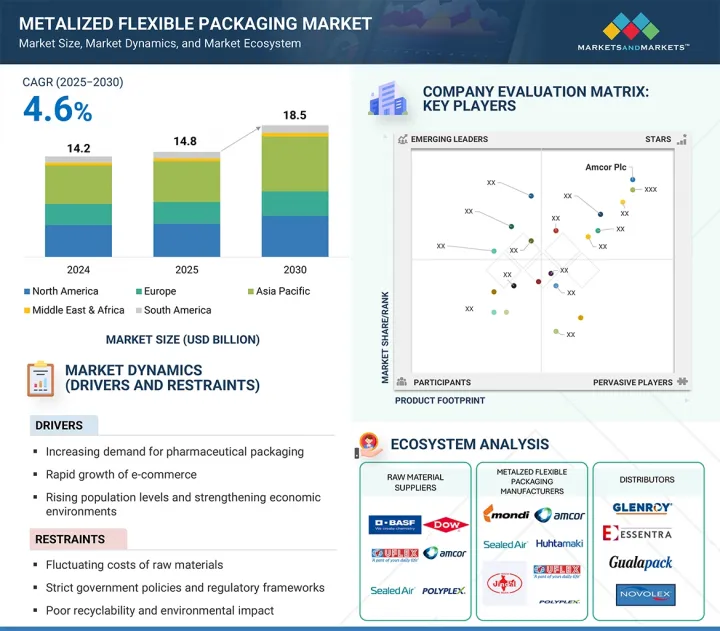

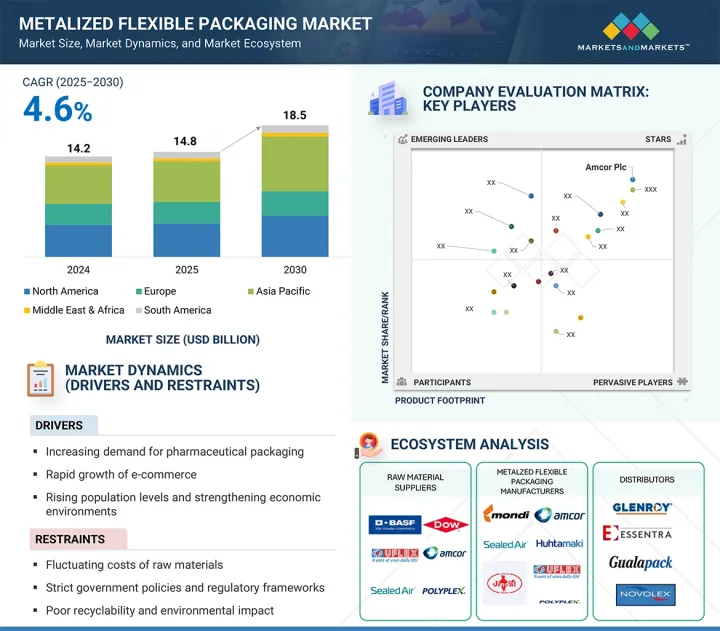

세계의 금속화 연포장 시장 규모는 2025년 148억 달러에서 2030년까지 185억 달러에 달할 것으로 추정되며, CAGR로 4.6%의 성장이 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상연도 | 2021-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 금액(100만 달러), 킬로톤 |

| 부문 | 재료 유형, 구조, 포장 유형, 최종 용도 산업, 지역 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미 |

금속화 연포장 산업은 제품 유통기한을 연장할 수 있는 가볍고 장벽이 높은 포장에 대한 수요 증가, E-Commerce 및 D2C 소매 시장의 성장, 식품, 퍼스널케어 및 반려동물 사료 부문에서 보다 매력적이고 사용하기 쉬운 포장의 인기 증가, 습기, 산소 및 빛으로부터 보호하는 의약품에 대한 사용 증가로 인해 성장할 것으로 예측됩니다. 증가로 인해 예측 기간 중 확대될 가능성이 높습니다. 또한 신흥경제국에서는 가처분소득이 증가하고 라이프스타일이 진화하고 있으며, 소비가 많다는 특징이 있습니다.

재료 유형별로는 Allox/SiOx PET가 예측 기간 중 가장 빠르게 성장할 것으로 예측됩니다.

Alox/SiOx PET는 유연성, 투명성, 재활용성을 유지하면서도 기존 알루미늄 포일에 비해 산소, 습기, 향기에 대한 차단성이 매우 높아 금속화 연포장 시장에서 가장 빠르게 성장하고 있는 소재입니다. PET에 적용된 초박막 무기 코팅을 통해 브랜드는 스탠드업 파우치 및 파우치에서 볼 수 있듯이 제품의 가시성, 고품질 그래픽 및 구조적 강도를 실현할 수 있습니다. 이러한 미관, 보존성, 지속가능한 가격의 조합은 소비자의 기대치가 높아지고 식품 안전, 유통기한 연장, 순환 경제에 부합하는 포장 시스템에 대한 규제기관의 요구사항이 점점 더 엄격해짐에 따라 Allox/SiOx PET와 같은 통기성 포장 구조는 향후 또한 향후 선호되는 연포장재가 될 것입니다.

구조별로는 단층 압출 구조 부문이 예측 기간 중 가장 빠르게 성장한 부문을 차지했습니다.

금속화 연포장 시장에서 가장 빠르게 성장하고 있는 것은 단층 압출 구조입니다. 이 브랜드는 단층 기반의 금속화를 통해 기존 라미네이트와 동일한 수준의 습기 및 산소 보호 및 내광성을 달성합니다. 또한 기존 라미네이트에 비해 재활용이 단순화되어 소비자의 기대에 부응할 수 있습니다. 단층 압출 필름은 또한 생산 비용 효율이 높고, 파우치, 봉지, 뚜껑 등 다양한 포장 형태에 사용할 수 있으며, 식품, 애완동물 케어, 퍼스널케어, 퍼스널케어, 의약품 포장에 비용과 편의성 측면에서 이상적인 선택입니다.

포장 유형별로는 파우치 부문이 예측 기간 중 가장 빠르게 성장하고 있습니다.

파우치는 올인원 하이 배리어 기능뿐만 아니라 편의성, 제품 판매 매력도, 다용도성, 효율성 등의 이점을 소비자에게 제공하므로 금속화 연포장 산업에서 가장 성장세가 활발한 포장 형태로서 매우 호조세를 보이고 있습니다. 얇고 휴대가 간편한 디자인으로 운반과 보관이 용이하며, 지퍼락, 티어노치, 스파우트 등의 측면은 깔끔하게 휴대하고 사용하는 현재 소비자 동향에 맞게 디자인되었습니다. 금속화 코팅은 매장과 E-Commerce에서 개봉시 광택과 시각적 매력을 더하고 식품, 애완동물 케어, 퍼스널케어, 건강 보조 식품 산업에서 다양한 용도로 사용되면서 전 세계에서 빠르게 시장에 침투하고 있습니다.

세계의 금속화 연포장 시장에 대해 조사분석했으며, 주요 촉진요인과 억제요인, 경쟁 구도, 향후 동향 등의 정보를 제공하고 있습니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 중요한 인사이트

- 금속화 연포장 시장에서의 매력적인 기회

- 금속화 연포장 시장 : 재료별

- 금속화 연포장 시장 : 구조별

- 금속화 연포장 시장 : 포장 유형별

- 금속화 연포장 시장 : 최종 용도 산업별

- 아시아태평양의 금속화 연포장 시장 : 최종 용도 산업별, 국가별

- 금속화 연포장 시장 : 주요 국가별

제5장 시장 개요

- 서론

- 시장 역학

- 촉진요인

- 억제요인

- 기회

- 과제

- 고객 비즈니스에 영향을 미치는 동향/혼란

- 에코시스템 분석

- 밸류체인 분석

- 규제 상황

- 규제 상황

- 주요 규제

- 가격 분석

- 주요 기업의 평균 판매 가격 동향 : 최종 용도 산업별(2024년)

- 평균 판매 가격 동향 : 지역별(2021-2030년)

- 무역 분석

- 수출 시나리오(HS 코드 7607)

- 수입 시나리오(HS 코드 7607)

- 기술 분석

- 주요 기술

- 보완 기술

- 인접 기술

- 특허 분석

- 사례 연구 분석

- GSK용으로 개발된 새로운 블리스터 포장 기술

- Celplast, 산업 수요에 대응하는 보다 경량의 재활용 가능한 고차단성 포장 솔루션을 개발

- 주요 이해관계자와 구입 기준

- 주요 컨퍼런스와 이벤트(2025-2026년)

- 투자와 자금조달 시나리오

- 금속화 연포장 시장에 대한 생성형 AI/AI의 영향

- Porter's Five Forces 분석

- 거시경제 분석

- 서론

- GDP의 동향과 예측(2021-2028년)

- 금속화 연포장 시장에 대한 2025년 미국 관세의 영향

- 서론

- 주요 관세율

- 가격의 영향 분석

- 국가/지역에 대한 영향

- 최종 용도 산업에 대한 영향

제6장 금속화 연포장 시장 : 최종 용도 산업별

- 서론

- 식품

- 음료

- 퍼스널케어

- 의약품

- 애완동물 사료

- 기타 최종 용도 산업

제7장 금속화 연포장 시장 : 재료별

- 서론

- 알루미늄 포일계 연포장

- 금속화 필름 연포장

- ALOX/SIOX PP

- ALOX/SIOX PET

- 기타 ALOX/SIOX 금속화 연포장

제8장 금속화 연포장 시장 : 포장 유형별

- 서론

- 파우치

- 백

- 랩

- 롤스톡

- 기타 포장 유형

제9장 금속화 연포장 시장 : 구조별

- 서론

- 적층 구조

- 단층 압출 구조

- 기타 구조

제10장 금속화 연포장 시장 : 지역별

- 서론

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- GCC 국가

- 남아프리카공화국

- 기타 중동 및 아프리카

제11장 경쟁 구도

- 개요

- 주요 참여 기업의 전략/강점

- 매출 분석(2020-2024년)

- 시장 점유율 분석(2024년)

- 기업의 평가와 재무 지표

- 브랜드/제품의 비교

- 기업 평가 매트릭스 : 주요 기업(2024년)

- 기업 평가 매트릭스 : 스타트업/중소기업(2024년)

- 경쟁 시나리오

제12장 기업 개요

- 주요 기업

- AMCOR PLC

- MONDI

- SEALED AIR CORPORATION

- HUHTAMAKI OYJ

- TOPPAN HOLDINGS INC.

- TRANSCONTINENTAL INC.

- POLYPLEX CORPORATION LIMITED

- COSMO FIRST LIMITED

- UFLEX LIMITED

- JPFL FILMS PRIVATE LIMITED

- 기타 기업

- ESTER INDUSTRIES LIMITED

- CONSTANTIA FLEXIBLES

- TAGHLEEF INDUSTRIES

- POLINAS

- DUNMORE

- GR(SHANDONG) NEW MATERIAL CO., LTD.

- SHANGHAI RUITU NEW MATERIALS TECHNOLOGY CO., LTD.

- XIAMEN CHANGSU INDUSTRIAL CO., LTD.

- CELPLAST METALLIZED PRODUCTS LIMITED

- ULTIMET FILMS LIMITED

- ACCRUED PLASTIC LTD.

- ALL FOILS, INC.

- MANUCOR SPA

- SRF LIMITED

- KAVERI METALLISING & COATING IND. PRIVATE LIMITED

제13장 인접 시장과 관련 시장

- 서론

- 제한 사항

제14장 부록

KSA 25.08.07The market for metalized flexible is estimated to grow from USD 14.8 billion in 2025 to USD 18.5 billion in 2030 at a CAGR of 4.6%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million) and Volume (Kiloton) |

| Segments | Material Type, Structure, Packaging Type, End-use Industry, and Region |

| Regions covered | North America, Asia Pacific, Europe, Middle East & Africa, and South America |

The metalized flexible packaging industry is likely to expand during the forecast period due to the increasing demand for lightweight yet high-barrier packaging that extends the shelf life of products, the growth of e-commerce and direct-to-consumer retail markets, the rising popularity of more attractive and user-friendly packaging in the food, personal care, and pet food segments, and the growing use in pharmaceuticals that protect against moisture, oxygen, and light. Furthermore, emerging economies are characterized by high consumption, as their disposable incomes have risen and their lifestyles are evolving.

By material type, Alox/SiOx PET accounted for the fastest-growing segment during the forecast period.

Alox/SiOx PET is the fastest-growing type of material in the metallized flexible packaging market, as it provides an exceptional high barrier to oxygen, moisture, and fragrances compared to traditional aluminum foil, while still maintaining flexibility, clarity, and recyclability. Its ultra-thin inorganic coatings applied to PET allow brands to achieve product visibility, high-quality graphics, and structural strength, as seen in stand-up pouches and sachets. This combination of aesthetics, shelf performance, and sustainable pricing is poised to meet the growing consumer expectations and increasingly stringent requirements set by regulatory bodies regarding food safety, extended shelf life, and packaging systems that align with the circular economy, where aerated packaging structures, such as Alox/SiOx PET, become the preferred future-proof flexible packaging material.

By structure, the mono-extruded structures segment accounted for the fastest-growing segment during the forecast period.

The fastest-growing segment within the metalized flexible packaging market is mono-extruded structures, as they effectively combine high-barrier capabilities with full recyclability in a single material film. Brands achieve the same level of protection against moisture and oxygen, and against light, as a traditional laminate, due to the metallization of a mono-layer base. Additionally, recycling is simplified and aligned with consumer expectations compared to a traditional laminate; the only difference in effectiveness lies in moisture resistance. Mono-extruded films are also cost-effective to manufacture and versatile for various packaging forms, such as pouches, sachets, and lidding, making them an ideal choice for cost and convenience in food, pet care, personal care, and pharmaceutical packaging.

By packaging type, the pouches segment was the fastest-growing segment during the forecast period

Pouches are performing exceptionally well as the packaging format with the most active growth in the metalized flexible packaging industry since pouches present an all-in-one high barrier functionality, as well as the benefit of convenience, product sales attractiveness, versatility, and efficiency to the consumer. Their thin portable design makes shipping and storage cheaper, and aspects such as zip-locks, tear notches, and spouts are designed to be able to meet the current consumer trend of portable use with no mess. The metalised coating adds gloss and visual appeal on-shelf and in e-commerce unboxing, and its versatile applications in food, pet care, personal care, and nutraceutical industries have led to its swift market penetration throughout the world.

By end-use industry, the pet food segment accounted for the highest CAGR during the forecast period

The fastest-growing end-use in the metalized flexible packaging market is pet food, as it has been reported that pet owners are actively seeking high-quality, convenient, and smelly-free packaging that retains pet treats, food in wet form, and supplements so that they do not spoil and metalized stand-up pouches that reseal address these requirements to ensure there is good barrier protection, high portability, and shelf presence, both in-store and online.

By region, Asia Pacific is projected to account for the highest CAGR during the forecast period.

The fastest growing metalized flexible packaging market is Asia Pacific, driven by rapid urbanization and a surging middle-income consumer base that creates high demand for packaged and convenience food, personal care, pharmaceutical, and pet care products. This trend is further supported by the remarkable rise of e-commerce and DTC retail, investments in regional manufacturing infrastructure, and the development of metalized packaging designed to protect while being lightweight and appealing to various industries.

- By Company Type: Tier 1: 25%, Tier 2: 42%, Tier 3: 33%

- By Designation: C Level: 20%, Director Level: 30%, Others: 50%

- By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, Middle East & Africa: 20%, and South America: 10%.

Companies Covered:

Amcor plc (Switzerland), Mondi Plc (UK), Sealed Air Corporation (US), Huhtamaki Oyj (Finland), Transcontinental Inc. (Canada), and Polyplex Corporation Ltd. (India) are some key players in the metalized flexible packaging market.

Research Coverage

The market study examines the metalized flexible packaging market across various segments. It aims to estimate the market size and growth potential across different segments based on material type, structure, packaging type, end-use industry, and region. Additionally, the study includes a thorough competitive analysis of key players, their company profiles, notable observations regarding their products and business offerings, recent developments they have undertaken, and key growth strategies they have adopted to enhance their position in the metalized flexible packaging market.

Key Benefits of Buying the Report

The report is expected to assist market leaders and new entrants in this sector by providing the closest approximations of the revenue figures for the overall metalized flexible packaging market, as well as its segments and sub-segments. This report aims to help stakeholders comprehend the competitive landscape of the market, acquire insights to enhance their business positions, and plan effective go-to-market strategies. Additionally, the report seeks to help stakeholders gauge the market's pulse and provide information on the key drivers, challenges, and opportunities within the market.

The report provides insights on the following pointers:

- Analysis of key drivers (rapid growth of e-commerce), restraints (poor recyclability and environmental impact), opportunities (expansion of pet food packaging), and challenges (intensifying competition from emerging high-barrier alternatives) influencing the growth of the metalized flexible packaging market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the metalized flexible packaging market

- Market Development: Comprehensive information about profitable markets - the report analyses the metalized flexible packaging market across varied regions

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the metalized flexible packaging market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like as Amcor plc (Switzerland), Mondi Plc (UK), Sealed Air Corporation (US), Huhtamaki Oyj (Finland), and Transcontinental Inc. (Canada) in the metalized flexible packaging market. The report also helps stakeholders understand the pulse of the metalized flexible packaging market and provides them with information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 METALIZED FLEXIBLE PACKAGING MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 LIMITATIONS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Critical secondary inputs

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Critical primary inputs

- 2.1.2.2 Key primary participants

- 2.1.2.3 Key data from primary sources

- 2.1.2.4 Key industry insights

- 2.1.2.5 Breakdown of interviews with experts

- 2.1.1 SECONDARY DATA

- 2.2 BASE NUMBER CALCULATION

- 2.2.1 ESTIMATION OF METALIZED FLEXIBLE PACKAGING MARKET SIZE BASED ON MARKET SHARE ANALYSIS

- 2.2.2 SUPPLY-SIDE APPROACH-1

- 2.2.3 SUPPLY-SIDE APPROACH-2

- 2.2.4 SUPPLY-SIDE APPROACH-3

- 2.3 FACTOR ANALYSIS

- 2.3.1 INTRODUCTION

- 2.3.2 DEMAND-SIDE ANALYSIS

- 2.3.3 SUPPLY-SIDE ANALYSIS

- 2.4 MARKET SIZE ESTIMATION

- 2.4.1 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

- 2.4.2 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

- 2.5 DATA TRIANGULATION

- 2.6 RESEARCH ASSUMPTIONS

- 2.7 RESEARCH LIMITATIONS

- 2.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN METALIZED FLEXIBLE PACKAGING MARKET

- 4.2 METALIZED FLEXIBLE PACKAGING MARKET, BY MATERIAL TYPE

- 4.3 METALIZED FLEXIBLE PACKAGING MARKET, BY STRUCTURE

- 4.4 METALIZED FLEXIBLE PACKAGING MARKET, BY PACKAGING TYPE

- 4.5 METALIZED FLEXIBLE PACKAGING MARKET, BY END-USE INDUSTRY

- 4.6 ASIA PACIFIC: METALIZED FLEXIBLE PACKAGING MARKET, BY END-USE INDUSTRY AND COUNTRY

- 4.7 METALIZED FLEXIBLE PACKAGING MARKET, BY KEY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Rising population and strengthening economies

- 5.2.1.2 Increasing demand for pharmaceutical packaging

- 5.2.1.3 Rapid growth of e-commerce

- 5.2.1.4 Rising demand for easy-to-use food packaging solutions

- 5.2.2 RESTRAINTS

- 5.2.2.1 Fluctuating costs of raw materials

- 5.2.2.2 Stringent government policies and regulatory frameworks

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Increasing demand for packaging personal care and cosmetics products

- 5.2.3.2 Growing demand for pet food packaging

- 5.2.3.3 Sustainable and new metalized flexible packaging solutions

- 5.2.4 CHALLENGES

- 5.2.4.1 Poor recyclability and environmental impact

- 5.2.4.2 Supply chain disruptions

- 5.2.1 DRIVERS

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 VALUE CHAIN ANALYSIS

- 5.6 REGULATORY LANDSCAPE

- 5.6.1 REGULATORY LANDSCAPE

- 5.6.1.1 Regulatory bodies, government agencies, and other organizations

- 5.6.2 KEY REGULATIONS

- 5.6.2.1 NSF/ANSI standards

- 5.6.1 REGULATORY LANDSCAPE

- 5.7 PRICING ANALYSIS

- 5.7.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY END-USE INDUSTRY,2024

- 5.7.2 AVERAGE SELLING PRICE TREND, BY REGION, 2021-2030

- 5.8 TRADE ANALYSIS

- 5.8.1 EXPORT SCENARIO (HS CODE 7607)

- 5.8.2 IMPORT SCENARIO (HS CODE 7607)

- 5.9 TECHNOLOGY ANALYSIS

- 5.9.1 KEY TECHNOLOGIES

- 5.9.1.1 Lamination

- 5.9.1.2 Mono-extrusion

- 5.9.1.3 Co-extrusion

- 5.9.2 COMPLEMENTARY TECHNOLOGIES

- 5.9.2.1 High-barrier coatings

- 5.9.2.2 Laser scoring and micro-perforation

- 5.9.3 ADJACENT TECHNOLOGIES

- 5.9.3.1 Smart packaging

- 5.9.1 KEY TECHNOLOGIES

- 5.10 PATENT ANALYSIS

- 5.10.1 INTRODUCTION

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 NEW BLISTER PACKAGING TECHNOLOGY DEVELOPED FOR GSK

- 5.11.2 CELPLAST DEVELOPED LIGHTER, RECYCLABLE, HIGH-BARRIER PACKAGING SOLUTIONS TO MEET INDUSTRY DEMAND

- 5.12 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.12.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.12.2 BUYING CRITERIA

- 5.13 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.14 INVESTMENT AND FUNDING SCENARIO

- 5.15 IMPACT OF GEN AI/AI ON METALIZED FLEXIBLE PACKAGING MARKET

- 5.15.1 INTRODUCTION

- 5.16 PORTER'S FIVE FORCES ANALYSIS

- 5.16.1 THREAT OF NEW ENTRANTS

- 5.16.2 THREAT OF SUBSTITUTES

- 5.16.3 BARGAINING POWER OF SUPPLIERS

- 5.16.4 BARGAINING POWER OF BUYERS

- 5.16.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.17 MACROECONOMIC ANALYSIS

- 5.17.1 INTRODUCTION

- 5.17.2 GDP TRENDS AND FORECASTS, 2021-2028

- 5.18 IMPACT OF 2025 US TARIFF ON METALIZED FLEXIBLE PACKAGING MARKET

- 5.18.1 INTRODUCTION

- 5.18.2 KEY TARIFF RATES

- 5.18.3 PRICE IMPACT ANALYSIS

- 5.18.4 IMPACT ON COUNTRY/REGION

- 5.18.4.1 US

- 5.18.4.2 China

- 5.18.4.3 Europe

- 5.18.5 IMPACT ON END-USE INDUSTRIES

6 METALIZED FLEXIBLE PACKAGING MARKET, BY END-USE INDUSTRY

- 6.1 INTRODUCTION

- 6.2 FOOD

- 6.2.1 GROWTH OF E-COMMERCE SECTOR TO DRIVE MARKET

- 6.3 BEVERAGE

- 6.3.1 INCREASING NEED FOR LONGER SHELF LIFE PACKAGING TO FUEL GROWTH

- 6.4 PERSONAL CARE

- 6.4.1 VERSATILITY AND PRODUCT PROTECTION FROM DAMAGE DUE TO MOISTURE OR GAS TO BOOST MARKET

- 6.5 PHARMACEUTICALS

- 6.5.1 INCREASING AWARENESS ABOUT HEALTH AND HEALTHCARE SPENDING TO FUEL MARKET

- 6.6 PET FOOD

- 6.6.1 DEMAND FOR RELIABLE, EFFECTIVE PACKAGING SOLUTIONS THAT PRESERVE QUALITY AND SAFETY TO PROPEL MARKET

- 6.7 OTHER END-USE INDUSTRIES

7 METALIZED FLEXIBLE PACKAGING MARKET, BY MATERIAL TYPE

- 7.1 INTRODUCTION

- 7.2 ALUMINUM-FOIL-BASED FLEXIBLE PACKAGING

- 7.2.1 GOOD THERMAL AND MECHANICAL PROPERTIES TO DRIVE MARKET

- 7.2.2 ALUMINUM PAPER

- 7.2.3 ALUMINUM PAPER POLYMER

- 7.2.4 ALUMINUM POLYMER

- 7.3 METALIZED FILM FLEXIBLE PACKAGING

- 7.3.1 GROWING DEMAND FOR READY-TO-EAT FOOD AND LONGER SHELF LIFE OF PACKAGED PRODUCTS TO BOOST MARKET

- 7.3.2 MET PP/PE

- 7.3.3 MET PET/PE

- 7.3.4 OTHER METALIZED FILM PACKAGING

- 7.4 ALOX/SIOX PP

- 7.4.1 INCREASING DEMAND FOR SUSTAINABLE AND RECYCLABLE PACKAGING MATERIALS TO PROPEL MARKET

- 7.5 ALOX/SIOX PET

- 7.5.1 BARRIER PERFORMANCE AND SUSTAINABILITY TO DRIVE GROWTH

- 7.6 OTHER ALOX/SIOX METALIZED FLEXIBLE PACKAGING

8 METALIZED FLEXIBLE PACKAGING MARKET, BY PACKAGING TYPE

- 8.1 INTRODUCTION

- 8.2 POUCHES

- 8.2.1 RISING POPULARITY OF READY-TO-EAT FOODS TO DRIVE MARKET

- 8.3 BAGS

- 8.3.1 INCREASING DEMAND FROM HEALTHCARE AND FOOD SECTORS TO PROPEL MARKET

- 8.4 WRAPS

- 8.4.1 HIGH DEMAND FOR FLEXIBLE PLASTIC PACKAGING TO BOOST MARKET

- 8.5 ROLLSTOCK

- 8.5.1 LEAK-PROOF AND HIGH OXYGEN BARRIER PROPERTIES TO FUEL MARKET

- 8.6 OTHER PACKAGING TYPES

9 METALIZED FLEXIBLE PACKAGING MARKET, BY STRUCTURE

- 9.1 INTRODUCTION

- 9.2 LAMINATED STRUCTURES

- 9.2.1 HIGH BARRIER PROPERTIES TO DRIVE MARKET

- 9.3 MONO-EXTRUDED STRUCTURES

- 9.3.1 SUSTAINABILITY AND RECYCLABILITY TO BOOST MARKET

- 9.4 OTHER STRUCTURES

10 METALIZED FLEXIBLE PACKAGING MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 ASIA PACIFIC

- 10.2.1 CHINA

- 10.2.1.1 Strong pharmaceutical production base to drive market

- 10.2.2 INDIA

- 10.2.2.1 Rising e-commerce industry to fuel market

- 10.2.3 JAPAN

- 10.2.3.1 Growing demand for generic drugs to drive market

- 10.2.4 SOUTH KOREA

- 10.2.4.1 Implementation of rigorous standards and rules to boost market

- 10.2.5 REST OF ASIA PACIFIC

- 10.2.1 CHINA

- 10.3 EUROPE

- 10.3.1 GERMANY

- 10.3.1.1 Increasing manufacturing activities and government initiatives toward circular economy to boost market

- 10.3.2 UK

- 10.3.2.1 Growth of healthcare industry to propel market

- 10.3.3 FRANCE

- 10.3.3.1 Surge in retail sales of packaged foods and growing health concerns to fuel market

- 10.3.4 ITALY

- 10.3.4.1 Rising demand from retail and healthcare industries to drive growth

- 10.3.5 SPAIN

- 10.3.5.1 Growing demand from food & beverage industry to fuel market

- 10.3.6 RUSSIA

- 10.3.6.1 Increasing awareness and need for eco-friendly solutions to boost market

- 10.3.7 REST OF EUROPE

- 10.3.1 GERMANY

- 10.4 NORTH AMERICA

- 10.4.1 US

- 10.4.1.1 Rising e-commerce sector to drive market

- 10.4.2 CANADA

- 10.4.2.1 Increasing demand for convenient, lightweight, and sustainable packaging solutions to propel growth

- 10.4.3 MEXICO

- 10.4.3.1 Increasing demand for convenience food and changing lifestyles to fuel growth

- 10.4.1 US

- 10.5 SOUTH AMERICA

- 10.5.1 BRAZIL

- 10.5.1.1 Rising demand from food processing industry to drive market

- 10.5.2 ARGENTINA

- 10.5.2.1 Rising consumption of packaged meat products to propel market

- 10.5.3 REST OF SOUTH AMERICA

- 10.5.1 BRAZIL

- 10.6 MIDDLE EAST & AFRICA

- 10.6.1 GCC COUNTRIES

- 10.6.1.1 UAE

- 10.6.1.1.1 Rapidly expanding food and beverage industry to drive market

- 10.6.1.2 Saudi Arabia

- 10.6.1.2.1 Rising urban population and changing consumer preferences to fuel demand

- 10.6.1.3 Rest of GCC countries

- 10.6.1.1 UAE

- 10.6.2 SOUTH AFRICA

- 10.6.2.1 Growth of pharmaceutical industry to boost market

- 10.6.3 REST OF MIDDLE EAST & AFRICA

- 10.6.1 GCC COUNTRIES

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 11.3 REVENUE ANALYSIS, 2020-2024

- 11.4 MARKET SHARE ANALYSIS, 2024

- 11.5 COMPANY VALUATION AND FINANCIAL METRICS

- 11.5.1 COMPANY VALUATION

- 11.5.2 FINANCIAL METRICS

- 11.6 BRAND/PRODUCT COMPARISON

- 11.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 11.7.1 STARS

- 11.7.2 EMERGING LEADERS

- 11.7.3 PERVASIVE PLAYERS

- 11.7.4 PARTICIPANTS

- 11.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 11.7.5.1 Company footprint

- 11.7.5.2 Region footprint

- 11.7.5.3 Structure footprint

- 11.7.5.4 Packaging type footprint

- 11.7.5.5 End-use industry footprint

- 11.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 11.8.1 PROGRESSIVE COMPANIES

- 11.8.2 RESPONSIVE COMPANIES

- 11.8.3 DYNAMIC COMPANIES

- 11.8.4 STARTING BLOCKS

- 11.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 11.8.5.1 Detailed list of key startups/SMEs

- 11.8.5.2 Competitive benchmarking of key startups/SMEs

- 11.9 COMPETITIVE SCENARIO

- 11.9.1 PRODUCT LAUNCHES

- 11.9.2 DEALS

- 11.9.3 EXPANSIONS

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 AMCOR PLC

- 12.1.1.1 Business overview

- 12.1.1.2 Products/Solutions/Services offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Product launches

- 12.1.1.3.2 Deals

- 12.1.1.3.3 Expansions

- 12.1.1.4 MnM view

- 12.1.1.4.1 Right to win

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses and competitive threats

- 12.1.2 MONDI

- 12.1.2.1 Business overview

- 12.1.2.2 Products/Solutions/Services offered

- 12.1.2.3 Recent developments

- 12.1.2.3.1 Deals

- 12.1.2.3.2 Expansions

- 12.1.2.4 MnM view

- 12.1.2.4.1 Right to win

- 12.1.2.4.2 Strategic choices

- 12.1.2.4.3 Weaknesses and competitive threats

- 12.1.3 SEALED AIR CORPORATION

- 12.1.3.1 Business overview

- 12.1.3.2 Products/Solutions/Services offered

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Deals

- 12.1.3.4 MnM view

- 12.1.3.4.1 Right to win

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses and competitive threats

- 12.1.4 HUHTAMAKI OYJ

- 12.1.4.1 Business overview

- 12.1.4.2 Products/Solutions/Services offered

- 12.1.4.3 Recent developments

- 12.1.4.3.1 Deals

- 12.1.4.4 MnM view

- 12.1.4.4.1 Right to win

- 12.1.4.4.2 Strategic choices

- 12.1.4.4.3 Weaknesses and competitive threats

- 12.1.5 TOPPAN HOLDINGS INC.

- 12.1.5.1 Business overview

- 12.1.5.2 Products/Solutions/Services offered

- 12.1.5.3 Recent developments

- 12.1.5.3.1 Deals

- 12.1.5.4 MnM view

- 12.1.5.4.1 Right to win

- 12.1.5.4.2 Strategic choices

- 12.1.5.4.3 Weaknesses and competitive threats

- 12.1.6 TRANSCONTINENTAL INC.

- 12.1.6.1 Business overview

- 12.1.6.2 Products/Solutions/Services offered

- 12.1.6.3 Recent developments

- 12.1.6.3.1 Product launches

- 12.1.6.3.2 Deals

- 12.1.6.3.3 Expansions

- 12.1.6.4 MnM view

- 12.1.7 POLYPLEX CORPORATION LIMITED

- 12.1.7.1 Business overview

- 12.1.7.2 Products/Solutions/Services offered

- 12.1.7.3 MnM view

- 12.1.8 COSMO FIRST LIMITED

- 12.1.8.1 Business overview

- 12.1.8.2 Products/Solutions/Services offered

- 12.1.8.3 Recent developments

- 12.1.8.3.1 Deals

- 12.1.8.4 MnM view

- 12.1.9 UFLEX LIMITED

- 12.1.9.1 Business overview

- 12.1.9.2 Products/Solutions/Services offered

- 12.1.9.3 Recent developments

- 12.1.9.3.1 Product launches

- 12.1.9.4 MnM view

- 12.1.10 JPFL FILMS PRIVATE LIMITED

- 12.1.10.1 Business overview

- 12.1.10.2 Products/Solutions/Services offered

- 12.1.10.3 Recent developments

- 12.1.10.3.1 Deals

- 12.1.10.4 MnM view

- 12.1.1 AMCOR PLC

- 12.2 OTHER PLAYERS

- 12.2.1 ESTER INDUSTRIES LIMITED

- 12.2.2 CONSTANTIA FLEXIBLES

- 12.2.3 TAGHLEEF INDUSTRIES

- 12.2.4 POLINAS

- 12.2.5 DUNMORE

- 12.2.6 GR (SHANDONG) NEW MATERIAL CO.,LTD.

- 12.2.7 SHANGHAI RUITU NEW MATERIALS TECHNOLOGY CO., LTD.

- 12.2.8 XIAMEN CHANGSU INDUSTRIAL CO., LTD.

- 12.2.9 CELPLAST METALLIZED PRODUCTS LIMITED

- 12.2.10 ULTIMET FILMS LIMITED

- 12.2.11 ACCRUED PLASTIC LTD.

- 12.2.12 ALL FOILS, INC.

- 12.2.13 MANUCOR SPA

- 12.2.14 SRF LIMITED

- 12.2.15 KAVERI METALLISING & COATING IND. PRIVATE LIMITED

13 ADJACENT AND RELATED MARKET

- 13.1 INTRODUCTION

- 13.2 LIMITATIONS

- 13.2.1 FLEXIBLE PACKAGING MARKET

- 13.2.1.1 Market definition

- 13.2.1.2 Flexible packaging market, by material

- 13.2.1.3 Flexible packaging market, by packaging type

- 13.2.1.4 Flexible packaging market, by printing technology

- 13.2.1.5 Flexible packaging market, by application

- 13.2.1.6 Flexible packaging market, by region

- 13.2.1 FLEXIBLE PACKAGING MARKET

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 CUSTOMIZATION OPTIONS

- 14.3 RELATED REPORTS

- 14.4 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.5 AUTHOR DETAILS