|

시장보고서

상품코드

1783242

전동 건설기계 시장 예측(-2032년) : 유형별, 배터리 용량별, 배터리 화학별, 출력별, 추진력별, 용도별, 지역별Electric Construction Equipment Market by Type (Excavator, Loader, Grader, Dump Truck, LHD, Self-propelled Sprayer, Tractor), Propulsion (Electric, Hybrid, Hydrogen), Battery Capacity & Chemistry, Power Output, and Region - Global Forecast to 2032 |

||||||

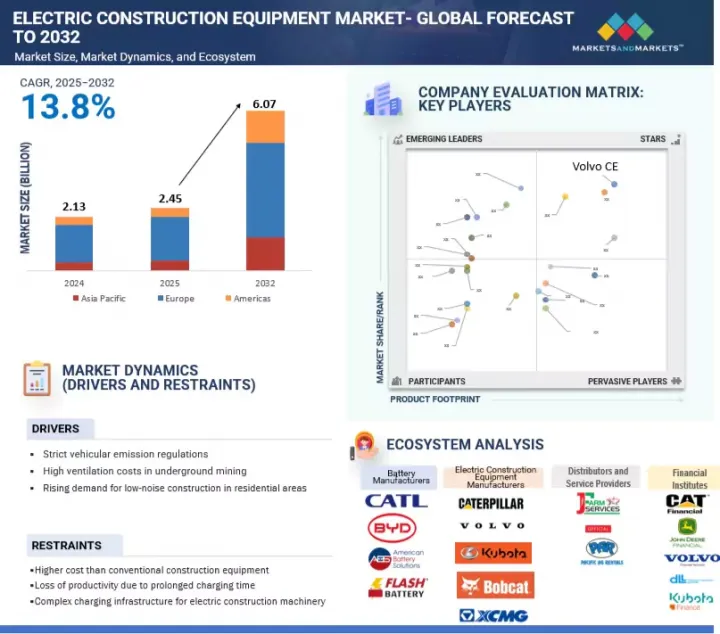

전동 건설기계 시장 규모는 2025년 24억 5,000만 달러에서 2032년에는 60억 7,000만 달러에 달하며, CAGR은 13.8%로 예측됩니다.

건설 및 광업의 전동화 추세는 도시 대기질에 대한 우려와 새로운 소음 저감 의무화에 의해 추진되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상연도 | 2021-2032년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2032년 |

| 대상 유닛 | 수량(단위) 및 금액(1,000달러/100만 달러) |

| 부문 | 유형별, 배터리 용량별, 배터리 화학별, 출력별, 추진력별, 용도별, 지역별 |

| 대상 지역 | 아시아태평양, 아메리카, 유럽 |

최근 시장의 주요 시장 진출기업은 특히 중동과 유럽에서 진행중인 분쟁의 결과로 다양한 국가의 인프라 수요 증가로 인해 전기 굴착기 및 관련 제품을 홍보할 수 있는 새로운 기회를 얻었습니다. 또한 도시 수준의 배기가스 규제로 인해 OEM은 첨단 배터리 전기 모델을 개발해야 하며, 하이브리드 솔루션과 자율주행 기술은 높은 에너지 밀도와 연장된 주행 주기가 필요한 용도에서 인기를 얻고 있습니다.

전기 기계는 도시 환경과 화석 연료가 없는 건설 지역에서 매우 우수한 성능을 발휘하며, 무공해, 소음 감소, 운전 효율 향상 등의 이점을 제공합니다. 또한 디지털 모니터링 시스템 및 스마트 데이터 분석과의 통합이 가능하므로 그 매력은 더욱 커지고 있습니다. 그 결과, 배터리 전기, 하이브리드, 심지어 수소연료전지 파워트레인으로의 전환이 두드러지게 나타나고 있으며, 건설, 광업, 농업 등 다양한 오프로드 차량(OHV) 부문에 큰 영향을 미치고 있습니다.

배터리용량이 100kWh를 초과하는 전기 트랙터는 유럽에서 수요가 급증하고 있으며, 대용량 배터리 팩이 가장 큰 폭으로 성장하고 있습니다. 이러한 빠른 성장의 배경에는 더 긴 주행 자율성, 더 높은 토크 출력, 그리고 열악한 농업 환경에서 첨단 장비에 전력을 공급할 수 있는 능력에 대한 요구가 있습니다. 예를 들어 2024년에 출시된 Fendt e100 Barrio는 100kWh의 배터리를 탑재하여 농가에 장시간의 밭 작업과 견고한 성능을 제공하며, 대규모 농장이나 특수 작업에서 특히 유용하게 사용되고 있습니다. AGCO와 Deere &Company를 포함한 유럽의 주요 기업은 고급 배터리 관리 시스템을 탑재하고 100kWh 이상의 용량을 가진 하이최종 용도의 전기 트랙터를 개발 및 상용화함으로써 주도권을 쥐고 있습니다. 이러한 추세는 2025년 3월부터 전기 농기계를 도입할 경우 최대 4만5000달러의 보조금을 지급하는 유럽연합(EU)과 각국의 엄격한 규제에 의해 강력하게 지원되고 있습니다.

또한 유럽의 그린딜에 따라 지속가능한 농법에 대한 광범위한 지원이 이러한 움직임을 촉진하고 있습니다. 유럽이 대용량 전기 트랙터 시장의 선두를 달리고 있는 것은 정부의 지원 정책, 첨단 농가의 강력한 수요, 혁신과 지속가능성 추진에 대한 주요 제조업체의 노력에 기인합니다. 그러나 이러한 장점에도 불구하고 보급에 있어서는 여전히 큰 과제가 남아있습니다. 여기에는 높은 초기 비용, 긴 충전 시간, 농촌 지역의 충전 인프라 제한, 고부하 연속 사용으로 인한 배터리 성능 저하 우려 등이 있습니다.

배터리 전기 부문은 하이브리드 및 연료전지 대체품에 비해 작동이 간편하고 유지보수 요구사항이 낮으며 배출가스가 즉각적으로 감소하므로 전기 건설기계에서 가장 큰 시장 점유율을 차지하고 있습니다. 이 때문에 제조업체와 최종사용자 모두에게 선호되는 선택이 되고 있습니다. 북미와 남미에서는 엄격한 환경 규제, 정부 혜택, 케이스 컨스트럭션의 12EV 휠 로더와 580EV 백호, 볼보 CE의 전기 로더, 밥캣의 전기 소형 트럭 로더와 같은 새로운 모델의 도입이 전동화로의 전환을 촉진하고 있습니다. 이러한 발전은 지속가능한 기계로 시장이 크게 이동하고 있음을 반영합니다. 유럽은 야심찬 탈탄소화 목표, 강력한 규제 프레임워크, 저소음 및 무공해 장비에 대한 높은 수요에 힘입어 시장 점유율을 주도하고 있습니다.

한편, 아시아태평양은 급속한 도시화, 인프라 개발, 중국, 인도, 일본 등 각국의 정부 정책에 힘입어 급성장하고 있습니다. 이러한 정책은 오염 방지를 의무화하고, 전기 장비의 현지 생산을 지원하고 있습니다. 이들 지역의 행정기관은 재정적 인센티브, 세금 감면, 직접 보조금을 통해 건설 및 채굴용 배터리 전기자동차(BEV)를 적극 장려하고 있습니다. 이러한 조치는 전기 기계를 보다 경제적으로 매력적으로 만들고 높은 초기 비용을 상쇄하는 데 도움이 됩니다. Caterpillar, Volvo Construction Equipment, Komatsu, Hitachi, JCB, Bobcat 등 이 시장의 주요 기업은 전기 굴착기, 로더, 트럭 등 신제품을 출시하며 전기 건설기계 수요 증가에 대응하기 위해 제품 포트폴리오를 확장하고 있습니다. 을 확대하고 있습니다.

환경 규제, 정부 혜택, 지속가능한 건축 관행에 대한 수요 증가 등으로 인해 북미 및 남미 지역의 전기 건설기계 시장은 빠르게 성장하고 있습니다. 미국에서는 전기 건설기계 시장이 확대되고 있으며, 굴착기가 판매를 주도하여 2025년까지 시장 점유율의 약 60%를 차지할 것으로 예측됩니다. 이러한 성장의 배경에는 굴착기의 다용도성, 높은 현장 가동률, 소음과 배출가스 최소화가 필수적인 도시 및 실내 환경에 대한 적합성 등이 있습니다. 이러한 추세에 기여하는 중요한 요인은 Li-NMC(리튬-니켈-망간-코발트(Li-NMC) 배터리의 보급으로, 2025년에는 시장 점유율의 45% 이상을 차지할 것으로 예측됩니다. 이 배터리는 우수한 에너지 밀도, 더 긴 사이클 수명, 더 빠른 충전 기능을 제공하여 가동 시간과 성능이 중요한 까다로운 건설 및 광산 환경에 이상적입니다.

미주 주요 기업으로는 Bobcat, Caterpillar, Volvo Construction Equipment, Komatsu, John Deere, CASE Construction Equipment 등이 있습니다. 이들 기업은 최근 수년간 새로운 전동화 모델을 도입하고 전동화 전략을 확대하고 있습니다. 캘리포니아주의 엄격한 배기가스 배출 기준과 주요 도시의 새로운 소음 규제 등 최근 규제 변경으로 인해 전기로의 전환이 가속화되고 있습니다. 예를 들어 로스엔젤레스와 뉴욕시에서는 무공해 건설 현장을 추진하고 있으며, 친환경 장비 구매에 대한 연방 및 주정부의 인센티브도 제조업체들이 전기 기술에 투자하도록 장려하고 있습니다.

또한 주정부나 지자체는 학교, 병원, 법원 등 영향을 받기 쉬운 장소 근처에서 소음 수준을 제한하는 등 추가적인 조례를 시행하는 경우가 많습니다. 온타리오 주 토론토에서는 오후 7시부터 오전 7시까지 공사 소음을 제한하고 있으며, 뉴욕시에서는 시간 외 공사는 특별 허가를 받아야 합니다. 전기화를 지원하기 위해 정부 및 기관은 저소음 전기 기기 구매에 대한 세액 공제, 보조금 등의 인센티브를 제공합니다. 그러나 이러한 정책은 주와 지역마다 다르며, 일부 지역에서는 더 강력한 지원을 제공하는 곳도 있습니다.

세계의 전동 건설기계 시장에 대해 조사했으며, 유형별, 배터리 용량별, 배터리 화학별, 출력별, 추진력별, 용도별, 지역별 동향 및 시장에 참여하는 기업의 개요 등을 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 주요 인사이트

제5장 시장 개요

- 서론

- 시장 역학

- 무역 분석

- 고객 비즈니스에 영향을 미치는 동향과 혼란

- 특허 분석

- 공급망 분석

- 에코시스템 분석

- 가격 분석

- 기술 분석

- 규제 상황

- 2025-2026년의 주요 컨퍼런스와 이벤트

- 사례 연구 분석

- 주요 이해관계자와 구입 기준

- 전기 건설기계의 총소유 비용

- 전동 트랙터의 총소유 비용

- 로더의 총소유 비용

- 배터리 기술의 향후 발전

- OEM 분석

제6장 전기 건설기계 시장(유형별)

- 서론

- 전동 굴착기

- 전동 로더

- 전동 모터 그레이더

- 전동 도저

- 전동 덤프트럭/와이드보디 트럭

- 전동 하역 덤프 로더

- 주요 인사이트

제7장 전동 건설기계 시장(배터리 용량별)

- 서론

- 50KWH 미만

- 50-200KWH

- 200-500KWH

- 500KWH 이상

- OEM 레벨 기기의 배터리 용량

- 주요 인사이트

제8장 전기 건설기계 시장(배터리 화학별)

- 서론

- 인산철리튬

- 리튬 니켈 망간 코발트 산화물

- 기타

- 비용 분석

- 배터리 화학의 발전

- 주요 인사이트

제9장 전기 건설기계 시장(출력별)

- 서론

- 50HP 미만

- 50-150HP

- 150-300HP

- 300HP 이상

- 주요 인사이트

제10장 전동 건설기계 시장(추진력별)

- 서론

- 배터리 전기

- 하이브리드 전기자동차

- 수소

- 주요 인사이트

제11장 전기 건설기계 시장(용도별)

- 서론

- 건설

- 광업

- 원예

- 농업

- 주요 인사이트

제12장 전기 농업 기기 시장(유형별)

- 서론

- 운영 데이터

- 전동 잔디깎기기계

- 전동 자주식 분무기

- 전기 트랙터

- 주요 인사이트

제13장 전동 트랙터 시장(배터리 용량별)

- 서론

- 50KWH 미만

- 50-100KWH

- 100KWH 이상

- 전동 트랙터 모델과 배터리 용량

- 주요 인사이트

제14장 전동 트랙터 시장(배터리 화학별)

- 서론

- 인산철리튬

- 리튬 니켈 망간 코발트 산화물

- 기타

- 주요 인사이트

제15장 전동 트랙터 시장(추진력별)

- 서론

- 배터리 전기

- 하이브리드 전기자동차

- 수소

- 주요 인사이트

제16장 전기 건설기계 시장(지역별)

- 서론

- 아시아태평양

- 거시경제 전망

- 중국

- 인도

- 일본

- 한국

- 기타

- 유럽

- 거시경제 전망

- 독일

- 영국

- 프랑스

- 스페인

- 러시아

- 이탈리아

- 기타

- 아메리카

- 거시경제 전망

- 미국

- 캐나다

- 멕시코

- 브라질

- 아르헨티나

- 주요 인사이트

제17장 경쟁 구도

- 개요

- 주요 참여 기업의 전략/강점, 2021-2025년

- 매출 분석, 2020-2024년

- 시장 점유율 분석, 2024년

- 기업 평가

- 재무 지표

- 브랜드/제품 비교

- 기업 평가 매트릭스 : 전기 건설기계 제조업체, 2024년

- 기업 평가 매트릭스 : 전동 삽 제조업체, 2025년

- 경쟁 시나리오

제18장 기업 개요

- 주요 참여 기업

- HITACHI CONSTRUCTION MACHINERY CO., LTD.

- CATERPILLAR INC.

- KOMATSU LTD.

- VOLVO CONSTRUCTION EQUIPMENT

- SANY HEAVY INDUSTRIES CO., LTD.

- JCB

- DEERE & COMPANY

- SANDVIK AB

- EPIROC AB

- LIEBHERR

- BOBCAT COMPANY

- 기타 기업

- SOLETRAC INC.

- FENDT

- HUSQVARNA AB

- XUZHOU CONSTRUCTION MACHINERY GROUP CO., LTD.

- KUBOTA CORPORATION

- KOBELCO CONSTRUCTION MACHINERY EUROPE BV

- BHARAT EARTH MOVERS LIMITED

- CNH INDUSTRIAL NV

- WACKER NEUSON SE

- TAKEUCHI GLOBAL

- HD HYUNDAI HEAVY INDUSTRIES CO., LTD.

- LUIGONG MACHINERY CO., LTD.

제19장 시장으로부터의 제안

제20장 부록

KSA 25.08.11The electric construction equipment market is projected to reach USD 6.07 billion by 2032, from USD 2.45 billion in 2025, with a CAGR of 13.8%. The electrification trend in the construction and mining industries is driven by concerns over urban air quality and new noise reduction mandates.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Units Considered | Volume (Unit) and Value (USD Thousand/Million) |

| Segments | Type, Battery Capacity, Battery Chemistry, Power Output, Application, and Region |

| Regions covered | Asia Pacific, Americas, and Europe |

Recently, key players in the market have new opportunities to promote their electric excavators and related products due to increased infrastructure demand in various countries, particularly as a result of the ongoing conflicts in the Middle East and Europe. Additionally, city-level emissions regulations are compelling OEMs to develop advanced battery-electric models, while hybrid solutions and autonomous technologies are gaining popularity for applications that require high energy density or extended operating cycles.

Electric machinery performs exceptionally well in urban environments and fossil-free construction zones, offering benefits such as zero emissions, reduced noise levels, and improved operational efficiency. Furthermore, their capability to integrate with digital monitoring systems and smart data analytics enhances their attractiveness. As a result, there is a noticeable shift toward battery-electric, hybrid, and even hydrogen fuel cell powertrains, which significantly impact various off-highway vehicle (OHV) sectors, including construction, mining, and agriculture.

Tractors with >100 kWh battery capacity exhibit the fastest growth in Europe.

Electric tractors with battery capacities exceeding 100 kWh are experiencing rapidly increasing demand in Europe, which is seeing the strongest growth for large-capacity battery packs. This surge is driven by the need for longer operational autonomy, higher torque output, and the ability to power advanced implements in demanding agricultural environments. For instance, the Fendt e100 Vario, launched in 2024, features a 100-kWh battery that provides farmers with extended field hours and robust performance, making it especially valuable for large-scale farms and specialized operations. Major European manufacturers, including AGCO Corporation and Deere & Company, are leading the charge by developing and commercializing electric tractors equipped with advanced battery management systems and capacities that meet or exceed 100 kWh for high-end applications. This trend is strongly supported by stringent EU and national regulations, such as the Common Agricultural Policy (CAP), which offers grants of up to USD 45,000 for adopting electric farm equipment starting in March 2025.

Additionally, the broader push toward sustainable farming practices under Europe's Green Deal bolsters this movement. Europe is at the forefront of the market for large-capacity electric tractors due to supportive government policies, strong demand from progressive farmers, and a commitment from major manufacturers to innovate and promote sustainability. However, despite these advantages, significant challenges remain for widespread adoption. These include high upfront costs, longer charging times, limited charging infrastructure in rural areas, and concerns about battery degradation under continuous high-load use.

The battery electric segment secures the leading market position.

The battery electric segment holds the largest market share in electric construction equipment due to its operational simplicity, lower maintenance requirements, and immediate emissions reduction when compared to hybrid or fuel cell alternatives. This makes it the preferred choice for both manufacturers and end users. In the Americas, the shift toward electrification is driven by strict environmental regulations, government incentives, and the introduction of new models such as Case Construction's 12EV wheel loader and 580EV backhoe, Volvo CE's electric loader, and Bobcat's electric compact track loader. These developments reflect a significant market shift toward sustainable machinery. Europe leads in market share, fueled by ambitious decarbonization targets, strong regulatory frameworks, and a high demand for low-noise, zero-emission equipment.

Meanwhile, the Asia Pacific region is experiencing the fastest growth, driven by rapid urbanization, infrastructure development, and government policies in countries like China, India, and Japan. These policies mandate pollution control and support the local manufacturing of electric equipment. Governing bodies across these regions actively promote battery electric vehicles (BEVs) for construction and mining through financial incentives, tax breaks, and direct subsidies. These measures make electric machinery more economically attractive and help offset higher upfront costs. Key players in the market, including Caterpillar, Volvo Construction Equipment, Komatsu, Hitachi, JCB, and Bobcat, have launched new electric excavators, loaders, and trucks, expanding their product portfolios to meet the rising demand for electric construction equipment.

The Americas is the second fastest-growing market for electric construction equipment.

The trend of electric construction equipment in the Americas is rapidly growing, driven by a mix of environmental regulations, government incentives, and increasing demand for sustainable building practices. In the United States, the electric construction equipment market is expanding, with excavators leading sales and accounting for around 60% of the market share by 2025. This growth is attributed to excavators' versatility, high utilization rates on job sites, and their suitability for urban and indoor environments where minimizing noise and emissions is essential. A significant factor contributing to this trend is the prevalence of Li-NMC (Lithium Nickel Manganese Cobalt) batteries, which will make up more than 45% of the market share in 2025. These batteries offer superior energy density, longer cycle life, and faster charging capabilities, making them ideal for demanding construction and mining environments where uptime and performance are critical.

Key players in the Americas include Bobcat, Caterpillar, Volvo Construction Equipment, Komatsu, John Deere, and CASE Construction Equipment. These companies have introduced new electric models and expanded their electrification strategies in recent years. Recent regulatory changes, such as stricter emissions standards in California and new noise level ordinances in major cities, have accelerated the shift toward electrification. For example, the push for zero-emission construction sites in Los Angeles and New York City, along with federal and state incentives for purchasing green equipment, has encouraged manufacturers to invest in electric technology.

Additionally, states and municipalities often implement further ordinances, such as restrictions on noise levels near sensitive areas like schools, hospitals, and courts. In Toronto, Ontario, construction noise is restricted from 7 PM to 7 AM, while in New York City, after-hours construction requires special authorization. To support the move toward electrification, governments and agencies offer incentives such as tax credits or grants for purchasing quieter electric equipment. However, these policies vary by state and locality, with some regions providing more robust support than others.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and strategy directors, and executives from various key organizations operating in this market.

- By Company Type: Electric Construction Equipment OEM - 100%

- By Designation: C Level - 30%, Directors- 20%, and Others - 50%

- By Region: Asia Pacific - 50%, Americas - 30%, and Europe -20%

The key players in the electric construction equipment market are Hitachi Construction Machinery (Japan), Caterpillar Inc. (US), Komatsu Ltd. (Japan), Volvo Construction Equipment (Sweden), Hitachi Construction Machinery Co., Ltd. (Japan), and JCB (UK). Major companies' key strategies to maintain their position in the global electric construction equipment market are strong global networking, mergers and acquisitions, partnerships, and technological advancement.

Research Coverage

The study segments and forecasts the size of the electric construction equipment market based on type (electric excavators, electric motor graders, electric dozers, electric loaders, electric dump trucks, and electric load-haul-dump loaders), battery capacity (<50 kWh, 50-200 kWh, 200-500 kWh, and >500 kWh), battery chemistry (lithium iron phosphate, lithium nickel manganese cobalt oxide, and others), power output (<50 hp, 50-150 hp, 150-300 hp, and >300 hp), application (construction, mining, agriculture, and gardening), propulsion (battery electric, hybrid electric, and hydrogen), electric agriculture equipment market by type (electric lawnmowers, electric self-propelled sprayers, and electric tractors), electric tractor market by propulsion (battery electric, hybrid electric, and hydrogen), electric tractor market by battery capacity (<50 KWh, 50-100 KWh, and >100 KWh), electric tractor market by battery chemistry (lithium iron phosphate, lithium nickel manganese cobalt oxide, and others), and region (Asia Pacific, Europe, and Americas). It also includes an in-depth competitive analysis of the major electric construction equipment manufacturers, their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying this Report:

The report will assist market leaders and new entrants by providing estimates of revenue for the overall electric construction equipment market and its sub-segments. This report will help stakeholders understand the competitive landscape and gain valuable insights to better position their businesses and develop effective go-to-market strategies. Additionally, it helps stakeholders stay informed about the market's current trends and offers information on key market drivers, restraints, challenges, and opportunities.

This report provides insights into the following pointers:

- Analysis of key drivers (strict vehicular emission regulations, high ventilation costs in underground mining, rising demand for low-noise construction in residential areas), restraints (higher initial costs than conventional ICE equipment, loss of productivity due to prolonged charging times, complex charging infrastructure for electric construction machinery), opportunities (development of long-range and fast-charging battery technology, increased manufacturing and testing of hybrid electric vehicles, emergence of hydrogen-powered construction equipment), and challenges (limited compatibility, interchangeability, and standardization of electric construction equipment for long-haul applications, complex thermal management of batteries, rapid transition of construction equipment toward alternative power sources) influencing the growth of the electric construction equipment market

- Product Development/Innovation: In-depth insights on upcoming technologies and new product and service launches in the electric construction equipment market

- Market Development: Comprehensive market information - the report analyses the authentication and brand protection market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the electric construction equipment market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players in the electric construction equipment market, such as Caterpillar Inc. (US), Komatsu Ltd. (Japan), Volvo Construction Equipment (Sweden), Hitachi Construction Machinery Co., Ltd. (Japan), and JCB (UK)

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Sampling techniques and data collection methods

- 2.1.2.2 Primary interview participants

- 2.1.2.3 Breakdown of primary interviews

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.3 DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.5 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN THE ELECTRIC CONSTRUCTION EQUIPMENT MARKET

- 4.2 ELECTRIC CONSTRUCTION EQUIPMENT MARKET, BY TYPE

- 4.3 ELECTRIC CONSTRUCTION EQUIPMENT MARKET, BY APPLICATION

- 4.4 ELECTRIC CONSTRUCTION EQUIPMENT MARKET, BY BATTERY CHEMISTRY

- 4.5 ELECTRIC CONSTRUCTION EQUIPMENT MARKET, BY BATTERY CAPACITY

- 4.6 ELECTRIC CONSTRUCTION EQUIPMENT MARKET, BY PROPULSION

- 4.7 ELECTRIC CONSTRUCTION EQUIPMENT MARKET, BY POWER OUTPUT

- 4.8 ELECTRIC CONSTRUCTION EQUIPMENT MARKET, BY REGION

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Strict vehicular emission regulations

- 5.2.1.2 High ventilation costs in underground mining

- 5.2.1.3 Surge in demand for low-noise construction in residential areas

- 5.2.1.4 Incentives on electric tractors and finance credits

- 5.2.2 RESTRAINTS

- 5.2.2.1 Higher initial cost than conventional ICE equipment

- 5.2.2.2 Loss of productivity due to prolonged charging time

- 5.2.2.3 Complex charging infrastructure for electric construction machinery

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Development of long-range and fast-charging battery technology

- 5.2.3.2 Increased manufacturing and testing of hybrid electric vehicles

- 5.2.3.3 Emergence of hydrogen-powered construction equipment

- 5.2.4 CHALLENGES

- 5.2.4.1 Limited compatibility, interchangeability, and standardization for long-haul applications

- 5.2.4.2 Complex thermal management of batteries

- 5.2.4.3 Rapid transition of construction equipment toward alternative power sources

- 5.2.1 DRIVERS

- 5.3 TRADE ANALYSIS

- 5.3.1 IMPORT SCENARIO (HS CODE 842710)

- 5.3.2 EXPORT SCENARIO (HS CODE 842710)

- 5.4 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.5 PATENT ANALYSIS

- 5.6 SUPPLY CHAIN ANALYSIS

- 5.7 ECOSYSTEM ANALYSIS

- 5.8 PRICING ANALYSIS

- 5.8.1 BY TYPE

- 5.8.2 BY APPLICATION

- 5.9 TECHNOLOGY ANALYSIS

- 5.9.1 KEY TECHNOLOGIES

- 5.9.1.1 Autonomous construction equipment

- 5.9.1.2 Remote monitoring and predictive maintenance

- 5.9.2 COMPLEMENTARY TECHNOLOGIES

- 5.9.2.1 Grade control systems

- 5.9.2.2 Regenerative braking

- 5.9.2.3 Hydrogen fuel cells

- 5.9.2.4 Augmented reality

- 5.9.3 ADJACENT TECHNOLOGIES

- 5.9.3.1 Agricultural equipment automation

- 5.9.3.2 Advanced telematics

- 5.9.1 KEY TECHNOLOGIES

- 5.10 REGULATORY LANDSCAPE

- 5.10.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.10.2 QUALITY STANDARDS

- 5.11 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.12 CASE STUDY ANALYSIS

- 5.12.1 CATERPILLAR'S ELECTRIC MINI EXCAVATOR

- 5.12.2 HITACHI'S ZE85 ELECTRIC EXCAVATOR

- 5.12.3 KOMATSU'S ELECTRIC MINI EXCAVATORS

- 5.12.4 VOLVO CE'S MID-SIZE ELECTRIC WHEEL LOADERS

- 5.12.5 JCB'S ELECTRIC TELEHANDLERS

- 5.13 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.13.2 BUYING CRITERIA

- 5.14 TOTAL COST OF OWNERSHIP OF ELECTRIC CONSTRUCTION EQUIPMENT

- 5.15 TOTAL COST OF OWNERSHIP OF ELECTRIC TRACTORS

- 5.16 TOTAL COST OF OWNERSHIP OF LOADERS

- 5.17 FUTURE DEVELOPMENTS IN BATTERY TECHNOLOGY

- 5.17.1 SOLID-STATE BATTERIES

- 5.17.2 LITHIUM-ION BATTERIES

- 5.17.3 SODIUM-ION BATTERIES

- 5.17.4 SWAPPABLE BATTERY TECHNOLOGY

- 5.18 OEM ANALYSIS

- 5.18.1 BATTERY CAPACITY OF ELECTRIC COMPACT CONSTRUCTION EQUIPMENT OFFERED BY OEMS

- 5.18.2 BATTERY CAPACITY VS. POWER OUTPUT

6 ELECTRIC CONSTRUCTION EQUIPMENT MARKET, BY TYPE

- 6.1 INTRODUCTION

- 6.2 ELECTRIC EXCAVATORS

- 6.2.1 EXTENSIVE USE IN CONSTRUCTION AND MINING DUE TO NOISELESS OPERATIONS

- 6.3 ELECTRIC LOADERS

- 6.3.1 INCREASED INVESTMENTS BY PROMINENT COMPANIES

- 6.4 ELECTRIC MOTOR GRADERS

- 6.4.1 RISING NEED IN US DUE TO STRINGENT EMISSION NORMS

- 6.5 ELECTRIC DOZERS

- 6.5.1 HIGH DEMAND FROM ASIA PACIFIC DUE TO STRONG PRESENCE OF CONSTRUCTION AND MINING COMPANIES

- 6.6 ELECTRIC DUMP TRUCKS/WIDE-BODIED TRUCKS

- 6.6.1 SURGE IN MINING ACTIVITIES

- 6.7 ELECTRIC LOAD HAUL DUMP LOADERS

- 6.7.1 FOCUS ON MINIMIZING UNDERGROUND VENTILATION COST

- 6.8 PRIMARY INSIGHTS

7 ELECTRIC CONSTRUCTION EQUIPMENT MARKET, BY BATTERY CAPACITY

- 7.1 INTRODUCTION

- 7.2 <50 KWH

- 7.2.1 SUITABLE FOR PACKED CONSTRUCTION SITES AND NARROW MINING APPLICATIONS

- 7.3 50-200 KWH

- 7.3.1 HIGH DEMAND FOR SMALL AND MID-RANGE CONSTRUCTION EQUIPMENT T

- 7.4 200-500 KWH

- 7.4.1 ONGOING DEVELOPMENT OF NEWER MODELS

- 7.5 >500 KWH

- 7.5.1 UNTAPPED GROWTH POTENTIAL WITH ADVANCES IN BATTERY TECHNOLOGY

- 7.6 BATTERY CAPACITY OF OEM-LEVEL EQUIPMENT

- 7.7 PRIMARY INSIGHTS

8 ELECTRIC CONSTRUCTION EQUIPMENT MARKET, BY BATTERY CHEMISTRY

- 8.1 INTRODUCTION

- 8.2 LITHIUM IRON PHOSPHATE

- 8.2.1 NEED FOR EFFICIENT ENERGY STORAGE DUE TO RISE IN RENEWABLE ENERGY SOURCES

- 8.3 LITHIUM NICKEL MANGANESE COBALT OXIDE

- 8.3.1 HIGHER CONSUMER ACCEPTANCE IN EUROPE AND AMERICAS

- 8.4 OTHERS

- 8.4.1 SODIUM-ION BATTERIES

- 8.4.2 SOLID-STATE BATTERIES

- 8.5 COST ANALYSIS

- 8.6 DEVELOPMENTS IN BATTERY CHEMISTRY

- 8.7 PRIMARY INSIGHTS

9 ELECTRIC CONSTRUCTION EQUIPMENT MARKET, BY POWER OUTPUT

- 9.1 INTRODUCTION

- 9.2 <50 HP

- 9.2.1 LARGE-SCALE ADOPTION IN LIGHT CONSTRUCTION APPLICATIONS

- 9.3 50-150 HP

- 9.3.1 INCREASED PRODUCT DEVELOPMENT ACTIVITIES

- 9.4 150-300 HP

- 9.4.1 EXPANDING DEVELOPMENTS IN BATTERIES AND CONSTRUCTION EQUIPMENT PRODUCTS

- 9.5 >300 HP

- 9.5.1 LIMITED COMMERCIALIZATION DUE TO HIGH BATTERY COSTS

- 9.6 PRIMARY INSIGHTS

10 ELECTRIC CONSTRUCTION EQUIPMENT MARKET, BY PROPULSION

- 10.1 INTRODUCTION

- 10.2 BATTERY ELECTRIC

- 10.2.1 EMPHASIS ON ENVIRONMENTAL SUSTAINABILITY

- 10.3 HYBRID ELECTRIC

- 10.3.1 LIMITATIONS ASSOCIATED WITH 100% ELECTRIFICATION

- 10.4 HYDROGEN

- 10.4.1 GROWING ADOPTION OF ENVIRONMENTALLY CONSCIOUS PRACTICES

- 10.5 PRIMARY INSIGHTS

11 ELECTRIC CONSTRUCTION EQUIPMENT MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 CONSTRUCTION

- 11.2.1 COMPLIANCE WITH STRINGENT EMISSION AND NOISE REGULATIONS

- 11.3 MINING

- 11.3.1 EMERGING TREND OF ELECTRIFICATION

- 11.4 GARDENING

- 11.4.1 HIGHER RATE OF ELECTRIFICATION THAN OTHER EQUIPMENT

- 11.5 AGRICULTURE

- 11.5.1 ELEVATED DEMAND FOR FOOD PRODUCTION

- 11.6 PRIMARY INSIGHTS

12 ELECTRIC AGRICULTURE EQUIPMENT MARKET, BY TYPE

- 12.1 INTRODUCTION

- 12.2 OPERATIONAL DATA

- 12.3 ELECTRIC LAWNMOWERS

- 12.3.1 HIGH FUEL COSTS AND WORKFORCE SHORTAGES

- 12.4 ELECTRIC SELF-PROPELLED SPRAYERS

- 12.4.1 PREVENTION OF CROP WITHERING

- 12.5 ELECTRIC TRACTORS

- 12.5.1 GOVERNMENT INITIATIVES FOR BOOSTING FOOD PRODUCTIVITY

- 12.6 PRIMARY INSIGHTS

13 ELECTRIC TRACTOR MARKET, BY BATTERY CAPACITY

- 13.1 INTRODUCTION

- 13.2 <50 KWH

- 13.2.1 INCREASED PREFERENCE DUE TO ACCESSIBILITY AND LOW COST

- 13.3 50-100 KWH

- 13.3.1 LONG-TERM SAVINGS THROUGH REDUCED FUEL AND MAINTENANCE COSTS

- 13.4 >100 KWH

- 13.4.1 RIGOROUS DEVELOPMENT OF HIGH-POWERED ELECTRIC TRACTORS BY OEMS

- 13.5 ELECTRIC TRACTOR MODELS AND BATTERY CAPACITIES

- 13.6 PRIMARY INSIGHTS

14 ELECTRIC TRACTOR MARKET, BY BATTERY CHEMISTRY

- 14.1 INTRODUCTION

- 14.2 LITHIUM IRON PHOSPHATE

- 14.2.1 INCREASED INVESTMENTS BY AGRICULTURAL MACHINERY MANUFACTURERS

- 14.3 LITHIUM NICKEL MANGANESE COBALT OXIDE

- 14.3.1 HIGHER DENSITY AND FASTER CHARGING CAPABILITIES THAN OTHER CHEMISTRIES

- 14.4 OTHERS

- 14.4.1 SODIUM-ION BATTERIES

- 14.4.2 SOLID-STATE BATTERIES

- 14.5 PRIMARY INSIGHTS

15 ELECTRIC TRACTOR MARKET, BY PROPULSION

- 15.1 INTRODUCTION

- 15.2 BATTERY ELECTRIC

- 15.2.1 DECLINING COST OF LITHIUM-ION BATTERIES

- 15.3 HYBRID ELECTRIC

- 15.3.1 HIGHER POWER OUTPUT THAN BATTERY ELECTRIC TRACTORS

- 15.4 HYDROGEN

- 15.4.1 ADVANCEMENTS IN FUEL CELL TECHNOLOGY AND INFRASTRUCTURE

- 15.5 PRIMARY INSIGHTS

16 ELECTRIC CONSTRUCTION EQUIPMENT MARKET, BY REGION

- 16.1 INTRODUCTION

- 16.2 ASIA PACIFIC

- 16.2.1 MACROECONOMIC OUTLOOK

- 16.2.2 CHINA

- 16.2.2.1 National emission standards for mining automation to drive market

- 16.2.3 INDIA

- 16.2.3.1 Growing demand for eco-friendly, cost-effective electric construction equipment to drive market

- 16.2.4 JAPAN

- 16.2.4.1 Increasing investments in electric construction excavators and other equipment to drive market

- 16.2.5 SOUTH KOREA

- 16.2.5.1 Ongoing electrification of loaders for mining to drive market

- 16.2.6 REST OF ASIA PACIFIC

- 16.3 EUROPE

- 16.3.1 MACROECONOMIC OUTLOOK

- 16.3.2 GERMANY

- 16.3.2.1 Stringent government norms to drive market

- 16.3.3 UK

- 16.3.3.1 Rising demand for electric construction excavators to drive market

- 16.3.4 FRANCE

- 16.3.4.1 Implementation of National Low-Carbon Strategy to drive market

- 16.3.5 SPAIN

- 16.3.5.1 Emphasis on reducing carbon emissions from construction machinery to drive market

- 16.3.6 RUSSIA

- 16.3.6.1 Electric construction equipment expected to drive market

- 16.3.7 ITALY

- 16.3.7.1 Electrification of construction and mining sectors to drive market

- 16.3.8 REST OF EUROPE

- 16.4 AMERICAS

- 16.4.1 MACROECONOMIC OUTLOOK

- 16.4.2 US

- 16.4.2.1 Presence of major electric construction equipment providers to drive market

- 16.4.3 CANADA

- 16.4.3.1 Global dominance in electric construction industry to drive market

- 16.4.4 MEXICO

- 16.4.4.1 Ongoing electrification promotion programs to drive market

- 16.4.5 BRAZIL

- 16.4.5.1 Incorporation of electric excavators in construction frameworks to regularize mining to drive market

- 16.4.6 ARGENTINA

- 16.4.6.1 Commitment to sustainability and emission reductions to drive market

- 16.5 PRIMARY INSIGHTS

17 COMPETITIVE LANDSCAPE

- 17.1 OVERVIEW

- 17.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

- 17.3 REVENUE ANALYSIS, 2020-2024

- 17.4 MARKET SHARE ANALYSIS, 2024

- 17.5 COMPANY VALUATION

- 17.6 FINANCIAL METRICS

- 17.7 BRAND/PRODUCT COMPARISON

- 17.8 COMPANY EVALUATION MATRIX: ELECTRIC CONSTRUCTION EQUIPMENT MANUFACTURERS, 2024

- 17.8.1 STARS

- 17.8.2 EMERGING LEADERS

- 17.8.3 PERVASIVE PLAYERS

- 17.8.4 PARTICIPANTS

- 17.8.5 COMPANY FOOTPRINT

- 17.8.5.1 Company footprint

- 17.8.5.2 Region footprint

- 17.8.5.3 Type footprint

- 17.8.5.4 Application footprint

- 17.9 COMPANY EVALUATION MATRIX: ELECTRIC EXCAVATOR MANUFACTURERS, 2025

- 17.9.1 STARS

- 17.9.2 EMERGING LEADERS

- 17.9.3 PERVASIVE PLAYERS

- 17.9.4 PARTICIPANTS

- 17.9.5 COMPANY FOOTPRINT

- 17.9.5.1 Company footprint

- 17.9.5.2 Region footprint

- 17.9.5.3 Propulsion footprint

- 17.9.5.4 Battery chemistry footprint

- 17.10 COMPETITIVE SCENARIO

- 17.10.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 17.10.2 DEALS

- 17.10.3 EXPANSIONS

- 17.10.4 OTHER DEVELOPMENTS

18 COMPANY PROFILES

- 18.1 KEY PLAYERS

- 18.1.1 HITACHI CONSTRUCTION MACHINERY CO., LTD.

- 18.1.1.1 Business overview

- 18.1.1.2 Products offered

- 18.1.1.3 Recent developments

- 18.1.1.3.1 Product launches/developments

- 18.1.1.3.2 Deals

- 18.1.1.3.3 Expansions

- 18.1.1.3.4 Other developments

- 18.1.1.4 MnM view

- 18.1.1.4.1 Key strengths

- 18.1.1.4.2 Strategic choices

- 18.1.1.4.3 Weaknesses and competitive threats

- 18.1.2 CATERPILLAR INC.

- 18.1.2.1 Business overview

- 18.1.2.2 Products offered

- 18.1.2.3 Recent developments

- 18.1.2.3.1 Product launches/developments

- 18.1.2.3.2 Deals

- 18.1.2.3.3 Expansions

- 18.1.2.3.4 Other developments

- 18.1.2.4 MnM view

- 18.1.2.4.1 Key strengths

- 18.1.2.4.2 Strategic choices

- 18.1.2.4.3 Weaknesses and competitive threats

- 18.1.3 KOMATSU LTD.

- 18.1.3.1 Business overview

- 18.1.3.2 Products offered

- 18.1.3.3 Recent developments

- 18.1.3.3.1 Product launches/developments

- 18.1.3.3.2 Deals

- 18.1.3.4 MnM view

- 18.1.3.4.1 Key strengths

- 18.1.3.4.2 Strategic choices

- 18.1.3.4.3 Weaknesses and competitive threats

- 18.1.4 VOLVO CONSTRUCTION EQUIPMENT

- 18.1.4.1 Business overview

- 18.1.4.2 Products offered

- 18.1.4.3 Recent developments

- 18.1.4.3.1 Product launches/developments

- 18.1.4.3.2 Deals

- 18.1.4.3.3 Other developments

- 18.1.4.4 MnM view

- 18.1.4.4.1 Key strengths

- 18.1.4.4.2 Strategic choices

- 18.1.4.4.3 Weaknesses and competitive threats

- 18.1.5 SANY HEAVY INDUSTRIES CO., LTD.

- 18.1.5.1 Business overview

- 18.1.5.2 Products offered

- 18.1.5.3 Recent developments

- 18.1.5.3.1 Product launches/developments

- 18.1.5.3.2 Other developments

- 18.1.5.4 MnM view

- 18.1.5.4.1 Key strengths

- 18.1.5.4.2 Strategic choices

- 18.1.5.4.3 Weaknesses and competitive threats

- 18.1.6 JCB

- 18.1.6.1 Business overview

- 18.1.6.2 Products offered

- 18.1.6.3 Recent developments

- 18.1.6.3.1 Product launches/developments

- 18.1.6.3.2 Deals

- 18.1.6.3.3 Expansions

- 18.1.6.3.4 Other developments

- 18.1.7 DEERE & COMPANY

- 18.1.7.1 Business overview

- 18.1.7.2 Products offered

- 18.1.7.3 Recent developments

- 18.1.7.3.1 Product launches/developments

- 18.1.7.3.2 Deals

- 18.1.7.3.3 Expansions

- 18.1.7.3.4 Other developments

- 18.1.8 SANDVIK AB

- 18.1.8.1 Business overview

- 18.1.8.2 Products offered

- 18.1.8.3 Recent developments

- 18.1.8.3.1 Product launches/developments

- 18.1.8.3.2 Deals

- 18.1.8.3.3 Expansions

- 18.1.8.3.4 Other developments

- 18.1.9 EPIROC AB

- 18.1.9.1 Business overview

- 18.1.9.2 Products offered

- 18.1.9.3 Recent developments

- 18.1.9.3.1 Product launches/developments

- 18.1.9.3.2 Deals

- 18.1.9.3.3 Other developments

- 18.1.10 LIEBHERR

- 18.1.10.1 Business overview

- 18.1.10.2 Products offered

- 18.1.10.3 Recent developments

- 18.1.10.3.1 Product launches/developments

- 18.1.10.3.2 Deals

- 18.1.10.3.3 Other developments

- 18.1.11 BOBCAT COMPANY

- 18.1.11.1 Business overview

- 18.1.11.2 Products offered

- 18.1.11.3 Recent developments

- 18.1.11.3.1 Product launches/developments

- 18.1.11.3.2 Other developments

- 18.1.1 HITACHI CONSTRUCTION MACHINERY CO., LTD.

- 18.2 OTHER PLAYERS

- 18.2.1 SOLETRAC INC.

- 18.2.2 FENDT

- 18.2.3 HUSQVARNA AB

- 18.2.4 XUZHOU CONSTRUCTION MACHINERY GROUP CO., LTD.

- 18.2.5 KUBOTA CORPORATION

- 18.2.6 KOBELCO CONSTRUCTION MACHINERY EUROPE BV

- 18.2.7 BHARAT EARTH MOVERS LIMITED

- 18.2.8 CNH INDUSTRIAL NV

- 18.2.9 WACKER NEUSON SE

- 18.2.10 TAKEUCHI GLOBAL

- 18.2.11 HD HYUNDAI HEAVY INDUSTRIES CO., LTD.

- 18.2.12 LUIGONG MACHINERY CO., LTD.

19 RECOMMENDATIONS FROM MARKETSANDMARKETS

- 19.1 ASIA PACIFIC TO GROW SWIFTLY IN ELECTRIC CONSTRUCTION EQUIPMENT MARKET

- 19.2 HYDROGEN-FUELED CONSTRUCTION EQUIPMENT TO CREATE LUCRATIVE OPPORTUNITIES

- 19.3 EMPHASIS ON ELECTRIFICATION OF UNDERGROUND MINING EQUIPMENT

- 19.4 INTEGRATION OF SOLID-STATE BATTERIES IN ELECTRIC TRACTORS

- 19.5 CONCLUSION

20 APPENDIX

- 20.1 INSIGHTS FROM INDUSTRY EXPERTS

- 20.2 DISCUSSION GUIDE

- 20.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 20.4 CUSTOMIZATION OPTIONS

- 20.4.1 ELECTRIC CONSTRUCTION EQUIPMENT MARKET, BY APPLICATION

- 20.4.1.1 Construction

- 20.4.1.2 Mining

- 20.4.1.3 Agriculture

- 20.4.1.4 Gardening

- 20.4.2 ELECTRIC CONSTRUCTION EQUIPMENT MARKET, BY PROPULSION

- 20.4.2.1 Electric

- 20.4.2.2 Hybrid

- 20.4.2.3 Hydrogen

- 20.4.3 ELECTRIC CONSTRUCTION EQUIPMENT MARKET, BY BATTERY CAPACITY AND BATTERY CHEMISTRY

- 20.4.3.1 <50 kWh

- 20.4.3.2 50-200 kWh

- 20.4.3.3 200-500 kWh

- 20.4.3.4 >500 kWh

- 20.4.3.5 Lithium Iron Phosphate

- 20.4.3.6 Lithium Nickel Manganese Cobalt Oxide

- 20.4.3.7 Other Battery Chemistries

- 20.4.4 ELECTRIC MINING MACHINERY MARKET, BY BATTERY CAPACITY AND CHEMISTRY

- 20.4.4.1 <50 kWh

- 20.4.4.2 50-200 kWh

- 20.4.4.3 200-500 kWh

- 20.4.4.4 >500 kWh

- 20.4.4.5 Lithium Iron Phosphate

- 20.4.4.6 Lithium Nickel Manganese Cobalt Oxide

- 20.4.4.7 Others

- 20.4.5 ELECTRIC AGRICULTURE EQUIPMENT MARKET, BY BATTERY CAPACITY AND CHEMISTRY

- 20.4.5.1 <50 kWh

- 20.4.5.2 50-200 kWh

- 20.4.5.3 200-500 kWh

- 20.4.5.4 >500 kWh

- 20.4.5.5 Lithium Iron Phosphate

- 20.4.5.6 Lithium Nickel Manganese Cobalt Oxide

- 20.4.5.7 Others

- 20.4.6 ELECTRIC CONSTRUCTION EQUIPMENT MARKET FOR ADDITIONAL COUNTRIES

- 20.4.6.1 Australia

- 20.4.6.2 Scandinavian Countries

- 20.4.7 DETAILED ANALYSIS AND PROFILING OF UP TO FIVE ADDITIONAL MARKET PLAYERS

- 20.4.1 ELECTRIC CONSTRUCTION EQUIPMENT MARKET, BY APPLICATION

- 20.5 RELATED REPORTS

- 20.6 AUTHOR DETAILS