|

시장보고서

상품코드

1800731

RWE(Real World Evidence) 솔루션 시장(-2030년) : 컴포넌트(데이터 세트), 용도(의약품/디바이스 개발(암, 심장, 신경), 상환), 최종사용자(제약, 의료 기술, 보험자, 의료 제공업체), 지역별Real World Evidence Solutions Market by Component (Datasets), Application (Drug/Device Development (Cancer, Cardio, Neuro), Reimbursement), End User (Pharma, Medtech, Payers, Provider), Region - Global Forecast to 2030 |

||||||

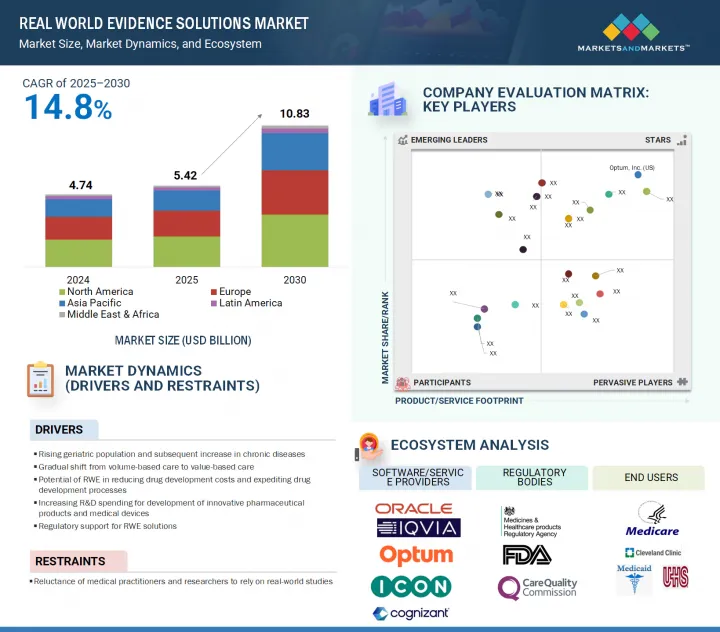

세계의 RWE(Real World Evidence) 솔루션 시장 규모는 2025년 54억 2,000만 달러에서 예측 기간중 CAGR 14.8%로 성장을 지속하여, 2030년에는 108억 3,000만 달러에 이를 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2024-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 금액(달러) |

| 부문 | 컴포넌트, 용도, 전개 모드, 수익 모델, 최종사용자 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

시장의 성장은 가치 기반 의료로의 전환과 만성질환 발생률 증가로 인해 촉진되고 있습니다. RWE(Real World Evidence)는 의약품 개발 과정에서 비용과 시간을 모두 절감할 수 있는 잠재력을 가지고 있습니다. 이에 따라 제약 및 의료기기 기업에서 RWE 솔루션의 채택이 확대되고 있습니다.

"용도별로는 시판 후 조사 부문이 예측 기간 동안 가장 높은 CAGR을 나타낼 것으로 예측됩니다."

규제 당국이 시판 후 의약품 및 의료기기의 장기적인 안전성과 유효성에 대한 관심이 높아짐에 따라 이 분야의 높은 성장을 가속하고 있습니다. 미국 FDA, 유럽 EMA, 일본 PMDA와 같은 규제 기관은 실제 결과를 모니터링하고, 부작용을 식별하고, 제품 성능을 추적하고, 위험 관리 계획을 지원하는 데 중점을 두고 있습니다.

"최종 사용자별로는 제약 및 생명공학 기업 부문이 예측 기간 동안 가장 높은 CAGR로 성장할 것으로 예측됩니다."

시장 성장의 주요 요인으로는 RWE 데이터가 신약 및 의료기기 개발에 대한 임상적 통찰력을 제공하고, 개발 비용과 시간을 절감할 수 있다는 점에서 RWE 솔루션 도입이 증가하고 있다는 점을 들 수 있습니다. 또한, 제약 산업 자체가 크게 성장한 것도 RWE 솔루션의 채택을 가속화하는 또 다른 요인으로 작용하고 있습니다.

"아시아태평양이 예측 기간 동안 가장 높은 CAGR을 나타낼 것으로 예측됩니다."

이러한 급속한 성장은 중국, 인도, 일본, 한국 등 여러 나라에서 진행된 수많은 임상시험과 더불어, 의약품 승인 및 시판 후 조사에서 RWE를 수용하기 시작한 진화하는 규제 프레임워크에 의해 촉진되고 있습니다.

세계의 RWE(Real World Evidence) 솔루션 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술 및 특허 동향, 법 및 규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별/지역별/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요, 주요 기업 개요 등의 정보를 전해드립니다. 프로파일 등을 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 프리미엄 인사이트

제5장 시장 개요

- 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 기회

- 과제

- 업계 동향

- 현실 세계의 데이터 소스

- 생태계 분석

- 밸류체인 분석

- 고객 사업에 영향을 미치는 동향/혼란

- Porter의 Five Forces 분석

- 가격 분석

- 기술 분석

- 관세 및 규제 상황

- 특허 분석

- 주요 컨퍼런스 및 이벤트

- 주요 이해관계자와 구입 기준

- 사례 연구 분석

- 최종사용자 분석

- RWE 솔루션 시장 : 비즈니스 모델

- 투자 및 자금조달 시나리오

- AI/생성형 AI가 RWE 솔루션 시장에 미치는 영향

- 미국 관세

제6장 RWE(Real World Evidence) 솔루션 시장 : 컴포넌트별

- 서비스

- 데이터 세트

- 이종 데이터 세트

- 통합 데이터 세트

제7장 RWE(Real World Evidence) 솔루션 시장 : 용도별

- 의약품 개발, 승인

- 종양

- 심혈관질환

- 신경

- 면역

- 희귀질환

- 기타

- 의료기기 개발 및 승인

- 시판 후 조사

- 시장 접근과 상환/적용 범위 의사결정

- 임상 및 규제상 의사결정

- 기타

제8장 RWE(Real World Evidence) 솔루션 시장 : 수익 모델별

- 종량 빌링(가치 기반 가격 결정)

- 구독

- 라이선스

제9장 RWE(Real World Evidence) 솔루션 시장 : 전개 모드별

- On-Premise

- 클라우드 기반

- 하이브리드

제10장 RWE(Real World Evidence) 솔루션 시장 : 최종사용자별

- 제약 기업 및 바이오테크놀러지 기업

- 의료 기술 기업

- 보험자

- 공적 보험자

- 민간 보험자

- 의료 제공업체

- 병원

- 클리닉, 기타 외래 진료소

- 기타

- 기타

제11장 RWE(Real World Evidence) 솔루션 시장 : 지역별

- 북미

- 거시경제 전망

- 미국

- 캐나다

- 유럽

- 거시경제 전망

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타

- 아시아태평양

- 거시경제 전망

- 일본

- 중국

- 인도

- 호주

- 한국

- 기타

- 라틴아메리카

- 거시경제 전망

- 브라질

- 멕시코

- 기타

- 중동 및 아프리카

- 거시경제 전망

- GCC 국가

- 남아프리카

- 기타

제12장 경쟁 구도

- 주요 시장 진출기업의 전략/강점

- 매출 분배 분석

- 시장 점유율 분석

- 기업 평가 매트릭스 : 주요 기업

- 기업 평가 매트릭스 : 스타트업 기업/중소기업

- 브랜드/제품 비교

- 평가와 재무 지표

- 경쟁 시나리오

제13장 기업 개요

- 주요 기업

- IQVIA

- MERATIVE

- OPTUM, INC.

- ICON PLC

- SYNEOS HEALTH

- PAREXEL INTERNATIONAL(MA) CORPORATION

- FLATIRON HEALTH

- FORTREA

- ORACLE

- ELEVANCE HEALTH

- SAS INSTITUTE INC.

- AETION, INC.

- TRINETX, LLC

- TRINITY

- MEDIDATA

- COGNIZANT TECHNOLOGY SOLUTIONS CORPORATION

- CEGEDIM HEALTH DATA

- VERANTOS

- MEDPACE

- TATA CONSULTANCY SERVICES LIMITED

- 기타 기업

- HEALTHVERITY, INC.

- OM1

- OPEN HEALTH

- TEMPUS

- QUANTZIG

제14장 부록

LSH 25.09.05The global real world evidence solutions market is projected to reach USD 10.83 billion by 2030 from USD 5.42 billion in 2025, at a CAGR of 14.8% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Component, Application, Deployment Mode, Revenue Model, and End User |

| Regions covered | North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa |

The market's growth is fueled by the transition to value-based care and the increasing incidence of chronic diseases. Real world evidence (RWE) can potentially reduce both costs and time in the drug development process. This has resulted in the growing adoption of RWE solutions across pharmaceutical & medical device companies.

"By component, the data sets segment is expected to grow at the highest CAGR during the forecast period."

Based on component, the real world evidence solution market is segmented into services, data sets, and integrated data sets. The data sets segment is projected to grow at the highest CAGR during the forecast period. With the growing digitization of healthcare and increasing acceptance of real world data by regulators such as the FDA and EMA; the demand for high-quality, curated datasets, such as EHRs, claims, and registry data, has surged. These datasets power analytics, AI models, and health economics studies, making them critical assets for pharma, biotech, and healthcare companies. Additionally, their recurring revenue potential through licensing further drives their dominance in the RWE landscape.

"By application, the post-market surveillance segment is expected to register the highest CAGR during the forecast period."

By application, the real world evidence solutions market is segmented into drug development & approvals, medical device development & approvals, post-market surveillance, market access & reimbursement decision-making, clinical & regulatory decision-making, and other applications. The post-market surveillance segment is expected to register the highest CAGR during the forecast period. The increasing regulatory focus on long-term safety and the efficacy of drugs & medical devices after market approval drives the high growth rate of this segment. Regulatory agencies such as the US FDA, the EMA, and the PMDA in Japan have emphasized monitoring real-world outcomes to identify adverse events, track product performance, and support risk management plans.

"By end user, the pharmaceutical & biotechnology companies segment is projected to grow at the highest CAGR during the forecast period."

The RWE solutions market is segmented by end users into pharmaceutical & biotechnology companies, MedTech companies, healthcare payers, healthcare providers, and other end users. The pharmaceutical & biotechnological companies segment is projected to grow at the highest CAGR during the forecast period. The key factors contributing to market growth include adopting RWE solutions to decrease the costs & time for drug development, as RWE data provides clinical insights on the development of new drugs & medical devices. The high growth in the pharmaceutical industry is also an additional factor, fueling the adoption of real world solutions.

"The Asia Pacific region is projected to register the highest CAGR during the forecast period."

The market is segmented by region into North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa. The RWE solutions market in the Asia Pacific region is projected to register the highest CAGR during the forecast period. The high growth rate of this region is attributed to the rising initiatives towards adopting RWE by pharmaceutical & medical device companies. This rapid expansion is driven by the high volume of clinical trials undertaken by emerging economies such as China, India, Japan, and South Korea, along with evolving regulatory frameworks that are beginning to accept RWE for drug approvals and post-market surveillance.

Breakdown of supply-side primary interviews, by company type, designation, and region:

- By Company Type: Tier 1 (40%), Tier 2 (35%), and Tier 3 (25%)

- By Designation: C-level (35%), Director-level (45%), and Others (20%)

- By Region: North America (55%), Europe (20%), the Asia Pacific (15%), Latin America (5%), and the Middle East & Africa (5%)

List of Companies Profiled in the Report

- IQVIA Inc. (US)

- Merative (US)

- Optum Inc. (US)

- ICON Plc (Ireland)

- Syneos Health (US)

- Parexel International Corporation (US)

- Tata Consultancy Services (India)

- Oracle (US)

- Elevance Health (US)

- SAS Institute Inc. (US)

- Aetion Inc. (US)

- Trinetx LLC (US)

- Trinity (US)

- Cognizant Technology Solutions Corporation (US)

- Cegedim Health Data (France)

- Verantos (US)

- Medspace Holdings Inc. (US)

- FLATIRON HEALTH (US)

- Fortrea (US)

- Medidata (US) (subsidiary of Dassault Systemes)

- HealthVerity, Inc. (US)

- Quantzig (US)

- OPEN Health (UK)

- Tempus (US)

- Certara (US)

Research Coverage

This report studies the real world evidence solutions market based on component, application, revenue model, deployment mode, end user, and region. The report also analyzes market growth factors (drivers, restraints, opportunities, and challenges). It evaluates the market's opportunities and challenges for stakeholders and details the competitive landscape for market leaders. The report also studies micro markets concerning their growth trends, prospects, and contributions to the total real world evidence solutions market. The report forecasts the revenue of the market segments in five regions.

Reasons to Buy the Report

This report also includes.

- Analysis of key drivers (rising geriatric population and rise in incidences of chronic diseases, shift from volume-based care to value-based care, potential of RWE in reducing drug development costs and expediting drug development process, increased R&D spending for development of new pharmaceutical products and medical devices, and support from regulatory bodies for use of RWE solutions), restraints (reluctance of medical practitioners and researchers to rely on real-world studies), opportunities (increase focus on end-to-end RWE services, and growth opportunities in emerging markets), and challenges (scarcity of skilled personnel, and the lack of universally accepted methodology principles and data processing infrastructure).

- Product Development/Innovation: Detailed insights on upcoming trends, research & development activities, and new software launches in the real world evidence solutions market.

- Market Development: Comprehensive information on the lucrative emerging markets, by component, application, revenue model, deployment mode, end user, and region.

- Market Diversification: Exhaustive information about the software portfolios, growing geographies, recent developments, and investments in the real world evidence solutions market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, company evaluation matrix, and capabilities of leading players in the global real world evidence solutions market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key industry insights

- 2.1.1 SECONDARY DATA

- 2.2 RESEARCH METHODOLOGY DESIGN

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 BOTTOM-UP APPROACH

- 2.3.2 TOP-DOWN APPROACH

- 2.4 MARKET BREAKDOWN AND DATA TRIANGULATION

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RISK ASSESSMENT

- 2.7 LIMITATIONS

- 2.7.1 SCOPE-RELATED LIMITATIONS

- 2.7.2 METHODOLOGY-RELATED LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 REAL WORLD EVIDENCE SOLUTIONS MARKET OVERVIEW

- 4.2 ASIA PACIFIC: REAL WORLD EVIDENCE SOLUTIONS MARKET, BY END USER AND COUNTRY

- 4.3 REAL WORLD EVIDENCE SOLUTIONS MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 4.4 REGIONAL MIX: REAL WORLD EVIDENCE SOLUTIONS MARKET, 2025-2030

- 4.5 REAL WORLD EVIDENCE SOLUTIONS MARKET: DEVELOPED MARKETS VS. EMERGING ECONOMIES, 2025 VS. 2030

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Rising geriatric population and subsequent increase in prevalence of chronic diseases

- 5.2.1.2 Shift from volume-based care to value-based care

- 5.2.1.3 Potential of real world evidence in reducing drug development costs and expediting drug development process

- 5.2.1.4 Increased R&D spending for development of new pharmaceutical products and medical devices

- 5.2.1.5 Support from regulatory bodies for use of real world evidence solutions

- 5.2.2 RESTRAINTS

- 5.2.2.1 Reluctance of medical practitioners and researchers to rely on real world studies

- 5.2.2.2 Data quality and standardization issues

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Growth opportunities in emerging markets

- 5.2.3.2 Increased focus on end-to-end RWE services

- 5.2.3.3 Increased focus on personalized and precision medicine

- 5.2.3.4 Market access, health technology assessment (HTA), and reimbursement

- 5.2.4 CHALLENGES

- 5.2.4.1 Lack of universally accepted methodology standards and data processing infrastructure

- 5.2.4.2 Shortage of skilled professionals

- 5.2.1 DRIVERS

- 5.3 INDUSTRY TRENDS

- 5.3.1 EMERGING ROLE OF WEARABLE DEVICES

- 5.3.2 SOCIAL MEDIA-SOURCED RWE

- 5.3.3 RISING USE OF RWD AND RWE ACROSS PHARMACEUTICAL INDUSTRY

- 5.3.4 RWE ANALYTICS APPROACH: INTERNAL VS. OUTSOURCED

- 5.3.5 INCORPORATION OF ARTIFICIAL INTELLIGENCE INTO RWD MANAGEMENT

- 5.4 REAL WORLD DATA SOURCES

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 VALUE CHAIN ANALYSIS

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 PORTER'S FIVE FORCES ANALYSIS

- 5.8.1 THREAT FROM NEW ENTRANTS

- 5.8.2 BARGAINING POWER OF SUPPLIERS

- 5.8.3 BARGAINING POWER OF BUYERS

- 5.8.4 THREAT FROM SUBSTITUTES

- 5.8.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.9 PRICING ANALYSIS

- 5.9.1 INDICATIVE PRICING FOR REAL WORLD EVIDENCE SOLUTIONS, BY COMPONENT

- 5.9.2 INDICATIVE PRICING OF REAL WORLD EVIDENCE SOLUTIONS, BY REGION

- 5.10 TECHNOLOGY ANALYSIS

- 5.10.1 KEY TECHNOLOGIES

- 5.10.1.1 Use of AI and ML

- 5.10.1.2 Blockchain technology

- 5.10.2 ADJACENT TECHNOLOGIES

- 5.10.2.1 Predictive analytics

- 5.10.2.2 Visualization dashboard software

- 5.10.3 COMPLEMENTARY TECHNOLOGIES

- 5.10.3.1 Electronic health records (EHRs)

- 5.10.3.2 Clinical trial management system

- 5.10.1 KEY TECHNOLOGIES

- 5.11 TARIFF AND REGULATORY LANDSCAPE

- 5.11.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.11.2 REGULATORY ANALYSIS

- 5.11.2.1 North America

- 5.11.2.1.1 US

- 5.11.2.1.1.1 Use cases

- 5.11.2.1.2 Canada

- 5.11.2.1.1 US

- 5.11.2.2 Europe

- 5.11.2.3 Asia Pacific

- 5.11.2.3.1 China

- 5.11.2.3.2 Japan

- 5.11.2.3.3 India

- 5.11.2.4 Middle East & Africa

- 5.11.2.5 Latin America

- 5.11.2.1 North America

- 5.12 PATENT ANALYSIS

- 5.12.1 PATENT PUBLICATION TRENDS FOR REAL WORLD EVIDENCE SOLUTIONS MARKET

- 5.12.2 JURISDICTION AND TOP APPLICANT ANALYSIS

- 5.13 KEY CONFERENCES & EVENTS

- 5.14 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.14.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.14.2 BUYING CRITERIA

- 5.15 CASE STUDY ANALYSIS

- 5.15.1 DESIGNING AND BUILDING RWE DASHBOARDS AND LEVERAGING EHR AND CLAIMS DATA

- 5.15.2 INTEGRATING SPECIALTY PHARMACY AND PATIENT HUB DATA WITH RWD DATA TO INVESTIGATE INTO NON-ADHERENCE FACTORS

- 5.15.3 SIMPLIFYING DATA ANALYTICS WITH RWE PLATFORM

- 5.16 END USER ANALYSIS

- 5.16.1 UNMET NEEDS

- 5.16.2 END USER EXPECTATIONS

- 5.17 REAL WORLD EVIDENCE SOLUTIONS MARKET: BUSINESS MODELS

- 5.17.1 PLATFORM-AS-A-SERVICE (PAAS) MODEL

- 5.17.2 DATA PROVIDER MODEL

- 5.17.3 CONSULTING AND SERVICES MODEL

- 5.17.4 COLLABORATIVE RESEARCH MODEL

- 5.18 INVESTMENT & FUNDING SCENARIO

- 5.19 IMPACT OF AI/GENERATIVE AI ON REAL WORLD EVIDENCE SOLUTIONS MARKET

- 5.19.1 TOP USE CASES & MARKET POTENTIAL

- 5.19.1.1 Key use cases

- 5.19.2 IMPLEMENTATION OF AI/GENERATIVE AI: CASE STUDIES

- 5.19.2.1 AI-powered RWE transformed patient targeting and treatment initiation

- 5.19.3 IMPACT OF GENERATIVE AI ON INTERCONNECTED AND ADJACENT MARKET ECOSYSTEM

- 5.19.3.1 Electronic health record (EHR) market

- 5.19.3.2 Real world data (RWD) market

- 5.19.4 USER READINESS AND IMPACT ASSESSMENT

- 5.19.1 TOP USE CASES & MARKET POTENTIAL

- 5.20 US TARIFF 2025

- 5.20.1 INTRODUCTION

- 5.20.2 KEY TARIFF RATES

- 5.20.3 PRICE IMPACT ANALYSIS

- 5.20.4 IMPACT ON COUNTRY/REGION

- 5.20.4.1 US

- 5.20.4.2 Europe

- 5.20.4.3 Asia Pacific

- 5.20.5 IMPACT ON END-USE INDUSTRIES

6 REAL WORLD EVIDENCE SOLUTIONS MARKET, BY COMPONENT

- 6.1 INTRODUCTION

- 6.2 SERVICES

- 6.2.1 RISING NEED TO CONVERT DATA INTO ACTIONABLE EVIDENCE TO DRIVE DEMAND

- 6.3 DATA SETS

- 6.3.1 DISPARATE DATA SETS

- 6.3.1.1 Clinical settings data sets

- 6.3.1.1.1 Increasing utilization of EHR data for trial recruitment to fuel growth

- 6.3.1.2 Claims data sets

- 6.3.1.2.1 Growing need to understand economic benefits of drug reimbursement by payers to drive growth

- 6.3.1.3 Pharmacy data sets

- 6.3.1.3.1 Increasing adoption of e-prescribing systems to drive growth

- 6.3.1.4 Patient-powered data sets

- 6.3.1.4.1 Increasing need to access opinions on diseases and treatments across social media to drive growth

- 6.3.1.5 Registry-based data sets

- 6.3.1.5.1 Increasing number of disease registries to drive demand for registry-based data sets in evidence generation

- 6.3.1.6 Others

- 6.3.1.6.1 Increasing number of genomics registries to drive demand for RWE evidence solutions

- 6.3.1.1 Clinical settings data sets

- 6.3.2 INTEGRATED DATA SETS

- 6.3.2.1 Increasing demand for integrated data from multiple sources to drive growth

- 6.3.1 DISPARATE DATA SETS

7 REAL WORLD EVIDENCE SOLUTIONS MARKET, BY APPLICATION

- 7.1 INTRODUCTION

- 7.2 DRUG DEVELOPMENT & APPROVALS

- 7.2.1 ONCOLOGY

- 7.2.1.1 Growing number of clinical trials focused on cancer treatment to drive demand

- 7.2.2 CARDIOVASCULAR DISEASES

- 7.2.2.1 High prevalence of cardiovascular diseases to support market growth

- 7.2.3 NEUROLOGY

- 7.2.3.1 Rapidly aging global population and subsequent increase in prevalence of neurological disorders to drive growth

- 7.2.4 IMMUNOLOGY

- 7.2.4.1 Increasing focus on developing innovative products to drive growth

- 7.2.5 RARE DISEASES

- 7.2.5.1 Need for harnessing RWE to advance therapies for rare diseases to boost market

- 7.2.6 OTHER THERAPEUTIC AREAS

- 7.2.1 ONCOLOGY

- 7.3 MEDICAL DEVICE DEVELOPMENT & APPROVALS

- 7.3.1 INCREASING RESEARCH IN MEDICAL DEVICE DEVELOPMENT TO DRIVE DEMAND

- 7.4 POST-MARKET SURVEILLANCE

- 7.4.1 EXTENSIVE USE OF RWE SOLUTIONS IN POST-MARKET SURVEILLANCE TO BOOST MARKET

- 7.5 MARKET ACCESS & REIMBURSEMENT/COVERAGE DECISION-MAKING

- 7.5.1 GROWING USE OF RWE SOLUTIONS TO DEVELOP ECONOMIC AND BUDGET IMPACT MODELS TO FAVOR MARKET GROWTH

- 7.6 CLINICAL & REGULATORY DECISION-MAKING

- 7.6.1 LIMITED VALIDITY OF RANDOMIZED CONTROLLED TRIALS TO DRIVE USE OF RWE SOLUTIONS

- 7.7 OTHER APPLICATIONS

8 REAL WORLD EVIDENCE SOLUTIONS MARKET, BY REVENUE MODEL

- 8.1 INTRODUCTION

- 8.2 PAY-PER-USAGE (VALUE-BASED PRICING)

- 8.2.1 RISING DEMAND FOR COST-EFFECTIVE AND FLEXIBLE SOLUTIONS TO BOOST MARKET

- 8.3 SUBSCRIPTION

- 8.3.1 RISING PREFERENCE FOR FLEXIBILITY AND SCALABILITY TO SUPPORT MARKET GROWTH

- 8.4 LICENSE

- 8.4.1 FOCUS ON ENABLING END-TO-END RWE DELIVERY THROUGH PLATFORM LICENSING TO DRIVE MARKET

9 REAL WORLD EVIDENCE SOLUTIONS MARKET, BY DEPLOYMENT MODE

- 9.1 INTRODUCTION

- 9.2 ON-PREMISES

- 9.2.1 NEED FOR ENHANCED DATA CONTROL BENEFITS TO BOOST DEMAND

- 9.3 CLOUD-BASED

- 9.3.1 INCREASED SCALABILITY AND FLEXIBILITY IN DATA COLLECTION TO DRIVE GROWTH

- 9.4 HYBRID

- 9.4.1 EMPHASIS ON INCREASED SCALABILITY AND FLEXIBILITY IN DATA COLLECTION TO DRIVE GROWTH

10 REAL WORLD EVIDENCE SOLUTIONS MARKET, BY END USER

- 10.1 INTRODUCTION

- 10.2 PHARMACEUTICAL & BIOTECHNOLOGY COMPANIES

- 10.2.1 INCREASED R&D EXPENDITURE IN INNOVATIVE MEDICINES TO DRIVE MARKET GROWTH

- 10.3 MEDTECH COMPANIES

- 10.3.1 NEED FOR ACCELERATING MEDTECH MARKET ACCESS VIA REAL WORLD EVIDENCE SOLUTIONS TO BOOST GROWTH

- 10.4 HEALTHCARE PAYERS

- 10.4.1 INCREASED FOCUS ON OUTCOME-BASED PAYMENT MODELS TO DRIVE DEMAND

- 10.5 PUBLIC PAYERS

- 10.5.1 FOCUS ON ENHANCING PUBLIC PAYER DECISION-MAKING WITH RWE SOLUTIONS TO BOOST MARKET

- 10.6 PRIVATE PAYERS

- 10.6.1 NEED FOR LEVERAGING PRIVATE PAYERS FOR SUSTAINABLE RWE SOLUTIONS TO SPUR DEMAND

- 10.7 HEALTHCARE PROVIDERS

- 10.7.1 GROWING FOCUS ON IMPROVING PROFITABILITY TO SUPPORT MARKET GROWTH

- 10.7.2 HOSPITALS

- 10.7.3 CLINICS & OTHER OUTPATIENT SETTINGS

- 10.7.4 OTHER HEALTHCARE PROVIDERS

- 10.8 OTHER END USERS

11 REAL WORLD EVIDENCE SOLUTIONS MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 NORTH AMERICA: MACROECONOMIC OUTLOOK

- 11.2.2 US

- 11.2.2.1 US to account for significant share of North American market

- 11.2.3 CANADA

- 11.2.3.1 Increase in pharma hub growth in Canada to drive market

- 11.3 EUROPE

- 11.3.1 EUROPE: MACROECONOMIC OUTLOOK

- 11.3.2 GERMANY

- 11.3.2.1 High pharmaceutical R&D spending in Germany to boost market growth

- 11.3.3 UK

- 11.3.3.1 Growing adoption of HTA to support market growth

- 11.3.4 FRANCE

- 11.3.4.1 Need for extensive and diversified database to drive market growth

- 11.3.5 ITALY

- 11.3.5.1 High demand for RWE due to widespread use of pay-for-outcomes to drive market

- 11.3.6 SPAIN

- 11.3.6.1 Rising R&D expenditure to propel market growth

- 11.3.7 REST OF EUROPE

- 11.4 ASIA PACIFIC

- 11.4.1 ASIA PACIFIC: MACROECONOMIC OUTLOOK

- 11.4.2 JAPAN

- 11.4.2.1 Stringent regulatory scenario in Japan to restrain market growth

- 11.4.3 CHINA

- 11.4.3.1 Low cost of clinical trials and large pharmaceutical R&D base in China to drive market

- 11.4.4 INDIA

- 11.4.4.1 Growing adoption of outcome-based research to drive market

- 11.4.5 AUSTRALIA

- 11.4.5.1 Policy reforms and strong regulations to support market growth

- 11.4.6 SOUTH KOREA

- 11.4.6.1 Increased focus on pharma R&D to boost market growth

- 11.4.7 REST OF ASIA PACIFIC

- 11.5 LATIN AMERICA

- 11.5.1 LATIN AMERICA: MACROECONOMIC OUTLOOK

- 11.5.2 BRAZIL

- 11.5.2.1 Evolving regulatory frameworks that facilitate clinical research to drive market

- 11.5.3 MEXICO

- 11.5.3.1 Increased funding and investments in pharma R&D to favor growth

- 11.5.4 REST OF LATIN AMERICA

- 11.6 MIDDLE EAST & AFRICA

- 11.6.1 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

- 11.6.2 GCC COUNTRIES

- 11.6.2.1 Growing availability of healthcare funding to offer opportunities for market growth

- 11.6.2.2 Saudi Arabia

- 11.6.2.2.1 Digital health reform and regulatory innovation to offer opportunities for market growth

- 11.6.2.3 UAE

- 11.6.2.3.1 Need for driving data-driven healthcare transformation to boost market

- 11.6.2.4 Rest of GCC

- 11.6.3 SOUTH AFRICA

- 11.6.3.1 Emphasis on supporting healthcare infrastructure to drive market growth

- 11.6.4 REST OF MIDDLE EAST & AFRICA

12 COMPETITIVE LANDSCAPE

- 12.1 INTRODUCTION

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 12.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS

- 12.3 REVENUE SHARE ANALYSIS

- 12.4 MARKET SHARE ANALYSIS

- 12.5 COMPANY EVALUATION MATRIX: KEY PLAYERS

- 12.5.1 STARS

- 12.5.2 EMERGING LEADERS

- 12.5.3 PERVASIVE PLAYERS

- 12.5.4 PARTICIPANTS

- 12.5.5 COMPANY FOOTPRINT

- 12.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES

- 12.6.1 PROGRESSIVE COMPANIES

- 12.6.2 RESPONSIVE COMPANIES

- 12.6.3 DYNAMIC COMPANIES

- 12.6.4 STARTING BLOCKS

- 12.6.5 COMPETITIVE BENCHMARKING

- 12.7 BRAND/PRODUCT COMPARISON

- 12.8 VALUATION AND FINANCIAL METRICS

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 PRODUCT LAUNCHES/ENHANCEMENTS

- 12.9.2 DEALS

- 12.9.3 OTHER DEVELOPMENTS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 IQVIA

- 13.1.1.1 Business overview

- 13.1.1.2 Products offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Deals

- 13.1.1.4 MnM view

- 13.1.1.4.1 Key strengths/Right to win

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses and competitive threats

- 13.1.2 MERATIVE

- 13.1.2.1 Business overview

- 13.1.2.2 Products offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Deals

- 13.1.2.3.2 Other developments

- 13.1.2.4 MnM view

- 13.1.2.4.1 Key strengths/Right to win

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses and competitive threats

- 13.1.3 OPTUM, INC.

- 13.1.3.1 Business overview

- 13.1.3.2 Products offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product launches/developments

- 13.1.3.3.2 Deals

- 13.1.3.4 MnM view

- 13.1.3.4.1 Key strengths/Right to win

- 13.1.3.4.2 Strategic choices made

- 13.1.3.4.3 Weaknesses and competitive threats

- 13.1.4 ICON PLC

- 13.1.4.1 Business overview

- 13.1.4.2 Products offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Product launches/developments

- 13.1.4.3.2 Deals

- 13.1.4.4 MnM view

- 13.1.4.4.1 Key strengths/Right to win

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses and competitive threats

- 13.1.5 SYNEOS HEALTH

- 13.1.5.1 Business overview

- 13.1.5.2 Products offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Deals

- 13.1.5.4 MnM view

- 13.1.5.4.1 Key strengths/Right to win

- 13.1.5.4.2 Strategic choices

- 13.1.5.4.3 Weaknesses and competitive threats

- 13.1.6 PAREXEL INTERNATIONAL (MA) CORPORATION

- 13.1.6.1 Business overview

- 13.1.6.2 Products offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Product launches/developments

- 13.1.6.3.2 Deals

- 13.1.7 FLATIRON HEALTH

- 13.1.7.1 Business overview

- 13.1.7.2 Products offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Product launches/developments

- 13.1.7.3.2 Deals

- 13.1.8 FORTREA

- 13.1.8.1 Business overview

- 13.1.8.2 Products offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Product launches/developments

- 13.1.8.3.2 Deals

- 13.1.9 ORACLE

- 13.1.9.1 Business overview

- 13.1.9.2 Products offered

- 13.1.9.3 Recent developments

- 13.1.9.3.1 Product launches/developments

- 13.1.9.3.2 Deals

- 13.1.10 ELEVANCE HEALTH

- 13.1.10.1 Business overview

- 13.1.10.2 Products offered

- 13.1.11 SAS INSTITUTE INC.

- 13.1.11.1 Business overview

- 13.1.11.2 Products offered

- 13.1.11.3 Recent developments

- 13.1.11.3.1 Product launches/developments

- 13.1.12 AETION, INC.

- 13.1.12.1 Business overview

- 13.1.12.2 Products offered

- 13.1.12.3 Recent developments

- 13.1.12.3.1 Product launches/developments

- 13.1.12.3.2 Deals

- 13.1.13 TRINETX, LLC

- 13.1.13.1 Business overview

- 13.1.13.2 Products offered

- 13.1.13.3 Recent developments

- 13.1.13.3.1 Product launches/developments

- 13.1.13.3.2 Deals

- 13.1.14 TRINITY

- 13.1.14.1 Business overview

- 13.1.14.2 Products offered

- 13.1.14.3 Recent developments

- 13.1.14.3.1 Deals

- 13.1.15 MEDIDATA

- 13.1.15.1 Business overview

- 13.1.15.2 Products offered

- 13.1.15.3 Recent developments

- 13.1.15.3.1 Product launches/developments

- 13.1.15.3.2 Deals

- 13.1.16 COGNIZANT TECHNOLOGY SOLUTIONS CORPORATION

- 13.1.16.1 Business overview

- 13.1.16.2 Products offered

- 13.1.17 CEGEDIM HEALTH DATA

- 13.1.17.1 Business overview

- 13.1.17.2 Products offered

- 13.1.17.3 Recent developments

- 13.1.17.3.1 Product launches/developments

- 13.1.17.3.2 Deals

- 13.1.18 VERANTOS

- 13.1.18.1 Business overview

- 13.1.18.2 Products offered

- 13.1.18.3 Recent developments

- 13.1.18.3.1 Product launches/developments

- 13.1.18.3.2 Deals

- 13.1.19 MEDPACE

- 13.1.19.1 Business overview

- 13.1.19.2 Products offered

- 13.1.20 TATA CONSULTANCY SERVICES LIMITED

- 13.1.20.1 Business overview

- 13.1.20.2 Products offered

- 13.1.20.3 Recent developments

- 13.1.20.3.1 Deals

- 13.1.1 IQVIA

- 13.2 OTHER PLAYERS

- 13.2.1 HEALTHVERITY, INC.

- 13.2.2 OM1

- 13.2.3 OPEN HEALTH

- 13.2.4 TEMPUS

- 13.2.5 QUANTZIG

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 CUSTOMIZATION OPTIONS

- 14.4 RELATED REPORTS

- 14.5 AUTHOR DETAILS