|

시장보고서

상품코드

1811728

안과 영상 시장 : 기술별, 제품별, 용도별, 최종 사용자별, 지역별 예측(-2030년)Ophthalmic Imaging Market by Product Type, Application, End User - Global Forecast to 2030 |

||||||

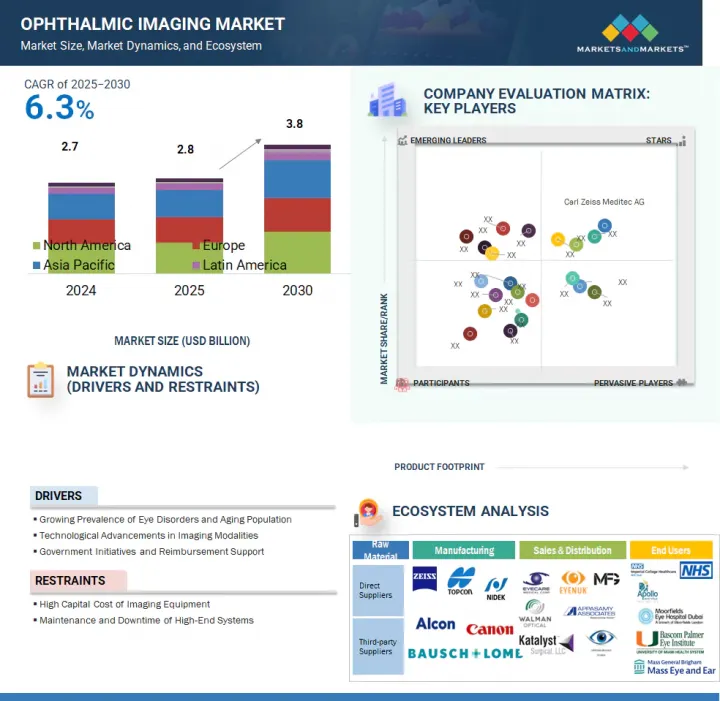

안과 영상 시장 규모는 예측 기간 동안 6.3%의 연평균 성장률(CAGR)로 확대되어 2025년 28억 3,000만 달러에서 2030년에 38억 4,000만 달러에 이를 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2024-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 검토 단위 | 금액(10억 달러) |

| 부문 | 기술별, 제품별, 용도별, 최종 사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카, GCC 국가 |

안과 영상 시장은 특히 고령화되는 전 세계 인구에서 녹내장, 당뇨성 망막병증, 노인성 황반변성과 같은 안과 질환의 유병률 증가에 의해 촉진되고 있습니다. 조기 및 정확한 진단에 대한 수요 증가, OCT 및 안저 카메라와 같은 영상 기술의 발전, 예방적 안과 치료에 대한 인식 제고가 시장 성장을 촉진하고 있습니다. 또한 정부의 유리한 정책과 의료비 지출 증가가 시장 확장을 뒷받침하고 있습니다. 그러나 높은 장비 비용, 특정 지역의 제한된 보험 적용, 숙련된 전문가 부족은 특히 저소득 및 농촌 지역에서 광범위한 도입을 저해하고 있습니다. 임상 워크플로우에서의 데이터 관리 및 통합 문제도 일부 의료 시설의 효율성을 제한합니다. 휴대용 AI 통합 영상 장치 개발과 의료 서비스가 부족한 인구층을 대상으로 한 원격 안과 서비스 확장에 기회가 있습니다.

제품별로는 OCT 시스템 부문이 예측 기간 동안 가장 높은 성장률을 보일 것으로 예상됩니다. 광간섭단층촬영(OCT) 시스템은 망막 및 시신경 질환의 조기 진단에 필수적인 비침습적 초고해상도 영상 촬영을 제공하기 때문에 예측 기간 동안 가장 높은 연평균 복합 성장률(연평균 성장률(CAGR))을 기록할 전망입니다. 스윕 소스 OCT, OCT 혈관조영술, AI 기반 분석과 같은 기술적 발전은 진단 능력과 워크플로우 효율성을 향상시킵니다. 소형 휴대용 OCT 기기는 일차 진료 및 농촌 지역에서의 접근성을 확대되고 있습니다. 당뇨병, 녹내장, 황반변성(AMD)의 전 세계적 유병률 증가와 함께 의료 투자 확대 및 유리한 보험 적용이 더해져 OCT 도입과 시장 급속 확대를 촉진하고 있습니다.

최종 사용자별로 보면, 안과 클리닉 부문은 눈 건강과 정기 시력 검진에 대한 소비자 인식 증가로 예측 기간 동안 가장 높은 성장률을 보일 것으로 예상됩니다. 이들은 접근성 높고 경제적인 안과 검진을 제공하는 일차 진료 허브 역할을 합니다. OCT, 안저 카메라, 시야 분석기 등 휴대용 고해상도 진단 장비의 클리닉 내 도입 증가가 이러한 동향을 더욱 가속화합니다. 진료소는 업무 효율성 향상과 신속한 진단을 위해 인공지능 기반 소형 장비에 대한 투자를 확대하고 있습니다. 또한 원격 검안 및 원격 검진 모델의 성장은 특히 의료 서비스가 부족한 지역에서 확장 가능한 접근성을 뒷받침하여 진료소 기반의 지속적인 확장을 촉진하고 있습니다.

아시아태평양 지역은 급속한 인구 고령화, 녹내장 및 백내장 및 당뇨성 망막병증 등 안과 질환 유병률 증가, 중국 및 인도 등 주요국의 의료 인프라 투자 확대로 예측 기간 동안 가장 높은 성장률을 보일 전망입니다. 정부는 원격 안과 네트워크와 이동식 클리닉을 통해 접근성을 확대하고 있으며, 지역별 혁신과 저렴한 장비 생산은 의료 취약 지역에서의 도입을 촉진하고 있습니다. 기술 도입, 특히 OCT, AI 공구 및 멀티모달 플랫폼은 지역 전반의 성장을 가속화하고 있습니다.

본 보고서에서는 세계의 안과 영상 시장에 대해 조사했으며, 기술별, 제품별, 용도별, 최종 사용자별, 지역별 동향 및 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

- 소개

- 시장 역학

- 고객의 비즈니스에 영향을 미치는 동향 및 혼란

- 가격 분석

- 밸류체인 분석

- 공급망 분석

- 생태계 분석

- 투자 및 자금조달 시나리오

- 기술 분석

- 업계 동향

- 특허 분석

- 무역 분석

- 주된 회의 및 이벤트(2025-2026년)

- 사례 연구 분석

- 규제 분석

- Porter's Five Forces 분석

- 주요 이해관계자와 구매 기준

- 미충족 요구, 최종 사용자 기대

- 미국 관세가 안과 영상 시장에 미치는 영향(2025년)

- AI/생성형 AI가 안과 영상 시장에 미치는 영향

- 인접 시장 분석

제6장 안과 영상 시장(기술별)

- 소개

- AI 기반 기기

- AI 비기반 기기

제7장 안과 영상 시장(제품별)

- 소개

- 광학 일관성 단층 촬영 시스템

- 안과용 초음파 시스템

- 안저 카메라

- 세극등 검사기

- 스페큘러 마이크로스코프

- 안압계

- 안저경

- 망막경

- 기타

제8장 안과 영상 시장(용도별)

- 소개

- 녹내장

- 백내장

- 망막병증

- 굴절 이상

- 노인성 황반변성

- 기타

제9장 안과 영상 시장(최종사용자별)

- 소개

- 병원

- 안과 클리닉

- 검안 클리닉

- 기타

제10장 안과 영상 시장(지역별)

- 소개

- 북미

- 북미의 거시경제 전망

- 미국

- 캐나다

- 유럽

- 유럽의 거시 경제 전망

- 독일

- 프랑스

- 영국

- 이탈리아

- 스페인

- 기타

- 아시아태평양

- 아시아태평양의 거시 경제 전망

- 일본

- 중국

- 인도

- 한국

- 호주

- 기타

- 라틴아메리카

- 라틴아메리카의 거시 경제 전망

- 브라질

- 멕시코

- 기타

- 중동 및 아프리카

- GCC 국가

제11장 경쟁 구도

- 소개

- 주요 진입기업의 전략 및 강점

- 수익 분석(2020-2024년)

- 시장 점유율 분석(2024년)

- 기업평가 매트릭스 : 주요 진입기업(2024년)

- 기업평가 매트릭스 : 스타트업, 중소기업(2024년)

- 기업평가와 재무지표

- 브랜드, 제품 비교

- 경쟁 시나리오

제12장 기업 프로파일

- 주요 진출기업

- CARL ZEISS MEDITEC AG

- TOPCON CORPORATION

- NIDEK CO., LTD.

- HALMA PLC

- ALCON

- HEIDELBERG ENGINEERING GMBH

- HAAG-STREIT GROUP

- CANON MEDICAL SYSTEMS CORPORATION

- ESSILORLUXOTTICA

- OCULUS

- VISIONIX

- SONOMED ESCALON

- COBURN TECHNOLOGIES, INC.

- DGH TECHNOLOGY, INC.

- SHANGHAI MEDIWORKS PRECISION INSTRUMENTS CO., LTD.

- 기타 기업

- VISUNEX MEDICAL SYSTEMS

- FORUS HEALTH PVT. LTD.

- ZIEMER OPHTHALMIC SYSTEMS AG

- EYENUK INC.

- COSTRUZIONE STRUMENTI OFTALMICI(CSO)

- HAI LABORATORIES, INC.

- CRYSTALVUE MEDICAL CORPORATION

- SUZHOU KANGJIE MEDICAL INC.

- KONAN MEDICAL USA, INC.

- REMIDIO INNOVATIVE SOLUTIONS PVT. LTD.

제13장 부록

HBR 25.09.22The ophthalmic imaging market is projected to reach USD 3.84 billion by 2030 from USD 2.83 billion in 2025, at a CAGR of 6.3% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Product, Application, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa, and GCC Countries |

The ophthalmic imaging market is driven by the growing prevalence of eye diseases such as glaucoma, diabetic retinopathy, and age-related macular degeneration, particularly among the aging global population. Increasing demand for early and accurate diagnosis, advancements in imaging technologies like OCT and fundus cameras, and rising awareness of preventive eye care are boosting market growth. Additionally, favorable government initiatives and rising healthcare expenditure support market expansion. However, high equipment costs, limited reimbursement in certain regions, and a shortage of skilled professionals restrain widespread adoption, especially in low-income and rural settings. Data management and integration challenges in clinical workflows further limit efficiency in some healthcare facilities. Opportunities lie in the development of portable, AI-integrated imaging devices and the expansion of teleophthalmology services to reach underserved populations.

Based on product, the OCT systems segment is expected to have the highest growth rate during the forecast year. Optical coherence tomography (OCT) systems are expected to grow at the highest CAGR during the forecast period because they offer non-invasive, ultra-high-resolution imaging essential for early diagnosis of retinal and optic nerve diseases. Technological advances-such as swept-source OCT, OCT-angiography, and AI-driven analytics-enhance diagnostic capability and workflow efficiency. Compact, handheld OCT devices are expanding access in primary care and rural settings. The growing global prevalence of diabetes, glaucoma, and AMD, combined with rising healthcare investments and favorable reimbursements, further drives OCT adoption and rapid market expansion.

Based on end user, the optometry clinics segment is expected to have the highest growth rate during the forecast year due to increasing consumer awareness of eye health and routine vision screenings. They serve as primary care hubs, offering accessible and affordable eye examinations. The rising adoption of portable, high-resolution diagnostic devices such as OCT, fundus cameras, and visual field analyzers in clinics further accelerates this trend. Clinics are increasingly investing in AI-enabled, compact equipment to enhance workflow efficiency and deliver rapid diagnostics. Additionally, growth in tele-optometry and remote screening models supports scalable reach, particularly in underserved regions, driving sustained clinic-based expansion.

Asia Pacific is expected to have the highest growth rate during the forecast period due to a rapidly aging population, rising prevalence of eye disorders like glaucoma, cataracts, and diabetic retinopathy, and increasing investment in healthcare infrastructure across key countries like China and India. Governments are expanding access via teleophthalmology networks and mobile clinics, while local innovation and affordable device production enhance adoption in underserved areas. Technological adoption, particularly OCT, AI tools, and multimodal platforms, is accelerating region-wide growth.

A breakdown of the primary participants (supply-side) for the ophthalmic imaging market referred to in this report is provided below:

- By Company Type: Tier 1:34%, Tier 2: 38%, and Tier 3: 28%

- By Designation: C-level: 26%, Director Level: 35%, and Others: 39%

- By Region: North America: 17%, Europe: 39%, Asia Pacific: 28%, Latin America: 8%, Middle East & Africa: 3%, GCC Countries: 5%

Prominent players in the ophthalmic imaging market are Carl Zeiss Meditec AG (Germany), Topcon Corporation (Japan), Nidek Co. Ltd. (Japan), Alcon Inc. (Switzerland), Optopol Technology Sp. z o.o (Poland), Essilor International S.A. (France), Bausch & Lomb Incorporated (US), and Halma Plc (UK), among others.

Research Coverage

The report evaluates the ophthalmic imaging market and estimates its size and future growth potential based on various segments, including products, applications, end users, and regions. The report also includes a competitive analysis of the major players in this market, along with company profiles, product offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report will assist the market leader/new entrants in the market with data on the nearest approximations of the revenue numbers for the overall ophthalmic imaging market and the subsegments. The report will assist stakeholders in understanding the competitive landscape and gain further insights into better placing their businesses and making appropriate go-to-market strategies. The report assists the stakeholders in understanding the market pulse and gives them data on influential drivers, hindrances, obstacles, and opportunities in the market.

This report provides insights into the following points:

- Analysis of key drivers (Rising number of preterm and low-weight births, Public-private initiatives to strengthen patient care, Increasing incidence of HAIs among newborns, Changing clinical risks for congenital and obstetric complications, Rising number of neonatal care facilities worldwide), restraints (Premium pricing of advanced neonatal care equipment, Growing preference for refurbished devices across emerging countries), opportunities (Development of integrated and multifunctional neonatal care equipment, Market opportunities in emerging markets) and challenges (Limited access in low-income regions, Regulatory and compliance complexities)

- Product Enhancement/Innovation: Comprehensive details about product launches and anticipated trends in the global ophthalmic imaging market

- Market Development: Thorough knowledge and analysis of the profitable rising markets by product, application, end user, and region

- Market Diversification: Comprehensive information about newly launched products and services, expanding markets, current advancements, and investments in the global ophthalmic imaging market

- Competitive Assessment: Thorough evaluation of the market shares, growth plans, offerings, and capacities of the major competitors in the global ophthalmic imaging market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 OPHTHALMIC IMAGING MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key sources of secondary data

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key sources of primary data

- 2.1.2.2 Key objectives of primary research

- 2.1.2.3 Key data from primary sources

- 2.1.2.4 Key industry insights

- 2.1.2.5 Breakdown of primary interviews

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 SUPPLY-SIDE ANALYSIS (REVENUE SHARE ANALYSIS)

- 2.2.1.1 Company presentations and primary interviews

- 2.2.1.2 Demand-side analysis

- 2.2.1.3 Top-down approach

- 2.2.1 SUPPLY-SIDE ANALYSIS (REVENUE SHARE ANALYSIS)

- 2.3 DATA TRIANGULATION

- 2.4 MARKET SHARE ESTIMATION

- 2.5 STUDY ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

- 2.7 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 OPHTHALMIC IMAGING MARKET OVERVIEW

- 4.2 ASIA PACIFIC: OPHTHALMIC IMAGING MARKET, BY TECHNOLOGY AND COUNTRY (2024)

- 4.3 OPHTHALMIC IMAGING MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 4.4 OPHTHALMIC IMAGING MARKET, REGIONAL MIX, 2023-2030

- 4.5 OPHTHALMIC IMAGING MARKET: EMERGING VS. DEVELOPED MARKETS

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Growing prevalence of chronic eye diseases among geriatric patients

- 5.2.1.2 Technological advancements in imaging modalities

- 5.2.1.3 Favorable government initiatives and better reimbursement support

- 5.2.2 RESTRAINTS

- 5.2.2.1 High capital cost of ophthalmic imaging equipment

- 5.2.2.2 High maintenance costs and increased downtime of high-end systems

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 High growth opportunities in emerging economies

- 5.2.3.2 Focus on AI-enabled screening and workflow optimization

- 5.2.4 CHALLENGES

- 5.2.4.1 Shortage of skilled ophthalmic technicians and clinicians

- 5.2.4.2 Data privacy and AI regulation challenges

- 5.2.1 DRIVERS

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE OF OPHTHALMIC IMAGING PRODUCTS, BY TYPE, 2024

- 5.4.2 AVERAGE SELLING PRICE TREND OF OPTICAL COHERENCE TOMOGRAPHY SYSTEMS, BY REGION, 2022-2024

- 5.5 VALUE CHAIN ANALYSIS

- 5.6 SUPPLY CHAIN ANALYSIS

- 5.7 ECOSYSTEM ANALYSIS

- 5.7.1 ROLE IN ECOSYSTEM

- 5.8 INVESTMENT & FUNDING SCENARIO

- 5.9 TECHNOLOGY ANALYSIS

- 5.9.1 KEY TECHNOLOGIES

- 5.9.1.1 Fluorescein angiography

- 5.9.1.2 Ultrasound B-scan imaging

- 5.9.2 COMPLEMENTARY TECHNOLOGIES

- 5.9.2.1 Artificial intelligence and deep learning

- 5.9.3 ADJACENT TECHNOLOGIES

- 5.9.3.1 Smartphone-based retinal imaging

- 5.9.3.2 Gene therapy & retinal implants

- 5.9.1 KEY TECHNOLOGIES

- 5.10 INDUSTRY TRENDS

- 5.10.1 RAPID SHIFT TOWARD MULTIMODAL AND AI-INTEGRATED IMAGING SYSTEMS

- 5.10.2 INCREASED PENETRATION OF PORTABLE AND HANDHELD IMAGING SOLUTIONS

- 5.10.3 PREMIUM IMAGING GROWTH TO GET HIGH CAPITAL INVESTMENTS IN HOSPITALS AND TERTIARY CARE CENTERS

- 5.10.4 OEM CONSOLIDATION AND SOFTWARE-DRIVEN ECOSYSTEMS TO RESHAPE COMPETITIVE LANDSCAPE

- 5.11 PATENT ANALYSIS

- 5.12 TRADE ANALYSIS

- 5.12.1 IMPORT DATA FOR HS CODE 901850, 2020-2024

- 5.12.2 EXPORT DATA FOR HS CODE 901850, 2020-2024

- 5.13 KEY CONFERENCES & EVENTS, 2025-2026

- 5.14 CASE STUDY ANALYSIS

- 5.14.1 ZEISS TO ENHANCE CIRRUS HD-OCT PLATFORM BY INTEGRATING AI-BASED TOOLS FOR DETECTING GLAUCOMA AND RETINAL DISEASES

- 5.14.2 INDIA'S NATIONAL PROGRAM FOR CONTROL OF BLINDNESS (NPCB) TO COLLABORATE WITH FORUS HEALTH FOR REDUCING AVOIDABLE BLINDNESS

- 5.14.3 UK NATIONAL HEALTH SERVICE TO DEPLOY HEIDELBERG ENGINEERING'S SPECTRALIS OCT PLATFORM FOR IMPROVING EARLY DETECTION OF CHRONIC DISEASES

- 5.15 REGULATORY ANALYSIS

- 5.15.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.15.2 REGULATORY FRAMEWORK

- 5.15.2.1 North America

- 5.15.2.1.1 US

- 5.15.2.1.2 Canada

- 5.15.2.2 Europe

- 5.15.2.2.1 Germany

- 5.15.2.2.2 France

- 5.15.2.2.3 UK

- 5.15.2.3 Asia Pacific

- 5.15.2.3.1 China

- 5.15.2.3.2 Japan

- 5.15.2.3.3 India

- 5.15.2.4 Latin America

- 5.15.2.4.1 Brazil

- 5.15.2.4.2 Mexico

- 5.15.2.5 Middle East & Africa

- 5.15.2.5.1 Saudi Arabia

- 5.15.2.5.2 UAE

- 5.15.2.5.3 South Africa

- 5.15.2.5.4 Nigeria

- 5.15.2.1 North America

- 5.16 PORTER'S FIVE FORCES ANALYSIS

- 5.16.1 BARGAINING POWER OF SUPPLIERS

- 5.16.2 BARGAINING POWER OF BUYERS

- 5.16.3 THREAT OF NEW ENTRANTS

- 5.16.4 THREAT OF SUBSTITUTES

- 5.16.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.17 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.17.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.17.2 KEY BUYING CRITERIA

- 5.18 UNMET NEEDS/END-USER EXPECTATIONS

- 5.19 IMPACT OF 2025 US TARIFF ON OPHTHALMIC IMAGING MARKET

- 5.19.1 KEY TARIFF RATES

- 5.19.2 PRICE IMPACT ANALYSIS

- 5.19.3 KEY IMPACT ON COUNTRY/REGION

- 5.19.3.1 North America

- 5.19.3.1.1 US

- 5.19.3.2 Europe

- 5.19.3.3 Asia Pacific

- 5.19.3.1 North America

- 5.19.4 IMPACT ON END-USE INDUSTRIES

- 5.20 IMPACT OF AI/ GEN AI ON OPHTHALMIC IMAGING MARKET

- 5.21 ADJACENT MARKET ANALYSIS

6 OPHTHALMIC IMAGING MARKET, BY TECHNOLOGY

- 6.1 INTRODUCTION

- 6.2 AI-ENABLED EQUIPMENT

- 6.2.1 RISING DEMAND FOR EARLY DIAGNOSIS, EFFICIENCY, AND STANDARDIZATION TO DRIVE MARKET

- 6.3 NON-AI-ENABLED EQUIPMENT

- 6.3.1 ESTABLISHED CLINICAL UTILITY AND COST-EFFECTIVENESS TO SUSTAIN DOMINANCE

7 OPHTHALMIC IMAGING MARKET, BY PRODUCT

- 7.1 INTRODUCTION

- 7.2 OPTICAL COHERENCE TOMOGRAPHY SYSTEMS

- 7.2.1 SPECTRAL-DOMAIN OCT (SD-OCT)

- 7.2.1.1 Growing demand for high-resolution retinal imaging to accelerate market adoption

- 7.2.2 SWEPT-SOURCE OCT (SS-OCT)

- 7.2.2.1 Rising preference for deep tissue imaging and faster scanning to fuel market growth

- 7.2.3 HANDHELD OCT

- 7.2.3.1 Surging demand for portability and pediatric imaging to propel market growth

- 7.2.1 SPECTRAL-DOMAIN OCT (SD-OCT)

- 7.3 OPHTHALMIC ULTRASOUND SYSTEMS

- 7.3.1 OPHTHALMIC A-SCAN ULTRASOUND SYSTEMS

- 7.3.1.1 Rising prevalence of cataracts and increasing intraocular lens (IOL) implantation procedures to aid market growth

- 7.3.2 OPHTHALMIC B-SCAN ULTRASOUND SYSTEMS

- 7.3.2.1 Rising incidence of retinal disorders and opaque media cases to augment segment growth

- 7.3.3 OPHTHALMIC ULTRASOUND BIOMICROSCOPES

- 7.3.3.1 Demand for high-resolution anterior segment imaging to fuel market growth

- 7.3.4 OPHTHALMIC PACHYMETERS

- 7.3.4.1 Growing incidence of glaucoma and increasing demand for refractive surgery to support segment growth

- 7.3.5 OTHER OPHTHALMIC ULTRASOUND SYSTEMS

- 7.3.1 OPHTHALMIC A-SCAN ULTRASOUND SYSTEMS

- 7.4 FUNDUS CAMERAS

- 7.4.1 MYDRIATIC FUNDUS CAMERAS

- 7.4.1.1 Advancements in retinal disease diagnosis and imaging precision to boost market growth

- 7.4.2 NON-MYDRIATIC FUNDUS CAMERAS

- 7.4.2.1 Rising diabetic retinopathy screening and growing focus on primary eye care to augment market growth

- 7.4.3 HYBRID FUNDUS CAMERAS

- 7.4.3.1 Demand for versatile retinal imaging and workflow efficiency to fuel market adoption

- 7.4.4 ROP FUNDUS CAMERAS

- 7.4.4.1 Urgent need for early detection of retinal disorders in newborns to propel segment growth

- 7.4.1 MYDRIATIC FUNDUS CAMERAS

- 7.5 SLIT LAMPS

- 7.5.1 HANDHELD SLIT LAMPS

- 7.5.1.1 Portability, tele-ophthalmology, and field screening to fuel market demand

- 7.5.2 TABLE MOUNT SLIT LAMPS

- 7.5.2.1 Focus on precision diagnostics and need for better image clarity to augment market growth

- 7.5.1 HANDHELD SLIT LAMPS

- 7.6 SPECULAR MICROSCOPES

- 7.6.1 RISING NUMBER OF CORNEAL TRANSPLANTS AND CATARACT SURGERIES TO ACCELERATE MARKET DEMAND

- 7.7 TONOMETERS

- 7.7.1 APPLANATION TONOMETERS

- 7.7.1.1 Widespread clinical acceptance and diagnostic accuracy to aid market growth

- 7.7.2 REBOUND TONOMETERS

- 7.7.2.1 Adoption of rebound tonometers to gain preference for better portability and greater patient comfort

- 7.7.1 APPLANATION TONOMETERS

- 7.8 OPHTHALMOSCOPES

- 7.8.1 DIRECT OPHTHALMOSCOPES

- 7.8.1.1 Technological upgrades to sustain global demand for direct ophthalmoscopes

- 7.8.2 INDIRECT OPHTHALMOSCOPES

- 7.8.2.1 Growing demand in retinal care to increase product demand

- 7.8.1 DIRECT OPHTHALMOSCOPES

- 7.9 RETINOSCOPES

- 7.9.1 RISING DEMAND AMONG PEDIATRIC, NON-VERBAL, AND UNCOOPERATIVE PATIENTS TO SUSTAIN DEMAND

- 7.10 OTHER OPHTHALMIC IMAGING PRODUCTS

8 OPHTHALMIC IMAGING MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- 8.2 GLAUCOMA

- 8.2.1 NEED FOR EARLY DETECTION AND LONG-TERM MONITORING TO FUEL ADOPTION OF ADVANCED IMAGING MODALITIES

- 8.3 CATARACTS

- 8.3.1 INCREASING CATARACT SURGERIES AND PREOPERATIVE IMAGING TO SPUR DEMAND FOR DIAGNOSTIC OPHTHALMIC SYSTEMS

- 8.4 RETINOPATHIES

- 8.4.1 RISING DIABETIC AND HYPERTENSIVE POPULATION TO ACCELERATE DEMAND FOR ADVANCED RETINAL IMAGING SOLUTIONS

- 8.5 REFRACTIVE DISORDERS

- 8.5.1 RISING DEMAND FOR REFRACTIVE SURGERIES TO BOOST UPTAKE OF ADVANCED IMAGING SYSTEMS FOR PREOPERATIVE PLANNING

- 8.6 AGE-RELATED MACULAR DEGENERATION

- 8.6.1 AGING DEMOGRAPHICS AND INCREASED LIFESPAN TO PROPEL PREVALENCE OF AGE-RELATED MACULAR DEGENERATION

- 8.7 OTHER APPLICATIONS

9 OPHTHALMIC IMAGING MARKET, BY END USER

- 9.1 INTRODUCTION

- 9.2 HOSPITALS

- 9.2.1 RISING ADOPTION OF ADVANCED OPHTHALMIC DIAGNOSTICS TO AUGMENT MARKET GROWTH

- 9.3 OPHTHALMOLOGY CLINICS

- 9.3.1 USE OF HIGH-THROUGHPUT, AI-INTEGRATED, AND PORTABLE IMAGING DEVICES TO FUEL MARKET GROWTH

- 9.4 OPTOMETRY CLINICS

- 9.4.1 INCREASING PREVALENCE OF MYOPIA AND LIFESTYLE-RELATED VISION DISORDERS TO AID MARKET GROWTH

- 9.5 OTHER END USERS

10 OPHTHALMIC IMAGING MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 10.2.2 US

- 10.2.2.1 US to dominate North American ophthalmic imaging market during forecast period

- 10.2.3 CANADA

- 10.2.3.1 Rising geriatric population with chronic eye diseases to propel market growth

- 10.3 EUROPE

- 10.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 10.3.2 GERMANY

- 10.3.2.1 Strong clinical infrastructure and favorable healthcare policies to boost market growth

- 10.3.3 FRANCE

- 10.3.3.1 Government-funded eye screening programs and widespread insurance coverage to accelerate market growth

- 10.3.4 UK

- 10.3.4.1 Popularity on national screening programs and focus on NHS-backed digital adoption to stabilize market growth

- 10.3.5 ITALY

- 10.3.5.1 High geriatric population and expansion of regional eye care programs to boost demand for ophthalmic imaging

- 10.3.6 SPAIN

- 10.3.6.1 Increased public investment in health screening programs to aid market growth

- 10.3.7 REST OF EUROPE

- 10.4 ASIA PACIFIC

- 10.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 10.4.2 JAPAN

- 10.4.2.1 Strong focus on preventive and advanced eye care infrastructure to augment market growth

- 10.4.3 CHINA

- 10.4.3.1 Popularity of large-scale eye screening programs and focus on advanced ophthalmic imaging infrastructure to drive market

- 10.4.4 INDIA

- 10.4.4.1 Rising diabetic population and increasing popularity of nationwide eye health programs to propel market growth

- 10.4.5 SOUTH KOREA

- 10.4.5.1 High-tech healthcare adoption and aging demographics to accelerate smart ophthalmic imaging integration

- 10.4.6 AUSTRALIA

- 10.4.6.1 Government-backed eye care programs and expanding teleophthalmology to propel market growth

- 10.4.7 REST OF ASIA PACIFIC

- 10.5 LATIN AMERICA

- 10.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 10.5.2 BRAZIL

- 10.5.2.1 Focus on public tele-ophthalmology initiatives and diagnostics to boost market growth

- 10.5.3 MEXICO

- 10.5.3.1 Increasing prevalence of diabetic eye disease and growing focus on digital health expansion to drive market

- 10.5.4 REST OF LATIN AMERICA

- 10.6 MIDDLE EAST & AFRICA

- 10.6.1 INCREASED HEALTHCARE MODERNIZATION AND FOCUS ON PUBLIC HEALTH INVESTMENTS TO AID MARKET GROWTH

- 10.6.2 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 10.7 GCC COUNTRIES

- 10.7.1 GOVERNMENT-LED HEALTHCARE DIGITALIZATION AND INCREASED DIABETES-LINKED VISION DISORDERS TO DRIVE MARKET

- 10.7.2 MACROECONOMIC OUTLOOK FOR GCC COUNTRIES

11 COMPETITIVE LANDSCAPE

- 11.1 INTRODUCTION

- 11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 11.2.1 KEY STRATEGIES ADOPTED BY MAJOR PLAYERS IN OPHTHALMIC IMAGING MARKET

- 11.3 REVENUE ANALYSIS, 2020-2024

- 11.4 MARKET SHARE ANALYSIS, 2024

- 11.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 11.5.1 STARS

- 11.5.2 EMERGING LEADERS

- 11.5.3 PERVASIVE PLAYERS

- 11.5.4 PARTICIPANTS

- 11.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 11.5.5.1 Company footprint

- 11.5.5.2 Region footprint

- 11.5.5.3 Product footprint

- 11.5.5.4 Application footprint

- 11.5.5.5 End-user footprint

- 11.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 11.6.1 PROGRESSIVE COMPANIES

- 11.6.2 RESPONSIVE COMPANIES

- 11.6.3 DYNAMIC COMPANIES

- 11.6.4 STARTING BLOCKS

- 11.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 11.6.5.1 Detailed list of key startups/SMEs

- 11.6.5.2 Competitive benchmarking of startups/SMEs

- 11.7 COMPANY VALUATION & FINANCIAL METRICS

- 11.7.1 FINANCIAL METRICS

- 11.7.2 COMPANY VALUATION

- 11.8 BRAND/PRODUCT COMPARISON

- 11.9 COMPETITIVE SCENARIO

- 11.9.1 PRODUCT LAUNCHES

- 11.9.2 DEALS

- 11.9.3 OTHER DEVELOPMENTS

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 CARL ZEISS MEDITEC AG

- 12.1.1.1 Business overview

- 12.1.1.2 Products offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Product launches & upgrades

- 12.1.1.3.2 Deals

- 12.1.1.4 MnM view

- 12.1.1.4.1 Right to win

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses & competitive threats

- 12.1.2 TOPCON CORPORATION

- 12.1.2.1 Business overview

- 12.1.2.2 Products offered

- 12.1.2.3 Recent developments

- 12.1.2.3.1 Deals

- 12.1.2.3.2 Other developments

- 12.1.2.4 MnM view

- 12.1.2.4.1 Right to win

- 12.1.2.4.2 Strategic choices

- 12.1.2.4.3 Weaknesses & competitive threats

- 12.1.3 NIDEK CO., LTD.

- 12.1.3.1 Business overview

- 12.1.3.2 Products offered

- 12.1.3.3 MnM view

- 12.1.3.3.1 Right to win

- 12.1.3.3.2 Strategic choices

- 12.1.3.3.3 Weaknesses & competitive threats

- 12.1.4 HALMA PLC

- 12.1.4.1 Business overview

- 12.1.4.2 Products offered

- 12.1.4.3 MnM view

- 12.1.4.3.1 Right to win

- 12.1.4.3.2 Strategic choices

- 12.1.4.3.3 Weaknesses & competitive threats

- 12.1.5 ALCON

- 12.1.5.1 Business overview

- 12.1.5.2 Products offered

- 12.1.5.3 MnM view

- 12.1.5.3.1 Right to win

- 12.1.5.3.2 Strategic choices

- 12.1.5.3.3 Weaknesses & competitive threats

- 12.1.6 HEIDELBERG ENGINEERING GMBH

- 12.1.6.1 Business overview

- 12.1.6.2 Products offered

- 12.1.7 HAAG-STREIT GROUP

- 12.1.7.1 Business overview

- 12.1.7.2 Products offered

- 12.1.8 CANON MEDICAL SYSTEMS CORPORATION

- 12.1.8.1 Business overview

- 12.1.8.2 Products offered

- 12.1.9 ESSILORLUXOTTICA

- 12.1.9.1 Business overview

- 12.1.9.2 Products offered

- 12.1.10 OCULUS

- 12.1.10.1 Business overview

- 12.1.10.2 Products offered

- 12.1.10.3 Recent developments

- 12.1.10.3.1 Product launches

- 12.1.11 VISIONIX

- 12.1.11.1 Business overview

- 12.1.11.2 Products offered

- 12.1.11.3 Recent developments

- 12.1.11.3.1 Deals

- 12.1.12 SONOMED ESCALON

- 12.1.12.1 Business overview

- 12.1.12.2 Products offered

- 12.1.13 COBURN TECHNOLOGIES, INC.

- 12.1.13.1 Business overview

- 12.1.13.2 Products offered

- 12.1.13.3 Recent developments

- 12.1.13.3.1 Product launches

- 12.1.14 DGH TECHNOLOGY, INC.

- 12.1.14.1 Business overview

- 12.1.14.2 Products offered

- 12.1.15 SHANGHAI MEDIWORKS PRECISION INSTRUMENTS CO., LTD.

- 12.1.15.1 Business overview

- 12.1.15.2 Products offered

- 12.1.1 CARL ZEISS MEDITEC AG

- 12.2 OTHER PLAYERS

- 12.2.1 VISUNEX MEDICAL SYSTEMS

- 12.2.2 FORUS HEALTH PVT. LTD.

- 12.2.3 ZIEMER OPHTHALMIC SYSTEMS AG

- 12.2.4 EYENUK INC.

- 12.2.5 COSTRUZIONE STRUMENTI OFTALMICI (CSO)

- 12.2.6 HAI LABORATORIES, INC.

- 12.2.7 CRYSTALVUE MEDICAL CORPORATION

- 12.2.8 SUZHOU KANGJIE MEDICAL INC.

- 12.2.9 KONAN MEDICAL USA, INC.

- 12.2.10 REMIDIO INNOVATIVE SOLUTIONS PVT. LTD.

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS