|

시장보고서

상품코드

1811729

산소 농축기 시장 : 유형별, 기술별, 유량별, 용도별, 최종 사용자별, 지역별 예측(-2030년)Oxygen Concentrators Market by Type, Technology, Flowrate, Application, End User - Global Forecast to 2030 |

||||||

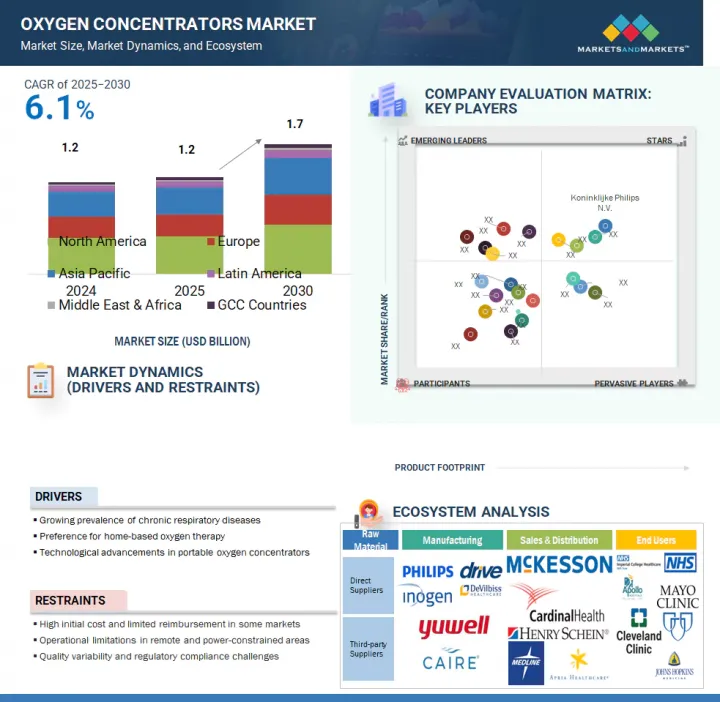

산소 농축기 시장 규모는 예측 기간 동안 6.1%의 연평균 성장률(CAGR)로 확대되어 2025년 12억 7,000만 달러에서 2030년에 17억 1,000만 달러에 이를 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2024-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 검토 단위 | 금액(10억 달러) |

| 부문 | 유형별, 기술별, 유량별, 용도별, 최종 사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카, GCC 국가 |

기술적 발전은 산소 농축기 시장의 성장을 촉진하는 데 매우 중요합니다. 최근 장치는 더 작고 가볍고 에너지 효율적이며 사용자 친화적입니다. 펄스 도즈 기술과 같은 혁신은 특히 휴대용 모델에서 산소를 절약하고 배터리 수명을 연장하기 위해 흡입 중에만 산소를 공급합니다. 새로운 장치들은 저소음 작동, 디지털 디스플레이, 경보, 원격 모니터링을 위한 연결성을 특징으로 하며 펄스 및 연속 유량 모드를 모두 뒷받침합니다.

장시간 사용 가능한 배터리를 장착한 휴대용 농축기는 활동적인 사용자 및 여행자들 사이에서 인기가 높으며, 일부는 항공기 탑승이 허용된 FAA 인증을 받았습니다. IoT 통합은 의료 제공자와의 실시간 데이터 공유를 가능하게 하여 환자 순응도를 향상시킵니다. AI 알고리즘은 호흡 패턴에 기반해 산소 공급을 최적화합니다. 이러한 혁신은 편의성과 환자 삶의 질을 개선하고 용도를 확대하여 시장 성장에 기여합니다.

유형별 시장 분류는 휴대용과 고정형 산소 농축기로 나뉩니다. 2024년 기준 휴대용 산소 농축기 부문이 전 세계 시장의 최대 점유율을 기록합니다. 전 세계 고령 인구 증가가 휴대용 산소 농축기(POC) 수요를 촉진하는 핵심 요인입니다. 노년층은 만성 폐쇄성 폐질환(COPD), 폐섬유증, 심부전 관련 저산소증 등 만성 호흡기 질환에 더 취약합니다. 노년기의 이동성 제약으로 인해 POC는 고정형 장치에 얽매이지 않고 산소 치료를 받을 수 있는 실용적인 해결책입니다. 가정 내 이동, 야외 활동, 여행 중에도 산소 지원을 휴대할 수 있습니다.는 점은 그들의 독립성과 삶의 질을 크게 향상시킵니다. 노령 인구가 지속적으로 증가함에 따라, 특히 북미, 유럽, 아시아 일부 지역과 같은 선진 지역에서 POC와 같은 소형, 신뢰성 높고 사용하기 쉬운 산소 장치에 대한 수요가 꾸준히 증가하며 시장 지배력을 강화하고 있습니다.

최종 사용자 기준으로 산소 농축기 시장은 재택 치료, 병원 및 클리닉, 외래 수술 센터 및 의사 사무실로 분류됩니다. 2024년 기준 재택 치료가 산소 농축기 시장에서 가장 큰 점유율을 기록했습니다. 전 세계 고령 인구 증가는 산소 농축기 시장의 재택 치료 부문의 수요를 촉진하는 핵심 요인입니다. 노년층은 만성 폐쇄성 폐질환(COPD), 폐기종, 노화 관련 폐 기능 저하 등 만성 호흡기 질환에 더 취약하다. 이러한 질환은 종종 장기적인 산소 치료를 필요로 하며, 편의성과 비용 절감 효과로 인해 가정에서 관리되는 경우가 점점 늘고 있습니다. 또한 노인 환자들은 이동성 문제로 인해 빈번한 병원 방문이 어려운 경우가 많다. 가정용 산소 농축기는 지속적인 호흡 지원을 유지하면서 독립성을 보장하는 안전하고 접근성 높은 해결책을 제공합니다. 일본, 독일, 이탈리아, 미국 등 고령화 속도가 빠른 국가들은 특히 재택 치료 환경에서 산소 농축기 채택률이 매우 높습니다.

북미는 예측 기간 동안 OC 시장에서 가장 큰 점유율을 기록할 것으로 예상됩니다. 북미, 특히 미국과 캐나다는 최근 진단 및 치료 기술을 갖춘 고도로 발달된 의료 시스템을 보유하고 있습니다. 이 지역의 병원, 클리닉, 외래 진료 센터는 농축기를 포함한 산소 공급 장비를 광범위하게 이용할 수 있습니다. 또한 체계적인 의료 정책, 통합된 보험 네트워크, 간소화된 조달 채널을 통해 이러한 기기의 원활한 공급과 유통이 보장됩니다. 환자들은 더 빠른 진단과 즉각적인 산소 요법 시작의 혜택을 받습니다. 재택 치료 지원 시스템 또한 고급으로 발전되어 지속적인 산소 지원 하에 병원에서 가정으로의 안전한 전환이 가능합니다. 이러한 유리한 조건은 특히 만성 환자를 대상으로 산소 농축기의 접근성과 사용률을 높이며, 전 세계 산소 농축기 시장에서 북미의 선도적 위치를 공고히 합니다.

본 보고서에서는 세계의 산소 농축기 시장에 대해 조사했으며, 유형별, 기술별, 유량별, 용도별, 최종 사용자별, 지역별 동향 및 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

- 소개

- 시장 역학

- 고객의 비즈니스에 영향을 미치는 동향 및 혼란

- 가격 분석

- 밸류체인 분석

- 공급망 분석

- 생태계 분석

- 투자 및 자금조달 시나리오

- 기술 분석

- 업계 동향

- 특허 분석

- 무역 분석

- 주된 회의 및 이벤트(2025-2026년)

- 사례 연구 분석

- 규제 분석

- 규제기관, 정부기관, 기타 조직

- Porter's Five Forces 분석

- 주요 이해관계자와 구매 기준

- 미충족 요구, 최종 사용자 기대

- 미국 관세가 산소 농축기 시장에 미치는 영향(2025년)

- 산소 농축기 시장에 있어서의 인공지능(AI)의 영향

- 인접 시장 분석

제6장 산소 농축기 시장(유형별)

- 소개

- 휴대용 산소 농축기

- 고정형 산소 농축기

제7장 산소 농축기 시장(기술별)

- 소개

- 연속

- 펄스

제8장 산소 농축기 시장(유량별)

- 소개

- 0-5L/분

- 5-10L/분

- 10L/분 이상

제9장 산소 농축기 시장(용도별)

- 소개

- COPD

- 천식

- 호흡곤란

- 기타

제10장 산소 농축기 시장(최종사용자별)

- 소개

- 재택 치료

- 병원 및 클리닉

- 외래수술 센터(ASC) 및 의사 사무실

제11장 산소 농축기 시장(지역별)

- 소개

- 북미

- 북미의 거시경제 전망

- 미국

- 캐나다

- 유럽

- 유럽의 거시 경제 전망

- 독일

- 프랑스

- 영국

- 이탈리아

- 스페인

- 기타

- 아시아태평양

- 아시아태평양의 거시 경제 전망

- 일본

- 중국

- 인도

- 한국

- 호주

- 기타

- 라틴아메리카

- 라틴아메리카의 거시 경제 전망

- 브라질

- 멕시코

- 기타

- 중동 및 아프리카

- 중동 및 아프리카의 거시경제 전망

- GCC 국가

- GCC 국가의 거시 경제 전망

제12장 경쟁 구도

- 개요

- 주요 진입기업의 전략 및 강점

- 수익 분석

- 시장 점유율 분석

- 기업평가 매트릭스 : 주요 진입기업(2024년)

- 기업평가 매트릭스 : 스타트업, 중소기업(2024년)

- 기업평가와 재무지표

- 브랜드, 제품 비교

- 경쟁 시나리오

제13장 기업 프로파일

- 주요 진출기업

- KONINKLIJKE PHILIPS NV

- INOGEN, INC.

- JIANGSU YUYUE MEDICAL EQUIPMENT & SUPPLY CO., LTD.

- CAIRE INC.

- DRIVE DEVILBISS HEALTHCARE

- TEIJIN LIMITED

- DAIKIN INDUSTRIES, LTD.

- ESAB CORPORATION(GCE GROUP)

- REACT HEALTH

- PRECISION MEDICAL, INC.

- NIDEK MEDICAL PRODUCTS, INC.

- O2 CONCEPTS, LLC

- BPL MEDICAL TECHNOLOGIES

- BESCO

- OXUS

- 기타 기업

- FOSHAN KEYHUB ELECTRONIC INDUSTRIES CO., LTD

- LONGFIAN SCITECH CO., LTD.

- SHENYANG CANTA MEDICAL TECH. CO., LTD.

- BELLUSCURA

- HOYO SCITECH CO., LTD.

- HACENOR SOLUTIONS

- XNUO INTERNATIONAL GROUP(USA) HOLDINGS

- OXYMED

- KALSTEIN

- ESS PEE ENTERPRISES

제14장 부록

HBR 25.09.22The oxygen concentrators market is projected to reach USD 1.71 billion by 2030 from USD 1.27 billion in 2025, at a CAGR of 6.1% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Type, Technology, Flowrate, Application, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa, and GCC Countries |

Technological advancements are crucial in driving growth in the oxygen concentrators market. Modern units are more compact, lightweight, energy-efficient, and user-friendly. Innovations like pulse dose technology deliver oxygen only during inhalation to conserve it and extend battery life, especially in portable models. New devices feature silent operation, digital displays, alarms, connectivity for remote monitoring, and support both pulse and continuous flow modes.

Portable concentrators with long-lasting batteries are popular among active users and travelers, some FAA-approved for flights. IoT integration enables real-time data sharing with healthcare providers, enhancing patient compliance. AI algorithms optimize oxygen delivery based on respiratory patterns. These innovations improve convenience, patient quality of life, and broaden application scope, fueling market growth as adoption increases.

Based on type, the market is divided into portable and stationary oxygen concentrators. In 2024, the portable oxygen concentrator segment holds the largest share of the global oxygen concentrator market. The increasing global geriatric population is a key factor driving demand for portable oxygen concentrators (POCs). Older adults are more vulnerable to chronic respiratory conditions such as COPD, pulmonary fibrosis, and hypoxia related to heart failure. Mobility challenges in old age make POCs a practical solution, allowing elderly patients to receive oxygen therapy without being restricted to a stationary device. Being able to carry oxygen support while moving around at home, outdoors, or during travel greatly improves their independence and quality of life. As the aging population continues to grow-especially in developed areas like North America, Europe, and parts of Asia-the demand for compact, dependable, and easy-to-use oxygen devices like POCs steadily increases, strengthening their market dominance.

Based on end users, the OC market has been categorized into home care settings, hospitals and clinics, and ambulatory surgical centers & physician offices. In 2024, home care settings held the largest share in the OC market. The increasing global elderly population is a key factor driving demand in the home care segment of the oxygen concentrators market. Older adults are more vulnerable to chronic respiratory conditions such as chronic obstructive pulmonary disease (COPD), emphysema, and age-related decline in lung function. These conditions often require long-term oxygen therapy, which is increasingly managed at home due to its convenience and lower cost. Additionally, elderly patients often face mobility issues, making frequent hospital visits difficult. Home-based oxygen concentrators provide a safe and accessible solution, allowing independence while maintaining continuous respiratory support. Countries like Japan, Germany, Italy, and the US-with rapidly aging populations-are seeing a particularly high adoption of oxygen concentrators in home care settings.

North America is expected to hold the largest share of the OC market during the forecast period. North America, especially the US and Canada, has highly developed healthcare systems equipped with modern diagnostic and therapeutic technologies. The region's hospitals, clinics, and outpatient centers have widespread access to oxygen delivery equipment, including concentrators. Additionally, structured healthcare policies, integrated insurance networks, and streamlined procurement channels ensure the smooth availability and distribution of these devices. Patients benefit from faster diagnoses and prompt initiation of oxygen therapy. Home care support systems are also advanced, allowing a safe transition from hospital to home with continuous oxygen support. These favorable conditions improve the accessibility and use of oxygen concentrators, especially for chronic patients, and reinforce North America's leadership position in the global oxygen concentrators market.

A breakdown of the primary participants (supply-side) for the oxygen concentrators market referred to in this report is provided below:

- By Company Type: Tier 1:34%, Tier 2: 38%, and Tier 3: 28%

- By Designation: C-level: 26%, Director Level: 35%, and Others: 39%

- By Region: North America: 17%, Europe: 39%, Asia Pacific: 28%, Latin America: 8%, Middle East & Africa: 3%, GCC Countries: 5%

Major players in the oxygen concentrators market include Koninklijke Philips N.V. (Netherlands), Inogen, Inc. (US), Jiangsu Yuyue Medical Equipment & Supply Co., Ltd. (China), Caire, Inc. (US), and Drive DeVilbiss Healthcare (US).

Research Coverage

The report assesses the oxygen concentrators market and estimates its size and future growth potential across various segments, including type, technology, flow rate, application, end user, and region. It also provides a competitive analysis of the leading companies in the market, along with their profiles, product offerings, recent developments, and key strategies.

Reasons to Buy the Report

The report will help market leaders and new entrants by providing data on the closest estimates of revenue for the overall oxygen concentrators market and its subsegments. It will aid stakeholders in understanding the competitive landscape and gaining insights to better position their businesses and develop effective go-to-market strategies. Additionally, the report helps stakeholders grasp market trends and offers data on key drivers, obstacles, challenges, and opportunities within the market.

This report provides insights into the following points:

- Analysis of key drivers (rising prevalence of respiratory diseases, growing geriatric population, increasing demand for home healthcare, government initiatives and reimbursement support, technological advancements), restraints (high cost of advanced oxygen concentrators, product recalls or malfunctions), opportunities (integration of digital health features, development of solar-powered or battery-efficient models) and challenges (lack of awareness and diagnosis, competition from low-cost alternatives)

- Product Enhancement/Innovation: Comprehensive details about product launches and anticipated trends in the global OC market

- Market Development: Thorough knowledge and analysis of the profitable rising markets by type, technology, flowrate, application, end user, and region

- Market Diversification: Comprehensive information about newly launched products and services, expanding markets, current advancements, and investments in the global OC market

- Competitive Assessment: Thorough evaluation of the market shares, growth plans, offerings, and capacities of the major competitors in the global OC market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 SEGMENTS COVERED

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY USED

- 1.6 STAKEHOLDERS

- 1.7 LIMITATIONS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key industry insights

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.3 DATA TRIANGULATION

- 2.4 MARKET SHARE ESTIMATION

- 2.5 STUDY ASSUMPTIONS

- 2.6 METHODOLOGY-RELATED LIMITATIONS

- 2.7 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 OXYGEN CONCENTRATORS MARKET OVERVIEW

- 4.2 ASIA PACIFIC: OXYGEN CONCENTRATORS MARKET, BY TECHNOLOGY AND COUNTRY

- 4.3 OXYGEN CONCENTRATORS MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 4.4 OXYGEN CONCENTRATORS MARKET, REGIONAL MIX

- 4.5 OXYGEN CONCENTRATORS MARKET: EMERGING VS. DEVELOPED MARKETS

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Growing prevalence of chronic respiratory diseases

- 5.2.1.2 Preference for home-based oxygen therapy

- 5.2.1.3 Technological advancements in portable oxygen concentrators

- 5.2.2 RESTRAINTS

- 5.2.2.1 High initial cost and limited reimbursement in some markets

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Expansion in emerging markets

- 5.2.3.2 Integration with remote monitoring and telehealth

- 5.2.3.3 Institutional demand and tender-based opportunities

- 5.2.4 CHALLENGES

- 5.2.4.1 Operational limitations in remote and power-constrained areas

- 5.2.4.2 Quality variability and regulatory compliance challenges

- 5.2.1 DRIVERS

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY TYPE

- 5.4.2 AVERAGE SELLING PRICE TREND OF PORTABLE OXYGEN CONCENTRATORS, BY REGION

- 5.5 VALUE CHAIN ANALYSIS

- 5.6 SUPPLY CHAIN ANALYSIS

- 5.7 ECOSYSTEM ANALYSIS

- 5.8 INVESTMENT & FUNDING SCENARIO

- 5.9 TECHNOLOGY ANALYSIS

- 5.9.1 KEY TECHNOLOGIES

- 5.9.1.1 Pressure swing adsorption (PSA) technology

- 5.9.1.2 Pulse-dose vs. continuous flow delivery

- 5.9.2 COMPLEMENTARY TECHNOLOGIES

- 5.9.2.1 Remote patient monitoring (RPM) integration

- 5.9.2.2 Battery and power management systems

- 5.9.3 ADJACENT TECHNOLOGIES

- 5.9.3.1 PSA oxygen plants

- 5.9.3.2 Oxygen cylinders as backup systems

- 5.9.1 KEY TECHNOLOGIES

- 5.10 INDUSTRY TRENDS

- 5.10.1 RISING DEMAND FOR HOME-BASED OXYGEN THERAPY

- 5.10.2 INTEGRATION WITH TELEHEALTH AND REMOTE MONITORING

- 5.10.3 SHIFT TOWARD PORTABLE AND WEARABLE TECHNOLOGIES

- 5.10.4 CONSOLIDATION AND COMPETITIVE LANDSCAPE EVOLUTION

- 5.11 PATENT ANALYSIS

- 5.12 TRADE ANALYSIS

- 5.12.1 IMPORT DATA (HS CODE 901920)

- 5.12.2 EXPORT DATA (HS CODE 901920)

- 5.13 KEY CONFERENCES & EVENTS, 2025-2026

- 5.14 CASE STUDY ANALYSIS

- 5.14.1 DEPLOYMENT OF PORTABLE OXYGEN CONCENTRATORS IN RURAL INDIA

- 5.14.2 INOGEN'S DIRECT-TO-CONSUMER EXPANSION IN US

- 5.14.3 BELLUSCURA'S STRATEGIC PARTNERSHIP WITH CHINESE OEM

- 5.15 REGULATORY ANALYSIS

- 5.16 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.16.1 REGULATORY LANDSCAPE

- 5.16.1.1 North America

- 5.16.1.1.1 US

- 5.16.1.1.2 Canada

- 5.16.1.2 Europe

- 5.16.1.2.1 Germany

- 5.16.1.2.2 France

- 5.16.1.2.3 UK

- 5.16.1.3 Asia Pacific

- 5.16.1.3.1 China

- 5.16.1.3.2 Japan

- 5.16.1.3.3 India

- 5.16.1.4 Latin America

- 5.16.1.4.1 Brazil

- 5.16.1.4.2 Mexico

- 5.16.1.5 Middle East & Africa

- 5.16.1.5.1 South Africa

- 5.16.1.5.2 GCC Countries

- 5.16.1.1 North America

- 5.16.1 REGULATORY LANDSCAPE

- 5.17 PORTER'S FIVE FORCES ANALYSIS

- 5.17.1 THREAT OF NEW ENTRANTS

- 5.17.2 THREAT OF SUBSTITUTES

- 5.17.3 BARGAINING POWER OF SUPPLIERS

- 5.17.4 BARGAINING POWER OF BUYERS

- 5.17.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.18 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.18.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.18.2 BUYING CRITERIA

- 5.19 UNMET NEEDS/END-USER EXPECTATIONS

- 5.20 IMPACT OF 2025 US TARIFF ON OXYGEN CONCENTRATORS MARKET

- 5.20.1 KEY TARIFF RATES

- 5.20.2 PRICE IMPACT ANALYSIS

- 5.20.3 KEY IMPACT ON COUNTRY/REGION

- 5.20.3.1 US

- 5.20.3.2 Europe

- 5.20.3.3 Asia Pacific

- 5.20.4 IMPACT ON END-USER INDUSTRIES

- 5.21 IMPACT OF ARTIFICIAL INTELLIGENCE ON OXYGEN CONCENTRATORS MARKET

- 5.22 ADJACENT MARKET ANALYSIS

6 OXYGEN CONCENTRATORS MARKET, BY TYPE

- 6.1 INTRODUCTION

- 6.2 PORTABLE OXYGEN CONCENTRATORS

- 6.3 STATIONARY OXYGEN CONCENTRATORS

7 OXYGEN CONCENTRATORS MARKET, BY TECHNOLOGY

- 7.1 INTRODUCTION

- 7.2 CONTINUOUS FLOW

- 7.3 PULSE FLOW

8 OXYGEN CONCENTRATORS MARKET, BY FLOWRATE

- 8.1 INTRODUCTION

- 8.2 0-5 L/MIN FLOWRATE

- 8.3 5-10 L/MIN FLOWRATE

- 8.4 ABOVE 10 L/MIN FLOWRATE

9 OXYGEN CONCENTRATORS MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- 9.2 COPD

- 9.3 ASTHMA

- 9.4 RESPIRATORY DISTRESS

- 9.5 OTHER APPLICATIONS

10 OXYGEN CONCENTRATORS MARKET, BY END USER

- 10.1 INTRODUCTION

- 10.2 HOME CARE SETTINGS

- 10.3 HOSPITALS & CLINICS

- 10.4 AMBULATORY SURGICAL CENTERS & PHYSICIANS' OFFICES

11 OXYGEN CONCENTRATORS MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 11.2.2 US

- 11.2.2.1 Medicare coverage, COPD prevalence, and connected POCs to catalyze sustained market expansion through 2030

- 11.2.3 CANADA

- 11.2.3.1 Provincial funding, COPD burden, and connected POCs to accelerate home oxygen concentrator adoption trajectory

- 11.3 EUROPE

- 11.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 11.3.2 GERMANY

- 11.3.2.1 Strong payer coverage and clinical guidelines to drive predictable replacement cycles in Germany's market

- 11.3.3 FRANCE

- 11.3.3.1 Hospital-to-home shift and connected devices sustain resilient replacement cycles in France's oxygen concentrators market

- 11.3.4 UK

- 11.3.4.1 Aging population and funded home oxygen programs to underpin steady expansion

- 11.3.5 ITALY

- 11.3.5.1 Regional tenders, SSN homecare funding, and COPD burden to support steady growth in Italy's market

- 11.3.6 SPAIN

- 11.3.6.1 Driving home-based healthcare with portable oxygen concentrator growth

- 11.3.7 REST OF EUROPE

- 11.4 ASIA PACIFIC

- 11.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 11.4.2 JAPAN

- 11.4.2.1 Stable funding and service-led home care models to support steady growth

- 11.4.3 CHINA

- 11.4.3.1 Policy momentum and robust manufacturing ecosystem to drive resilient replacement cycles

- 11.4.4 INDIA

- 11.4.4.1 Building resilient healthcare infrastructure with rising oxygen concentrator demand

- 11.4.5 SOUTH KOREA

- 11.4.5.1 Hospital-to-home shift and connected POCs to propel South Korea's portable and stationary oxygen concentrator demand growth

- 11.4.6 AUSTRALIA

- 11.4.6.1 Policy support, service networks, and digital monitoring to drive steady expansion of Australia's market through 2030

- 11.4.7 REST OF ASIA PACIFIC

- 11.5 LATIN AMERICA

- 11.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 11.5.2 BRAZIL

- 11.5.2.1 Public procurement, ANVISA registration, and service networks to drive predictable replacement cycles in Brazil's oxygen therapy landscape

- 11.5.3 MEXICO

- 11.5.3.1 Strengthening respiratory care access through expanding oxygen concentrator adoption

- 11.5.4 REST OF LATIN AMERICA

- 11.6 MIDDLE EAST & AFRICA

- 11.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 11.7 GCC COUNTRIES

- 11.7.1 MACROECONOMIC OUTLOOK FOR GCC COUNTRIES

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 KEY PLAYER STRATEGY/RIGHT TO WIN

- 12.3 REVENUE ANALYSIS

- 12.4 MARKET SHARE ANALYSIS

- 12.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 12.5.1 STARS

- 12.5.2 EMERGING LEADERS

- 12.5.3 PERVASIVE PLAYERS

- 12.5.4 PARTICIPANTS

- 12.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.5.5.1 Company footprint

- 12.5.5.2 Regional footprint

- 12.5.5.3 Type footprint

- 12.5.5.4 Application footprint

- 12.5.5.5 End User footprint

- 12.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 12.6.1 PROGRESSIVE COMPANIES

- 12.6.2 RESPONSIVE COMPANIES

- 12.6.3 DYNAMIC COMPANIES

- 12.6.4 STARTING BLOCKS

- 12.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 12.6.5.1 Detailed list of key startups/SMEs

- 12.6.5.2 Competitive benchmarking of startups/SMEs

- 12.7 COMPANY VALUATION AND FINANCIAL METRICS

- 12.7.1 FINANCIAL METRICS

- 12.7.2 COMPANY VALUATION

- 12.8 BRAND/PRODUCT COMPARISON

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 PRODUCT LAUNCHES

- 12.9.2 DEALS

- 12.9.3 EXPANSIONS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 KONINKLIJKE PHILIPS N.V.

- 13.1.1.1 Business overview

- 13.1.1.2 Products offered

- 13.1.1.3 MnM view

- 13.1.1.3.1 Right to win

- 13.1.1.3.2 Strategic choices

- 13.1.1.3.3 Weaknesses and competitive threats

- 13.1.2 INOGEN, INC.

- 13.1.2.1 Business overview

- 13.1.2.2 Products offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Product launches & approvals

- 13.1.2.3.2 Deals

- 13.1.2.4 MnM view

- 13.1.2.4.1 Right to win

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses and competitive threats

- 13.1.3 JIANGSU YUYUE MEDICAL EQUIPMENT & SUPPLY CO., LTD.

- 13.1.3.1 Business overview

- 13.1.3.2 Products offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Deals

- 13.1.3.4 MnM view

- 13.1.3.4.1 Right to win

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses and competitive threats

- 13.1.4 CAIRE INC.

- 13.1.4.1 Business overview

- 13.1.4.2 Products offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Product launches & approvals

- 13.1.4.3.2 Deals

- 13.1.4.3.3 Expansions

- 13.1.4.4 MnM view

- 13.1.4.4.1 Right to win

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses and competitive threats

- 13.1.5 DRIVE DEVILBISS HEALTHCARE

- 13.1.5.1 Business overview

- 13.1.5.2 Products offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Product launches & approvals

- 13.1.5.4 MnM view

- 13.1.5.4.1 Right to win

- 13.1.5.4.2 Strategic choices

- 13.1.5.4.3 Weaknesses and competitive threats

- 13.1.6 TEIJIN LIMITED

- 13.1.6.1 Business overview

- 13.1.6.2 Products offered

- 13.1.7 DAIKIN INDUSTRIES, LTD.

- 13.1.7.1 Business overview

- 13.1.7.2 Products offered

- 13.1.8 ESAB CORPORATION (GCE GROUP)

- 13.1.8.1 Business overview

- 13.1.8.2 Products offered

- 13.1.9 REACT HEALTH

- 13.1.9.1 Business overview

- 13.1.9.2 Products offered

- 13.1.9.3 Recent developments

- 13.1.9.3.1 Deals

- 13.1.10 PRECISION MEDICAL, INC.

- 13.1.10.1 Business overview

- 13.1.10.2 Products offered

- 13.1.11 NIDEK MEDICAL PRODUCTS, INC.

- 13.1.11.1 Business overview

- 13.1.11.2 Products offered

- 13.1.12 O2 CONCEPTS, LLC

- 13.1.12.1 Business overview

- 13.1.12.2 Products offered

- 13.1.12.3 Recent developments

- 13.1.12.3.1 Product launches & approvals

- 13.1.12.3.2 Deals

- 13.1.13 BPL MEDICAL TECHNOLOGIES

- 13.1.13.1 Business overview

- 13.1.13.2 Products offered

- 13.1.14 BESCO

- 13.1.14.1 Business overview

- 13.1.14.2 Products offered

- 13.1.15 OXUS

- 13.1.15.1 Business overview

- 13.1.15.2 Products offered

- 13.1.1 KONINKLIJKE PHILIPS N.V.

- 13.2 OTHER COMPANIES

- 13.2.1 FOSHAN KEYHUB ELECTRONIC INDUSTRIES CO., LTD

- 13.2.2 LONGFIAN SCITECH CO., LTD.

- 13.2.3 SHENYANG CANTA MEDICAL TECH. CO., LTD.

- 13.2.4 BELLUSCURA

- 13.2.5 HOYO SCITECH CO., LTD.

- 13.2.6 HACENOR SOLUTIONS

- 13.2.7 XNUO INTERNATIONAL GROUP (USA) HOLDINGS

- 13.2.8 OXYMED

- 13.2.9 KALSTEIN

- 13.2.10 ESS PEE ENTERPRISES

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 CUSTOMIZATION OPTIONS

- 14.4 RELATED REPORTS

- 14.5 AUTHOR DETAILS