|

시장보고서

상품코드

1812624

디지털 전환 시장(-2031년) : 솔루션(고객 경험, 공정 자동화 플랫폼), 서비스(용도 및 인프라 현대화), 변혁 중점 분야별(재무, 오퍼레이션, 워크포스)Digital Transformation Market by Solution (Customer Experience, Process Automation Platform), Services (Application and Infrastructure Modernization), Transformation Focus Area (Financial, Operational, Workforce Transformation) - Global Forecast to 2031 |

||||||

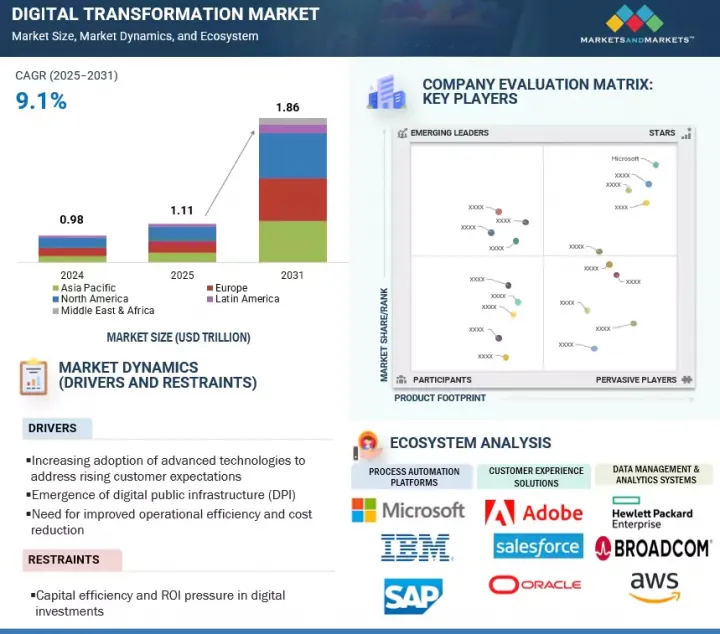

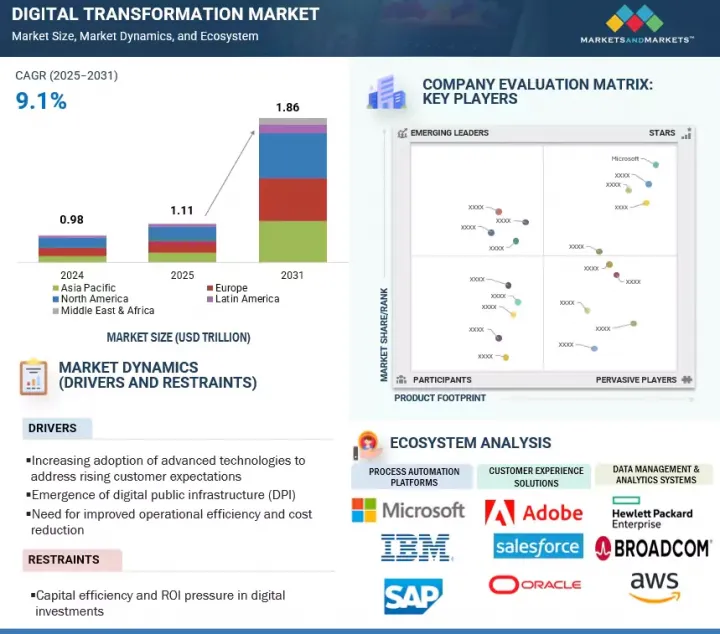

세계의 디지털 전환 시장은 빠르게 성장하고 있으며 시장 규모는 2025년 약 1조 1,100억 달러에서 예측 기간 중에는 9.1%의 연평균 복합 성장률(CAGR)로 성장을 지속하여 2031년까지 1조 8,600억 달러로 확대될 것으로 예측되고 있습니다.

운영 효율성 향상과 비용 절감에 대한 요구는 기업이 구식 시스템을 혁신하고 전사적 프로세스를 간소화하면서 디지털 변환을 추진하는 요인입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2020-2031년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2031년 |

| 단위 | 달러 |

| 부문 | 제공 구분, 기술, 변혁의 중점 분야, 조직 규모, 산업별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동, 아프리카, 라틴아메리카 |

클라우드 플랫폼, AI 중심의 애널리틱스, 통합 워크플로우 솔루션을 채택함으로써 기업은 IT 인프라를 통합하고 유지보수 비용을 절감하며 부서 간 협업을 개선할 수 있습니다. 디지털 변환은 프로세스 표준화, 리소스 최적화, 반복 작업 자동화를 지원하여 업무 속도와 정확성을 모두 향상시킵니다. 또한 데이터 기반 통찰력은 조직이 병목 현상을 발견하고 전략적으로 투자를 배분하는 데 도움이 됩니다. 효율성과 비용 관리에 주력함으로써 디지털 변환은 장기적인 업무 탄력성을 확보하고 경쟁력을 유지하는 데 중요한 요소가 되었습니다.

"솔루션 유형별로 공정 자동화 플랫폼이 예측 기간 동안 가장 빠른 성장을 이룰 전망"

공정 자동화 플랫폼은 운영 효율성 향상, 비용 절감, 워크플로우 최적화에 기업의 주력을 통해 가장 빠르게 성장하고 있습니다. 이 플랫폼은 로보틱 프로세스 자동화(RPA), AI, 지능형 워크플로우 관리를 활용하여 반복 작업을 자동화하고 비즈니스 프로세스를 간소화하며 인위적 실수를 줄입니다. 다양한 산업 조직들이 생산성 향상, 의사결정 가속화, 컴플라이언스 및 보고 강화를 위한 공정 자동화를 도입하고 있습니다. AI와 머신러닝 기능의 급속한 통합으로 실시간 프로세스 최적화 및 예측 분석이 가능하며, 이러한 솔루션은 확장성이 뛰어나고 민첩하고 데이터 중심의 디지털 변환을 목표로 하는 기업에 필수적입니다.

"산업별로는 BFSI(은행, 금융서비스 및 보험) 부문이 예측기간 동안 최대 점유율을 차지할 전망"

BFSI 부서는 운영 효율성 개선, 규제 준수, 보다 나은 고객 경험에 대한 요구에 따라 최대 시장 점유율을 차지합니다. BFSI 조직은 클라우드 컴퓨팅, AI, 애널리틱스, 프로세스 자동화를 적극적으로 도입하여 기간 업무, 리스크 관리, 고객 참여 활동을 간소화하고 있습니다. 디지털 전환은 실시간 거래 모니터링, 개인화된 금융 서비스, 원활한 옴니 채널 대응을 가능하게 하면서 보안을 강화하고 운영 비용을 절감합니다. 이 분야의 혁신, 데이터 중심의 의사 결정, 확장 가능한 기술 도입에 대한 주력은 BFSI를 세계 디지털 변환 업계의 성장을 견인하는 주요 원동력으로 삼고 있습니다.

"북미는 운용 효율로 디지털 전환을 추진, 아시아태평양은 디지털 공공 인프라로 진전"

북미는 성숙한 디지털 인프라, 첨단 IT 에코시스템, 업무, 고객 참여, 기업 워크플로우 전반에 걸쳐 AI의 광범위한 통합에 힘입어 디지털 전환 도입으로 계속 주도하고 있습니다. 첨단 기업은 AI 대응 솔루션을 활용하여 프로세스 자동화를 최적화하고, 예측적 의사결정을 개선하고, 부서 횡단적인 업무를 간소화하고 있습니다. 이 지역의 고급 분석 능력, 강력한 공급업체 생태계, 혁신 중심의 태도는 실시간 통찰력, 스마트 리소스 할당 및 자동화된 업무 효율성을 가능하게 합니다.

한편 아시아태평양은 급속한 기술 도입, 기업 디지털화의 진전, 디지털 공공 인프라에 대한 정부 지원 확대로 가장 급성장하고 있는 시장입니다. 중국, 인도, 한국 등 주요 시장에서는 업무 통합, 데이터 구동 전략의 실현, 고객 및 직원 체험 향상을 목적으로 솔루션이 도입되고 있습니다. 클라우드 도입의 확대, 도시화, 정책 이니셔티브가 더욱 보급을 가속화하고 있습니다. 효율성, 혁신, 가치를 높이는 확장 가능한 AI 탑재 솔루션을 요구하는 기업이 늘고 있는 가운데, 아시아태평양은 세계의 디지털 전환의 주요 성장 거점이 되고 있습니다.

본 보고서에서는 세계의 디지털 전환 시장을 조사했으며, 시장 개요, 시장 성장에 대한 각종 영향요인 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추이와 예측, 각종 구분 및 지역/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요와 업계 동향

- 시장 역학

- 성장 촉진요인

- 억제요인

- 기회

- 과제

- 2025년 미국 관세의 영향 : 디지털 전환 시장

- 시장의 진화

- 기술 로드맵

- 공급망 분석

- 생태계 분석

- 비즈니스 모델

- 성숙 모델

- 투자 및 자금조달 시나리오

- 사례 연구 분석

- 기술 분석

- 규제 상황

- 특허 분석

- 가격 분석

- 2025-2026년 주요 회의 및 이벤트

- Porter's Five Forces 분석

- 주요 이해관계자와 구매 기준

- 고객의 사업에 영향을 미치는 동향/혼란

- 생성형 AI가 디지털 전환에 미치는 영향

- 변혁의 여행 : 프로세스의 디지털화로부터 비즈니스 모델의 혁신으로

제6장 디지털 전환 시장 : 제공 구분별

- 솔루션

- 프로세스 자동화 플랫폼

- 고객 경험 솔루션

- 데이터 관리 및 분석 시스템

- 워크포스 활성화 툴

- 서비스

- 매니지드 서비스

제7장 디지털 전환 시장 : 변혁 중점 분야별

- 오퍼레이션

- 워크포스

- 고객중심

- 재무

- R&D

제8장 디지털 전환 시장 : 기술별

- 클라우드 컴퓨팅

- AI 및 애널리틱스

- 블록체인

- 사이버 보안

- IoT

- 기타

제9장 디지털 전환 시장 : 조직 규모별

- 중소기업

- 대기업

제10장 디지털 전환 시장 : 산업별

- BFSI

- 소매 및 E커머스

- IT 및 ITES

- 미디어 및 엔터테인먼트

- 제조

- 헬스케어, 생명과학, 의약품

- 에너지 및 유틸리티

- 정부 및 방위

- 통신

- 교육

- 수송 및 물류

- 건설 및 부동산

- 기타

제11장 디지털 전환 시장 : 지역별

- 북미

- 시장 성장 촉진요인

- 거시경제 전망

- 미국

- 캐나다

- 유럽

- 시장 성장 촉진요인

- 거시경제 전망

- 영국

- 독일

- 핀란드

- 스웨덴

- 기타

- 아시아태평양

- 시장 성장 촉진요인

- 거시경제 전망

- 중국

- 인도

- 한국

- 싱가포르

- 기타

- 중동 및 아프리카

- 시장 성장 촉진요인

- 거시경제 전망

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 기타

- 라틴아메리카

- 시장 성장 촉진요인

- 거시경제 전망

- 브라질

- 멕시코

- 기타

제12장 경쟁 구도

- 개요

- 주요 진입기업의 전략/강점

- 수익 분석

- 시장 점유율 분석

- 제품 비교 분석

- 기업평가와 재무지표

- 기업 평가 매트릭스 : 주요 기업(솔루션 공급자)

- 기업 평가 매트릭스 : 주요 기업(서비스 제공업체)

- 기업 평가 매트릭스 : 스타트업/중소기업

- 경쟁 시나리오와 동향

제13장 기업 프로파일

- 주요 기업(소프트웨어 중심)

- MICROSOFT

- SAP

- IBM

- ORACLE

- ADOBE

- SALESFORCE

- HPE

- HCLTECH

- AWS

- BROADCOM

- EQUINIX

- ALIBABA CLOUD

- BAIDU

- CISCO

- EMUDHRA

- HAPPIEST MINDS

- CENTIFIC

- TIBCO SOFTWARE

- BRILLIO

- 주요 기업(서비스 중심)

- ALMAVIVA

- COGNIZANT

- ERNST & YOUNG

- ACCENTURE

- GENPACT

- KYNDRYL

- SCIENCESOFT

- DELOITTE

- 기타 기업(소프트웨어 중심)

- BUDIBASE

- ELECTRONEEK

- AIXORA.AI

- MATTERWAY

- LAIYE

- ORBY AI

- KISSFLOW

- PROCESSMAKER

- PROCESS STREET

- INFINITUS SYSTEMS

- SCORO

- ALCOR SOLUTIONS

- SMARTSTREAM

- CLOUDANGLES

- SCITARA

- INTRINSIC

- AEXONIC TECHNOLOGIES

- 스타트업/SME(서비스 중심)

- VERITIS

- DEMPTON CONSULTING GROUP

- MAGNETAR IT

- AGICENT

제14장 인접 시장과 관련 시장

제15장 부록

JHS 25.09.26The digital transformation market is growing quickly, with an estimated value expected to increase from about USD 1.11 trillion in 2025 to USD 1.86 trillion by 2031, at a CAGR of 9.1% during the forecast period. The push for better operational efficiency and cost savings is driving digital transformation as organizations upgrade old systems and streamline enterprise-wide processes.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2031 |

| Base Year | 2024 |

| Forecast Period | 2025-2031 |

| Units Considered | USD Billion |

| Segments | Offering, Technology, Transformation Focus Area, Organization Size, and Vertical |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, and Latin America |

By adopting cloud platforms, AI-driven analytics, and integrated workflow solutions, companies can unify IT infrastructure, lower maintenance costs, and improve collaboration across departments. Digital transformation supports process standardization, resource optimization, and automation of repetitive tasks, boosting both speed and accuracy of operations. Additionally, data-driven insights help organizations spot bottlenecks and allocate investments strategically. This focus on efficiency and cost management makes digital transformation a key factor for long-term operational resilience and maintaining a competitive edge.

"By solution type, process automation platforms will witness the fastest growth during the forecast period."

Process automation platforms are experiencing the fastest growth in the digital transformation market, driven by enterprises' increasing focus on operational efficiency, cost reduction, and workflow optimization. These platforms utilize robotic process automation (RPA), AI, and intelligent workflow management to automate repetitive tasks, streamline business processes, and decrease human error. Organizations across industries are adopting process automation to boost productivity, speed up decision-making, and enhance compliance and reporting. The rapid incorporation of AI and machine learning capabilities allows for real-time process optimization and predictive analytics, making these solutions vital for organizations aiming for scalable, agile, and data-driven digital transformation efforts.

"By vertical, the BFSI segment is expected to hold the largest market share during the forecast period."

The BFSI sector holds the largest market share in the digital transformation industry, driven by the need for improved operational efficiency, regulatory compliance, and better customer experiences. BFSI organizations are increasingly adopting cloud computing, AI, analytics, and process automation to simplify core operations, risk management, and customer engagement activities. Digital transformation allows for real-time transaction monitoring, personalized financial services, and seamless omnichannel interactions while enhancing security and lowering operational costs. The sector's focus on innovation, data-driven decision-making, and scalable technology adoption makes BFSI a key driver of growth in the global digital transformation industry.

North America drives digital transformation through operational efficiency, while Asia Pacific advances with digital public infrastructure.

North America continues to lead in digital transformation adoption, supported by mature digital infrastructure, advanced IT ecosystems, and extensive integration of AI across operations, customer engagement, and enterprise workflows. Leading organizations use AI-enabled solutions to optimize process automation, improve predictive decision-making, and streamline cross-functional operations. The region's sophisticated analytics capabilities, strong vendor ecosystem, and focus on innovation enable real-time insights, smart resource allocation, and automated operational efficiency. Conversely, Asia Pacific is the fastest-growing market for digital transformation, driven by rapid technology adoption, increasing enterprise digitization, and growing government support for digital public infrastructure. Key markets such as China, India, and South Korea are implementing solutions to unify business operations, enable data-driven strategies, and improve customer and employee experiences. Growing cloud adoption, urbanization, and policy initiatives further speed up adoption. As enterprises look for scalable, AI-powered solutions to boost efficiency, innovation, and value, Asia Pacific is becoming a key growth hub for digital transformation worldwide.

Breakdown of Primaries

In-depth interviews were conducted with CEOs, innovation and technology directors, system integrators, and executives from various major organizations in the digital transformation industry.

- By Company: Tier I - 25%, Tier II - 45%, and Tier III - 30%

- By Designation: C-Level Executives - 35%, D-Level Executives - 40%, and Others - 25%

- By Region: North America - 45%, Europe - 25%, Asia Pacific - 15%, Middle East & Africa - 10%, and Latin America - 5%

The report includes a study of key players offering digital transformation solutions and services. The major market players include Microsoft (US), IBM (US), SAP (Germany), Oracle (US), Google (US), Salesforce (US), HPE (US), Adobe (US), AWS (US), HCLTech (India), EY (UK), Cognizant (US), Accenture (Ireland), Broadcom (US), Equinix (US), Alibaba Cloud (China), Baidu (China), Cisco (US), eMudhra (India), Happiest Minds (India), Budibase (Ireland), ElectroNeek (US), Aixora.ai (US), Matterway (Germany), Laiye (China), KissFlow (India), Orby AI (US), ProcessMaker (US), Process Street (US), Infinitus Systems (US), Scoro (UK), Alcor Solution (US), SmartStream (UK), Cloud Angles (US), Magnetar IT (UK), Scitara (US), Intrinsic (US), Dempton Consulting Group (Canada), Brillio (US), Aexonic Technologies (US), TIBCO Software (US), Genpact (US), Twilio (US), Kyndryl (US), Veritis (US), and ScienceSoft (US).

Research Coverage

This research report covers the digital transformation market and has been segmented based on offering, technology, transformation focus area, organization size, vertical, and region. The offering segment includes solutions and services. It also covers detailed information regarding drivers, restraints, challenges, and opportunities influencing the growth of the digital transformation market. A detailed analysis of the key industry players was conducted to provide insights into their business overview, solutions, and services; key strategies; contracts, partnerships, agreements, product & service launches, and mergers & acquisitions; and recent developments related to the market. This report also included a competitive analysis of upcoming startups in the market ecosystem.

Key Benefits of Buying the Report

The report will provide market leaders and new entrants with estimates of the revenue figures for the overall digital transformation market and its subsegments. It will help stakeholders understand the competitive landscape and gain insights to better position their businesses and develop effective go-to-market strategies. It will also offer stakeholders an understanding of the market's pulse and key information on drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

- Analysis of key drivers, such as the increasing adoption of advanced technologies to meet rising customer expectations, the emergence of digital public infrastructure (DPI), and the need for improved operational efficiency and cost reduction; restraints like capital efficiency and ROI pressures in digital investments; opportunities including leveraging generative and agentic AI for strategic digital advancement, redefining customer and workforce engagement via the Metaverse; and challenges like fragmented digital initiatives that hinder enterprise strategic alignment.

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and solutions & service launches in the digital transformation

- Market Development: Comprehensive information about lucrative markets - analyzing the digital transformation market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the digital transformation market

- Competitive Assessment: In-depth assessment of market share, growth strategies and service offerings of leading players such as Microsoft (US), IBM (US), SAP (Germany), Oracle (US), Google (US), Salesforce (US), HPE (US), Adobe (US), AWS (US), HCLTech (India), EY (UK), Cognizant (US), Accenture (Ireland), Broadcom (US), Equinix (US), Alibaba Cloud (China), Baidu (China), Cisco (US), eMudhra (India), Happiest Minds (India), Budibase (Ireland), ElectroNeek (US), Aixora.ai (US), Matterway (Germany), Laiye (China), KissFlow (India), Orby AI (US), ProcessMaker (US), Process Street (US), Infinitus Systems (US), Scoro (UK), Alcor Solution (US), SmartStream (UK), Cloud Angles (US), Magnetar IT (UK), Scitara (US), Intrinsic (US), Dempton Consulting Group (Canada), Brillio (US), Aexonic Technologies (US), TIBCO software (US), Genpact (US), Twilio (US), Kyndryl (US), Veritis (US), and ScienceSoft (US).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 OBJECTIVES OF THE STUDY

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Breakup of primary profiles

- 2.1.2.2 Key industry insights

- 2.2 MARKET BREAKUP AND DATA TRIANGULATION

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 TOP-DOWN APPROACH

- 2.3.2 BOTTOM-UP APPROACH

- 2.4 MARKET FORECAST

- 2.5 ASSUMPTIONS FOR THE STUDY

- 2.6 LIMITATIONS OF THE STUDY

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DIGITAL TRANSFORMATION MARKET

- 4.2 DIGITAL TRANSFORMATION MARKET: TOP SOLUTION TYPES

- 4.3 NORTH AMERICA: DIGITAL TRANSFORMATION MARKET, BY TOP TECHNOLOGY AND TRANSFORMATION FOCUS AREA

- 4.4 DIGITAL TRANSFORMATION MARKET: BY REGION

5 MARKET OVERVIEW AND INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Increasing adoption of advanced technologies to address rising customer expectations

- 5.2.1.2 Emergence of digital public infrastructure

- 5.2.1.3 Need for improved operational efficiency and cost reduction

- 5.2.2 RESTRAINTS

- 5.2.2.1 Capital efficiency and ROI pressure in digital investments

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Leveraging generative and agentic AI for strategic digital advancement

- 5.2.3.2 Redefining customer and workforce engagement via the Metaverse

- 5.2.4 CHALLENGES

- 5.2.4.1 Fragmented digital initiatives impeding enterprise strategic alignment

- 5.2.1 DRIVERS

- 5.3 IMPACT OF 2025 US TARIFF - DIGITAL TRANSFORMATION MARKET

- 5.3.1 INTRODUCTION

- 5.3.2 KEY TARIFF RATES

- 5.3.3 PRICE IMPACT ANALYSIS

- 5.3.3.1 Strategic shifts and emerging trends

- 5.3.4 KEY IMPACT ON VARIOUS REGIONS/COUNTRIES

- 5.3.4.1 US

- 5.3.4.1.1 Strategic shifts and key observations

- 5.3.4.2 China

- 5.3.4.2.1 Strategic shifts and key observations

- 5.3.4.3 Europe

- 5.3.4.3.1 Strategic shifts and key observations

- 5.3.4.4 India

- 5.3.4.4.1 Strategic shifts and key observations

- 5.3.4.1 US

- 5.3.5 IMPACT ON END-USE INDUSTRIES

- 5.3.5.1 Media & entertainment

- 5.3.5.2 Retail & eCommerce

- 5.3.5.3 Healthcare & life sciences

- 5.4 EVOLUTION OF DIGITAL TRANSFORMATION MARKET

- 5.5 DIGITAL TRANSFORMATION MARKET TECHNOLOGY ROADMAP

- 5.6 SUPPLY CHAIN ANALYSIS

- 5.7 ECOSYSTEM ANALYSIS

- 5.7.1 DIGITAL TRANSFORMATION SOLUTION PROVIDERS

- 5.7.2 DIGITAL TRANSFORMATION SERVICE PROVIDERS

- 5.8 BUSINESS MODELS OF DIGITAL TRANSFORMATION MARKET

- 5.9 DIGITAL TRANSFORMATION MARKET: MATURITY MODELS

- 5.10 INVESTMENT AND FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 BFSI

- 5.11.1.1 Cognizant's AI and automation solution helps property and casualty insurance company improve claims process

- 5.11.2 TELECOMMUNICATIONS

- 5.11.2.1 American TSP provider collaborates with HCL to enhance experience in dynamic virtual ecosystem

- 5.11.3 RETAIL & ECOMMERCE

- 5.11.3.1 ASOS uses Microsoft Azure ML to reduce time-to-market for recommendation model

- 5.11.4 ENERGY & UTILITIES

- 5.11.4.1 Searcher Seismic enables easy access in oil & gas industry with Cloudera solutions

- 5.11.5 HEALTHCARE & LIFE SCIENCES

- 5.11.5.1 Leading healthcare company adopts Cognizant's AI-driven solution to identify drug-seeking behavior

- 5.11.6 MANUFACTURING

- 5.11.6.1 IBM helps Shenzhen CSOT boost production quality and output

- 5.11.7 MEDIA & ENTERTAINMENT

- 5.11.7.1 Leading media conglomerate redefines with HCL's digital transformation solution

- 5.11.1 BFSI

- 5.12 TECHNOLOGY ANALYSIS

- 5.12.1 KEY TECHNOLOGIES

- 5.12.1.1 Low-code/No-code development platforms

- 5.12.1.2 MLOps

- 5.12.1.3 NLP

- 5.12.2 COMPLEMENTARY TECHNOLOGIES

- 5.12.2.1 AR/VR

- 5.12.2.2 Edge computing

- 5.12.2.3 3D printing (additive manufacturing)

- 5.12.3 ADJACENT TECHNOLOGIES

- 5.12.3.1 Digital twin modeling

- 5.12.3.2 Quantum computing

- 5.12.3.3 API management platforms

- 5.12.1 KEY TECHNOLOGIES

- 5.13 REGULATORY LANDSCAPE

- 5.13.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.13.2 KEY REGULATIONS

- 5.13.2.1 North America

- 5.13.2.1.1 US

- 5.13.2.1.2 Canada

- 5.13.2.2 Europe

- 5.13.2.3 Asia Pacific

- 5.13.2.3.1 Singapore

- 5.13.2.3.2 China

- 5.13.2.3.3 India

- 5.13.2.3.4 Japan

- 5.13.2.4 Middle East & Africa

- 5.13.2.4.1 UAE

- 5.13.2.4.2 Saudi Arabia

- 5.13.2.4.3 South Africa

- 5.13.2.5 Latin America

- 5.13.2.5.1 Brazil

- 5.13.2.5.2 Mexico

- 5.13.2.1 North America

- 5.14 PATENT ANALYSIS

- 5.14.1 METHODOLOGY

- 5.14.2 PATENTS FILED, BY DOCUMENT TYPE, 2016-2025

- 5.14.3 INNOVATION AND PATENT APPLICATIONS

- 5.15 PRICING ANALYSIS

- 5.15.1 AVERAGE SELLING PRICE OF OFFERINGS, BY KEY PLAYER, 2025

- 5.15.2 AVERAGE SELLING PRICE, BY TECHNOLOGY, 2025

- 5.16 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.17 PORTER'S FIVE FORCES ANALYSIS

- 5.17.1 THREAT OF NEW ENTRANTS

- 5.17.2 THREAT OF SUBSTITUTES

- 5.17.3 BARGAINING POWER OF SUPPLIERS

- 5.17.4 BARGAINING POWER OF BUYERS

- 5.17.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.18 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.18.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.18.2 BUYING CRITERIA

- 5.19 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.20 IMPACT OF GENERATIVE AI ON DIGITAL TRANSFORMATION

- 5.20.1 TOP USE CASES & MARKET POTENTIAL

- 5.20.1.1 Key use cases

- 5.20.1.1.1 Automated code generation

- 5.20.1.1.2 Customer support chatbots

- 5.20.1.1.3 Predictive maintenance

- 5.20.1.1.4 Fraud detection & prevention

- 5.20.1.1.5 Product development & design

- 5.20.1.1.6 Automated content creation

- 5.20.1.1 Key use cases

- 5.20.1 TOP USE CASES & MARKET POTENTIAL

- 5.21 TRANSFORMATION JOURNEY: FROM PROCESS DIGITIZATION TO BUSINESS MODEL INNOVATION

- 5.21.1 PROCESS DIGITIZATION

- 5.21.2 PROCESS OPTIMIZATION

- 5.21.3 DATA-DRIVEN DECISION MAKING

- 5.21.4 CUSTOMER EXPERIENCE

- 5.21.5 BUSINESS MODEL INNOVATION

- 5.21.6 STRATEGIC INTEGRATION

6 DIGITAL TRANSFORMATION MARKET, BY OFFERING

- 6.1 INTRODUCTION

- 6.1.1 OFFERING: DIGITAL TRANSFORMATION MARKET DRIVERS

- 6.2 SOLUTIONS

- 6.2.1 PROCESS AUTOMATION PLATFORMS

- 6.2.1.1 Enterprise modernization driven by process automation platforms and intelligent workflows

- 6.2.2 CUSTOMER EXPERIENCE SOLUTIONS

- 6.2.2.1 Enhanced engagement in enterprise transformation to boost segment

- 6.2.3 DATA MANAGEMENT AND ANALYTICS SYSTEMS

- 6.2.3.1 Data-driven decision-making with analytics to transform enterprise operations

- 6.2.4 WORKFORCE ENABLEMENT TOOLS

- 6.2.4.1 Accelerated organizational efficiency to drive segment

- 6.2.1 PROCESS AUTOMATION PLATFORMS

- 6.3 SERVICES

- 6.3.1 COMPREHENSIVE DIGITAL TRANSFORMATION SERVICES DRIVE GROWTH AND ORGANIZATIONAL EXCELLENCE

- 6.3.2 PROFESSIONAL SERVICES

- 6.3.2.1 Strategic professional services used to facilitate technology and business transformation

- 6.3.2.2 Training, strategy, and consulting

- 6.3.2.3 System integration & implementation

- 6.3.2.4 Support & maintenance

- 6.3.2.5 Infrastructure modernization

- 6.3.2.6 Application modernization

- 6.3.3 MANAGED SERVICES

7 DIGITAL TRANSFORMATION MARKET, BY TRANSFORMATION FOCUS AREA

- 7.1 INTRODUCTION

- 7.1.1 TRANSFORMATION FOCUS AREA: DIGITAL TRANSFORMATION MARKET DRIVERS

- 7.2 OPERATIONAL TRANSFORMATION

- 7.2.1 OPTIMIZED EFFICIENCY AND AGILITY THROUGH ADVANCED DIGITAL OPERATIONAL STRATEGIES

- 7.3 WORKFORCE TRANSFORMATION

- 7.3.1 ENHANCED ORGANIZATIONAL PRODUCTIVITY AND AGILITY THROUGH WORKFORCE ENGAGEMENT

- 7.4 CUSTOMER-CENTRIC TRANSFORMATION

- 7.4.1 PERSONALIZED EXPERIENCE AND ENGAGEMENT ENABLED THROUGH CUSTOMER-CENTRIC STRATEGIES

- 7.5 FINANCIAL TRANSFORMATION

- 7.5.1 OPTIMIZED FINANCIAL OPERATIONS AND DECISION-MAKING ACHIEVED THROUGH DIGITAL SOLUTIONS

- 7.6 R&D TRANSFORMATION

- 7.6.1 PRODUCT AND SERVICE INNOVATION DRIVEN THROUGH ADVANCED DIGITAL CAPABILITIES

8 DIGITAL TRANSFORMATION MARKET, BY TECHNOLOGY

- 8.1 INTRODUCTION

- 8.1.1 TECHNOLOGIES: DIGITAL TRANSFORMATION MARKET DRIVERS

- 8.2 CLOUD COMPUTING

- 8.2.1 WORKS AS FOUNDATIONAL ENABLER OF ENTERPRISE-WIDE MODERNIZATION

- 8.3 AI & ANALYTICS

- 8.3.1 HELPS ENHANCE ENTERPRISE INTELLIGENCE AND DECISION-MAKING

- 8.4 BLOCKCHAIN

- 8.4.1 HELPS IMPROVE OPERATIONS, INCREASE TRANSPARENCY, AND MAINTAIN DATA ACCURACY

- 8.5 CYBERSECURITY

- 8.5.1 STRENGTHENS ENTERPRISE RESILIENCE AND SECURES DIGITAL OPERATIONS

- 8.6 INTERNET OF THINGS

- 8.6.1 DRIVES CONNECTED SOFTWARE-BASED ENTERPRISE INSIGHTS AND OPTIMIZATION

- 8.7 OTHER TECHNOLOGIES

9 DIGITAL TRANSFORMATION MARKET, BY ORGANIZATION SIZE

- 9.1 INTRODUCTION

- 9.1.1 ORGANIZATION SIZE: DIGITAL TRANSFORMATION MARKET DRIVERS

- 9.2 SMES

- 9.2.1 DRIVE RAPID INNOVATION AND SCALABLE DIGITAL TECHNOLOGY ADOPTION

- 9.3 LARGE ENTERPRISES

- 9.3.1 LEAD COMPREHENSIVE TECHNOLOGY ADOPTION AND STRATEGIC DIGITAL GROWTH

10 DIGITAL TRANSFORMATION MARKET, BY VERTICAL

- 10.1 INTRODUCTION

- 10.1.1 VERTICALS: DIGITAL TRANSFORMATION MARKET DRIVERS

- 10.2 BFSI

- 10.2.1 USES AUTOMATION TO REDUCE MANUAL WORK PROCESSES, BOOST PRODUCTIVITY, AND LOWER COSTS OF OPERATION

- 10.2.2 AUTOMATIC FRAUD DETECTION & PREVENTION

- 10.2.3 ASSET & INVESTMENT MANAGEMENT

- 10.2.4 AUTOMATED CUSTOMER SERVICE (CHATBOTS)

- 10.2.5 HYPER-PERSONALIZED FINANCIAL SERVICES

- 10.2.6 REGULATORY COMPLIANCE MONITORING

- 10.2.7 OTHER BANKING, FINANCIAL SERVICES, AND INSURANCE APPLICATIONS

- 10.3 RETAIL & ECOMMERCE

- 10.3.1 DIGITAL TRANSITION TO HELP CUSTOMERS INTERACT WITH BRANDS, IMPROVE CUSTOMER EXPERIENCES, AND OPTIMIZE OPERATIONS

- 10.3.2 PERSONALIZED PRODUCT RECOMMENDATIONS

- 10.3.3 CUSTOMER RELATIONSHIP MANAGEMENT

- 10.3.4 PAYMENT SERVICES MANAGEMENT

- 10.3.5 SELF-CHECKOUT SYSTEMS

- 10.3.6 OMNICHANNEL INTEGRATION

- 10.3.7 OTHER RETAIL & ECOMMERCE APPLICATIONS

- 10.4 IT & ITES

- 10.4.1 NEED TO IMPROVE USER EXPERIENCE, ESTABLISH NEW REVENUE STREAMS, AND SCALE UP SERVICES TO FOSTER MARKET GROWTH

- 10.4.2 AUTOMATED CODE GENERATION & OPTIMIZATION

- 10.4.3 AUTOMATED IT ASSET MANAGEMENT

- 10.4.4 IT TICKETING & SUPPORT AUTOMATION

- 10.4.5 INTELLIGENT DATA BACKUP & RECOVERY

- 10.4.6 AUTOMATED SOFTWARE TESTING & QUALITY ASSURANCE

- 10.4.7 OTHER IT & ITES APPLICATIONS

- 10.5 MEDIA & ENTERTAINMENT

- 10.5.1 ENHANCEMENT IN CONTENT CREATION & GENERATION AND NEED FOR PERSONALIZED ADVERTISEMENT TO PROPEL MARKET

- 10.5.2 CONTENT RECOMMENDATION SYSTEMS

- 10.5.3 CONTENT CREATION & GENERATION

- 10.5.4 CONTENT COPYRIGHT PROTECTION

- 10.5.5 AUDIENCE ENGAGEMENT & PERSONALIZATION

- 10.5.6 PERSONALIZED ADVERTISING

- 10.5.7 OTHER MEDIA & ENTERTAINMENT APPLICATIONS

- 10.6 MANUFACTURING

- 10.6.1 NEED TO OPTIMIZE PRODUCTION SCHEDULES AND RESOURCE ALLOCATION TO FOSTER MARKET GROWTH

- 10.6.2 PREDICTIVE MAINTENANCE & MACHINERY INSPECTION

- 10.6.3 PRODUCTION PLANNING

- 10.6.4 DEFECT DETECTION & PREVENTION

- 10.6.5 QUALITY CONTROL

- 10.6.6 PRODUCTION LINE OPTIMIZATION

- 10.6.7 INTELLIGENT INVENTORY MANAGEMENT

- 10.6.8 OTHER MANUFACTURING APPLICATIONS

- 10.7 HEALTHCARE, LIFE SCIENCES, AND PHARMACEUTICALS

- 10.7.1 NEED FOR OPTIMIZED CLINICAL TRIALS, FAST-TRACKING OF NEW DRUG TIME-TO-MARKET TO DRIVE MARKET

- 10.7.2 ELECTRONIC HEALTH & MEDICAL RECORDS

- 10.7.3 TELEMEDICINE & REMOTE PATIENT MONITORING

- 10.7.4 AUTOMATIC APPOINTMENT SCHEDULING

- 10.7.5 MEDICAL IMAGING & DIAGNOSTICS

- 10.7.6 PATIENT BILLING MANAGEMENT

- 10.7.7 OTHER HEALTHCARE, LIFE SCIENCES, AND PHARMACEUTICAL APPLICATIONS

- 10.8 ENERGY & UTILITIES

- 10.8.1 NEED TO ACCOMPLISH OPERATIONAL EFFICIENCY AND ENCOURAGE SUSTAINABILITY TO DRIVE MARKET

- 10.8.2 ENERGY DEMAND FORECASTING

- 10.8.3 GRID OPTIMIZATION & MANAGEMENT

- 10.8.4 AUTOMATED ASSET TRACKING

- 10.8.5 SMART METERING & ENERGY DATA MANAGEMENT

- 10.8.6 REAL-TIME ENERGY MONITORING & CONTROL

- 10.8.7 OTHER ENERGY & UTILITIES APPLICATIONS

- 10.9 GOVERNMENT & DEFENSE

- 10.9.1 TRANSITION TO CLOUD-BASED SOLUTIONS FOR SAFE AND QUICK SHARING OF CRUCIAL INFORMATION TO BOOST GROWTH

- 10.9.2 INTELLIGENCE ANALYSIS & DATA PROCESSING

- 10.9.3 EGOVERNANCE & DIGITAL CITY SERVICES

- 10.9.4 BORDER SECURITY & SURVEILLANCE

- 10.9.5 DIGITAL IDENTITY & AUTHENTICATION

- 10.9.6 COMMAND & CONTROL SYSTEMS

- 10.9.7 TAX & REVENUE MANAGEMENT

- 10.9.8 OTHER GOVERNMENT & DEFENSE APPLICATIONS

- 10.10 TELECOMMUNICATIONS

- 10.10.1 NEED FOR ENHANCED SERVICE DELIVERY AND OPTIMIZATION TO PROPEL MARKET

- 10.10.2 NETWORK OPTIMIZATION

- 10.10.3 NETWORK SECURITY

- 10.10.4 CUSTOMER SERVICE & SUPPORT

- 10.10.5 NETWORK PLANNING & OPTIMIZATION

- 10.10.6 VOICE & SPEECH RECOGNITION

- 10.10.7 OTHER TELECOMMUNICATION APPLICATIONS

- 10.11 EDUCATION

- 10.11.1 NEED FOR PERSONALIZED LEARNING EXPERIENCES AND ENHANCED TEACHING PROCESSES TO BOOST MARKET

- 10.11.2 PERSONALIZED LEARNING

- 10.11.3 SMART CLASSROOMS

- 10.11.4 ADAPTIVE LEARNING & ASSESSMENT

- 10.11.5 DIGITAL TEXTBOOKS & EBOOKS

- 10.11.6 INTERACTIVE SIMULATIONS

- 10.11.7 OTHER EDUCATIONAL APPLICATIONS

- 10.12 TRANSPORTATION & LOGISTICS

- 10.12.1 OPTIMIZED RESOURCE USAGE AND ROUTE ENHANCEMENT TO DRIVE MARKET

- 10.12.2 ROUTE OPTIMIZATION

- 10.12.3 TRAFFIC MANAGEMENT

- 10.12.4 LAST-MILE LOGISTICS SYSTEMS

- 10.12.5 FLEET MANAGEMENT

- 10.12.6 INTELLIGENT PARKING SYSTEMS

- 10.12.7 OTHER TRANSPORTATION & LOGISTICS APPLICATIONS

- 10.13 CONSTRUCTION & REAL ESTATE

- 10.13.1 EMERGING CLOUD AND COLLABORATIVE TECHNOLOGIES RESHAPING OPERATIONS

- 10.13.2 DIGITAL PROJECT PLANNING & DESIGN

- 10.13.3 SITE OPERATIONS & RESOURCE MONITORING

- 10.13.4 SMART ASSET & FACILITY MANAGEMENT

- 10.13.5 DIGITAL SALES & LEASING EXPERIENCE

- 10.13.6 OTHER CONSTRUCTION & REAL ESTATE

- 10.14 OTHER VERTICALS

11 DIGITAL TRANSFORMATION MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 NORTH AMERICA: DIGITAL TRANSFORMATION MARKET DRIVERS

- 11.2.2 NORTH AMERICA: MACROECONOMIC OUTLOOK

- 11.2.3 US

- 11.2.3.1 Need to improve efficiency and adapt to consumer habits to drive market

- 11.2.4 CANADA

- 11.2.4.1 Government initiatives and need to bypass in-person sales and marketing to propel market

- 11.3 EUROPE

- 11.3.1 EUROPE: DIGITAL TRANSFORMATION MARKET DRIVERS

- 11.3.2 EUROPE: MACROECONOMIC OUTLOOK

- 11.3.3 UK

- 11.3.3.1 Technological advancements and government initiatives to improve digital capabilities to fuel market growth

- 11.3.4 GERMANY

- 11.3.4.1 Increased technology adoption and strategic government regulations to foster market growth

- 11.3.5 FINLAND

- 11.3.5.1 Establishment of "Digital Finland Framework" to promote innovation and improve digital skills to propel market

- 11.3.6 SWEDEN

- 11.3.6.1 Advancing AI research and sustainability initiatives accelerate digital future

- 11.3.7 REST OF EUROPE

- 11.4 ASIA PACIFIC

- 11.4.1 ASIA PACIFIC: DIGITAL TRANSFORMATION MARKET DRIVERS

- 11.4.2 ASIA PACIFIC: MACROECONOMIC OUTLOOK

- 11.4.3 CHINA

- 11.4.3.1 Integration of sophisticated technologies into contemporary business systems to fuel market growth

- 11.4.4 INDIA

- 11.4.4.1 Technological advancements, wider internet access, and government efforts to bolster market growth

- 11.4.5 SOUTH KOREA

- 11.4.5.1 Ongoing government support, investment in innovative technologies, and thriving startup scenario to drive market

- 11.4.6 SINGAPORE

- 11.4.6.1 Innovation-driven market leadership result of public-private collaboration

- 11.4.7 REST OF ASIA PACIFIC

- 11.5 MIDDLE EAST & AFRICA

- 11.5.1 MIDDLE EAST & AFRICA: DIGITAL TRANSFORMATION MARKET DRIVERS

- 11.5.2 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

- 11.5.3 SAUDI ARABIA

- 11.5.3.1 Vision 2030 initiative, investments in digital infrastructure, and focus on eGovernance to boost market growth

- 11.5.4 UAE

- 11.5.4.1 Strong infrastructure, supportive regulatory environment, government focus on technology and innovation to fuel market growth

- 11.5.5 SOUTH AFRICA

- 11.5.6 REST OF MIDDLE EAST & AFRICA

- 11.6 LATIN AMERICA

- 11.6.1 LATIN AMERICA: DIGITAL TRANSFORMATION MARKET DRIVERS

- 11.6.2 LATIN AMERICA: MACROECONOMIC OUTLOOK

- 11.6.3 BRAZIL

- 11.6.3.1 Digital Transformation Strategy (E-Digital) to boost market

- 11.6.4 MEXICO

- 11.6.4.1 Enhanced customer experience and streamlined operations to fuel market growth

- 11.6.5 REST OF LATIN AMERICA

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- 12.3 REVENUE ANALYSIS, 2020-2024

- 12.4 MARKET SHARE ANALYSIS, 2024

- 12.5 PRODUCT COMPARATIVE ANALYSIS

- 12.5.1 PRODUCT COMPARATIVE ANALYSIS, BY OFFERING (SOLUTION PROVIDERS)

- 12.5.1.1 Microsoft Dynamics 365 (Microsoft)

- 12.5.1.2 IBM Watsonx (IBM)

- 12.5.1.3 Salesforce Einstein Platform (Salesforce)

- 12.5.1.4 Google Cloud (Google)

- 12.5.1.5 Oracle Digital Connect (Oracle)

- 12.5.2 PRODUCT COMPARATIVE ANALYSIS, BY OFFERING (SERVICE PROVIDERS)

- 12.5.2.1 Intelligent Process Automation Services (Cognizant)

- 12.5.2.2 Technology Transformation services (Ernst & Young)

- 12.5.2.3 Enterprise Platform Services (Accenture)

- 12.5.2.4 Intelligent Automation services (Genpact)

- 12.5.2.5 Digital Transformation Services (ScienceSoft)

- 12.5.1 PRODUCT COMPARATIVE ANALYSIS, BY OFFERING (SOLUTION PROVIDERS)

- 12.6 COMPANY VALUATION AND FINANCIAL METRICS

- 12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024 (SOLUTION PROVIDERS)

- 12.7.1 STARS

- 12.7.2 EMERGING LEADERS

- 12.7.3 PERVASIVE PLAYERS

- 12.7.4 PARTICIPANTS

- 12.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024 (SOLUTION PROVIDERS)

- 12.7.5.1 Company footprint

- 12.7.5.2 Regional footprint

- 12.7.5.3 Offering footprint

- 12.7.5.4 Transformation focus area footprint

- 12.7.5.5 Vertical footprint

- 12.8 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024 (SERVICE PROVIDERS)

- 12.8.1 STARS

- 12.8.2 EMERGING LEADERS

- 12.8.3 PERVASIVE PLAYERS

- 12.8.4 PARTICIPANTS

- 12.8.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024 (SERVICE PROVIDERS)

- 12.8.5.1 Company footprint

- 12.8.5.2 Regional footprint

- 12.8.5.3 Offering footprint

- 12.8.5.4 Transformation focus area footprint

- 12.8.5.5 Vertical footprint

- 12.9 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 12.9.1 PROGRESSIVE COMPANIES

- 12.9.2 RESPONSIVE COMPANIES

- 12.9.3 DYNAMIC COMPANIES

- 12.9.4 STARTING BLOCKS

- 12.9.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 12.9.5.1 Detailed list of key startups/SMEs

- 12.9.5.2 Competitive benchmarking of key startups/SMEs

- 12.10 COMPETITIVE SCENARIO AND TRENDS

- 12.10.1 PRODUCT LAUNCHES AND ENHANCEMENTS

- 12.10.2 DEALS

13 COMPANY PROFILES

- 13.1 INTRODUCTION

- 13.2 KEY PLAYERS (SOFTWARE-CENTRIC)

- 13.2.1 MICROSOFT

- 13.2.1.1 Business overview

- 13.2.1.2 Products/Solutions/Services offered

- 13.2.1.3 Recent developments

- 13.2.1.3.1 Product launches and enhancements

- 13.2.1.3.2 Deals

- 13.2.1.4 MnM view

- 13.2.1.4.1 Right to win

- 13.2.1.4.2 Strategic choices

- 13.2.1.4.3 Weaknesses and competitive threats

- 13.2.2 SAP

- 13.2.2.1 Business overview

- 13.2.2.2 Products/Solutions/Services offered

- 13.2.2.3 Recent developments

- 13.2.2.3.1 Product launches and enhancements

- 13.2.2.3.2 Deals

- 13.2.2.4 MnM view

- 13.2.2.4.1 Right to win

- 13.2.2.4.2 Strategic choices

- 13.2.2.4.3 Weaknesses and competitive threats

- 13.2.3 GOOGLE

- 13.2.3.1 Business overview

- 13.2.3.2 Products/Solutions/Services offered

- 13.2.3.3 Recent developments

- 13.2.3.3.1 Product launches and enhancements

- 13.2.3.3.2 Deals

- 13.2.3.4 MnM view

- 13.2.3.4.1 Right to win

- 13.2.3.4.2 Strategic choices

- 13.2.3.4.3 Weaknesses and competitive threats

- 13.2.4 IBM

- 13.2.4.1 Business overview

- 13.2.4.2 Products/Solutions/Services offered

- 13.2.4.3 Recent developments

- 13.2.4.3.1 Product launches and enhancements

- 13.2.4.3.2 Deals

- 13.2.4.4 MnM view

- 13.2.4.4.1 Right to win

- 13.2.4.4.2 Strategic choices

- 13.2.4.4.3 Weaknesses and competitive threats

- 13.2.5 ORACLE

- 13.2.5.1 Business overview

- 13.2.5.2 Products/Solutions/Services offered

- 13.2.5.3 Recent developments

- 13.2.5.3.1 Product launches and enhancements

- 13.2.5.3.2 Deals

- 13.2.5.4 MnM view

- 13.2.5.4.1 Right to win

- 13.2.5.4.2 Strategic choices

- 13.2.5.4.3 Weaknesses and competitive threats

- 13.2.6 ADOBE

- 13.2.6.1 Business overview

- 13.2.6.2 Products/Solutions/Services offered

- 13.2.6.3 Recent developments

- 13.2.6.3.1 Product launches and enhancements

- 13.2.6.3.2 Deals

- 13.2.7 SALESFORCE

- 13.2.7.1 Business overview

- 13.2.7.2 Products/Solutions/Services offered

- 13.2.7.3 Recent developments

- 13.2.7.3.1 Product launches and enhancements

- 13.2.7.3.2 Deals

- 13.2.8 HPE

- 13.2.8.1 Business overview

- 13.2.8.2 Products/Solutions/Services offered

- 13.2.8.3 Recent developments

- 13.2.8.3.1 Product launches and enhancements

- 13.2.8.3.2 Deals

- 13.2.9 HCLTECH

- 13.2.9.1 Business overview

- 13.2.9.2 Products/Solutions/Services offered

- 13.2.9.3 Recent developments

- 13.2.9.3.1 Product launches and enhancements

- 13.2.9.3.2 Deals

- 13.2.10 AWS

- 13.2.10.1 Business overview

- 13.2.10.2 Products/Solutions/Services offered

- 13.2.10.3 Recent developments

- 13.2.10.3.1 Product launches and enhancements

- 13.2.10.4 Deals

- 13.2.11 BROADCOM

- 13.2.12 EQUINIX

- 13.2.13 ALIBABA CLOUD

- 13.2.14 BAIDU

- 13.2.15 CISCO

- 13.2.16 EMUDHRA

- 13.2.17 HAPPIEST MINDS

- 13.2.18 CENTIFIC

- 13.2.19 TIBCO SOFTWARE

- 13.2.20 BRILLIO

- 13.2.1 MICROSOFT

- 13.3 KEY PLAYERS (SERVICE-CENTRIC)

- 13.3.1 ALMAVIVA

- 13.3.1.1 Business overview

- 13.3.1.2 Recent developments

- 13.3.1.2.1 Deals

- 13.3.1.2.2 Expansions

- 13.3.2 COGNIZANT

- 13.3.3 ERNST & YOUNG

- 13.3.4 ACCENTURE

- 13.3.5 GENPACT

- 13.3.6 KYNDRYL

- 13.3.7 SCIENCESOFT

- 13.3.8 DELOITTE

- 13.3.1 ALMAVIVA

- 13.4 OTHER PLAYERS (SOFTWARE-CENTRIC)

- 13.4.1 BUDIBASE

- 13.4.2 ELECTRONEEK

- 13.4.3 AIXORA.AI

- 13.4.4 MATTERWAY

- 13.4.5 LAIYE

- 13.4.6 ORBY AI

- 13.4.7 KISSFLOW

- 13.4.8 PROCESSMAKER

- 13.4.9 PROCESS STREET

- 13.4.10 INFINITUS SYSTEMS

- 13.4.11 SCORO

- 13.4.12 ALCOR SOLUTIONS

- 13.4.13 SMARTSTREAM

- 13.4.14 CLOUDANGLES

- 13.4.15 SCITARA

- 13.4.16 INTRINSIC

- 13.4.17 AEXONIC TECHNOLOGIES

- 13.5 STARTUPS/SMES (SERVICE-CENTRIC)

- 13.5.1 VERITIS

- 13.5.2 DEMPTON CONSULTING GROUP

- 13.5.3 MAGNETAR IT

- 13.5.4 AGICENT

14 ADJACENT AND RELATED MARKETS

- 14.1 INTRODUCTION

- 14.2 ARTIFICIAL INTELLIGENCE (AI) MARKET - GLOBAL FORECAST TO 2032

- 14.2.1 MARKET DEFINITION

- 14.2.2 MARKET OVERVIEW

- 14.2.2.1 Artificial intelligence market, by offering

- 14.2.2.2 Artificial intelligence market, by technology

- 14.2.2.3 Artificial intelligence market, by end user

- 14.2.2.4 Artificial intelligence market, by region

- 14.3 CLOUD COMPUTING MARKET - GLOBAL FORECAST TO 2028

- 14.3.1 MARKET DEFINITION

- 14.3.2 MARKET OVERVIEW

- 14.3.2.1 Cloud computing market, by service model

- 14.3.2.2 Cloud computing market, by deployment model

- 14.3.2.3 Cloud computing market, by organization size

- 14.3.2.4 Cloud computing market, by vertical

- 14.3.2.5 Cloud computing market, by region

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS