|

시장보고서

상품코드

1823724

용접 장비, 액세서리, 소모품 시장 예측(-2030년) : 장비별, 액세서리별, 소모품별, 기술별, 최종 용도 산업별, 지역별Welding Equipment, Accessories, and Consumables Market by Equipment, Accessory, Consumable, Technology, End-use Industry, Region - Global Forecast to 2030 |

||||||

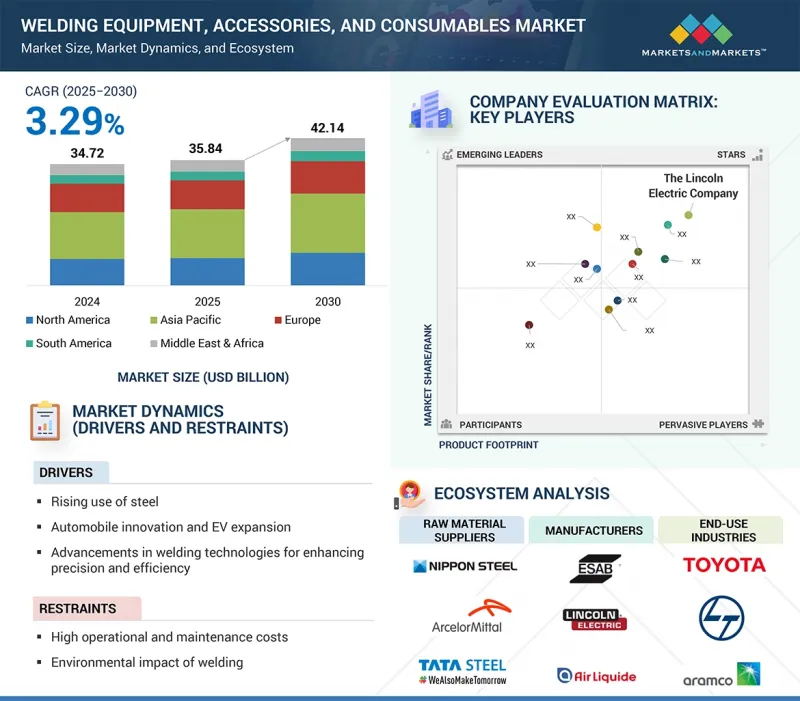

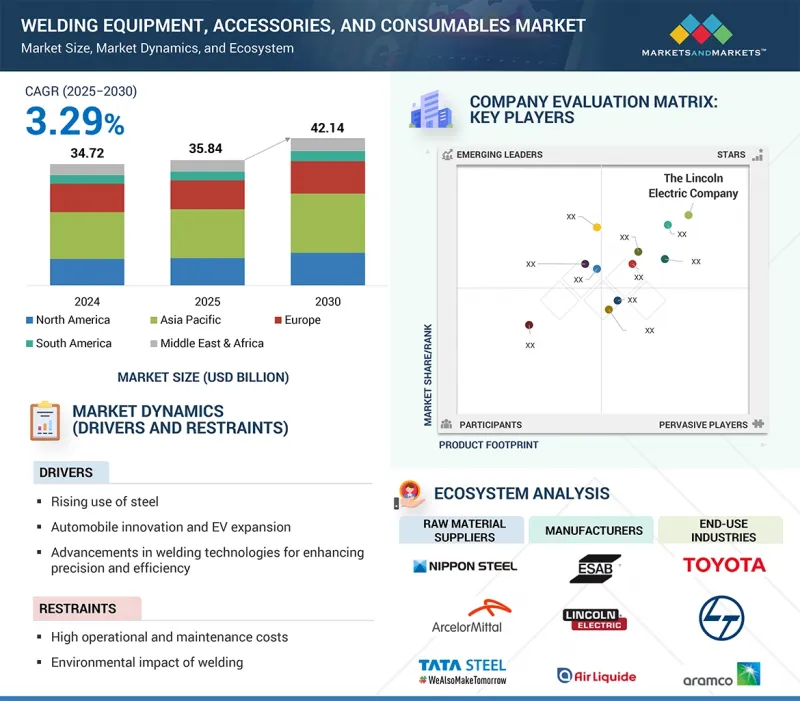

세계의 용접 장비·액세서리·소모품 시장 규모는 2025년에 358억 4,000만 달러, 2030년까지 421억 4,000만 달러에 달할 것으로 예측되며, CAGR로 3.29%의 성장이 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2021-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 100만 달러/10억 달러 |

| 부문 | 장비, 소모품, 액세서리, 기술, 최종 용도 산업, 지역 |

| 대상 지역 | 아시아태평양, 북미, 유럽, 중동 및 아프리카, 남미 |

용접 장비 및 액세서리, 소모품 시장은 다양한 요인으로 인해 성장이 예상됩니다. 철강 사용 확대, 자동차 기술 혁신과 전기자동차 성장, 정밀도와 효율성을 향상시키는 용접 기술 발전, 기타 최종 사용 산업에서 수요 증가가 시장을 촉진할 것으로 예측됩니다.

"전극 및 용가재 장비 부문이 예측 기간 중 시장을 주도할 것입니다. "

용접 소모품, 장비 및 액세서리 부문에서 전극 및 용가재 장비 부문의 성장은 자동차, 건설, 중공업 등 여러 산업에 걸친 다양한 구조적, 기술적 요인에 의해 촉진되고 있습니다. 전극과 용가재는 용접 공정에서 매우 중요하며, 인프라 개발, 조선, 에너지, 자동차 제조에서 용접의 사용이 증가함에 따라 수요가 증가할 것입니다. 자동차 및 전기자동차 생산에서 고강도 강철, 합금 및 경량 재료로의 전환은 내구성, 내식성 및 정밀한 연결을 제공하는 특수 용가재 및 첨단 유형의 전극에 대한 요구를 창출하고 있습니다.

"아크 용접 부문이 예측 기간 중 시장을 주도할 것입니다. "

아크 용접 부문은 예측 기간 중 용접 장비, 액세서리 및 소모품의 가장 큰 시장 점유율을 차지할 것으로 예측됩니다. 이 기술에서는 전극과 모재 사이에 전기아크를 발생시켜 금속을 녹이는 용접 공정에 고농도의 열이 포함됩니다. 또한 금속의 안정된 석출, 우수한 내식성, 높은 충격 인성으로 인해 주요 용접 기술로 자리 잡았습니다. 아크 용접은 또한 비용 효율적이고 다양한 금속 표면에 대응할 수 있으므로 산업계에서도 인기가 높습니다. 아크 용접이 신뢰할 수 있고 내구성이 뛰어나며 효율적인 금속 접합이 필요한 산업에서 용접 장비, 액세서리 및 소모품으로 아크 용접이 선호되는 이유는 바로 이러한 장점 때문입니다.

"플럭스 와이어는 예측 기간 중 두 번째로 큰 부문이 될 것입니다. "

플럭스 와이어는 용접 소모품, 장비 및 액세서리 중 강력한 성장세를 보이고 있습니다. 플럭스 와이어는 대부분의 현대 용접 용도에서 필수적인 투입물이며, 효율성, 생산성 및 용접 품질에 직접적인 영향을 미치기 때문입니다. 인프라, 자동차, 조선, 에너지 부문의 확대가 대규모 용접 작업을 추진하고 있으며, 여기서 플럭스(서브머지드 아크 용접, 플럭스 함유 아크 용접 등에 사용)와 와이어(솔리드 와이어, 플럭스 함유 와이어, 서브머지드 아크 와이어)가 매우 중요합니다. 이러한 소모품은 안정적인 용접 강도, 높은 용접 속도, 아크 안정성 향상을 보장하며 대량 생산에 필수적입니다.

"연기 추출 장비는 예측 기간 중 두 번째 시장 점유율을 차지할 것입니다. "

작업자의 건강, 규제 준수, 작업장 효율성에 대한 관심이 높아지면서 용접 소모품, 장비 및 액세서리 분야에서 흄 추출 장비가 큰 성장세를 보이고 있습니다. 용접은 망간, 6가 크롬, 니켈과 같은 금속을 포함한 유해한 흄과 미립자 물질을 발생시켜 호흡기 질환, 신경 장애, 장기적인 직업적 건강 위험과 관련이 있습니다. 이러한 위험에 대한 인식이 높아짐에 따라 업계는 용접공과 주변 작업자를 보호하기 위해 흄 추출 장비와 환기 시스템 설치에 주력하고 있습니다.

"일반 제조 부문이 예측 기간 중 두 번째 시장 점유율을 차지할 것입니다. "

일반 제조 부문은 향후 예측 기간 중 용접 장비, 액세서리 및 소모품에서 금액 기준으로 두 번째로 큰 시장이 될 것으로 예측됩니다. 이 부문에는 경공업, 일반 제조, 예술적 금속 가공, 브레이징 및 납땜 기술 등 다양한 산업과 용도가 포함됩니다. 또한 연구소나 철강 용접 전용 센터에서 이루어지는 다양한 유형의 용접도 포함됩니다. 이 부문에서는 편의성과 다용도로 평가받는 봉용접, 정밀도와 숙련된 기술로 알려진 텅스텐 무산소 가스(TIG) 용접, 대량 생산의 효율성으로 평가받는 금속 무산소 가스(MIG) 용접 등 다양한 기술에 다양한 용접 장비가 사용되고 있습니다. 다양한 가공 분야에서 용접 금속 제품에 대한 수요가 증가함에 따라 용접 장비, 액세서리 및 소모품 시장의 성장이 촉진되고 있으며, 산업계는 구조적 무결성 및 전체 생산 능력에서 이러한 기술에 대한 의존도가 높아지고 있습니다.

세계의 용접 장비·액세서리·소모품 시장에 대해 조사분석했으며, 주요 촉진요인과 억제요인, 경쟁 구도, 향후 동향 등의 정보를 제공하고 있습니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 중요 인사이트

- 용접 장비·액세서리·소모품 시장의 기업에 매력적인 기회

- 아시아태평양의 용접 장비·액세서리·소모품 시장 : 소모품별

제5장 시장 개요

- 서론

- 시장 역학

- 촉진요인

- 억제요인

- 기회

- 과제

- 고객 비즈니스에 영향을 미치는 동향과 혼란

- 고객 비즈니스에 영향을 미치는 동향과 혼란

- 가격결정 분석

- 에코시스템 분석

- 밸류체인 분석

- 관세와 규제 상황

- 관세 분석(HS 코드 : 846820)

- 규제기관, 정부기관, 기타 조직

- 주요 규제

- 무역 분석

- 수출 시나리오(HS 코드 846820)

- 수입 시나리오(HS 코드 846820)

- 기술 분석

- 주요 기술

- 보완 기술

- 인접 기술

- 특허 분석

- 서론

- 조사 방법

- 용접 장비·액세서리·소모품 시장, 특허 분석(2015-2024년)

- 주요 컨퍼런스와 이벤트(2025-2026년)

- 사례 연구 분석

- 투자와 자금조달 시나리오

- 용접 장비·액세서리·소모품 시장에 대한 생성형 AI/AI의 영향

- Porter's Five Forces 분석

- 주요 이해관계자와 구입 기준

- 거시경제 분석

- 서론

- GDP의 동향과 예측

- 용접 장비·액세서리·소모품 시장에 대한 2025년 미국 관세의 영향

- 서론

- 주요 관세율

- 가격의 영향 분석

- 국가/지역에 대한 영향

- 최종 용도 산업에 대한 영향

제6장 용접 장비·액세서리·소모품 시장 : 장비별

- 서론

- 전극·용가재 장비

- 산소 연료 가스 장비

- 레이저 장비

- 기타 장비

제7장 용접 장비·액세서리·소모품 시장 : 액세서리별

- 서론

- 가스 레귤레이터

- 가스 유량계

- 가스 필터

- 체크 밸브

- 가스 매니폴드

- 플로우 컨트롤러

- 가스 패널

- 가스 캐비닛

- 보호구

- 흄 추출 장비

제8장 용접 장비·액세서리·소모품 시장 : 소모품별

- 서론

- 전극·용가재

- 플럭스·와이어

- 가스

제9장 용접 장비·액세서리·소모품 시장 : 기술별

- 서론

- 아크 용접

- 산소 연료 용접

- 기타 기술

제10장 용접 장비·액세서리·소모품 시장 : 최종 용도 산업별

- 서론

- 중기/토목 기기

- 트럭·트레일러

- 일반 제조

- 자동차

- 레일

- 탱크·압력 용기

- 항공우주

- 해사·조선

- 건설 인프라

- 석유 및 가스

- 발전

- 파이프라인

- 정비·수리

제11장 용접 장비·액세서리·소모품 시장 : 지역별

- 서론

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 중동 및 아프리카

- GCC 국가

- 남아프리카공화국

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

제12장 경쟁 구도

- 개요

- 주요 참여 기업의 전략/강점

- 시장 점유율 분석(2024년)

- 매출 분석(2020-2024년)

- 기업의 평가와 재무 지표

- 제품/브랜드의 비교

- 기업 평가 매트릭스 : 주요 기업(2024년)

- 기업 평가 매트릭스 : 스타트업/중소기업(2024년)

- 경쟁 시나리오

제13장 기업 개요

- 주요 기업

- THE LINCOLN ELECTRIC COMPANY

- ESAB

- ILLINOIS TOOL WORKS INC.

- FRONIUS INTERNATIONAL GMBH

- KEMPPI OY

- PANASONIC HOLDINGS CORPORATION

- DAIHEN CORPORATION

- AIR LIQUIDE

- VOESTALPINE AG

- SHENZHEN MEGMEET ELECTRIC CO., LTD.

- 기타 기업

- PRECISION CASTPARTS CORP.

- HYUNDAI WELDING CO.

- ADOR WELDING

- ATLANTIC CHINA WELDING CONSUMABLES

- OBARA GROUP INC.

- AMADA WELD TECH

- SWAGELOK COMPANY

- FORTIUS METALS

- CARL CLOOS SCHWEISSTECHNIK GMBH

- ROCKMOUNT

- WELDFAST ELECTRODES PVT. LTD.

- D&H SECHERON

- GEDIK WELDING

- SUPERON SCHWEISSTECHNIK INDIA

- NEXA WELD

제14장 인접 시장과 관련 시장

- 서론

- 로봇 용접 시장

- 시장의 정의

- 시장의 개요

- 로봇 용접 시장 : 유형별

- 로봇 용접 시장 : 페이로드별

- 로봇 용접 시장 : 최종사용자별

- 로봇 용접 시장 : 지역별

제15장 부록

KSA 25.10.02The market for welding equipment, accessories, and consumables is projected to be valued at USD 35.84 billion in 2025 and reach USD 42.14 billion by 2030, at a CAGR of 3.29%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million/USD Billion) |

| Segments | Equipment, Consumable, Accessory, Technology, End-use industry, and Region |

| Regions covered | Asia Pacific, North America, Europe, Middle East & Africa, and South America |

The market for welding equipment, accessories, and consumables is expected to grow due to various factors. Expanding steel usage, automotive innovation and EV growth, advances in welding technologies that improve precision and efficiency, and rising demand from other end-user industries are expected to drive the market.

"Electrode & filler material equipment segment to lead market during forecast period"

The growth of the electrode & filler material equipment segment in the welding consumables, equipment, and accessories sector is driven by various structural and technological factors across multiple industries, especially automotive, construction, and heavy manufacturing. Electrodes and filler materials are crucial in welding processes, and their demand rises with increased use of welding for infrastructure development, shipbuilding, energy, and automotive manufacturing. The shift toward high-strength steels, alloys, and lightweight materials in automotive and electric vehicle production has created a need for specialized filler materials and advanced types of electrodes that provide durability, corrosion resistance, and precise connections.

"Arc welding segment to lead market during forecast period"

The arc welding segment is expected to be the largest part of the market for welding equipment, accessories, and consumables throughout the forecast period. This technique involves a high concentration of heat in the welding process, where an electric arc is created between the electrode and the base materials, causing the metals to melt. Additionally, the steady deposition of metal, excellent resistance to corrosion, and high impact toughness make it a leading welding technology. Arc welding is also popular in the industry because of its cost-effectiveness and ability to work with various metal surfaces. These benefits explain why arc welding remains a preferred choice for welding equipment, accessories, and consumables in industries requiring reliable, durable, and efficient metal joining.

"Fluxes and wires to be second-largest segment during forecast period"

Fluxes and wires are experiencing strong growth in welding consumables, equipment, and accessories because they are essential inputs in most modern welding applications and directly influence efficiency, productivity, and weld quality. The expansion of infrastructure, automotive, shipbuilding, and energy sectors is fueling extensive welding activities, where fluxes (used in submerged arc welding, flux-cored arc welding, etc.) and wires (solid wires, flux-cored wires, and submerged arc wires) are crucial. These consumables ensure consistent weld strength, higher deposition rates, and improved arc stability, making them vital for high-volume production.

"Fume extraction equipment to hold second-largest market share during forecast period"

Fume extraction equipment is experiencing significant growth in welding consumables, equipment, and accessories because of rising concerns about worker health, regulatory compliance, and workplace efficiency. Welding produces hazardous fumes and particulate matter that contain metals like manganese, hexavalent chromium, and nickel, which are associated with respiratory illnesses, neurological problems, and long-term occupational health risks. With increased awareness of these hazards, industries are focusing on installing fume extraction and ventilation systems to safeguard welders and nearby workers.

"General fabrication segment to hold second-largest market share during forecast period"

The General Fabrication segment is expected to be the second-largest market in welding equipment, accessories, and consumables, based on value, during the upcoming forecast period. This segment includes a wide range of industries and applications, such as light fabrication, general manufacturing, artistic metalwork, as well as brazing and soldering techniques. It also covers various types of welding performed in laboratories and dedicated steel welding centers. A variety of welding equipment is used across this sector for different techniques, like stick welding, valued for its simplicity and versatility; tungsten inert gas (TIG) welding, known for its precision and skillfulness; and metal inert gas (MIG) welding, praised for its efficiency in high-volume production. The growing demand for welded metal products in multiple fabrication applications is driving growth in the welding equipment, accessories, and consumables market, as industries increasingly depend on these technologies for their structural integrity and overall production capacity.

"Asia Pacific welding equipment, accessories, and consumables market to register highest CAGR during forecast period"

The welding equipment, accessories, and consumables market in the Asia-Pacific (APAC) region is growing rapidly due to expanding industries, infrastructure projects, and increasing manufacturing activities. Countries like China and India are heavily investing in transportation systems, urban housing, power plants, ports, and industrial zones. These large construction projects require extensive welding for steel structures, pipelines, and components, resulting in higher demand for electrodes, wires, and fluxes. APAC also hosts major automotive manufacturing hubs in China, Japan, India, South Korea, and Thailand, along with key production sites for appliances and machinery. These industries utilize both automated and manual welding methods, which demand many materials. Additionally, nations are boosting their production of heavy machinery and rail systems.

By Company Type: Tier 1: 25%, Tier 2: 42%, and Tier 3: 33%

By Designation: C-level Executives: 20%, Directors: 30%, and Other Designations: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and Middle East & Africa 20%

Notes: Other designations include sales, marketing, and product managers.

Tier 1: >USD 1 Billion; Tier 2: USD 500 million-1 Billion; and Tier 3: <USD 500 million

Companies Covered: Air Liquide (France), Air Products Inc. (US), ESAB (US), Illinois Tool Works Inc. (US), Linde plc (Germany), Lincoln Electric Holdings Inc. (US), Ador Welding (India), Tianjin Bridge Welding Equipment, Accessories, and Consumables Group Co., Ltd. (China), Kobe Steel Ltd. (Japan), and voestalpine AG (Austria), among others, are included in the report.

The study includes an in-depth competitive analysis of these key players in the welding equipment, accessories, and consumables market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the welding equipment, accessories, and consumables market based on equipment, accessory, consumable, technology, end-use industry, and region. The report's scope includes detailed information about the drivers, restraints, challenges, and opportunities influencing the growth of the welding equipment, accessories, and consumables market. A thorough analysis of key industry players has been conducted to provide insights into their business overview, products offered, and key strategies, such as partnerships, agreements, product launches, expansions, and acquisitions related to the welding equipment, accessories, and consumables market. This report also provides a competitive analysis of emerging startups in the welding equipment, accessories, and consumables market ecosystem.

Reasons to Buy Report

The report will provide market leaders and new entrants with estimates of revenue figures for the overall welding equipment, accessories, and consumables market, including its key subsegments. This report will assist stakeholders in understanding the competitive landscape, gaining insights to better position their businesses, and developing appropriate go-to-market strategies. It will also offer insights into the market's current trends and key factors such as market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

- Analysis of key drivers (expanding steel utilization, automobile innovation and EV expansion, advancements in welding technologies, and increasing demand from end-use industries), restraints (high operational and maintenance costs, and environmental impact of welding), opportunities (developments in Asia Pacific and Middle East & Africa, digitalization and IoT integration, and development of wind energy infrastructure), and challenges (shortage of skilled labor and occupational health risks and intense competition).

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the welding equipment, accessories, and consumables market.

- Market Development: Comprehensive information about profitable markets - the report analyzes the welding equipment, accessories, and consumables market across varied regions.

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the welding equipment, accessories, and consumables market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as Lincoln Electric Holdings, Inc. (US), ESAB (US), Air Liquide (France), Illinois Tool Works Inc. (US), Fronius International GmbH (Austria), and Kemppi Oy (Finland).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 YEARS CONSIDERED

- 1.3.3 INCLUSIONS AND EXCLUSIONS

- 1.3.4 CURRENCY CONSIDERED

- 1.4 LIMITATIONS

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.3 DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.5 RISK ASSESSMENT

- 2.6 GROWTH RATE ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN WELDING EQUIPMENT, ACCESSORIES, AND CONSUMABLES MARKET

- 4.2 WELDING EQUIPMENT, ACCESSORIES, AND CONSUMABLES MARKET: BY ASIA PACIFIC AND CONSUMABLE

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Expanding utilization of steel for welding-intensive industries

- 5.2.1.2 Innovation in automotive and expansion of EV sector

- 5.2.1.3 Advancements in welding technologies driving precision and efficiency

- 5.2.1.4 Increasing demand from diverse end-use industries such as aerospace, rail, maintenance and repair, and marine or shipbuilding

- 5.2.2 RESTRAINTS

- 5.2.2.1 High running and maintenance costs

- 5.2.2.2 Environmental impact of welding

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Developments in Asia Pacific and Middle East & Africa offer opportunities

- 5.2.3.2 Digitalization and IoT integration

- 5.2.3.3 Development of wind energy infrastructure

- 5.2.4 CHALLENGES

- 5.2.4.1 Shortage of skilled labor and occupational health risks

- 5.2.4.2 Intense competition

- 5.2.1 DRIVERS

- 5.3 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.3.1 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.3.2 PRICING ANALYSIS

- 5.3.2.1 Pricing analysis based on welding type, user level, and equipment

- 5.3.2.2 Pricing analysis of consumables

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 VALUE CHAIN ANALYSIS

- 5.6 TARIFF AND REGULATORY LANDSCAPE

- 5.6.1 TARIFF ANALYSIS (HS CODE: 846820)

- 5.6.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.6.3 KEY REGULATIONS

- 5.7 TRADE ANALYSIS

- 5.7.1 EXPORT SCENARIO (HS CODE 846820)

- 5.7.2 IMPORT SCENARIO (HS CODE 846820)

- 5.8 TECHNOLOGY ANALYSIS

- 5.8.1 KEY TECHNOLOGIES

- 5.8.1.1 Unmanned robot welding system

- 5.8.1.2 New welding equipment and tools

- 5.8.1.3 Laser and hybrid welding

- 5.8.2 COMPLEMENTARY TECHNOLOGIES

- 5.8.2.1 Sustainable techniques and materials in welding

- 5.8.2.2 Nanotechnology in welding electrodes

- 5.8.3 ADJACENT TECHNOLOGIES

- 5.8.3.1 Innovations in welding personal protective equipment (PPE)

- 5.8.3.2 Micro welding

- 5.8.1 KEY TECHNOLOGIES

- 5.9 PATENT ANALYSIS

- 5.9.1 INTRODUCTION

- 5.9.2 METHODOLOGY

- 5.9.3 WELDING EQUIPMENT, ACCESSORIES, AND CONSUMABLES MARKET, PATENT ANALYSIS, 2015-2024

- 5.10 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 AUTOMATING WELDING AT LOU-RICH COMPANY FOR ENHANCED EFFICIENCY AND SAFETY

- 5.11.2 MCCORVEY SHEET METAL SOLVES POWER INEFFICIENCIES WITH WELDCOMPUTER TECHNOLOGY

- 5.12 INVESTMENT AND FUNDING SCENARIO

- 5.13 IMPACT OF GEN AI/AI ON WELDING EQUIPMENT, ACCESSORIES, AND CONSUMABLES MARKET

- 5.13.1 INTRODUCTION

- 5.14 PORTER'S FIVE FORCES ANALYSIS

- 5.14.1 THREAT OF NEW ENTRANTS

- 5.14.2 THREAT OF SUBSTITUTES

- 5.14.3 BARGAINING POWER OF SUPPLIERS

- 5.14.4 BARGAINING POWER OF BUYERS

- 5.14.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.15 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.15.2 BUYING CRITERIA

- 5.16 MACROECONOMIC ANALYSIS

- 5.16.1 INTRODUCTION

- 5.16.2 GDP TRENDS AND FORECASTS

- 5.17 IMPACT OF 2025 US TARIFF ON WELDING EQUIPMENT, ACCESSORIES, AND CONSUMABLES MARKET

- 5.17.1 INTRODUCTION

- 5.17.2 KEY TARIFF RATES

- 5.17.3 PRICE IMPACT ANALYSIS

- 5.17.4 IMPACT ON COUNTRY/REGION

- 5.17.4.1 US

- 5.17.4.2 Asia Pacific

- 5.17.4.3 Europe

- 5.17.5 END-USE INDUSTRY IMPACT

6 WELDING EQUIPMENT, ACCESSORIES, AND CONSUMABLES MARKET, BY EQUIPMENT

- 6.1 INTRODUCTION

- 6.2 ELECTRODE & FILLER MATERIAL EQUIPMENT

- 6.2.1 EASE OF CREATING STRONGER JOINTS TO BOOST MARKET

- 6.2.1.1 GMAW/ MIG welding guns

- 6.2.1.2 Welding torches

- 6.2.1.3 TIG welding torches

- 6.2.1.4 Subarc (SAW) welding tractors and torches

- 6.2.1.5 Other welding torches

- 6.2.1.6 Stick electrode holders

- 6.2.1.7 Others

- 6.2.1 EASE OF CREATING STRONGER JOINTS TO BOOST MARKET

- 6.3 OXY-FUEL GAS EQUIPMENT

- 6.3.1 LOW EQUIPMENT COSTS TO LEAD TO HIGH DEMAND

- 6.4 LASER EQUIPMENT

- 6.4.1 HIGH PRECISION OF PROCESS AND EFFICIENCY TO DRIVE MARKET GROWTH

- 6.5 OTHER EQUIPMENT

7 WELDING EQUIPMENT, ACCESSORIES, AND CONSUMABLES MARKET, BY ACCESSORY

- 7.1 INTRODUCTION

- 7.2 GAS REGULATORS

- 7.2.1 SAFETY TO BOOST MARKET

- 7.3 GAS FLOW METERS

- 7.3.1 MEASUREMENT OF SUPPLY OF GASES AND FLUIDS TO INCREASE DEMAND

- 7.4 GAS FILTERS

- 7.4.1 PREVENTION OF DAMAGE TO SOLENOIDS AND GUNS FOR WELDING METALS TO BOOST MARKET

- 7.5 CHECK VALVES

- 7.5.1 PREVENTION OF REVERSE FLOW OF GASES OR LIQUIDS TO DRIVE GROWTH

- 7.6 GAS MANIFOLDS

- 7.6.1 CENTRALIZED DISTRIBUTION OF GASES TO FUEL MARKET

- 7.7 FLOW CONTROLLERS

- 7.7.1 ENSURING REQUIRED OUTPUT AND COST-EFFECTIVENESS TO PROPEL MARKET

- 7.8 GAS PANELS

- 7.8.1 DEMAND FOR NON-CORROSIVE AND LOW FLOW RATE GASES TO FUEL GROWTH

- 7.9 GAS CABINETS

- 7.9.1 PROTECTION FROM ACCIDENTS CAUSED BY TOXIC, CORROSIVE, AND FLAMMABLE GAS LEAKS TO SUPPORT GROWTH

- 7.10 PROTECTIVE GEAR

- 7.10.1 PROTECTION OF WELDING PROFESSIONALS TO DRIVE GROWTH

- 7.11 FUME EXTRACTION EQUIPMENT

- 7.11.1 PREVENTION OF OCCUPATIONAL ILLNESSES TO LEAD TO MARKET GROWTH

8 WELDING EQUIPMENT, ACCESSORIES, AND CONSUMABLES MARKET, BY CONSUMABLE

- 8.1 INTRODUCTION

- 8.2 ELECTRODES & FILLER MATERIALS

- 8.2.1 ECONOMICAL AND USE ON WIDE RANGE OF METALS TO BOOST MARKET

- 8.3 FLUXES & WIRES

- 8.3.1 SHIELDING WELDS FROM ATMOSPHERE FOR PREVENTION OF OXIDATION TO FUEL MARKET

- 8.3.2 TUBULAR WIRE

- 8.3.3 METAL CORED

- 8.3.4 FLUX CORED

- 8.3.5 TUBULAR SUBARC

- 8.3.6 TUBULAR STAINLESS

- 8.3.7 TUBULAR HARDFACING

- 8.3.8 SOLID WIRES

- 8.3.9 MILD STEEL SOLID WIRE (MIG)

- 8.3.10 MILD STEEL SOLID WIRE (TIG)

- 8.3.11 SOLID WIRE SUB ARC

- 8.3.12 STAINLESS STEEL (MIG)

- 8.3.13 STAINLESS STEEL (TIG)

- 8.3.14 ALUMINUM (MIG)

- 8.3.15 ALUMINUM (TIG)

- 8.4 GASES

- 8.4.1 PROTECTION OF MOLTEN METALS FROM CONTAMINATION AND OXIDATION TO PROPEL MARKET

- 8.4.2 SHIELDING GASES

- 8.4.3 OXY-FUEL GASES

9 WELDING EQUIPMENT, ACCESSORIES, AND CONSUMABLES MARKET, BY TECHNOLOGY

- 9.1 INTRODUCTION

- 9.2 ARC WELDING

- 9.2.1 RISING DEMAND DUE TO HIGH PERFORMANCE TO DRIVE MARKET

- 9.3 OXY-FUEL WELDING

- 9.3.1 INCREASING DEMAND IN PLACES WITHOUT ACCESS TO ELECTRICITY TO BOOST MARKET

- 9.4 OTHER TECHNOLOGIES

10 WELDING EQUIPMENT, ACCESSORIES, AND CONSUMABLES MARKET, BY END-USE INDUSTRY

- 10.1 INTRODUCTION

- 10.2 HEAVY EQUIPMENT/EARTH MOVING EQUIPMENT

- 10.2.1 INCREASED SPENDING ON INFRASTRUCTURE AND MINING PROJECTS TO DRIVE MARKET

- 10.3 TRUCKS & TRAILERS

- 10.3.1 INCREASING FREIGHT TRANSPORTATION THROUGH TRAILERS TO BOOST MARKET

- 10.4 GENERAL MANUFACTURING

- 10.4.1 DURABLE, COST-EFFICIENT PRODUCTION OF CONSUMER AND INDUSTRIAL PRODUCTS TO FUEL MARKET

- 10.5 AUTOMOTIVE

- 10.5.1 GROWTH IN EV ADOPTION TO PROPEL MARKET

- 10.6 RAIL

- 10.6.1 GOVERNMENT SPENDING ON IMPROVING RAIL INFRASTRUCTURE TO SUPPORT MARKET GROWTH

- 10.7 TANKS & PRESSURE VESSELS

- 10.7.1 INCREASING DEMAND FOR SAFETY IN CHEMICAL AND ENERGY STORAGE TO LEAD TO MARKET GROWTH

- 10.8 AEROSPACE

- 10.8.1 EXPANSION OF AIR TRAFFIC, DEFENSE PROCUREMENT, AND AIRCRAFT MAINTENANCE, REPAIR, AND OVERHAUL PROGRAMS TO BOOST GROWTH

- 10.9 MARINE & SHIPBUILDING

- 10.9.1 GROWTH IN SHIPBUILDING IN ASIA PACIFIC REGION TO DRIVE MARKET

- 10.10 CONSTRUCTION & INFRASTRUCTURE

- 10.10.1 RISING CONSTRUCTION ACTIVITIES IN EMERGING ECONOMIES TO FUEL MARKET GROWTH

- 10.11 OIL & GAS

- 10.11.1 RISING OIL OUTPUT TO DRIVE MARKET DEMAND

- 10.12 POWER GENERATION

- 10.12.1 ACCELERATING POWER GENERATION EXPANSION AND UPGRADES TO PROPEL MARKET GROWTH

- 10.13 PIPELINES

- 10.13.1 INCREASING PIPELINE INSTALLATIONS TO ENCOURAGE MARKET GROWTH

- 10.14 MAINTENANCE & REPAIR

- 10.14.1 DEMAND ACROSS INDUSTRIES TO DRIVE MARKET GROWTH

11 WELDING EQUIPMENT, ACCESSORIES, AND CONSUMABLES MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 ASIA PACIFIC

- 11.2.1 CHINA

- 11.2.1.1 Increasing urbanization to drive demand

- 11.2.2 JAPAN

- 11.2.2.1 Increasing production of hybrid and electric vehicles to boost market

- 11.2.3 INDIA

- 11.2.3.1 High demand from automobile and construction sectors to fuel market growth

- 11.2.4 AUSTRALIA

- 11.2.4.1 Demand from metal fabrication, shipping, and construction sectors to support market growth

- 11.2.5 REST OF ASIA PACIFIC

- 11.2.1 CHINA

- 11.3 NORTH AMERICA

- 11.3.1 US

- 11.3.1.1 Demand from automobile, aerospace, oil & gas, and telecommunications sectors to fuel market growth

- 11.3.2 CANADA

- 11.3.2.1 Large automobile industry to drive market growth

- 11.3.3 MEXICO

- 11.3.3.1 Increasing investments in infrastructure to propel market

- 11.3.1 US

- 11.4 EUROPE

- 11.4.1 GERMANY

- 11.4.1.1 Increasing wind turbine installations, investments in automobile production facilities, and growing infrastructure to boost market

- 11.4.2 UK

- 11.4.2.1 Growth of automotive sector to offer lucrative opportunities

- 11.4.3 FRANCE

- 11.4.3.1 Increasing foreign investments in various end-use industries to drive market

- 11.4.4 ITALY

- 11.4.4.1 Vast construction industry to drive market

- 11.4.5 REST OF EUROPE

- 11.4.1 GERMANY

- 11.5 MIDDLE EAST & AFRICA

- 11.5.1 GCC COUNTRIES

- 11.5.1.1 Saudi Arabia

- 11.5.1.1.1 Government initiatives and Vision 2030 projects to drive market

- 11.5.1.2 UAE

- 11.5.1.2.1 Robust economic growth and expansion of non-oil sectors to boost market

- 11.5.1.3 Rest of GCC countries

- 11.5.1.1 Saudi Arabia

- 11.5.2 SOUTH AFRICA

- 11.5.2.1 Increasing adoption of new-energy vehicles to propel market

- 11.5.3 REST OF MIDDLE EAST & AFRICA

- 11.5.1 GCC COUNTRIES

- 11.6 SOUTH AMERICA

- 11.6.1 BRAZIL

- 11.6.1.1 Rapid urbanization and growing middle-class population to boost market

- 11.6.2 ARGENTINA

- 11.6.2.1 Growth of construction sector and infrastructure development to drive market

- 11.6.3 REST OF SOUTH AMERICA

- 11.6.1 BRAZIL

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 12.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS

- 12.3 MARKET SHARE ANALYSIS, 2024

- 12.4 REVENUE ANALYSIS, 2020-2024

- 12.5 COMPANY VALUATION AND FINANCIAL METRICS

- 12.6 PRODUCT/BRAND COMPARISON

- 12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 12.7.1 STARS

- 12.7.2 EMERGING LEADERS

- 12.7.3 PERVASIVE PLAYERS

- 12.7.4 PARTICIPANTS

- 12.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.7.5.1 Company footprint

- 12.7.5.2 Region footprint

- 12.7.5.3 End-use industry footprint

- 12.7.5.4 Technology footprint

- 12.7.5.5 Consumable footprint

- 12.7.5.6 Equipment footprint

- 12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 12.8.1 PROGRESSIVE COMPANIES

- 12.8.2 RESPONSIVE COMPANIES

- 12.8.3 DYNAMIC COMPANIES

- 12.8.4 STARTING BLOCKS

- 12.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 12.8.5.1 Detailed list of key startups/SMEs, 2024

- 12.8.5.2 Competitive benchmarking of key startups/SMEs

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 DEALS

- 12.9.2 PRODUCT LAUNCHES

- 12.9.3 EXPANSIONS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 THE LINCOLN ELECTRIC COMPANY

- 13.1.1.1 Business overview

- 13.1.1.2 Products/Solutions/Services offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Product launches

- 13.1.1.3.2 Deals

- 13.1.1.4 MnM view

- 13.1.1.4.1 Right to win

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses and competitive threats

- 13.1.2 ESAB

- 13.1.2.1 Business overview

- 13.1.2.2 Products/Solutions/Services offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Product launches

- 13.1.2.3.2 Deals

- 13.1.2.4 MnM view

- 13.1.2.4.1 Right to win

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses and competitive threats

- 13.1.3 ILLINOIS TOOL WORKS INC.

- 13.1.3.1 Business overview

- 13.1.3.2 Products/Solutions/Services offered

- 13.1.3.3 MnM view

- 13.1.3.3.1 Right to win

- 13.1.3.3.2 Strategic choices

- 13.1.3.3.3 Weaknesses and competitive threats

- 13.1.4 FRONIUS INTERNATIONAL GMBH

- 13.1.4.1 Business overview

- 13.1.4.2 Products/Solutions/Services offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Product launches

- 13.1.4.4 MnM view

- 13.1.4.4.1 Right to win

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses and competitive threats

- 13.1.5 KEMPPI OY

- 13.1.5.1 Business overview

- 13.1.5.2 Products/Solutions/Services offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Product launches

- 13.1.5.4 MnM view

- 13.1.5.4.1 Right to win

- 13.1.5.4.2 Strategic choices

- 13.1.5.4.3 Weaknesses and competitive threats

- 13.1.6 PANASONIC HOLDINGS CORPORATION

- 13.1.6.1 Business overview

- 13.1.6.2 Products/Solutions/Services offered

- 13.1.6.3 MnM view

- 13.1.7 DAIHEN CORPORATION

- 13.1.7.1 Business overview

- 13.1.7.2 Products/Solutions/Services offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Deals

- 13.1.7.4 MnM view

- 13.1.8 AIR LIQUIDE

- 13.1.8.1 Business overview

- 13.1.8.2 Products/Solutions/Services offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Expansions

- 13.1.8.4 MnM view

- 13.1.9 VOESTALPINE AG

- 13.1.9.1 Business overview

- 13.1.9.2 Products/Solutions/Services offered

- 13.1.9.3 Recent developments

- 13.1.9.3.1 Product launches

- 13.1.9.3.2 Deals

- 13.1.9.3.3 Expansions

- 13.1.9.4 MnM view

- 13.1.10 SHENZHEN MEGMEET ELECTRIC CO., LTD.

- 13.1.10.1 Business overview

- 13.1.10.2 Products/Solutions/Services offered

- 13.1.10.3 Recent developments

- 13.1.10.3.1 Product launches

- 13.1.10.3.2 Deals

- 13.1.10.3.3 Expansions

- 13.1.10.4 MnM view

- 13.1.1 THE LINCOLN ELECTRIC COMPANY

- 13.2 OTHER PLAYERS

- 13.2.1 PRECISION CASTPARTS CORP.

- 13.2.2 HYUNDAI WELDING CO.

- 13.2.3 ADOR WELDING

- 13.2.4 ATLANTIC CHINA WELDING CONSUMABLES

- 13.2.5 OBARA GROUP INC.

- 13.2.6 AMADA WELD TECH

- 13.2.7 SWAGELOK COMPANY

- 13.2.8 FORTIUS METALS

- 13.2.9 CARL CLOOS SCHWEISSTECHNIK GMBH

- 13.2.10 ROCKMOUNT

- 13.2.11 WELDFAST ELECTRODES PVT. LTD.

- 13.2.12 D&H SECHERON

- 13.2.13 GEDIK WELDING

- 13.2.14 SUPERON SCHWEISSTECHNIK INDIA

- 13.2.15 NEXA WELD

14 ADJACENT & RELATED MARKET

- 14.1 INTRODUCTION

- 14.2 ROBOTIC WELDING MARKET

- 14.2.1 MARKET DEFINITION

- 14.2.2 MARKET OVERVIEW

- 14.2.3 ROBOTIC WELDING MARKET, BY TYPE

- 14.2.4 ROBOTIC WELDING MARKET, BY PAYLOAD

- 14.2.5 ROBOTIC WELDING MARKET, BY END USER

- 14.2.6 ROBOTIC WELDING MARKET, BY REGION

15 APPENDIX

- 15.1 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.2 CUSTOMIZATION OPTIONS

- 15.3 RELATED REPORTS

- 15.4 AUTHOR DETAILS