|

시장보고서

상품코드

1830048

방사성 리간드 요법(RLT) 시장 : 제품별, 표적별, 적응증별, 최종사용자별, 지역별 - 예측(-2035년)Radioligand Therapy (RLT) Market by Product (Lutetium-177 Vipivotide Tetraxetan, (Lu-177)- PNT2002, Radium-223 dichloride), Target (PSMA, SSTR, Bone Metastases), Indication (Prostate Cancer, Neuroendocrine Tumors (NETS), SCLC) - Global Forecast to 2035 |

||||||

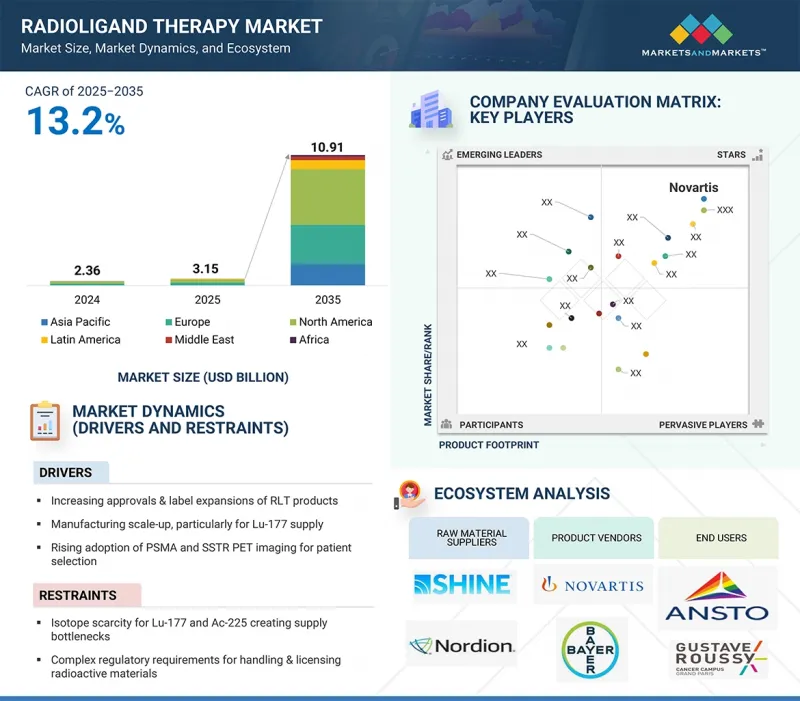

세계의 방사성 리간드 요법 시장 규모는 2025년 31억 5,000만 달러에서 2035년에는 109억 1,000만 달러에 이르고, 예측 기간 중 연평균 복합 성장률(CAGR)은 13.2%를 보일 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2024-2035년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2035년 |

| 검토 단위 | 금액(10억 달러) |

| 부문별 | 제품별, 표적별, 적응증별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

방사성 리간드 요법 시장의 성장은 RLT 제품 승인 및 라벨 확대, 제조 규모 확대(특히 Lu-177 공급), 환자 선택을 위한 PSMA 및 SSTR PET 이미징의 채택 증가, 환자 접근성 확대를 뒷받침하는 상환 범위 확대가 주요 요인으로 작용할 것으로 예측됩니다.

표적별로 시장은 전립선 특이적 막 항원(PSMA), 소마토스타틴 수용체(SSTR), 기타로 분류됩니다. 전립선 특이적 막 항원(PSMA) 부문은 2024년 시장에서 가장 큰 점유율을 차지했습니다. 이 부문의 큰 점유율은 전립선암 세포에서 높은 발현과 정상 조직에서 최소한의 존재에 기인합니다. 따라서 PSMA는 정밀 종양학에 이상적인 바이오마커로 정확한 환자 선별과 효과적인 치료를 가능하게 합니다. 특히 전이성 거세저항성 전립선암(mCRPC)의 경우, 플루빅토(루테튬-177 비피보타이드 테트락세탄)와 같은 PSMA를 표적으로 하는 치료제의 성공으로 그 우위가 더욱 강화되고 있습니다.

제품별로는 Lutetium-177 Vipivotide Tetraxetan,Lutetium-177 Dotatate,Radium-223 Dichloride,(LU-177)-PNT2002,225AC-PSMA-617,FPI-2265/225 ACPSMA-I&T,I-131-1095,TLX591(177LU Rosopatamab Tetraxetan),Alphamedix(212PB-DOTAMTATE),67CU-SAR-BISPSMA 등으로 구분됩니다. 2024년에는 루테튬-177 비피보타이드 테트라세탄 부문이 가장 큰 시장 점유율을 차지했습니다. 노바티스가 개발 및 상용화한 루테튬-177 비피보타이드 테트락세탄(성분명: 플루빅토)은 전립선암 세포에서 고도로 발현되는 단백질인 전립선특이적 막항원(PSMA)을 표적으로 하는 전이성 거세저항성 전립선암(mCRPC) 환자를 위한 정밀치료제입니다. FDA와 EMA의 승인 이후, 이 치료법은 치료 옵션이 제한적인 환자들의 생존 기간을 연장하고 삶의 질을 개선하는 능력으로 인해 널리 채택되고 있습니다. 루테튬177을 사용하면 표적화된 베타선 조사가 가능하여 종양을 최대한 억제하면서 주변의 건강한 조직을 보존할 수 있습니다.

지역별로는 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카로 나뉩니다. 아시아태평양은 예측 기간 동안 가장 높은 CAGR로 성장할 것으로 예측됩니다. 시장 성장의 주요 요인으로는 암 발병률 증가, 의료 인프라 개선, 정밀 종양학 솔루션의 인지도 향상 등을 꼽을 수 있습니다. 중국, 일본, 한국, 인도, 호주 등의 국가에서 핵의학 도입이 확대되고 있으며, 이는 진단 능력의 확대와 예후 진단에 대한 투자로 뒷받침되고 있습니다. 정부 및 민간 기관은 동위원소 생산 시설에 적극적으로 투자하고 있으며, 루테튬-177 및 악티늄 연-225와 같이 상용화된 RLT 제품 및 파이프라인 RLT 제품에 필수적인 주요 동위원소의 수년간공급 부족 문제를 해결하고 있습니다. 이 지역의 규제 당국도 방사성의약품의 승인에 적극적이어서 임상 개발 및 환자 접근성을 높이는 데 유리한 환경을 조성하고 있습니다.

세계의 방사성 리간드 요법(RLT) 시장에 대해 조사했으며, 제품별/표적별/적응증별/최종사용자별/지역별 동향, 시장 진출기업 프로파일 등의 정보를 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 프리미엄 인사이트

제5장 시장 개요

- 서론

- 시장 역학

- 고객의 비즈니스에 영향을 미치는 동향/혼란

- 가격 분석

- 밸류체인 분석

- 생태계 분석

- 투자 및 자금조달 시나리오

- 기술 분석

- 2025-2027년 주요 컨퍼런스 및 이벤트

- 규제 상황

- Porter의 Five Forces 분석

- 주요 이해관계자와 구입 프로세스

- 거시경제 지표

- 파이프라인 분석

- 미충족 요구와 공백

- AI/생성형 AI가 방사성 리간드 치료 시장에 미치는 영향

- 2025년 미국 관세의 영향

제6장 방사성 리간드 요법 시장(제품별)

- 서론

- LUTETIUM 177 VIPIVOTIDE TETRAXETAN

- LUTETIUM-177 DOTATATE

- RADIUM-223 DICHLORIDE

- LU-177 PNT2002

- 225AC-PSMA-617

- FPI-2265

- I-131-1095

- TLX591

- ALPHAMEDIX ( 212PB-DOTAMTATE)

- 67CU-SAR-BISPSMA

- 기타

제7장 방사성 리간드 요법 시장(표적 별)

- 서론

- 전립선 특이적 막 항원

- 소마토스타틴 수용체

- 기타

제8장 방사성 리간드 요법 시장(적응증별)

- 서론

- 전립선암

- 신경내분비 종양

- 기타

제9장 방사성 리간드 요법 시장(최종사용자별)

- 서론

- 삼차 의료 학술/종합 암센터

- 전문 핵의학 센터

- 기타

제10장 방사성 리간드 요법 시장(지역별)

- 서론

- 북미

- 북미의 거시경제 전망

- 미국

- 캐나다

- 유럽

- 유럽의 거시경제 전망

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타

- 아시아태평양

- 아시아태평양의 거시경제 전망

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타

- 라틴아메리카

- 라틴아메리카의 거시경제 전망

- 브라질

- 멕시코

- 기타 라틴아메리카

- 중동

- 중동의 거시경제 전망

- GCC 국가

- 사우디아라비아

- 아랍에미리트

- 기타 GCC 국가

- 기타 중동 국가

- 아프리카

- 성장을 가속하는 임상시험 에코시스템 강화와 규제 개혁

- 아프리카의 거시경제 전망

제11장 경쟁 구도

- 서론

- 주요 시장 진출기업의 전략/강점

- 주요 시장 진출기업이 채택한 전략 개요

- 매출 분석, 2028년-2030년

- 2030년 시장 점유율 분석

- 기업 평가와 재무 지표

- 브랜드/제품 비교

- 기업 평가 매트릭스 : 주요 시장 진출기업, 2024년

- 기업 평가 매트릭스 : 스타트업/중소기업, 2024년

- 경쟁 시나리오

제12장 기업 개요

- 주요 시장 진출기업

- NOVARTIS AG

- BAYER AG

- CURIUM US LLC

- ELI LILLY AND COMPANY

- ASTRAZENECA

- PROGENICS PHARMACEUTICALS INC.(LANTHEUS)

- ARICEUM THERAPEUTICS

- TELIX PHARMACEUTICALS

- ITM ISOTOPE TECHNOLOGIES

- CONVERGENT THERAPEUTICS, INC.

- ORANO SA

- ACTINIUM PHARMACEUTICALS, INC.

- PERSPECTIVE THERAPEUTICS, INC.

- CLARITY PHARMACEUTICALS

- RADIOPHARM THERANOSTICS LTD.

- 기타 기업

- ALPHA 9 ONCOLOGY

- RATIO THERAPEUTICS

- NORIA THERAPEUTICS

- PRECIRIX

- SOFIE

- ECKERT & ZIEGLER RADIOPHARMA

- NORTHSTAR MEDICAL RADIOISOTOPES, LLC

- IRE-IRE ELIT

- BWXT MEDICAL LTD.

- NTP RADIOISOTOPES

제13장 부록

LSH 25.10.16The global radioligand therapy market is projected to reach USD 10.91 billion by 2035 from an estimated USD 3.15 billion in 2025, at a CAGR of 13.2% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2035 |

| Base Year | 2024 |

| Forecast Period | 2025-2035 |

| Units Considered | Value (USD billion) |

| Segments | By Product, Target, Indication, End User, and Region |

| Regions covered | North America, Europe, the Asia Pacific, Latin America, the Middle East, and Africa |

The growth of the radioligand therapy market is majorly driven by increasing approvals and label expansions of RLT products, manufacturing scale-up, particularly for Lu-177 supply, rising adoption of PSMA and SSTR PET imaging for patient selection, and expanding reimbursement coverage supporting broader patient access.

By target, the prostate-specific membrane antigen segment accounted for the largest market share in 2024.

Based on target, the market is categorized into Prostate-Specific Membrane Antigen (PSMA), Somatostatin Receptor (SSTR), and other targets. The Prostate-Specific Membrane Antigen (PSMA) segment accounted for the largest share of the market in 2024. The large share of this segment is attributed to its high expression in prostate cancer cells and its minimal presence in normal tissues. This makes PSMA an ideal biomarker for precision oncology, enabling accurate patient selection and effective therapy delivery. The success of PSMA-targeted treatments, such as Pluvicto (lutetium-177 vipivotide tetraxetan), has reinforced its dominance, particularly in metastatic castration-resistant prostate cancer (mCRPC).

By product, the Lutetium-177 vipivotide tetraxetan segment accounted for the largest share of the market in 2024.

By product, the market is segmented into Lutetium-177 Vipivotide Tetraxetan, Lutetium-177 Dotatate, Radium-223 Dichloride, [LU-177]-PNT2002, 225AC-PSMA-617, FPI-2265/ 225 AC PSMA - I&T, I-131-1095, TLX591 (177LU Rosopatamab Tetraxetan), Alphamedix (212PB-DOTAMTATE), 67CU-SAR-BISPSMA, and other products. In 2024, the lutetium-177 vipivotide tetraxetan segment accounted for the largest share of the market. Developed and commercialized by Novartis, Lutetium-177 vipivotide tetraxetan (Pluvicto) targets Prostate-Specific Membrane Antigen (PSMA), a protein highly expressed in prostate cancer cells, making it a precision therapy for patients with metastatic castration-resistant prostate cancer (mCRPC). Since its FDA and EMA approvals, the therapy has become widely adopted due to its ability to extend survival and improve quality of life in patients with limited treatment options. Its use of lutetium-177 enables targeted beta radiation delivery, sparing surrounding healthy tissues while maximizing tumor control.

By region, the Asia Pacific market is projected to grow at the highest CAGR during the forecast period.

The market is segmented by region into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The Asia Pacific region is projected to grow at the highest CAGR during the forecast period. The key factors contributing to market growth include the rising cancer incidence, improvements in healthcare infrastructure, and increasing awareness of precision oncology solutions. Countries such as China, Japan, South Korea, India, and Australia are witnessing the growing adoption of nuclear medicine, which is supported by expanding diagnostic capabilities and investments in theragnostic. Governments & private institutions are actively investing in isotope production facilities, addressing long-standing supply challenges for key isotopes like lutetium-177 and actinium-225, essential for commercialized and pipeline RLT products. Regulatory authorities in the region also show greater receptivity to radiopharmaceutical approvals, creating a favourable environment for clinical development and faster patient access.

The primary interviews conducted for this report can be categorized as follows:

- By Respondent: Supply Side- 70% and Demand Side- 30%

- By Designation: Managers- 45%, CXO and Directors- 30%, and Executives- 25%

- By Region: North America- 30%, Europe- 30%, Asia Pacific- 30%, Latin America- 5%, and the Middle East & Africa- 5%

Key Companies

The key players in the radioligand therapy market include Novartis AG (Switzerland), Bayer AG (Germany), Curium US LLC (US), Eli Lilly and Company (US), AstraZeneca plc (UK), Progenics Pharmaceuticals, Inc. (US), Ariceum Therapeutics GmbH (Germany), Telix Pharmaceuticals Limited (Australia), ITM Isotope Technologies Munich SE (Germany), Convergent Therapeutics, Inc. (US), Orano Med SAS (France), Actinium Pharmaceuticals, Inc. (US), Perspective Therapeutics, Inc. (US), Clarity Pharmaceuticals Ltd. (Australia), and Radiopharm Theranostics Ltd. (Australia), among others.

Research Coverage

This research report categorizes the radioligand therapy market, by product [Lutetium-177 vipivotide tetraxetan, LUTETIUM-177 DOTATATE, Radium-223 dichloride, (LU-177)-PNT2002, 225AC-PSMA-617, FPI-2265/ 225 AC PSMA - I&T, I-131-1095, TLX591 (177LU ROSOPATAMAB TETRAXETAN), ALPHAMEDIX (212PB-DOTAMTATE), 67CU-SAR-BISPSMA, and other products), target (PSMA, SSTR, and other targets), indication (prostate cancer, neuroendocrine tumors, and other indications), and end user (tertiary care academic/comprehensive cancer centers, specialized nuclear medicine centers, and other end user), and region (North America, Europe, the Asia Pacific, Latin America, the Middle East & Africa).

The report's scope covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the radioligand therapy market. A thorough analysis of the key industry players has provided insights into their business overview, products, solutions, key strategies, collaborations, partnerships, and agreements: new approvals/launches, collaborations, acquisitions, and recent developments associated with the radioligand therapy market.

Reasons to buy this report

The report will help market leaders and new entrants by providing the closest approximations of the revenue numbers for the radioligand therapy market and its subsegments. It will also help stakeholders better understand the competitive landscape and gain more insights to position their businesses better and make suitable go-to-market strategies. This report will enable stakeholders to understand the market's pulse and provide them with information on the key market drivers, restraints, opportunities, and challenges.

The report provides insights into the following pointers:

- Analysis of key drivers (increasing approvals and label expansions of RLT products, manufacturing scale-up, particularly for Lu-177 supply, the rising adoption of PSMA and SSTR PET imaging for patient selection. Expanding reimbursement coverage supporting broader patient access), restraints (Isotope scarcity for Lu-177 and Ac-225 creating supply bottlenecks, complex regulatory requirements for handling & licensing radioactive materials, logistical hurdles & half-life constraints limiting distribution), opportunities [advancements of alpha therapies (Ac-225, Pb-212) with strong clinical potential, expansion into earlier-line and adjuvant use, broadening eligible populations, combination regimens with immuno-oncology, PARP inhibitors, and other targeted agents), and challenges (reactor outages and geopolitical risks impacting isotope production & supply chains and the growing competition from alternative modalities such as ADCs and bispecific antibodies)

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities in the radioligand therapy market

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about untapped geographies, recent developments, and investments in the radioligand therapy market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players. A detailed analysis of the key industry players has been done to provide insights into their key strategies, product launches/approvals, acquisitions, partnerships, agreements, collaborations, other recent developments, investment & funding activities, brand/product comparative analysis, and vendor valuation & financial metrics of the radioligand therapy market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Objectives of secondary research

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Breakdown of primaries

- 2.1.2.2 Key objectives of primary research

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 GLOBAL MARKET ESTIMATION

- 2.2.1.1 Company revenue analysis (Bottom-up approach)

- 2.2.1.2 Revenue share analysis

- 2.2.1.3 MnM repository analysis

- 2.2.1.4 Primary interviews

- 2.2.2 INSIGHTS FROM PRIMARY EXPERTS

- 2.2.3 SEGMENTAL MARKET SIZE ESTIMATION (TOP-DOWN APPROACH)

- 2.2.1 GLOBAL MARKET ESTIMATION

- 2.3 GROWTH RATE PROJECTIONS

- 2.4 DATA TRIANGULATION

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

- 2.7 RISK ANALYSIS

3 EXECUTIVE SUMMARY

- 3.1 STRATEGIC IMPERATIVES FOR KEY STAKEHOLDERS

- 3.1.1 BIOTECH STARTUPS AND INNOVATIVE COMPANIES

- 3.1.2 ESTABLISHED MARKET LEADERS

- 3.1.3 CDMOS AND CROS

4 PREMIUM INSIGHTS

- 4.1 RADIOLIGAND THERAPY MARKET OVERVIEW

- 4.2 NORTH AMERICA: RADIOLIGAND THERAPY MARKET, BY PRODUCT AND COUNTRY, 2025

- 4.3 RADIOLIGAND THERAPY MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 4.4 RADIOLIGAND THERAPY MARKET: EMERGING VS. DEVELOPED MARKETS

- 4.5 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.6 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFT

- 4.7 VC/PRIVATE EQUITY INVESTMENT TRENDS AND STARTUP LANDSCAPE

- 4.8 REGULATORY POLICY INITIATIVES

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Increasing approvals and label expansion of RLT products

- 5.2.1.2 Manufacturing scale-up of Lu-177

- 5.2.1.3 Rising adoption of prostate-specific membrane antigen and somatostatin receptor PET imaging

- 5.2.1.4 Expanding reimbursement coverage

- 5.2.2 RESTRAINTS

- 5.2.2.1 Isotope supply scarcity

- 5.2.2.2 Stringent regulatory requirements

- 5.2.2.3 Logistical hurdles and half-life constraints

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Advancements in alpha therapies

- 5.2.3.2 Expansion of radioligand therapy into earlier-line and adjuvant settings

- 5.2.3.3 Combination regimens integrating radioligand therapy

- 5.2.4 CHALLENGES

- 5.2.4.1 Reactor outages and geopolitical risks

- 5.2.4.2 Growing competition from alternative modalities

- 5.2.1 DRIVERS

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.4 PRICING ANALYSIS

- 5.4.1 INDICATIVE PRICING ANALYSIS, BY KEY PLAYER, 2024

- 5.4.2 INDICATIVE PRICING ANALYSIS, BY REGION

- 5.5 VALUE CHAIN ANALYSIS

- 5.6 ECOSYSTEM ANALYSIS

- 5.7 INVESTMENT AND FUNDING SCENARIO

- 5.8 TECHNOLOGY ANALYSIS

- 5.8.1 KEY TECHNOLOGIES

- 5.8.1.1 Beta-emitting therapeutic radionuclides

- 5.8.1.2 Alpha-emitting therapeutic radionuclides

- 5.8.1.3 Targeting ligands

- 5.8.1.4 Monoclonal antibody-directed radiotherapeutics

- 5.8.2 COMPLEMENTARY TECHNOLOGIES

- 5.8.2.1 SPECT/CT and PET/CT

- 5.8.2.2 Alternative isotopes

- 5.8.3 ADJACENT TECHNOLOGIES

- 5.8.3.1 Antibody drug conjugates

- 5.8.3.2 Bispecific antibodies

- 5.8.1 KEY TECHNOLOGIES

- 5.9 KEY CONFERENCES AND EVENTS, 2025-2027

- 5.10 REGULATORY LANDSCAPE

- 5.10.1 REGULATORY ANALYSIS

- 5.10.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.11 PORTER'S FIVE FORCES ANALYSIS

- 5.11.1 BARGAINING POWER OF SUPPLIERS

- 5.11.2 BARGAINING POWER OF BUYERS

- 5.11.3 THREAT OF NEW ENTRANTS

- 5.11.4 THREAT OF SUBSTITUTES

- 5.11.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.12 KEY STAKEHOLDERS AND BUYING PROCESS

- 5.12.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.12.2 BUYING CRITERIA

- 5.13 MACROECONOMICS INDICATORS

- 5.13.1 HEALTHCARE EXPENDITURE TRENDS

- 5.13.2 GLOBAL CANCER BURDEN

- 5.14 PIPELINE ANALYSIS

- 5.15 UNMET NEEDS AND WHITE SPACES

- 5.16 IMPACT OF AI/GEN AI ON RADIOLIGAND THERAPY MARKET

- 5.16.1 INTRODUCTION

- 5.16.2 MARKET POTENTIAL OF AI IN RADIOLIGAND THERAPY APPLICATIONS

- 5.16.3 AI USE CASES

- 5.17 IMPACT OF 2025 US TARIFF

- 5.17.1 INTRODUCTION

- 5.17.2 KEY TARIFF RATES

- 5.17.3 PRICE IMPACT ANALYSIS

- 5.17.4 IMPACT ON COUNTRY/REGION

- 5.17.4.1 US

- 5.17.4.2 Europe

- 5.17.4.3 Asia Pacific

- 5.17.4.4 Rest of the World

- 5.17.5 IMPACT ON MANUFACTURING INDUSTRY

6 RADIOLIGAND THERAPY MARKET, BY PRODUCT

- 6.1 INTRODUCTION

- 6.2 LUTETIUM 177 VIPIVOTIDE TETRAXETAN

- 6.2.1 BROADER REGULATORY ACCEPTANCE AND EXPANDING PAYER COVERAGE TO AID GROWTH

- 6.3 LUTETIUM-177 DOTATATE

- 6.3.1 INCREASING RECOGNITION OF LUTETIUM-177 DOTATATE IN TREATING GASTROENTEROPANCREATIC NEUROENDOCRINE TUMORS TO BOOST MARKET

- 6.4 RADIUM-223 DICHLORIDE

- 6.4.1 INCREASING ADOPTION OF RADIUM-223 DICHLORIDE IN EMERGING MARKETS TO STIMULATE GROWTH

- 6.5 LU-177 PNT2002

- 6.5.1 STRONG PHASE III CLINICAL VALIDATION AND STRATEGIC COMMERCIALIZATION PARTNERSHIPS TO SPUR GROWH

- 6.6 225AC-PSMA-617

- 6.6.1 POTENT THERAPEUTIC PROFILE AND EXPANDING CLINICAL VALIDATION TO BOLSTER GROWTH

- 6.7 FPI-2265

- 6.7.1 EARLY RESPONSE DATA AND SAFETY REASSURANCE TO AMPLIFY GROWTH

- 6.8 I-131-1095

- 6.8.1 FAVORABLE DOSIMETRY AND SAFETY PROFILES TO SUSTAIN GROWTH

- 6.9 TLX591

- 6.9.1 SIMPLIFIED DOSING REGIMEN AND FAVORABLE TOLERABILITY TO DRIVE MARKET

- 6.10 ALPHAMEDIX ( 212PB-DOTAMTATE)

- 6.10.1 ROBUST EARLY-PHASE EFFICACY AND STRONG COMMERCIALIZATION TO SUPPORT GROWTH

- 6.11 67CU-SAR-BISPSMA

- 6.11.1 ENHANCED LESION UPTAKE & RETENTION AND FAVORABLE TOLERABILITY PROFILE TO FOSTER GROWTH

- 6.12 OTHER PRODUCTS

7 RADIOLIGAND THERAPY MARKET, BY TARGET

- 7.1 INTRODUCTION

- 7.2 PROSTATE-SPECIFIC MEMBRANE ANTIGEN

- 7.2.1 STRONG BIOLOGICAL RATIONALE, ROBUST CLINICAL OUTCOMES, AND RAPID SCALING OF GLOBAL SUPPLY CHAINS TO PROMOTE GROWTH

- 7.3 SOMATOSTATIN RECEPTOR

- 7.3.1 PROVEN EFFICACY IN TREATING NEUROENDOCRINE TUMORS TO EXPEDITE GROWTH

- 7.4 OTHER TARGETS

8 RADIOLIGAND THERAPY MARKET, BY INDICATION

- 8.1 INTRODUCTION

- 8.2 PROSTATE CANCER

- 8.2.1 EXPANDING TREATMENT POPULATIONS AND CLINICAL VALIDATION TO ENCOURAGE GROWTH

- 8.3 NEUROENDOCRINE TUMORS

- 8.3.1 REGULATORY ADVANCEMENTS AND STRATEGIC INDUSTRY MOVES TO FACILITATE GROWTH

- 8.4 OTHER INDICATIONS

9 RADIOLIGAND THERAPY MARKET, BY END USER

- 9.1 INTRODUCTION

- 9.2 TERTIARY CARE ACADEMIC/COMPREHENSIVE CANCER CENTERS

- 9.2.1 ADVANCED TREATMENT DELIVERY AND CLINICAL TRIAL CAPABILITIES TO CONTRIBUTE TO GROWTH

- 9.3 SPECIALIZED NUCLEAR MEDICINE CENTERS

- 9.3.1 HIGHLY TRAINED PERSONNEL AND TARGETED FACILITIES TO ACCELERATE GROWTH

- 9.4 OTHER END USERS

10 RADIOLIGAND THERAPY MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 10.2.2 US

- 10.2.2.1 Robust ecosystem of biotech innovation and strong academic-industry collaboration to spur growth.

- 10.2.3 CANADA

- 10.2.3.1 Growing clinical trial momentum to drive market

- 10.3 EUROPE

- 10.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 10.3.2 GERMANY

- 10.3.2.1 Strong clinical advancements and active industry partnerships to foster growth.

- 10.3.3 UK

- 10.3.3.1 Growing efforts for decentralized access and innovations to boost market

- 10.3.4 FRANCE

- 10.3.4.1 Strong nuclear medicine manufacturing and isotope supply foundation to bolster growth

- 10.3.5 ITALY

- 10.3.5.1 Rising preclinical exploration and early discovery stages to stimulate growth

- 10.3.6 SPAIN

- 10.3.6.1 Established nuclear-medicine departments and authorized radiopharmacy frameworks to aid growth

- 10.3.7 REST OF EUROPE

- 10.4 ASIA PACIFIC

- 10.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 10.4.2 CHINA

- 10.4.2.1 Favorable regulatory reforms and expanding hospital-based nuclear medicine capabilities to amplify growth

- 10.4.3 JAPAN

- 10.4.3.1 Academic excellence, manufacturing expansion, and supportive regulation to contribute to growth

- 10.4.4 INDIA

- 10.4.4.1 Lower trial costs and skilled medical professionals to accelerate growth

- 10.4.5 SOUTH KOREA

- 10.4.5.1 Growing emphasis on nuclear medicine innovation to propel market

- 10.4.6 AUSTRALIA

- 10.4.6.1 Need to maintain high standards of quality, compliance, and innovation to facilitate growth

- 10.4.7 REST OF ASIA PACIFIC

- 10.5 LATIN AMERICA

- 10.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 10.5.2 BRAZIL

- 10.5.2.1 Favorable educational initiatives and expanding biopharma infrastructure to promote growth

- 10.5.3 MEXICO

- 10.5.3.1 Growing cyclotron capacity to fuel market

- 10.5.4 REST OF LATIN AMERICA

- 10.6 MIDDLE EAST

- 10.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST

- 10.6.2 GCC COUNTRIES

- 10.6.3 SAUDI ARABIA

- 10.6.3.1 Growing initiatives for healthcare and life sciences sectors to drive market

- 10.6.4 UAE

- 10.6.4.1 Emerging biotechnology sector to intensify growth

- 10.6.5 REST OF GCC COUNTRIES

- 10.6.6 REST OF MIDDLE EAST

- 10.7 AFRICA

- 10.7.1 ENHANCED CLINICAL TRIAL ECOSYSTEM AND REGULATORY REFORMS TO AID GROWTH

- 10.7.2 MACROECONOMIC OUTLOOK FOR AFRICA

11 COMPETITIVE LANDSCAPE

- 11.1 INTRODUCTION

- 11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 11.3 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS

- 11.4 REVENUE ANALYSIS, 2028-2030

- 11.5 MARKET SHARE ANALYSIS, 2030

- 11.6 COMPANY VALUATION AND FINANCIAL METRICS

- 11.7 BRAND/PRODUCT COMPARISON

- 11.8 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 11.8.1 STARS

- 11.8.2 EMERGING LEADERS

- 11.8.3 PERVASIVE PLAYERS

- 11.8.4 PARTICIPANTS

- 11.8.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 11.8.5.1 Region footprint

- 11.8.5.2 Target footprint

- 11.8.5.3 Indication footprint

- 11.9 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 11.9.1 PROGRESSIVE COMPANIES

- 11.9.2 RESPONSIVE COMPANIES

- 11.9.3 DYNAMIC COMPANIES

- 11.9.4 STARTING BLOCKS

- 11.9.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 11.9.5.1 Detailed list of key startups/SMEs

- 11.9.5.2 Competitive benchmarking of key startups/SMEs

- 11.10 COMPETITIVE SCENARIO

- 11.10.1 PRODUCT LAUNCHES AND APPROVALS

- 11.10.2 DEALS

- 11.10.3 EXPANSIONS

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 NOVARTIS AG

- 12.1.1.1 Business overview

- 12.1.1.2 Products offered

- 12.1.1.3 Products in pipeline

- 12.1.1.4 Recent developments

- 12.1.1.4.1 Product launches and approvals

- 12.1.1.4.2 Deals

- 12.1.1.4.3 Expansions

- 12.1.1.5 MnM view

- 12.1.1.5.1 Key strengths

- 12.1.1.5.2 Strategic choices

- 12.1.1.5.3 Weaknesses and competitive threats

- 12.1.2 BAYER AG

- 12.1.2.1 Business overview

- 12.1.2.2 Products offered

- 12.1.2.2.1 Deals

- 12.1.2.2.2 Other developments

- 12.1.2.3 MnM view

- 12.1.2.3.1 Key strengths

- 12.1.2.3.2 Strategic choices

- 12.1.2.3.3 Weaknesses and competitive threats

- 12.1.3 CURIUM US LLC

- 12.1.3.1 Business overview

- 12.1.3.2 Products in pipeline

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Deals

- 12.1.3.4 MnM view

- 12.1.3.4.1 Key strengths

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses and competitive threats

- 12.1.4 ELI LILLY AND COMPANY

- 12.1.4.1 Business overview

- 12.1.4.2 Products in pipeline

- 12.1.4.3 Recent developments

- 12.1.4.3.1 Product launches and approvals

- 12.1.4.3.2 Deals

- 12.1.4.4 MnM view

- 12.1.4.4.1 Key strengths

- 12.1.4.4.2 Strategic choices

- 12.1.4.4.3 Weaknesses and competitive threats

- 12.1.5 ASTRAZENECA

- 12.1.5.1 Business overview

- 12.1.5.2 Products in pipeline

- 12.1.5.3 Recent developments

- 12.1.5.3.1 Deals

- 12.1.5.4 MnM view

- 12.1.5.4.1 Key strengths

- 12.1.5.4.2 Strategic choices

- 12.1.5.4.3 Weaknesses and competitive threats

- 12.1.6 PROGENICS PHARMACEUTICALS INC. (LANTHEUS)

- 12.1.6.1 Business overview

- 12.1.6.2 Products in pipeline

- 12.1.6.3 Recent developments

- 12.1.6.3.1 Deals

- 12.1.7 ARICEUM THERAPEUTICS

- 12.1.7.1 Products in pipeline

- 12.1.7.2 Recent developments

- 12.1.7.2.1 Deals

- 12.1.8 TELIX PHARMACEUTICALS

- 12.1.8.1 Business overview

- 12.1.8.2 Products in pipeline

- 12.1.8.3 Recent developments

- 12.1.8.3.1 Deals

- 12.1.8.3.2 Expansions

- 12.1.8.3.3 Other developments

- 12.1.9 ITM ISOTOPE TECHNOLOGIES

- 12.1.9.1 Business overview

- 12.1.9.2 Products offered

- 12.1.9.3 Recent developments

- 12.1.9.3.1 Deals

- 12.1.9.3.2 Expansions

- 12.1.10 CONVERGENT THERAPEUTICS, INC.

- 12.1.10.1 Business overview

- 12.1.10.2 Products in pipeline

- 12.1.10.3 Recent developments

- 12.1.10.3.1 Product launches and approvals

- 12.1.10.3.2 Deals

- 12.1.11 ORANO SA

- 12.1.11.1 Business overview

- 12.1.11.2 Products in pipeline

- 12.1.11.3 Recent developments

- 12.1.11.3.1 Deals

- 12.1.11.3.2 Expansions

- 12.1.12 ACTINIUM PHARMACEUTICALS, INC.

- 12.1.12.1 Business overview

- 12.1.12.2 Products in pipeline

- 12.1.12.3 Recent developments

- 12.1.12.3.1 Product launches and approvals

- 12.1.12.3.2 Deals

- 12.1.13 PERSPECTIVE THERAPEUTICS, INC.

- 12.1.13.1 Business overview

- 12.1.13.2 Products in pipeline

- 12.1.13.3 Recent developments

- 12.1.13.3.1 Deals

- 12.1.14 CLARITY PHARMACEUTICALS

- 12.1.14.1 Business overview

- 12.1.14.2 Products in pipeline

- 12.1.14.3 Recent developments

- 12.1.14.3.1 Deals

- 12.1.14.3.2 Other developments

- 12.1.15 RADIOPHARM THERANOSTICS LTD.

- 12.1.15.1 Business overview

- 12.1.15.2 Products in pipeline

- 12.1.15.3 Recent developments

- 12.1.15.3.1 Deals

- 12.1.1 NOVARTIS AG

- 12.2 OTHER PLAYERS

- 12.2.1 ALPHA 9 ONCOLOGY

- 12.2.2 RATIO THERAPEUTICS

- 12.2.3 NORIA THERAPEUTICS

- 12.2.4 PRECIRIX

- 12.2.5 SOFIE

- 12.2.6 ECKERT & ZIEGLER RADIOPHARMA

- 12.2.7 NORTHSTAR MEDICAL RADIOISOTOPES, LLC

- 12.2.8 IRE- IRE ELIT

- 12.2.9 BWXT MEDICAL LTD.

- 12.2.10 NTP RADIOISOTOPES

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS