|

시장보고서

상품코드

1856026

골반장기탈출증(POP : Pelvic Organ Prolapse) 치료 및 관리 시장 예측(-2030년) : 제품, 치료, 용도, 최종사용자, 지역별POP Treatment and Management / Pelvic Organ Prolapse Market by Product, Treatment, Application, End User, Region - Global Forecast to 2030 |

||||||

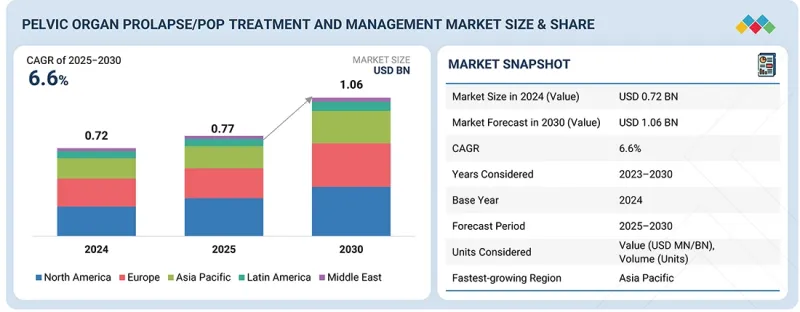

세계의 골반장기탈출증(POP : Pelvic Organ Prolapse) 치료·관리 시장 규모는 2025년 7억 7,000만 달러에서 예측 기간 중 6.6%의 CAGR로 추이하며, 2030년에는 10억 6,000만 달러에 달할 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2024-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 금액(달러) |

| 부문 | 제품, 치료, 용도, 최종사용자 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

세계에서 골반장기탈출증(POP)의 높은 유병률, 고령 여성 인구 증가, 인식 개선 및 조기 진단의 발전, 저침습 및 로봇 보조 수술 기술의 발전으로 이 시장은 향후 큰 성장이 예상됩니다. 한편, 질 메쉬 관련 합병증 및 리콜 문제, 개발도상국의 의료 접근성 및 비용 부담 제약, 사회적 낙인으로 인한 진단 지연, POP 제품의 안전성 위험 등이 시장 성장을 저해하는 요인으로 작용할 수 있습니다.

"최종사용자별로는 병원 부문이 예측 기간 중 가장 큰 점유율을 유지한다."

병원 및 클리닉 부문이 2024년 가장 큰 점유율을 차지했습니다. 병원은 중앙집중식 구매 시스템을 통해 새로운 POP 치료 기술을 효율적으로 도입할 수 있는 장점이 있습니다. 또한 정부-공공기관의 자금 조달을 통해 고가의 로봇수술 시스템 등 첨단 의료기기를 도입하기 쉽다는 점도 강점입니다. 또한 병원은 수술 중 합병증, 복잡한 재건수술, 고령 환자의 동반질환 등에 대응할 수 있는 유일한 의료시설인 경우가 많으며, 이러한 배경에서 POP 치료에서 병원의 우위는 앞으로도 유지될 것으로 보입니다.

"치료별로는 외과적 치료 부문이 시장의 대부분을 차지합니다. "

외과적 치료 부문이 2024년 시장의 대부분을 차지했습니다. 수술적 중재는 다발성 장기탈출증이나 복압성 요실금 등의 합병증이 동반된 경우에 선택되는 경우가 많으며, 최근에는 저침습적 로봇보조수술의 보급으로 회복기간 단축과 수술 후 합병증 감소가 가능해져 환자와 의사 모두 만족할 수 있는 선택이 되고 있습니다. 또한 수술용 메쉬, 생체 이식재, 에너지 지원형 박리장치 등 지속적인 기술 혁신으로 수술 성적 향상에 기여하고 있습니다. 또한 수술적 치료는 임상 가이드라인에서 중등도에서 중증의 POP에 대한 1차 치료법으로 강력히 권장하고 있으며, 시장에서의 우위를 유지하고 있습니다.

"지역별로는 아시아태평양이 가장 빠르게 성장하는 시장"

아시아태평양은 급속한 고령화가 진행되고 있으며, 특히 중국, 일본 등에서 고령 여성의 골반장기탈질환 발병률이 증가하고 있습니다. 또한 여성 건강에 대한 인식 개선과 골반저질환 치료에 대한 수용도가 높아지면서 진단율과 치료율 향상에 힘을 보태고 있습니다. 각국 정부는 의료 인프라에 대한 투자 확대, 수술 시설에 대한 접근성 강화, 로봇 보조 수술을 포함한 첨단 의료 기술 도입 촉진에 적극적입니다. 또한 인도, 한국 등에서의 의료관광 확대도 시장 성장을 더욱 가속화하고 있습니다. 이들 국가에서는 양질의 의료를 저렴한 비용으로 제공할 수 있다는 점이 강점으로 작용하고 있습니다. 한편, 지방의 의료 접근성 격차, 숙련된 의사 부족 등의 과제도 남아있지만, 의료 교육에 대한 투자, 디지털 헬스 도입, 대중 인식 개선 캠페인 등의 노력이 진행되고 있으며, 이러한 격차를 해소할 수 있을 것으로 기대됩니다. 이러한 요인들로 인해 아시아태평양은 세계에서 가장 빠르게 성장하는 POP 치료 및 관리 시장으로 자리매김하고 있습니다.

세계의 골반장기탈출증(POP : Pelvic Organ Prolapse) 치료·관리 시장을 조사했으며, 시장 개요, 시장 성장에 대한 각종 영향요인의 분석, 기술·특허의 동향, 법규제 환경, 사례 연구, 시장 규모 추이·예측, 각종 구분·지역/주요 국가별 상세 분석, 경쟁 구도, 주요 기업의 개요 등을 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 주요 인사이트

제5장 시장 개요

- 시장 역학

- 촉진요인

- 억제요인

- 기회

- 과제

- 고객 사업에 영향을 미치는 동향과 혼란

- 가격 분석

- 밸류체인 분석

- 공급망 분석

- 에코시스템 분석

- 투자와 자금조달 시나리오

- 기술 분석

- 특허 분석

- 무역 분석

- 주요 컨퍼런스와 이벤트

- 사례 연구 분석

- 규제 상황

- Porter's Five Forces 분석

- 주요 이해관계자와 구입 기준

- AI의 영향

- 미국의 2025년 관세

제6장 골반장기탈출증/골반저 재건 시장 : 제품별

- 합성 메시

- 생체 이식재

- 봉합사

- 질 페서리

- 골반저 치료 기기

- 로봇 수술 시스템

- 진단·평가 툴

제7장 골반장기탈출증/골반저 재건 시장 : 치료별

- 외과적 치료

- 폐쇄술

- COLPORRHAPY

- SACROCOLPOPEXY

- SACROHYSTEROPEXY

- 자궁선극·선골인대 고정술

- 비외과적 치료

- 질 페서리 관리

- 골반저근 치료

제8장 골반장기탈출증/골반저 재건 시장 : 용도별

- 방광혹

- 요도혹

- 소장혹

- 자궁탈출

- 직장혹

제9장 골반장기탈출증/골반저 재건 시장 : 최종사용자별

- 병원

- 전문 클리닉

- 외래 수술 센터

- 기타

제10장 골반장기탈출증/골반저 재건 시장 : 지역별

- 북미

- 거시경제 전망

- 미국

- 캐나다

- 유럽

- 거시경제 전망

- 독일

- 프랑스

- 영국

- 이탈리아

- 스페인

- 기타

- 아시아태평양

- 거시경제 전망

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타

- 라틴아메리카

- 거시경제 전망

- 브라질

- 멕시코

- 기타

- 중동 및 아프리카

- 거시경제 전망

제11장 경쟁 구도

- 주요 참여 기업의 전략/강점

- 매출 분석

- 시장 점유율 분석

- 기업 평가 매트릭스 : 주요 기업

- 기업 평가 매트릭스 : 신규 기업/중소기업

- 기업 평가와 재무 지표

- 브랜드/제품 비교

- 경쟁 시나리오

제12장 기업 개요

- 주요 기업

- BOSTON SCIENTIFIC CORPORATION

- COLOPLAST GROUP

- INTUITIVE SURGICAL OPERATIONS, INC.

- COOPERCOMPANIES

- JOHNSON & JOHNSON

- GE HEALTHCARE

- INTEGRA LIFESCIENCES CORPORATION

- B. BRAUN SE

- PFM MEDICAL GMBH

- CALDERA MEDICAL

- 기타 기업

- KEGEL8

- MEDGYN PRODUCTS INC.

- BETATECH MEDICAL

- FEG TEXTILTECHNIK FORSCHUNGS-UND ENTWICKLUNGSGESELLSCHAFT MBH

- BIOTEQUE AMERICA INC.

- PERSONAL MEDICAL CORP.

- DIPROMED SRL

- A.M.I. GMBH

- BRAY GROUP

- DIGITIMER LTD

- MEDESIGN I.C. GMBH

- DR. ARABIN GMBH & CO. KG

- FOR.ME.SA.

- COSM MEDICAL

- WILLOW INNOVATIONS, INC.

제13장 부록

KSA 25.11.12The global POP Treatment and Management / Pelvic Organ Prolapse market is projected to reach USD 1.06 billion by 2030 from USD 0.77 billion in 2025, at a CAGR of 6.6% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Product, Treatment, Application, and End User |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

The market is expected to witness high growth due to the high global prevalence of pelvic organ prolapse, rising geriatric female population, growing awareness and early diagnosis, and advancements in minimally invasive and robotic surgical techniques. Complications and recalls associated with vaginal mesh, limited access and affordability in developing markets, underdiagnosis due to social stigma, and the risk of POP products are likely to restrain market growth.

"The hospitals segment of the POP Treatment and Management / Pelvic Organ Prolapse market, by end user, is expected to hold the largest position during the forecast period."

Based on end user, the market is segmented into hospitals, specialty clinics, ambulatory surgery centers (ASCs), and others. In 2024, hospitals and clinics accounted for the largest share of the market. Hospitals benefit from centralized procurement systems, allowing for efficient integration of new POP technologies. Their access to government or institutional funding also facilitates the acquisition of expensive devices, such as robotic surgical systems, which may not be feasible in smaller outpatient facilities. Furthermore, hospitals are often the only facilities equipped to manage intraoperative complications, complex reconstructions, and comorbid conditions in elderly patients-ensuring their continued dominance in the pelvic organ prolapse treatment landscape.

"The surgical segment accounted for the larger market share in the POP Treatment and Management / Pelvic Organ Prolapse market."

The POP Treatment and Management / Pelvic Organ Prolapse market is segmented into surgical and non-surgical. The surgical segment accounted for the larger share of the market in 2024. Surgical intervention is often preferred in cases involving multiple-compartment prolapses or associated conditions like stress urinary incontinence. Moreover, with the growing availability of minimally invasive and robotic-assisted methods, surgical options now offer quicker recovery and reduced postoperative complications, making them more acceptable to both patients and clinicians. Continuous innovation in surgical meshes, biologic grafts, and energy-assisted dissection tools further enhances procedural outcomes. Importantly, surgical treatments are backed by strong clinical guidelines and are often the first-line recommendation in moderate to severe POP, reinforcing their dominant position in the market.

"Asia Pacific is the fastest-growing market for POP Treatment and Management / Pelvic Organ Prolapse."

The global POP Treatment and Management / Pelvic Organ Prolapse market is segmented into five segments, namely, North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Asia Pacific is experiencing rapid population aging, especially in countries like China and Japan, leading to a rising incidence of pelvic organ prolapse disorders among elderly women. Increasing awareness of women's health and growing acceptance of pelvic floor treatments are driving higher diagnosis and treatment rates. Governments across the region are investing in healthcare infrastructure, expanding access to surgical facilities, and supporting the adoption of advanced medical technologies, including robotic-assisted procedures. The rise of medical tourism in countries such as India and South Korea further fuels market growth, offering high-quality care at lower costs. While access disparities and a shortage of trained specialists still exist in rural areas, ongoing investments in healthcare training, digital health platforms, and public awareness campaigns are helping to close these gaps, positioning Asia Pacific as the fastest-growing regional market.

A breakdown of the primary participants referred to for this report is provided below:

- By Company Type: Tier 1: 40%, Tier 2: 30%, and Tier 3: 30%

- By Designation: C Level: 27%, Director Level: 18%, and Others: 55%

- By Region: North America: 51%, Europe: 21%, Asia Pacific: 18%, Latin America: 6%, and Middle East & Africa: 4%

Note 1: Companies are classified into tiers based on their total revenue. As of 2024, Tier 1 = >USD 10.00 billion, Tier 2 = USD 1.00 billion to USD 10.00 billion, and Tier 3 = <USD 1.00 billion.

Note 2: C-level primaries include CEOs, CFOs, COOs, and VPs.

Note 3: Other designations include sales managers, marketing managers, business development managers, product managers, distributors, and suppliers.

The major players operating in the POP Treatment and Management / Pelvic Organ Prolapse market are Boston Scientific Corporation (US), Coloplast Group (Denmark), Intuitive Surgical Operations, Inc. (US), CooperCompanies (US), and Johnson & Johnson (US).

Research Coverage

This report studies the POP Treatment and Management / Pelvic Organ Prolapse market based on product, treatment, application, end user, and region. The report also studies factors (such as drivers, restraints, opportunities, and challenges) affecting market growth and provides details of the competitive landscape for market leaders. Furthermore, the report analyzes micro markets with respect to their individual growth trends. It forecasts the revenue of the market segments with respect to five major regions (and the respective countries in these regions).

Reasons to Buy the Report

The report will enable established firms as well as entrants/smaller firms to gauge the pulse of the market, which, in turn, will help them to garner a larger market share. Firms purchasing the report could use one or a combination of the strategies mentioned below to strengthen their market presence.

This report provides insights into the following pointers:

Analysis of key drivers (High global prevalence of pelvic organ prolapse, rising geriatric female population, growing awareness and early diagnosis, and advancements in minimally invasive and robotic surgical techniques), restraints (complications and recalls associated with vaginal mesh, limited access and affordability in developing market, and underdiagnosis due to social stigma), opportunities (growth opportunities in emerging economies, development of bioengineered and absorbable mesh and digital health and pelvic floor therapy devices), and challenges (inconsistent clinical guidelines and treatment standards, and high recurrence and reoperation rates)

Market Penetration: Comprehensive information on the product portfolios offered by the top players in the POP Treatment and Management / Pelvic Organ Prolapse market

Product Development/Innovation: Detailed insights on the upcoming trends, R&D activities, and product launches in the POP Treatment and Management / Pelvic Organ Prolapse market

Market Development: Comprehensive information on lucrative emerging regions

Market Diversification: Exhaustive information about new products, growing geographies, and recent developments in the POP Treatment and Management / Pelvic Organ Prolapse market

Competitive Assessment: In-depth assessment of market segments, growth strategies, revenue analysis, and products of the leading market players

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 List of secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 List of primary sources

- 2.1.2.2 Key data from primary sources

- 2.1.2.3 Breakdown of primary interviews

- 2.1.2.4 Insights from industry experts

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.1.1 Approach 1: Revenue estimation of key players

- 2.2.1.2 Approach 2: Study of annual reports and investor presentations

- 2.2.1.3 Approach 3: Primary interviews

- 2.2.1.4 Growth forecast

- 2.2.1.5 CAGR projections

- 2.2.2 TOP-DOWN APPROACH

- 2.2.1 BOTTOM-UP APPROACH

- 2.3 DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.4.1 STUDY-RELATED ASSUMPTIONS

- 2.4.2 PARAMETRIC ASSUMPTIONS

- 2.4.3 GROWTH RATE ASSUMPTIONS

- 2.5 RESEARCH LIMITATIONS

- 2.6 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN PELVIC ORGAN PROLAPSE/ PELVIC FLOOR RECONSTRUCTION MARKET

- 4.2 ASIA PACIFIC PELVIC ORGAN PROLAPSE/PELVIC FLOOR RECONSTRUCTION MARKET, BY END USER AND COUNTRY

- 4.3 PELVIC ORGAN PROLAPSE/PELVIC FLOOR RECONSTRUCTION MARKET, BY REGION

- 4.4 PELVIC ORGAN PROLAPSE/PELVIC FLOOR RECONSTRUCTION MARKET, BY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Global prevalence of pelvic organ prolapse

- 5.2.1.2 Rise in female geriatric population

- 5.2.1.3 Improved awareness and early diagnosis

- 5.2.1.4 Advancements in robotic surgical techniques

- 5.2.2 RESTRAINTS

- 5.2.2.1 Complications and recalls associated with transvaginal synthetic mesh

- 5.2.2.2 Limited access in emerging economies

- 5.2.2.3 Underdiagnosis due to social stigma

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Increased investments in pelvic organ prolapse care from emerging economies

- 5.2.3.2 Rapid development of bioengineered and absorbable mesh

- 5.2.3.3 Advent of digital pelvic health solutions

- 5.2.4 CHALLENGES

- 5.2.4.1 Inconsistent clinical guidelines and treatment standards

- 5.2.4.2 High recurrence and reoperation rates

- 5.2.1 DRIVERS

- 5.3 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE TREND, BY PRODUCT

- 5.4.2 AVERAGE SELLING PRICE TREND, BY TREATMENT AND KEY PLAYER

- 5.4.3 AVERAGE SELLING PRICE TREND, BY REGION

- 5.5 VALUE CHAIN ANALYSIS

- 5.6 SUPPLY CHAIN ANALYSIS

- 5.7 ECOSYSTEM ANALYSIS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 TECHNOLOGY ANALYSIS

- 5.9.1 KEY TECHNOLOGIES

- 5.9.1.1 Pelvic mesh implants

- 5.9.1.2 Vaginal pessaries

- 5.9.2 COMPLEMENTARY TECHNOLOGIES

- 5.9.2.1 Wearable and app-based pelvic therapy devices

- 5.9.3 ADJACENT TECHNOLOGIES

- 5.9.3.1 Urinary incontinence devices

- 5.9.1 KEY TECHNOLOGIES

- 5.10 PATENT ANALYSIS

- 5.11 TRADE ANALYSIS

- 5.11.1 IMPORT SCENARIO (HS CODE 901890)

- 5.11.2 EXPORT SCENARIO (HS CODE 901890)

- 5.12 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.13 CASE STUDY ANALYSIS

- 5.13.1 NEGLECTED PESSARY IN PATIENT WITH PELVIC ORGAN PROLAPSE

- 5.13.2 SUCCESSFUL USE OF PESSARY FOR UTERINE PROLAPSE AFTER PELVIC TRAUMA IN YOUNG, NULLIPAROUS FEMALE

- 5.13.3 ROBOTIC AND LAPAROSCOPIC SACROCOLPOPEXY FOR PELVIC ORGAN PROLAPSE

- 5.14 REGULATORY LANDSCAPE

- 5.14.1 REGULATORY ANALYSIS

- 5.14.1.1 North America

- 5.14.1.1.1 US

- 5.14.1.1.2 Canada

- 5.14.1.2 Europe

- 5.14.1.2.1 Germany

- 5.14.1.2.2 UK

- 5.14.1.2.3 France

- 5.14.1.3 Asia Pacific

- 5.14.1.3.1 China

- 5.14.1.3.2 Japan

- 5.14.1.3.3 India

- 5.14.1.4 Latin America

- 5.14.1.5 Middle East

- 5.14.1.1 North America

- 5.14.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.14.1 REGULATORY ANALYSIS

- 5.15 PORTER'S FIVE FORCES ANALYSIS

- 5.15.1 BARGAINING POWER OF SUPPLIERS

- 5.15.2 BARGAINING POWER OF BUYERS

- 5.15.3 THREAT FROM NEW ENTRANTS

- 5.15.4 THREAT FROM SUBSTITUTES

- 5.15.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.16 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.16.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.16.2 BUYING CRITERIA

- 5.17 IMPACT OF AI

- 5.17.1 INTRODUCTION

- 5.17.2 POTENTIAL OF AI IN PELVIC ORGAN PROLAPSE/PELVIC FLOOR RECONSTRUCTION MARKET

- 5.17.3 KEY COMPANIES IMPLEMENTING AI

- 5.17.4 FUTURE OF AI IN PELVIC ORGAN PROLAPSE/PELVIC FLOOR RECONSTRUCTION MARKET

- 5.18 US 2025 TARIFF

- 5.18.1 INTRODUCTION

- 5.18.2 KEY TARIFF RATES

- 5.18.3 PRICE IMPACT ANALYSIS

- 5.18.4 IMPACT ON COUNTRY/REGION

- 5.18.4.1 North America

- 5.18.4.2 Europe

- 5.18.4.3 Asia Pacific

- 5.18.5 IMPACT ON END-USE INDUSTRIES

- 5.18.5.1 Hospitals

6 PELVIC ORGAN PROLAPSE/PELVIC FLOOR RECONSTRUCTION MARKET, BY PRODUCT

- 6.1 INTRODUCTION

- 6.2 SYNTHETIC MESH

- 6.2.1 ADOPTION OF ADVANCED, PATIENT-FOCUSED MESH TECHNOLOGIES

- 6.3 BIOLOGICAL GRAFTS

- 6.3.1 SHIFT TOWARD BIOCOMPATIBLE ALTERNATIVES

- 6.4 SUTURES

- 6.4.1 NEED FOR PRECISION IN PELVIC REPAIRS WITH ABSORBABLE AND ANTIBACTERIAL PRODUCTS

- 6.5 VAGINAL PESSARIES

- 6.5.1 INTRODUCTION OF CUSTOM-FIT, HOME-USE PESSARY SOLUTIONS

- 6.6 PELVIC FLOOR THERAPY DEVICES

- 6.6.1 PATIENT PREFERENCE FOR MANAGING PELVIC FLOOR DISORDERS INDEPENDENTLY

- 6.7 ROBOTIC SURGERY SYSTEMS

- 6.7.1 ELEVATED DEMAND FOR MINIMALLY INVASIVE SOLUTIONS IN COMPLEX PELVIC REPAIRS

- 6.8 DIAGNOSTIC & ASSESSMENT TOOLS

- 6.8.1 ACCURATE DETECTION WITH ADVANCED IMAGING AND SMART DEVICES

7 PELVIC ORGAN PROLAPSE/PELVIC FLOOR RECONSTRUCTION MARKET, BY TREATMENT

- 7.1 INTRODUCTION

- 7.2 SURGICAL

- 7.2.1 COLPOCLEISIS

- 7.2.1.1 Large-scale adoption among older women

- 7.2.2 COLPORRHAPY

- 7.2.2.1 Increased preference for foundational repair techniques

- 7.2.3 SACROCOLPOPEXY

- 7.2.3.1 Reduced postoperative discomfort and quicker recovery

- 7.2.4 SACROHYSTEROPEXY

- 7.2.4.1 Rise in demand for uterine-preserving options for prolapse repair

- 7.2.5 UTEROSACRAL OR SACROSPINOUS LIGAMENT FIXATION

- 7.2.5.1 Surge in native tissue repairs without mesh-based interventions

- 7.2.1 COLPOCLEISIS

- 7.3 NON-SURGICAL

- 7.3.1 VAGINAL PESSARY MANAGEMENT

- 7.3.1.1 Emphasis on early intervention

- 7.3.2 PELVIC FLOOR MUSCLE THERAPY

- 7.3.2.1 Extensive use in early-stage prolapse and postpartum women

- 7.3.1 VAGINAL PESSARY MANAGEMENT

8 PELVIC ORGAN PROLAPSE/PELVIC FLOOR RECONSTRUCTION MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- 8.2 CYSTOCELE

- 8.2.1 WEAKENED PELVIC FLOOR MUSCLES PROMPT DEVELOPMENT

- 8.3 URETHROCELE

- 8.3.1 CHRONIC INCREASE IN INTRA-ABDOMINAL PRESSURE

- 8.4 ENTEROCELE

- 8.4.1 SURGE IN APICAL VAGINAL SUPPORT DEFICIENCY

- 8.5 UTERINE PROLAPSE

- 8.5.1 GROWTH IN PROLAPSE BURDEN

- 8.6 RECTOCELE

- 8.6.1 PREVALENCE OF RECTOVAGINAL SEPTUM DEFICIENCY

9 PELVIC ORGAN PROLAPSE/PELVIC FLOOR RECONSTRUCTION MARKET, BY END USER

- 9.1 INTRODUCTION

- 9.2 HOSPITALS

- 9.2.1 HIGH PATIENT INFLOW AND WIDESPREAD AVAILABILITY OF REIMBURSEMENTS

- 9.3 SPECIALTY CLINICS

- 9.3.1 HEIGHTENED DEMAND FOR TAILORED, NON-INVASIVE, AND ACCESSIBLE CARE

- 9.4 AMBULATORY SURGERY CENTERS

- 9.4.1 COST ADVANTAGES AND FAVORABLE CLINICAL OUTCOMES

- 9.5 OTHER END USERS

10 PELVIC ORGAN PROLAPSE/PELVIC FLOOR RECONSTRUCTION MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 MACROECONOMIC OUTLOOK

- 10.2.2 US

- 10.2.2.1 Rise in female geriatric population to drive market

- 10.2.3 CANADA

- 10.2.3.1 High symptom prevalence and demographic trends to drive market

- 10.3 EUROPE

- 10.3.1 MACROECONOMIC OUTLOOK

- 10.3.2 GERMANY

- 10.3.2.1 Advanced surgical innovations to drive market

- 10.3.3 FRANCE

- 10.3.3.1 Increased clinical focus on pelvic floor disorders and pelvic organ prolapse to drive market

- 10.3.4 UK

- 10.3.4.1 Women's health policy initiatives to drive market

- 10.3.5 ITALY

- 10.3.5.1 Demographic shifts to drive market

- 10.3.6 SPAIN

- 10.3.6.1 Rising popularity of non-surgical interventions to drive market

- 10.3.7 REST OF EUROPE

- 10.4 ASIA PACIFIC

- 10.4.1 MACROECONOMIC OUTLOOK

- 10.4.2 CHINA

- 10.4.2.1 Growing incidence of pelvic organ prolapse to drive market

- 10.4.3 JAPAN

- 10.4.3.1 Evolving healthcare delivery and infrastructure landscape to drive market

- 10.4.4 INDIA

- 10.4.4.1 Booming medical tourism to drive market

- 10.4.5 AUSTRALIA

- 10.4.5.1 Rapid growth of medical manufacturing companies to drive market

- 10.4.6 SOUTH KOREA

- 10.4.6.1 Surge in healthcare spending to drive market

- 10.4.7 REST OF ASIA PACIFIC

- 10.5 LATIN AMERICA

- 10.5.1 MACROECONOMIC OUTLOOK

- 10.5.2 BRAZIL

- 10.5.2.1 Improving healthcare infrastructure to drive market

- 10.5.3 MEXICO

- 10.5.3.1 Expanding healthcare awareness and services to drive market

- 10.5.4 REST OF LATIN AMERICA

- 10.6 MIDDLE EAST & AFRICA

- 10.6.1 MACROECONOMIC OUTLOOK

11 COMPETITIVE LANDSCAPE

- 11.1 INTRODUCTION

- 11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- 11.3 REVENUE ANALYSIS, 2022-2024

- 11.4 MARKET SHARE ANALYSIS, 2024

- 11.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 11.5.1 STARS

- 11.5.2 EMERGING LEADERS

- 11.5.3 PERVASIVE PLAYERS

- 11.5.4 PARTICIPANTS

- 11.5.5 COMPANY FOOTPRINT

- 11.5.5.1 Company footprint

- 11.5.5.2 Region footprint

- 11.5.5.3 Product footprint

- 11.5.5.4 Treatment footprint

- 11.5.5.5 Application footprint

- 11.6 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2024

- 11.6.1 PROGRESSIVE COMPANIES

- 11.6.2 RESPONSIVE COMPANIES

- 11.6.3 DYNAMIC COMPANIES

- 11.6.4 STARTING BLOCKS

- 11.6.5 COMPETITIVE BENCHMARKING

- 11.6.5.1 List of start-ups/SMEs

- 11.6.5.2 Competitive benchmarking of start-ups/SMEs

- 11.7 COMPANY VALUATION AND FINANCIAL METRICS

- 11.8 BRAND/PRODUCT COMPARISON

- 11.9 COMPETITIVE SCENARIO

- 11.9.1 PRODUCT LAUNCHES/APPROVALS

- 11.9.2 DEALS

- 11.9.3 OTHER DEVELOPMENTS

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 BOSTON SCIENTIFIC CORPORATION

- 12.1.1.1 Business overview

- 12.1.1.2 Products offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Deals

- 12.1.1.4 MnM view

- 12.1.1.4.1 Right to win

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses and competitive threats

- 12.1.2 COLOPLAST GROUP

- 12.1.2.1 Business overview

- 12.1.2.2 Products offered

- 12.1.2.3 MnM view

- 12.1.2.3.1 Right to win

- 12.1.2.3.2 Strategic choices

- 12.1.2.3.3 Weaknesses and competitive threats

- 12.1.3 INTUITIVE SURGICAL OPERATIONS, INC.

- 12.1.3.1 Business overview

- 12.1.3.2 Products offered

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Product launches/approvals

- 12.1.3.4 MnM view

- 12.1.3.4.1 Right to win

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses and competitive threats

- 12.1.4 COOPERCOMPANIES

- 12.1.4.1 Business overview

- 12.1.4.2 Products offered

- 12.1.4.3 Recent developments

- 12.1.4.3.1 Deals

- 12.1.4.4 MnM view

- 12.1.4.4.1 Right to win

- 12.1.4.4.2 Strategic choices

- 12.1.4.4.3 Weaknesses and competitive threats

- 12.1.5 JOHNSON & JOHNSON

- 12.1.5.1 Business overview

- 12.1.5.2 Products offered

- 12.1.5.3 Recent developments

- 12.1.5.3.1 Product launches/approvals

- 12.1.5.3.2 Deals

- 12.1.5.3.3 Other developments

- 12.1.5.4 MnM view

- 12.1.5.4.1 Right to win

- 12.1.5.4.2 Strategic choices

- 12.1.5.4.3 Weaknesses and competitive threats

- 12.1.6 GE HEALTHCARE

- 12.1.6.1 Business overview

- 12.1.6.2 Products offered

- 12.1.6.3 Recent developments

- 12.1.6.3.1 Product launches/approvals

- 12.1.6.3.2 Deals

- 12.1.6.3.3 Other developments

- 12.1.7 INTEGRA LIFESCIENCES CORPORATION

- 12.1.7.1 Business overview

- 12.1.7.2 Products offered

- 12.1.8 B. BRAUN SE

- 12.1.8.1 Business overview

- 12.1.8.2 Products offered

- 12.1.8.3 Recent developments

- 12.1.8.3.1 Deals

- 12.1.9 PFM MEDICAL GMBH

- 12.1.9.1 Business overview

- 12.1.9.2 Products offered

- 12.1.10 CALDERA MEDICAL

- 12.1.10.1 Business overview

- 12.1.10.2 Products offered

- 12.1.10.3 Recent developments

- 12.1.10.3.1 Deals

- 12.1.1 BOSTON SCIENTIFIC CORPORATION

- 12.2 OTHER PLAYERS

- 12.2.1 KEGEL8

- 12.2.2 MEDGYN PRODUCTS INC.

- 12.2.3 BETATECH MEDICAL

- 12.2.4 FEG TEXTILTECHNIK FORSCHUNGS- UND ENTWICKLUNGSGESELLSCHAFT MBH

- 12.2.5 BIOTEQUE AMERICA INC.

- 12.2.6 PERSONAL MEDICAL CORP.

- 12.2.7 DIPROMED SRL

- 12.2.8 A.M.I. GMBH

- 12.2.9 BRAY GROUP

- 12.2.10 DIGITIMER LTD

- 12.2.11 MEDESIGN I.C. GMBH

- 12.2.12 DR. ARABIN GMBH & CO. KG

- 12.2.13 FOR.ME.SA.

- 12.2.14 COSM MEDICAL

- 12.2.15 WILLOW INNOVATIONS, INC.

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS